End of cheap deposits has been saved

Perspectives

End of cheap deposits

Implications for banks’ deposit betas, asset growth, and funding

After a long period of cheap deposits, the sharp rise in the federal funds rate from a near-zero base, while boosting net interest margins, is creating distinct challenges for US banks. The uncertain timing of the Federal Reserve’s interest rate “pivot,” coupled with the possibility of a recession, adds additional complexities. This article explores the questions bank leaders should be asking now and presents key considerations for developing a resilient deposit funding and asset growth strategy.

Deposit pricing strategy in the midst of rate hikes

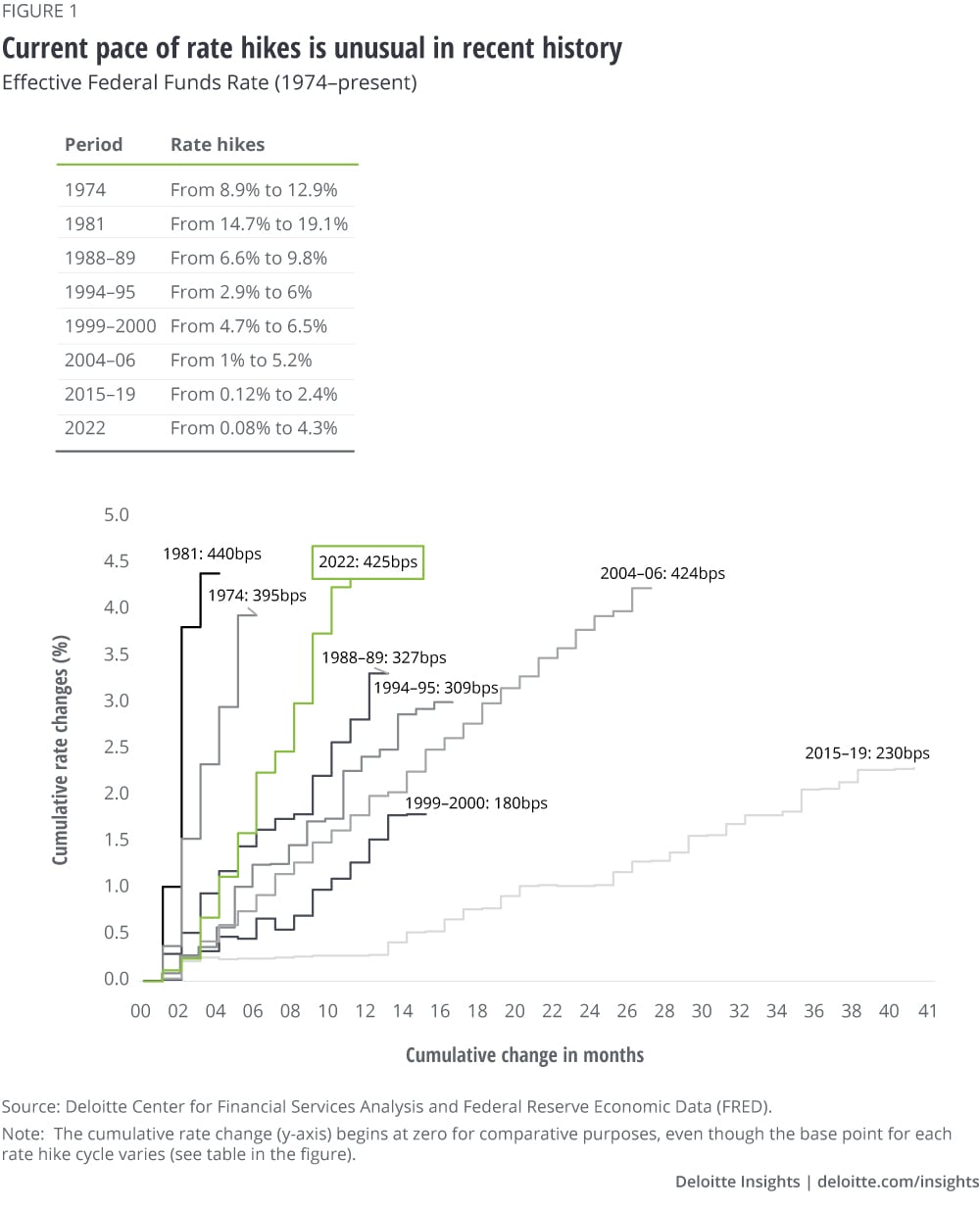

The US economy is experiencing the most aggressive rate hike cycle in recent memory (figure 1). In less than a year, the effective federal funds rate increased about 425 basis points (bps) by the end of December 2022. And there are more increases to come, with the target rate likely reaching above 500 bps in 2023. The sharpness of the rate increases, along with the recent hike cycle starting from a near-zero base, is creating some unique challenges for banks. And because we have lived through a long period of low rates, institutional memory of steep hikes like these is sparse in the banking industry.

Deposit pricing strategy considerations

Recent rate hikes indicate that the era of cheap deposits US banks enjoyed for more than a decade is over. For years leading up to this current rate cycle, banks could attract deposits at close-to-zero rates. For instance, the cost of interest-bearing deposits, including time, money market deposit accounts (MMDAs), and savings deposits, was only 0.26% at the end of 2020, compared to 0.75% at the end of Q3 2022.

Surplus deposits during the pandemic—fueled by more than $2 trillion of inflows—helped to reduce the cost of funding significantly but did not come without some headaches. Deposit growth outpaced loan growth. Deploying these funds in a tough macroeconomic environment with the pandemic still raging and low investment yields presented a challenge, so much so that some banks explored the idea of curtailing deposits from certain customers.

But how quickly the situation has changed. Multiple banks are already advertising higher yields on CDs, money market accounts, and commercial deposits. Even though rate hikes have boosted banks’ net interest margins, the pace of rate increases is beginning to affect customer behavior. Retail and corporate customers alike are demanding higher deposit rates. At the same time, there has also been a steady outflow of deposits.

Uncertainty about the Fed’s rate trajectory and the macroeconomy could make it challenging for banks—large and small—to manage their interest rate risk. This task is becoming more complex with the inversion of the treasury yield curve in recent weeks.

The current scenario raises several questions:

- How can banks manage interest rate risk in the current environment, especially with an inverted yield curve, and the possibility of a “Fed pivot” in 2023?

- How quickly should banks raise deposit rates? Which products (consumer vs. commercial or 5-year CDs vs. 3-month CDs) should get this boost first?

- How to rethink funding: Should banks borrow from the Federal Home Loan Banks (FHLBs), or should they pursue brokered deposits instead of growing deposits organically?

- In the current environment, how can banks sustain a favorable net interest margin? How high can these loan yields go without hurting loan growth and profitability?

Explore these questions and other key considerations below.

As rates rise, banks typically are quick to pass on the higher rates to borrowers. However, deposit rates tend to either remain suppressed or don’t move at the same pace, especially in the initial phases of rate hikes. This is especially likely when banks still have ample liquidity, and the impetus to offer higher yields on deposits is absent.

Such economic calculus makes sense: Why not grow interest income while keeping interest expenses under control? In essence, loan betas are higher than deposit betas in these situations (see endnotes for definitions). Investors also seem to appreciate this dynamic—generally, banks’ stock prices move in tandem with higher rates. For instance, the current rate surge has helped the industry generate $29.6 billion more in net interest income in Q3 2022, compared to Q1 2022.

But going forward, this trend might not persist. In fact, some banks are already forecasting lower or constrained margins over the next several quarters as deposits get costlier and concerns about economic slowdown grow. Complicating this picture are the unrealized losses in many banks’ bond holdings due to higher yields.

Concurrently, banks are contending with increased deposit outflows. The US banking industry saw $573 billion of deposits leave during the second and third quarters of 2022. These withdrawals may suggest that consumers are dipping into their savings. Another possible reason is the redirection of these withdrawals into higher-yielding investment products. Rate shopping by customers is also becoming more endemic.

To counter this threat, banks have begun offering promotions on higher-rate money market products and certificates of deposit—effectively intensifying deposit betas. For example, Capital One recently boosted rates on its Performance 360 Savings account in addition to raising its one-year 360 Certificate of Deposit rate. Similarly, JPMorgan Chase also recently upped its brokered CD rate to more than 4%.

However, these initiatives seem fragmented. Compared to the 142 bps rise in the fed funds rate during Q2 and Q3 2022, the average deposit beta was only 12% compared to 73% in 2019. In addition, there is quite a variation across the industry—among the top 100 US banks, deposit betas ranged from 6% to 82%.

Deposit rates are increasing the most for 3-month CDs (figure 2), suggesting banks are willing to bear the extra cost in the near term. Money market and savings deposit rates are rising the least. Also, brokered deposits are witnessing larger hikes.

Generally, rising rates coincide with positive economic prospects, resulting in a steep yield curve—that is, when yields on short-term securities are higher than yields on long-term securities. In these situations, the Fed is trying to get ahead of inflation. The current pace of rate hikes is atypical, barring the 1970s and 1980s (see figure 1) when interest rates were pushed higher to tame inflation, despite the possible negative impact on economic growth.

But unlike those historical precedents, the current rate-hike cycle started from near-zero rates, resulting in a starker shift in what customers expect in return for their deposits. This sudden, sharp jump from near-zero rates is seemingly having a stronger psychological effect on customers—prompting customers to consider alternative options.

Also, what is quite novel about the current environment is the growing competition from neobanks and fintechs. They have been quite aggressive in raising deposit rates to attract new customers.

Another complication banks face is the decline in the federal funds rate that is expected sometime in 2023. Market consensus is that the Fed will have to drop the fed funds rate after inflation gets under control and/or we enter a recessionary period. In fact, the Fed increased the December rate hike only by 50 bps with the goal of a soft landing in 2023. Such a scenario presents a conundrum for banks: when to reverse higher deposit rates as the Fed hits the brakes. Offering higher fixed-rate deposits could end up backfiring – with banks locking in a steep interest expense into the future.

Higher loan rates and the possibility of recession could also weaken borrowers’ ability to pay back loans, leading to higher delinquencies in almost all asset classes. Banks may be staring at higher loan losses in 2023.

Going forward, deposit mix will prove a key differentiator in managing interest expenses. Historically, core retail deposits have proven more valuable than commercial or high-net-worth consumer deposits as core retail deposits reprice more slowly. As a result, banks with a large proportion of consumer deposits are likely to be less affected. But those banks with a heavier reliance on commercial deposits may find it harder to keep their deposit costs in check.

The other differentiator will be scale. Most large banks should have sufficient liquidity to withstand modest levels of deposit withdrawals and higher interest expenses. They also have a massive customer base—particularly depositors with small accounts who are unlikely to defect. Also, large banks continue to invest in the right set of services and technology to retain customers. Hence, they may not necessarily feel the same pressure as other banks.

The path for regional and midsize banks (those with less than $1 trillion assets), which typically rely heavily on deposits as their key source of funding (figure 3), may be more challenging. Their cost of deposits also remains fairly high.

Similarly, neobanks’ resilience will likely be tested during this period. With incumbents upping their digital game in a rising rate environment, fintechs may have to sacrifice short-term growth for customer acquisition and retention.

Nevertheless, there are some banks that have begun adjusting their funding approach, seeking brokered deposits or wholesale options such as Federal Home Loan Bank advances. For example, First Foundation Inc. added around $1 billion in FHLB advances. Other banks plan to use cash flows from investments to fund loan growth.

So far, there has been a large degree of variation in how banks have responded to these challenges. Regional and midsize banks in particular are scrambling to adjust their funding sources and deposit mix and figure out a way to retain stickier deposits, especially from high-net-worth and commercial customers. Luckily, banks of all sizes have tools at their disposal to manage these ongoing uncertainties.

Although the Treasury groups, the asset-liability committees (ALCOs), and rate committees are working tirelessly on both sides of the balance sheet, there are still likely some additional considerations for banks.

- Ask the right questions. As deposit outflows likely continue, ALCOs and rate committees should redouble their efforts to answer the following questions:

- Should their bank take the lead or be a fast follower?

- How will they manage loan betas vis-à-vis deposit betas?

- How fast should they raise rates, and for which products first?

- Empower frontline employees. Transaction-focused customers may be hard to retain, especially in a competitive rate environment. So banks should consider focusing their energies on proactively reaching out to customers who demonstrate long-term value and solidifying such relationships. In addition to analytically driven outreach efforts, empowering and training frontline staff to make decisions on deposit rates for such customers, based on previously agreed-upon parameters, could pay dividends.

- Focus on holistic solutions. For a long time, rates had minimal input into customer decisions on deposits. Customer experience, brand, relationship, and convenience were the deciding factors. But as customers switch their focus to maximizing yield on their deposits, banks should find a way to broaden the conversation beyond deposits—by offering more holistic products and reiterating attention to additional products and services such as insurance or wealth management offerings. In these conversations, reinforcing the brand will be critical. Brand familiarity can be an important factor when selecting a high-yielding savings account. Integrating convenience through digital and physical channels, personalization, and financial health management into banking experiences can be the key to making deposits sticky.

- Utilize the data and analytical engines, but with a pinch of salt. Banks already use data to analyze customer behavior, but there is likely room to improve such power to predict “at-risk” customers, especially across product silos. Banks should also consider using data to target business customers with the highest share of deposits and tailor relevant solutions. In fact, even smaller banks such as Arbor Bank are reaping benefits from deposit pricing technology to aid customer discussions about the right products and pricing. However, such models only offer solutions based on historical data. Current economic circumstances are unique, so the rejiggering of these models may be required. Banks, especially the smaller institutions, should be proactively modeling a multitude of interest-rate scenarios, such as a pivot in the Fed’s interest rates, the need in the corporate sector to preserve more cash, or a rise in shorter-duration asset classes. But as the complexity of the macroeconomic environment rises, the accuracy of forecasting models may decline. So it is important to reinforce qualitative judgment as well.

- Use M&A as a tool for more long-term focus. In the near future, sticky deposits could find a premium in the M&A market. As banks look at securing cheaper deposits to keep NIMs and loan growth strong, they could look at their peers, and even fintechs, as a more sustainable funding solution. In particular, entities with sticky deposits and that do not have strong lending platforms could be attractive targets in the next set of M&A activity.

This is a critical time for US banks; however, taking a big-picture view, it is also a time to reassess the funding model, the customer segments to target, and product and pricing innovation across the portfolio. The current situation is an opportunity for banks to reengage with customers and reinforce purposeful relationships. How banks transform these moments into sustainable growth could help define their future success. This will require strong, clear, and consistent communications about deposit and loan repricing with customers, investors, and boards of directors, as well as regulators. As banks reassess their funding programs, one should expect greater attention and oversight from regulators on deposit strategies and their implications for banks’ liquidity.

Get in touch

Kristin Korzekwa

Consulting Managing Director | Deloitte Consulting LLP

Recommendations

The future of midsize banks

A new playbook for supercharging growth

2025 banking and capital markets M&A outlook

Explore the trends reshaping banking M&A