2025 investment management outlook

Navigating fast-paced change, elevated risk, and outsized opportunity

Krissy Davis

Julia Cloud

Karl Ehrsam

Snehal Waghulde

Doug Dannemiller

Key takeaways

- With increasing investor appetite for low-cost funds, the low-expense ratio environment may be here to stay with active management finding a home inside the exchange-traded fund (ETF) wrapper.

- Expanding the product lineup into alternative investment offerings such as private credit and evergreen or hybrid fund structures, as well as investing in technologies that integrate artificial intelligence (AI) into sales and distribution processes may be among some of the most successful revenue-enhancing strategies.

- In 2024, AI technologies promised to be one of the most disruptive forces in the investment management sector. Now, it seems that promise has likely surpassed expectations. While the opportunity buzz is growing, many organizations may be left to determine how to effectively harness AI solutions at scale without prior models to guide them.

- Firms likely face some of their biggest risks in areas such as digital transformation, technological advancements, and cybersecurity. Specific product and regulatory developments are also bringing important risk elements to the investment management industry in the form of direct indexing, mutual fund to ETF conversions, convergence of traditional and alternative asset classes, and sustainability-themed investment products.

“Fortune favors the bold,” wrote Virgil in the Aeneid—a phrase that has been embraced through time to modern history.1 In 2025, this phrase describes investment management firms that may be facing the steepest risk/reward curve in decades. In last year’s outlook, we identified generative AI as an emerging technology that firms were testing and exploring. In 2025, many firms will likely pass the exploration stage and may begin to change the way they do business with new technologies.

The new technologies available to investment management firms may lead to stark contrasts in results between the firms that deploy them quickly and effectively, compared to those that lag or act less boldly. This outlook for 2025 examines some key questions that investment management firms may face for the coming year in the form of revenue, efficiency, and overall risk management. But first, let’s review the industry landscape to better understand why those pursuing bold actions could separate themselves from the laggards in 2025.

Table of contents

- Do recent performance trends herald changes in the investment management industry structure?

- Which product and distribution innovations will likely drive AUM growth in the coming year?

- Are investment management firms ready to move AI deployments from concept to reality?

- How can firms manage mounting risks associated with digital transformation and product mix changes?

- 2025 is likely to be a period of rapid change

Do recent performance trends herald changes in the investment management industry structure?

The industry had a mixed year where flows into alternative investments slowed and outflows from mutual funds continued as ETFs gained momentum. Firms worked to navigate a shifting industry environment characterized by evolving investor preferences, shrinking profit margins, sustained high interest rates, and escalating regulatory demands.

Traditional investment managers bracing for a low-expense ratio environment

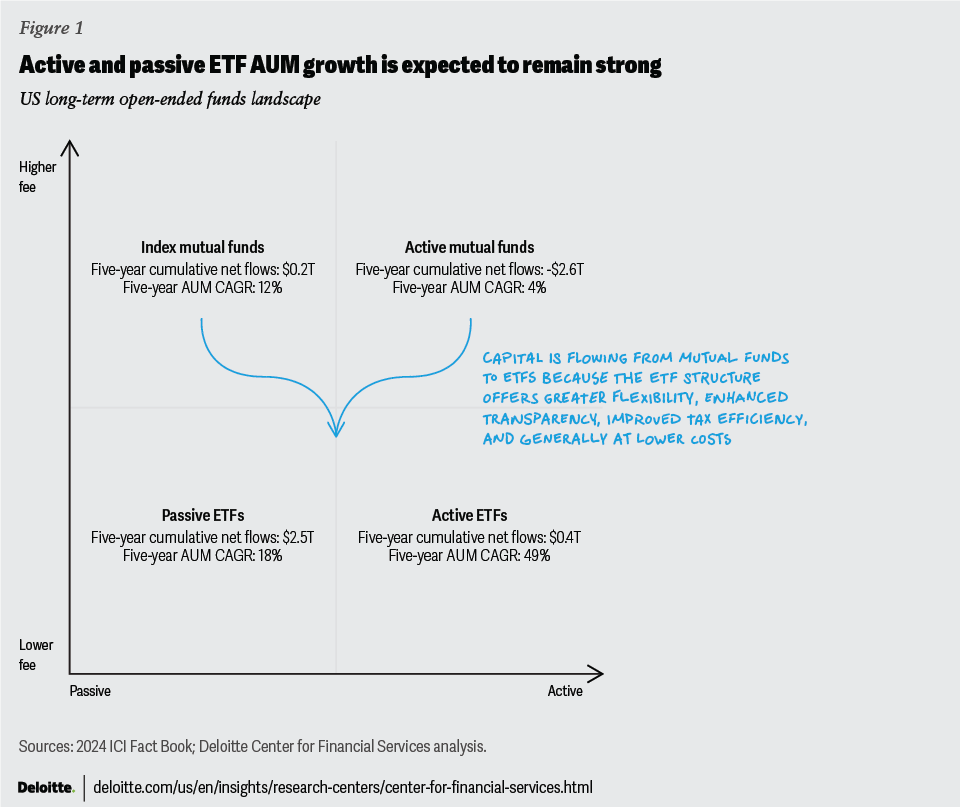

While traditional investment managers offer a variety of products and services, such as open-ended funds, closed-ended funds, separately managed accounts, and wealth management services, open-ended funds are often their primary source of revenue. The assets under management (AUM) for open-ended funds globally increased significantly last year, supported primarily by rising market valuations. The trend was consistent across North American and European open-ended fund markets. In the Asia-Pacific region, the story was slightly different as fund flows drove much of the rise in AUM. The United States dominated the open-ended funds segment, accounting for about half of global AUM. Although the US market experienced positive fund flows, money market funds and ETFs attracted most of the net fund inflows while long-term mutual funds experienced net outflows, driven primarily by active mutual funds (figure 1).2

In the United States, active mutual funds continued their streak of net cash outflows last year, marking a decade of continuous outflows.3 The intensity of outflows has also increased, with more than US$1.8 trillion of net fund outflows in this asset sub-category in the last two years, compared to about US$2.1 trillion cumulative net outflows between 2014 and 2021.4 The underperformance of a majority of active equity mutual funds compared to their benchmarks also influenced these outflows.5 On the other hand, index mutual funds continued to witness net cash inflow, but the volume of inflows has declined consistently over the last six years. Last year, net inflows to index mutual funds were a small portion of what they were in 2017. One of the primary reasons for this decline in fund flows to long-term mutual funds is the rise of low-cost ETFs, which now account for about a quarter of open-ended funds AUM. Collective investment trusts are also capturing market share from mutual funds and accounted for about US$4.6 trillion AUM overall in 2022 with a concentration in target date funds in retirement plans.6

ETFs have continued to attract investors and cumulatively received a net inflow of more than US$3.0 trillion in the last five years in the United States.7 Investor preference for low-cost funds is evident from the fact that across mutual funds and ETFs, the majority of AUM is invested in funds with lower expense ratios.8 This has also helped ETFs gain market share from mutual funds since the expense ratio for active equity and bond ETFs in 2023 has been on average 22 and 11 basis points lower than actively managed equity and bond mutual funds, respectively.9 Other features of investing in ETFs such as transparency, flexibility, and tax efficiency also helped garner additional flows. Some of the net fund flows into ETFs came from converting mutual funds to ETFs.10 The growing preference for ETFs is evident as some investment managers are now seeking approval to introduce ETFs as a share class for their existing index mutual funds.11

While passive ETFs continue to attract the lion’s share of net inflows within ETFs, the rise of passive investing may lead to concentration risk in the global equity markets.12 The rise of index portfolios may fuel opportunities for active equity management since active managers can predict the investment behaviors of the passive managers. This dynamic could be a leading indicator for passive investing reaching its peak, as active management is now accessible through the investor-friendly low-cost ETF structure. Actively managed ETFs are capturing a growing portion of the total ETF net inflows, albeit from a smaller base. Flows to actively managed ETFs accounted for 23% of all ETF net inflows compared to just 9% five years ago.13 Given the investor appetite for low-cost funds, the low-expense ratio environment could be here to stay with active management finding a home inside the ETF wrapper.

Alternative assets going through a rough patch

On the alternatives side, private capital performance was mediocre in 2023, whereas hedge funds exceeded their long-term average performance. Geopolitical uncertainty and shifting investor preferences toward more liquid and transparent investment vehicles likely resulted in continued net fund outflows from hedge funds.14 Private capital, on the other hand, experienced deceleration in fundraising. With these lackluster results and sluggish fundraising, the AUM for private capital remained unchanged, while hedge funds saw a slight increase in 2023, as market action surpassed outflows.

Smaller hedge funds performed slightly better on average than their larger peers.15 One probable reason for this performance advantage could be that their smaller size offers them an edge in security selection over larger competitors.16 There was some dispersion in larger hedge fund returns also. Notably, firms such as Citadel, Point72 Asset Management, and Millennium provided consistently better returns over the last five years.17 Some of the reasons for these consistent returns may be robust risk management discipline, data analytics, and the ability to attract highly skilled talent powered by a pass-through expense approach.18 Pass-through expense is a fee structure in which investors pay for most of the firm’s operating expenses, including spending on technology and talent, in addition to the traditional management fee.19 Expenses under this fee structure can go as high as 7% compared to the traditional hedge fund fees of 1% to 2%.20 The approach can allow the funds to compete for portfolio managers and equip them with the latest technologies to run a variety of trading strategies across markets. This approach may work well for firms that can provide consistent outperformance, which can offset the higher operating fee structure.

Overall, private capital has generated handsome returns for its investors over the past decade, although there was a performance dip in 2023, likely due to muted public market valuations leading to reduced exit activity and lower distributions. These conditions dampened the fundraising environment in 2023 after reaching record levels in the preceding two years.21 Investment activity is expected to rise in the next year or two as the pent-up deal flows likely occur due to substantial amounts of dry powder. Furthermore, the recent reductions in interest rates by the Bank of England and European Central Bank, along with the anticipated decreases by the US Federal Reserve, are expected to foster a more conducive atmosphere for fundraising and investment activity over the next year.22

Investment and wealth management firms continue to consolidate, albeit at a slower pace

The number of merger and acquisitions (M&A) transactions within the investment management and wealth management sectors experienced a downturn in 2023 following two successive years of growth. Globally, deal counts for investment and wealth management firms decreased 10% from 639 deals in 2022 to 576 deals in 2023.23 The declining trend in mergers and acquisitions gained more momentum stepping into 2024 as there was a 27% decline in deal count to 234 in the first half of 2024 compared to 321 in the same period last year.24 These deal count numbers are more comparable to pre-COVID–19 deal numbers when the interest rates were not near-zero levels. The wealth management sector continues to see a high volume of transactions, primarily driven by two key factors: the focus on succession planning within acquired firms and enthusiasm for product diversification to potentially offset lower growth in private capital.25 On the alternative asset side, building and diversifying capabilities in high-margin products could drive M&A activity in this space. BlackRock’s acquisition of Global Infrastructure Partners and TPG’s acquisition of Angelo Gordon are examples of these types of acquisitions.26 The ongoing M&A trend of private equity firms partnering with insurance companies may slow down as regulators express concerns about the potential for systemic risk arising from these deals.27

In the face of heightened competition and shifting economic conditions, investment management firms could look to innovate and explore fresh revenue-generation strategies. In the next section, strong revenue opportunities for investment management firms in 2025 are listed.

Which product and distribution innovations will likely drive AUM growth in the coming year?

Despite growing assets under management in 2023, both revenue growth and profit margin expansion remain elusive for the investment management industry.28 This dynamic appears to be driving a noticeable shift in how investment management leaders are approaching their firms’ product strategy. Having a diverse product mix is now often front and center for revenue growth, and implementing an effective distribution strategy alongside it will likely increase the chances for success.29 In 2025, expanding the product lineup into alternative investment offerings such as private credit and evergreen or hybrid fund structures, as well as investing in technologies that integrate AI into sales and distribution processes, is expected to be among the most successful revenue-enhancing strategies. Firms that execute these strategies in 2025 with excellence could experience differentiated results from the laggards.

Offer a new asset class to help drive AUM growth in 2025

Globally, private credit assets continue to experience double-digit annual growth, reaching more than US$2.1 trillion in 2023.30 There is little to suggest that a slowdown in growth is on the horizon. In fact, some investment management firms are exploring partnerships with banks that were once deemed unlikely to expand their reach into the private credit arena. Tie-ups such as those between Wells Fargo and Centerbridge Partners, and Barclays and AGL Credit Management, are redefining these relationships and providing mutual benefits—investment managers are gaining exclusive access to the banks’ respective deal flows, and the banks are, as a result, getting additional capital for their clients through investment managers.31 Strategic alliances such as these may provide investment managers who lack a significant private credit footprint with a potential opportunity to grab a foothold in this growing asset class more quickly than a go-it-alone strategy would afford. It’s expected that these alliances will represent a greater percentage of private credit AUM growth in 2025 as new entrants to the asset class look to build fundraising momentum from the start.

Another factor in the expected growth of private credit and other private capital assets is the use of evergreen fund structures such as interval funds and business development companies (BDCs) to attract flows from non-institutional investors. In 2023, assets that fall under the evergreen fund umbrella globally grew to a record US$350 billion as the number of funds reached 520, double the amount from five years ago.32 The growth in the number of funds also meant that evergreen structures have become more diverse.33 Recently, several private equity fund managers such as Apollo and Blackstone have utilized 3(c)(7) funds, which are non-registered and open-ended in the United States.34 While in the European Union, the European long-term investment fund (ELTIF) structure under the revised regime has been recently used by several firms.35 While these funds are only offered to accredited investors in the United States or the equivalent in the European Union and are intended as long-term investment vehicles, the structures tend to offer greater opportunity for liquidity through monthly subscriptions or redemptions.36 Securities and Exchange Commission (SEC)-registered private equity tender offer funds are also growing in popularity in part due to their low investment minimums and simplified tax reporting via a 1099 form as opposed to a more complicated Schedule K-1.37 These registered fund structures have the additional appeal of being available across many wealth distribution platforms in the United States.38 In addition to registered tender offer funds, investment managers are increasingly offering unlisted BDCs through both traditional wire house and registered investment adviser distribution channels as another SEC-registered structure to provide alternative investment exposure to accredited investors.39 While expanding distribution through wealth platforms can increase the opportunity for these funds to be used in client portfolios, educating clients about the potential benefits of this asset class may be just as important.

Financial advisers often play an integral role in educating investors about how these structures work and potential diversification benefits. However, some advisers believe that investment managers do not provide them with sufficient materials to educate clients about alternative investments.40 Both traditional and alternative investment managers are fulfilling this need by either launching their own platforms or partnering with third-party research platforms to provide financial advisers with educational resources.41 Over the coming year, investment management firms that expand into private credit offerings, particularly across retail distribution platforms, and make client education an integral part of their product strategy may achieve greater success.

Leverage AI to expand sales and distribution opportunities

While integrating AI for process efficiency improvements may be common across the investment management industry, examining how AI may be deployed to drive sales and distribution is expected to gain traction in 2025. Investment managers such as Amundi, Wealthfront, and Vanguard are creating in-house AI-powered platforms to support customized portfolio recommendations based on specific customer risk tolerances.42 These AI-powered tools are designed to analyze data from client interactions to gain real-time insights at both macro and micro levels of investment managers’ client base.43 Equipped with this level of detail about the current needs of their clients, sales teams can more effectively tailor specific fund recommendations. Firms such as Invesco and WisdomTree are using this generative AI approach to develop personalized marketing strategies for existing and prospective clients.44 About 60% of surveyed investment management firms are using AI in their data-related distribution undertakings to a modest degree, but just 11% describe the usage as “heavy,” despite an increase in use cases.45 In 2025, usage of AI in distribution initiatives is expected to expand at both “modest” and “heavy” degrees, as the potential benefits to revenue growth become clearer for the investment management industry.

Are investment management firms ready to move AI deployments from concept to reality?

In 2024, AI technologies were anticipated to be one of the most disruptive forces in the investment management sector. Now, it seems that promise has surpassed expectations. While the opportunity buzz is growing, many organizations may be left to determine how to effectively harness AI solutions at scale without prior models to guide them. Some investment managers may be finding that AI innovations require a robust data posture for both internal and external data along with strong data governance and control mechanisms. Additionally, AI innovations can also benefit from organizational nimbleness and adaptability in thought, especially when it comes to talent. Now, perhaps more critically than before, firms specializing in investment management should be careful and vigilant when integrating AI technologies. Those that lag in realizing efficiency or identifying ways to drive innovation may find it challenging to remain competitive in 2025, because efficiency in investment management operations is not just a margin enhancer but could also have potential to drive alpha. Considerable transformation is still looming on the horizon.

In investment management, the skill sets of natural language processing (NLP) technologies replicate the functions and responsibilities of a securities analyst in pre- and post-trade operations. NLP can offer two advantages: It can reach more data sources and can process derived data in a fraction of the time required by its human counterparts.46 If NLP is likened to the role of the securities analyst, natural language generation (NLG) can be likened to the role of a senior analyst. NLG technologies take data prepared by NLP and further refine it into a humanlike narrative, summarizing and customizing to provide language and purpose to the data.47 Gen AI can be thought of as NLP/G’s creative younger sibling, a technology that can process human queries to create new synthetic content—from text, to imagery, video, and melody.48 Imagine the impact the output generated by the AI model could have when it is fed inputs from a variety of sources—current news, financial statements, earnings call transcripts, historical pricing data, and proprietary valuation models. The output has the potential to revolutionize the role of securities analysts and portfolio managers.

AI technologies such as NLP/G and gen AI are already acting as driving forces of competitive advantage in the investment management industry. Based on the findings of a recent survey of C-suite executives, the Deloitte AI Institute reported that gen AI is expected to enhance value derived from both technology- and human-related skills. Within the investment management industry, the top three technology-related skills expected to increase in value include data analysis (76%), information research (74%), and application development (69%).49 Most investment management respondents reported that gen AI will enhance the value of the following human-centered skills: critical thinking and problem-solving (64%), creativity (55%), ability to work in teams (55%), and flexibility/resilience (55%).50 In the same survey, 57% of respondents expect gen AI to improve efficiency and productivity, 38% anticipate benefits to existing products and services, and 38% expect it to help detect fraud and mitigate risk.51 The impacts of AI deployment in the investment management sector are widespread and profound.52

The gen AI boom has prompted some firms in the investment management industry to experiment with the technology (see “Some investment managers are piloting gen AI solutions”). Some firms are using AI to eliminate historically time-consuming processes such as trade reconciliations, security research, and portfolio compliance monitoring.53 Toronto-based Boosted.ai recently launched Boosted Insights 3.0, a software capable of reviewing portfolios for departures from investment mandates, which is usually a time-consuming process.54 Additionally, investment operations are experiencing benefits, particularly in the investment research process where AI technologies are supporting more informed investment decisions. LG and Qraft Technologies employ a proprietary AI stock picking tool for their LQAI ETF that was launched in November 2023.55 The tool is designed to complement its portfolio manager by selecting investments and producing monthly reports with explanations of the investment decisions made.56 In 2025, the efficiencies gained through AI deployment in customer experience (CX) and investment operations are anticipated to fuel cost savings and enable firms to compete on price (an important investment selection criteria), while enhancing CX.

Some investment managers are piloting gen AI solutions

Investment managers are developing gen AI solutions aimed at boosting employee productivity and customer delight with quick response times and large data-crunching abilities.

Here are some examples:

- Voya Investment Management has developed AI-enabled virtual analysts to complement its human talent in providing stock recommendations.57

- Alternative asset manager Legalist Inc. has developed the “Truffle Sniffer” algorithm to search for lawsuits to fund.58

- JPMorgan Asset Management is developing the “Moneyball” tool to analyze portfolio manager and market behavior and mitigate biases.59

- LTX launched BondGPT+, an enterprise solution, to receive quick answers to complex bond questions.60

- BNP Paribas has partnered with Mistral AI to develop use cases across customer support, sales, and IT.61

- Goldman Sachs is rolling out its first gen AI tool to write code, which is expected to increase developer efficiency by 20%.62

- The AI @ Morgan Stanley Debrief tool is expected to allow financial advisers to capture and aggregate insights from client conversations to generate personalized recommendations and outline the next steps.63

Success factors for AI-driven efficiency

Although AI can offer considerable advantages, its implementation in investment management circles has not yet reached a mature stage. For investment managers, 2025 presents new challenges as firms will likely need to scale AI to realize the full value and disruptive power of its technologies.64 Additionally, early identification and transparency around the costs to invest in AI will likely be top of mind for investors.65

Here are some considerations for investment management firms as they aim to scale AI effectively.

Focus on practicality instead of hype

The rapid pace at which AI technologies are evolving makes it challenging for organizations to chart a course to effective scaling. Firms that begin implementation on too many use cases without adequate consideration and prioritization of risks, tangible returns, regulatory suitability, and ease of implementation may not achieve optimal results.66 Leading practices call for investment management firms to look at what AI strategies are practical and feasible for them and test them out through small pilots.

Deploy integrated risk management approaches

When exploring AI projects with a broader scope, investment management leaders should conduct a companywide risk management program that seeks to identify new and existing risks and potential governance and control mechanisms for each, as a starting point.67 Risk assessments will likely require constant revisiting to account for the continuing unknowns of AI technology. Providing AI models with accurate and impartial data is expected to mitigate some of these risks. Considering that AI technology is still in its nascent phase, human supervision should be leveraged to help manage risks. Moreover, there is little clarity on what kind of domestic or international laws might apply to AI and who would be responsible for implementing and governing such rules.68

Incorporate gen AI into existing initiatives

Another component of effective scaling includes the integration of gen AI use cases that can support and augment existing initiatives in the organization.69 Executives at State Street Alpha warn that outdated databases, spreadsheets, and isolated data stores are significant barriers to harnessing AI’s advantages, an issue that State Street Alpha addresses directly.70 Therefore, firms will likely benefit from a bottom-up assessment of their current technological landscape. TIAA achieved this most recently by launching a gen AI platform designed to support multiple projects, including the development of income education and services, investment research, talent experience, website functionality, and cybersecurity.71 In each of these examples, integrating gen AI with legacy operational transformation efforts has led to positive outcomes.

Establish a gen AI center of excellence to build trust

Consistent with our predictions in 2024, investment managers continue to face a need to upskill and reskill their workers coupled with the requirement to look for different talent than in the past. Establishing a gen AI center of excellence can be a potential solution for this problem. It can help, for example, bring together employees with different AI skill sets and drive implementation ownership across business divisions. Firms should work to create an environment in which employees see value in meaningful scaling of the AI process and feel empowered to be a part of it.

But that’s not all. When it comes to nurturing trust in the organization’s AI scaling process, there’s more that investment management firms should consider. Centralized testing of AI internally prior to exposure to external parties and investors can be critical in the face of significant governance and regulatory headwinds.72 A gen AI center of excellence can develop and maintain written policies and procedures that ensure deployment of new technologies meets potential regulatory requirements and builds stakeholder trust.

How can firms manage mounting risks associated with digital transformation and product mix changes?

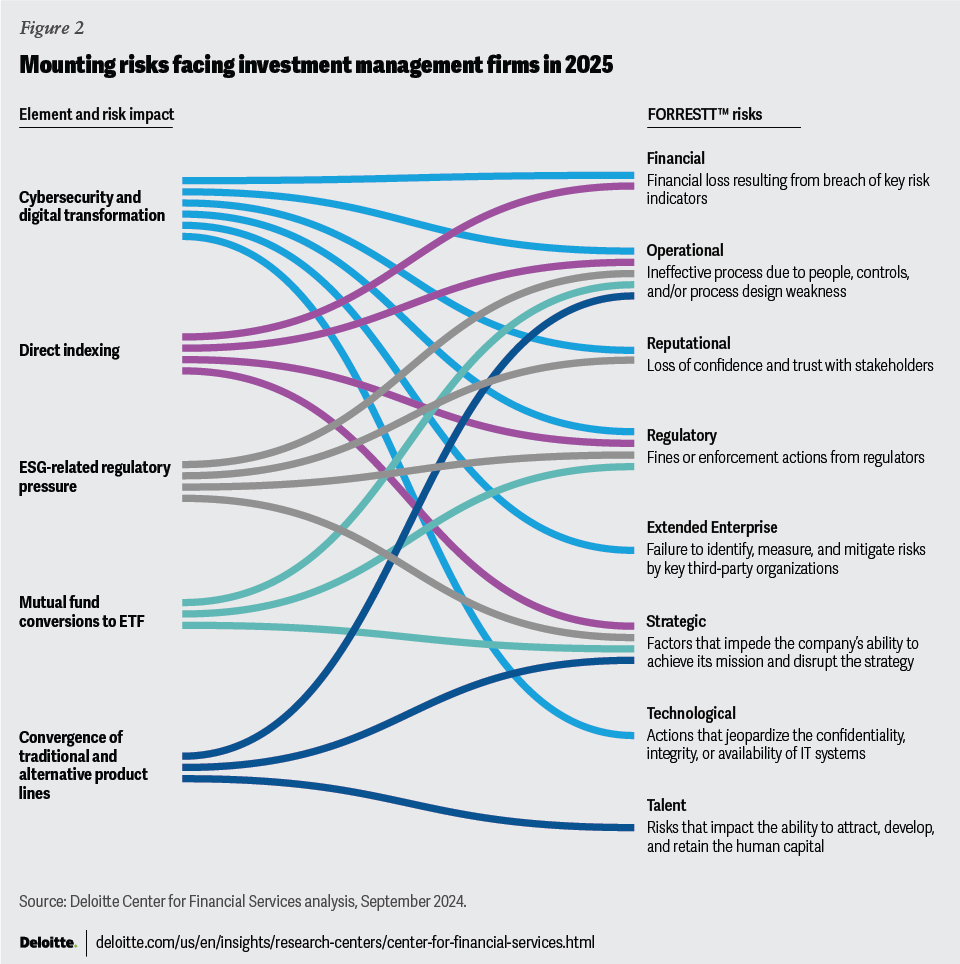

In 2025, firms may face significant risks in areas such as digital transformation, technological advancements, and cybersecurity. Specific product and regulatory developments are also bringing important risk elements to the investment management industry in the form of direct indexing, mutual fund to ETF conversions, convergence of traditional and alternative asset classes, and sustainability-themed products. The FORRESTT™ framework (figure 2) can help leaders identify, understand, and mitigate these risks. Let’s take a look at these risks in detail.

Cybersecurity and digital transformation risk

Cybersecurity breaches and ransomware incidents are rising worldwide. The financial services industry (FSI) is the second-most impacted industry globally.73 The average cost of each breach in FSI is touching an all-time high of US$5.9 million.74 While AI innovations are bolstering cybersecurity, they are simultaneously being misused by cybercriminals. Some of the AI-enabled threats include:75

- AI deepfakes

- Adversarial AI tools like WormGPT and FraudGPT (also called AI-as-a-Service)

- Ransomware-as-a-Service

- Identity fraud

- Vishing (Voice Cloning-as-a-Service, or VCaaS)

Investment management firms are mitigating cyber risks by updating their security policies, training staff to identify possible AI-enabled cyber frauds, and modernizing systems to counter new threats.

Using AI and modernizing threat detection technology have allowed firms to respond faster and lower the cost of data breaches.76 D Commerce Bank drove digital transformation with AI-driven cybersecurity solutions and experienced a 50% drop in security alerts.77 As part of its digital transformation journey, Mercury Financial partnered with a leading cybersecurity vendor to work toward a goal of zero downtime due to ransomware or malware attacks.78

Investment managers are taking action to tackle cybersecurity threats such as AI model validation, model maintenance, data control, data quality, and retention issues.79 Internally, firms are focusing on role-specific upskilling and bringing different AI risk governance areas under a single AI leader.80 As AI continues to play a critical role, investment management firms such as AllianceBernstein and Morgan Stanley have created chief AI officer positions.81 This new position is being added to firms across industry to help manage AI and gen AI deployment, with a focus on improving efficiency and managing AI-related risks. These risks include those that come with AI deployed internally and AI deployed across the extended enterprise.

Evolving industry landscape and associated risks

In 2025, risks are expected to emerge through multiple sources. Growth in direct indexing solutions and separately managed accounts (SMAs) bring both strategic and financial risks to many investment management firms.82 By 2026, the AUM of direct indexing and SMA platforms is expected to reach US$825 billion and US$2.5 trillion, respectively.83 Utilization of these platforms has the potential to enable wealth managers to disintermediate investment managers. At a minimum, they could have the tendency to commoditize the pricing of portfolio management services, representing both strategic and financial risks in the FORRESTT framework.

The recent flurry of mergers and acquisitions serves to help manage this disintermediation risk. Investment management firms such as Morgan Stanley and BlackRock have acquired firms such as Parametric and Aperio to bolster their SMA capabilities.84 These acquisitions are intended to help with the vertical extension of product and service lines potentially increasing revenues and satisfying customer preferences while mitigating both strategic and financial risk.

Customer preferences and regulatory change are contributing to firms transforming their product lines from mutual funds to ETFs. Mutual fund-to-ETF conversions, initiated by Guinness Atkinson in March 2021, have seen more than US$60 billion in assets make the transition, including conversions by investment firms such as JPMorgan, Franklin Templeton, Fidelity, and Dimensional.85 Some of the potential benefits of ETF conversions over ETF launches are the ability to retain fund performance track record and brand recognition while lowering operational costs and enhancing tax efficiency for existing investors.86 There is operational risk associated with these conversions that some firms have been able to manage. Some of these operational risks include managing fractional shares, brokerage account requirements, and distribution channel differences such as corporate retirement plans (for example, 401[k]).87

Investment managers are spending more on alternative data as they reach out to technology partners to combine and analyze alternative data to fulfill their core mission to generate alpha.88 A staggering 98% of investment professionals surveyed say they recognize the critical role of alternative data in generating alpha.89 However, the digital transformation effort to harness this data is not a siloed endeavor. It often requires stakeholder collaboration across the organization to integrate diverse alternative data sets effectively.90 The successful implementation of a data strategy could hinge not just on acquiring the right data but on curating and synthesizing it to distill actionable insights.91 These projects carry risks associated with change management as well as extended enterprise and regulatory risk. The journey to incorporating alternative data is itself a strategic risk as those that fall behind are likely to be at an information disadvantage in the marketplace.

As traditional investment managers venture into the realm of private assets, they find themselves in direct competition with seasoned private equity firms.92 Firms such as Fidelity International and Manulife Investment Management are forming strategic partnerships and acquiring alternative investment management firms.93 However, the integration of traditional and alternative investment management poses its own set of challenges. Traditional investment managers typically operate under compensation structures, investment horizons, and decision-making processes that may vary from their alternative counterparts.94 For instance, traditional investment managers often focus on relatively liquid assets and may have compensation tied directly to short-term performance metrics. In contrast, alternative investment managers may take a longer-term perspective—one where the compensation structures reward long-term value creation and are often tied to the eventual success of the investment. Post-merger integration and resulting economies of scale may prove to be difficult to achieve due to the potentially incompatible cultures. Tempering financial expectations may prove to be the prudent path for these alternative and traditional manager mergers.

Environmental, social, and governance (ESG) factors pose a strategic risk to investment managers due to regulatory and client reporting uncertainties. Investment managers are facing significant challenges in ensuring data reliability and dealing with the uncertainties in measuring the outcomes of sustainability initiatives for their regulatory and client reporting.95 In order to help manage risk associated with data reliability, investment management firms can incorporate a detailed bottom-up proprietary analysis to support their internal ESG ratings. Investment managers are also likely to trust audited corporate disclosures along with their internal sustainability metrics.96 On the regulatory front, having detailed policies, procedures, and governance models that ensure compliance can potentially manage some of the regulatory and reputational risks with funds marketed with a sustainability-related mandate.

2025 is likely to be a period of rapid change

While growing revenue, streamlining processes, and managing risks is expected to be a priority for management teams in 2025, the opportunities and pitfalls could present outsized risks and rewards for investment management firms. Firms that effectively integrate emerging technologies like generative AI have the potential to achieve significant rewards due to the substantial enhancements these technologies bring to the current environment. Firms that succeed will raise expectations for all industry participants. Firms that don’t keep up with these evolving expectations could risk falling out of favor, as the leaders accelerate away. A once-in-a-generation opportunity to differentiate may emerge in 2025.

{kind=link}

{kind=link}