2024 investment management outlook

Winning in tomorrow’s world with the lessons of today

Krissy Davis

Julia Cloud

Jeffrey B. Stakel

Doug Dannemiller

Key takeaways

- Firms will likely have to invest in technology and associated controls even amid weak performance and margin pressures, failing which they will likely fall short of client expectations and internal efficiency goals.

- Theme-driven portfolio construction is emerging as a vector for product development even though the age-old classification of investment strategies into scales of growth versus value, large cap versus small cap, and by industry sector are not going away.

- Although investment performance is an important factor that can help drive customer satisfaction, customers’ expectations have generally grown in terms of personalization and timeliness of interactions.

- While generative AI can transform the timelines and clarity of customer interactions, its successful implementation will likely require close collaboration across the organization, including front, back and middle office, finance, information technology, and risk management.

- As quantum computing technologies are increasingly being considered to help generate revenue and delight customers, firm leaders may need to play defense first owing to the quantum-related cybersecurity threats that are currently developing.

- Navigating organizational model changes can become easier when the organization is aligned with a strong sense of purpose. When survey respondents agree or strongly agree that their institutions workforce is aligned to the firm’s sense of purpose, they are also more likely to report that their institution’s culture became much stronger, which often leads to efficiency, productivity, and collaboration improvements.

Learn more

New forces drive industry change in 2024

Investment management companies are now facing new threats and uncommon opportunities in the postpandemic business environment. Even though some asset classes performed better than others, overall industry performance across asset classes remained subdued, driven by various economic and industry pressures. The difficult operating environment is causing many firms to reconsider larger M&A deals in favor of smaller, more tactical ones. In addition, firms also seem more selective to transformative projects with an eye towards shorter duration projects that balance cost cutting with innovation.

Product innovation and impactful customer experience are likely to remain the leading drivers of growth. Fresh challenges are impacting talent models, company purpose, workplace settings, and environmental, social & governance (ESG) mandates. Furthermore, while firms were busy implementing disrupting technologies over the last few years, governance has not kept pace with the technology implementation. Many firms will likely have to turn their attention to establishing governance and controls to efficiently manage risks in the highly regulated industry landscape.

Let’s take a look at these factors of change through the lens of what we call a “virtuous cycle” and a backdrop of industry performance and M&A activity—keeping in mind what industry leaders can do to empower accurate decision-making, effective risk management, and reliable performance outcomes (figure 1).

Industry performance

Competition for assets intensifies

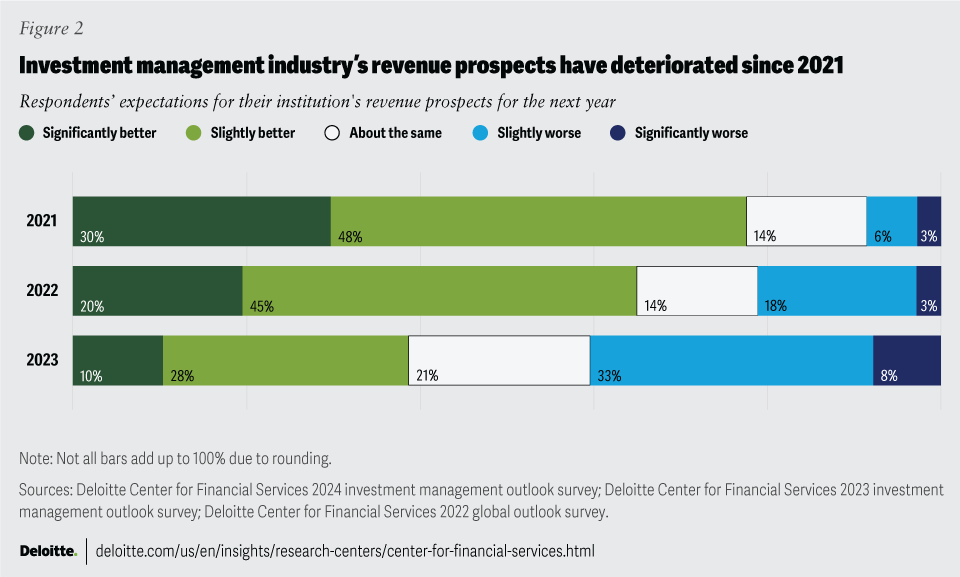

The investment management industry faced a tough year in 2022. In addition to margin pressures, high inflation, rising interest rates, instability in the geopolitical environment, and supply chain issues, 2022 was one of the few years since the late 1990s during which the bond and equity markets were simultaneously bearish.1 Private capital performed relatively well compared to other asset classes, demonstrating resilience, but overall, most asset classes exhibited weaker performance on a year-over-year basis. Since current revenue models are tied to assets under management (AUM), in a down market, revenues at many investment firms are expected to drop. Looking at this year's and the last two years of our proprietary survey data, we see growing pessimism in how respondents feel about their firm’s revenue prospects over the next year (figure 2). (See sidebar, “About the Deloitte Center for Financial Services 2024 investment management outlook survey” for details on the survey methodology.) Only 10% of survey respondents this year said they expect significantly better revenue prospects in the coming year, compared to 20% and 30% of respondents who said so last year and the year before, respectively.2 Furthermore, the percentage of respondents who expect significantly worse revenue prospects in the next year has grown.3 Although survey responses indicate that revenue will likely be subdued this year and next year, expectations may change over the course of the year depending on the changing market performance, economic outlook, and geopolitical environment.4

About the Deloitte Center for Financial Services 2024 investment management outlook survey

The Deloitte Center for Financial Services conducted a survey among 600 senior investment management executives in finance, risk management, regulatory compliance, operations, talent, and technology.

Survey respondents were asked to share their opinions about their organizational priorities and anticipated structural changes in the year ahead, as they pivot from recovering from the pandemic to the future.

Respondents were equally distributed among three regions: North America (the United States and Canada), Europe (the United Kingdom, France, Germany, and Switzerland), and Asia Pacific (Australia, China, Singapore, and Japan).

The survey included investment management companies with at least US$50 billion in assets under management and was fielded in June and July 2023.

Open-ended funds

Open-ended funds saw AUM decline by 15% in 2022, driven by fund outflows and market declines.5 For the United States, a large component of this significant decline in AUM was attributed to the decrease in active mutual funds AUM, which shrunk by about 24% year over year in 2022.6 In comparison, the AUM for index mutual funds and exchange traded funds (ETFs) in the United States fell by 17% and 10% year over year, respectively, while money market funds AUM rose marginally by 0.4% year over year in 2022.7 This decrease in AUM was the largest single-year year-over-year AUM drop experienced by active mutual funds in the United States since 2008, when the AUM plummeted by 36%.8

The narrative about active funds’ ability to better navigate market downturns seems to be fading over the last few years, an ebb that is replicated in fund outflows. US active mutual funds have seen a net outflow of assets for nine consecutive years, reaching US$1.2 trillion in 2022, the most significant single-year capital outflow from active mutual funds in the last three decades.9 Outflow from active fixed-income funds was a major driver of the negative cash flow, most likely triggered by the steepest interest rate hikes in three decades to combat inflation concerns.10

This year, however, about 50% of all US domestic equity funds have outperformed the benchmark, the first instance since 2013 with similar results.11 However, on an aggregate basis, US domestic equity funds underperformed the benchmark in 2022 by 1.4% and 3.0%, on an equal-weighted and asset-weighted basis, respectively, suggesting that at least some funds with large AUMs underperformed to a greater degree.12 Active equity managers across the globe also demonstrated similar underperformance characteristics. For example, active equity funds in the United Kingdom underperformed the benchmark by 14.6%, followed by those in the eurozone (-8.4%), Japan (-3.7%), Australia (-1.5%), and Canada (0%).13 Some active fixed-income mutual fund managers performed relatively better than their equity counterparts.14 The US general investment grade fixed income funds and high yield funds outperformed their benchmark by 8.3% and 0.02%, respectively, while general government funds underperformed its benchmark by 4.6%.15 In Eurozone, euro-denominated corporate bonds funds and government bond funds outperformed their benchmarks by 0.9% and 3.3%, respectively, while high yield bonds funds underperformed by 0.9%.16 Australian bonds funds outperformed their benchmarks by 0.8% on average.17

Smaller funds tend to be nimbler and quicker to adjust to market conditions than large funds. Larger fund managers, however, tend to have more capital to invest in technology to support alpha generation. To illustrate this point, when looking at survey respondents from firms with an AUM of greater than US$1 trillion, a higher percentage (19%) of respondents who claim their firm to have ideal digital technologies expect significantly better revenue prospects, compared to respondents from firms with lesser digital technology capability.18 However, fund performance analysis indicates that the technology investment hasn’t paid off yet in the aggregate. We’ll delve deeper into the latest technology and business processes developments in the subsequent sections.

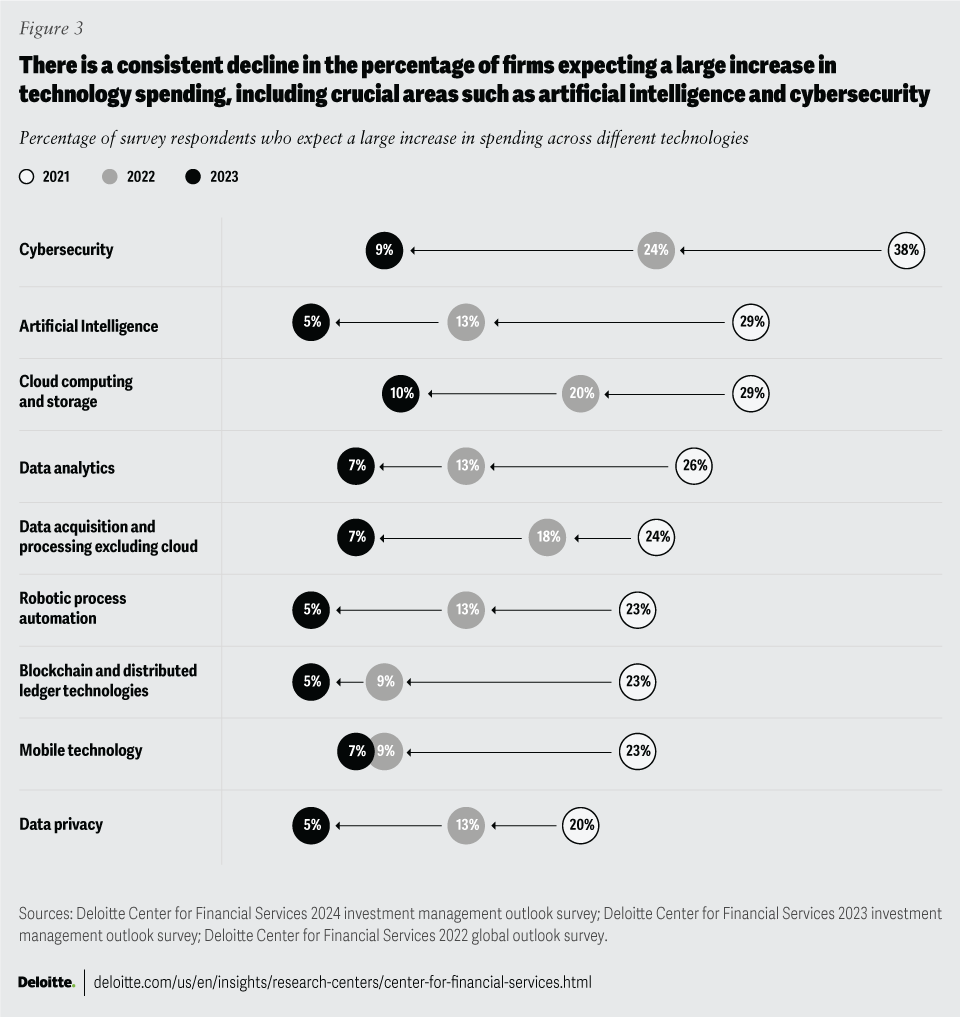

Investment managers’ financial performance is correlated to AUM, and the recent AUM decline has led to margin pressure across the industry, impacting the active managers to a greater extent. With this pressure, spending on technology—including disruptive emerging technology—is not expected to increase significantly. In fact, this year, fewer respondents are expecting a large increase in spending on technologies compared to last year and the year before (figure 3). A dynamic like this could further separate a small group of technology leaders from the rest of the pack, provided that the investments can actually lead to enhanced performance and delighted investors.

Uncorrelated results of alternative investment

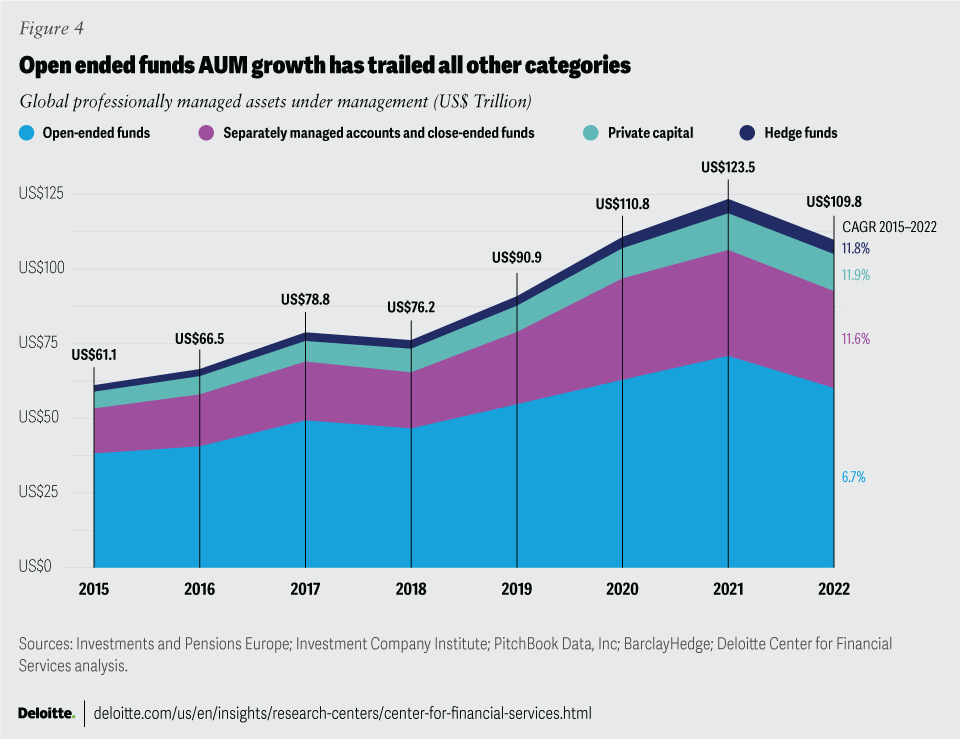

In terms of alternative investments, data suggests they were more resilient than their open-ended fund counterparts (figure 4). AUM for hedge funds remained flat year over year in 2022.19 The same is true for private capital, which includes private equity, venture capital, private debt, real estate, real assets, fund of funds, and secondaries.20 The growth in hedge funds and private capital AUM plateaued in 2022 after three and five years of double-digit growth, respectively.21

Hedge funds, on average, returned -8.22% on a fund-weighted, rather than asset-weighted, basis in 2022—the worst performance for hedge funds since 2008, when they returned -21.6%.22 Hedge funds experienced an outflow of US$323 billion overall, including 11 consecutive outflow months, in 2022.23 The magnitude of the outflow is seen by the fact that it accounted for more than 6% of the hedge fund industry’s AUM in 2021.24 Although hedge fund performances turned positive briefly at the beginning of 2023, the net cash outflow trend continued in subsequent months.25

Hedge fund AUM did not decline in 2022 despite net cash outflows and a negative return on average. These unusual circumstances dictate that there was a wide dispersion in fund performance, with some large funds outperforming their peers. Citadel and Elliott are examples of large hedge fund managers with above average performance. Elliott’s funds outperformed the industry in 2022.26 Citadel’s flagship fund outperformed the industry with an annual investment performance of 38%, along with strong performances in many of its other products.27 Furthermore, Citadel made a gross trading profit of US$28 billion and charged investors US$12 billion in performance fees and expenses, which shows that some investors are willing to accept higher fees if funds can generate higher returns.28

Private capital performed better than other asset classes, generating a rolling one-year IRR of 6.1% through the third quarter of 2022.29 However, the fundraising environment has become difficult for private capital funds. Private capital firms raised about 20% less capital in 2022 compared to 2021.30 The number of funds raising capital also declined by about 41% year over year in 2022.31 Furthermore, the amount of capital raised, and fund count, dropped by 28% and 32% year over year, respectively, in the first quarter of 2023.32 North America has consistently increased its share of private capital raised since 2018, due to the challenging fundraising environment in Asia and Europe, likely attributed to geopolitical concerns.33 Overall, high interest rates over the next year may continue to challenge private capital fundraising.

Furthermore, corporate valuations and asset prices have declined, so some funds may have to hold their assets longer to get better valuations. This may further impact fund distributions, which in turn could negatively impact investor liquidity. Lower capital raising and reduced investor liquidity will likely create opportunities for funds to utilize their dry power to make new investments. In fact, dry powder declined by 14% year over year in 2022 and now represents just 26% of total private capital AUM, compared to 31% in 2021.34 Reduced valuations can create opportunities for great vintage years for private capital funds that have the ability to deploy dry powder at opportune moments with attractive valuations.

M&A activity update

Mergers and acquisitions announced or completed in the investment management and wealth management space increased 4.4% year over year to 643 deals in 2022, compared to 616 deals in 2021.35 Deal volume continues to be elevated, with 324 deals in H12023, compared to 307 deals in the same period last year, a 5.5% increase.36 However, the value of deals in 2022 fell significantly compared to 2021.37 Furthermore, 14% of survey respondents this year believe their institution is very likely to increase its M&A activity in the next 6–12 months, compared to 6% of respondents last year.38 The combination of deal and survey statistics indicates that the number of deals will likely stay elevated compared to the previous year, albeit with lower average deal values likely compared to those seen in 2021.

Elevated industry, inflation, and geopolitical concerns, coupled with the high cost of capital, will likely lead firms to cautiously avoid large transformational deals, keeping the average transaction value low. According to our survey results, most respondents say that inflation (56%) and the geopolitical environment (58%) will negatively impact their operations, results that are similar to last year’s.39 A difficult operating environment can give rise to attractive deal opportunities and so, a small number of transformative deals may pass through. Some recent examples of such transformational M&A include deals between Franklin Templeton and Putnam Investments and Clayton, Dubilier & Rice and Focus Financial Partners. However, overall smaller tactical M&A deals will likely continue to tick the deal count over the next six to 12 months.

Unlike last year, since not many firms are not taking on large transformational deals, their top two challenges no longer include integration and strategy.40 According to our survey, the top two challenges organizations have faced or are facing with M&A transactions are due diligence and valuation and transaction readiness, which seems consistent with there being a larger volume of smaller, tactical deals than last year.41 Furthermore, 38% of survey respondents this year—compared to just 19% last year—believe regulatory approval is one of their top two M&A challenges, likely the result of rising regulatory scrutiny of M&A transactions.42

Another M&A trend relates to investment managers—especially private equity firms—partnering with insurance companies.43 Investment managers executed 28 insurance-related M&A deals in H12023 compared to 23 deals in H12022, indicating continued momentum.44 Insurance company acquisitions provide investment managers access to insurers’ large stash of reserves, which in turn can help increase AUMs and profitability. For insurance companies, adding the knowledge of private equity investment managers is likely to increase the breadth and depth of instruments utilized in their reserve portfolio management.

Deal activity may be slightly challenging in the short term with concentration on smaller deal value. Overall, the primary drivers for M&A—such as adding technology capabilities, building distribution capabilities, reducing cost through scale, adding new product lines, and divesting subscale businesses—remain intact. Newer deals will likely be driven by mergers and acquisitions of smaller investment managers that are finding it difficult to compete with larger investment managers in this challenging, highly volatile, and low-margin environment.

M&A is one way to improve the operational model with postmerger integration, an important success factor.45 Technology and business process improvement is another way of improving the operating model. However, since technology is consistently moving forward, what’s considered leading practices in the investment management industry is a continuously moving target.

Getting reliable results with technology and processes

Firms will likely have to find a way to invest in technology improvement even amid weak performance and margin pressures. Without the right technologies and matching processes and controls, investment managers could fall short of client expectations and internal efficiency goals. The state of technological development supports how and how well the vision and strategies are executed.

Meeting client expectations

Clients are delighted, or not, through their experiences. In investment management, investment performance is important, but it’s not the only factor in developing customer experience (CX). When performance wanes, the other elements of the CX can make the difference.

Investment vehicles and portfolios

Investing in client-centricity is predicated on knowing the target investor, the types of investments they want, and how the client prefers to interact with their investments and their investment manager.

Several product development trends are gathering steam—across areas such as packaging, pricing, investment strategy, theme, and operational approach to investment offerings—indicating what could be in store for 2024. Here’s a closer look at some of them.

Even though the first ETF was launched in 1990, ETFs remain one of the main drivers of innovation in the investment management industry. Pricing and liquidity characteristics have led to increased ETF usage, while placing competitive pressure across the industry.

Actively managed ETFs are one of the latest developments, and while the concept of active management in an ETF is not new, 2023 saw rapid growth. The AUM for active ETFs rose 10.6% year over year in 2022.46 Globally, actively managed ETFs accounted for 14.3% of net ETF fund flows in 2022, off a smaller base of only 5.3% of ETF AUM.47 Increased tax efficiency and enhanced transparency are likely driving this trend.48 There were 1,878 actively managed ETFs globally offered by investment management firms, comprising about US$488 billion of the US$9.3 trillion in AUM held in ETF at the end of 2022.49 A healthy slate of mutual fund to ETF conversions contributed to the significant growth of active ETFs in 2023. With the now broad menu of active ETFs available, a majority of surveyed advisors and investors indicate that active ETFs will likely become part of their future investment portfolios.50

Another innovation in investment management packaging is direct indexing, a technology-enabled tactic that is challenging both traditional mutual fund and ETF packaging approaches. Direct indexing is a twist on separately managed accounts (SMAs) because they offer the ability to deviate from an index, or fixed basket of securities, owned individually by the investor, for tax efficiency and client preferences. Retail investors often access this personalization through technology via a registered investment advisor relationship. However, retail brokerage and advisory providers are also offering these products to retail investors through an investment advisory intermediary. The investment minimums and pricing for direct indexing are both trending down, making these products more accessible for many retail investors, including those that use investment advisors.51 Some investment managers are trying to stand out by offering a diverse breadth of investment options, while others are trying to differentiate based on their investment minimums and trading frequency. Investment management firms face a new competition from direct indexing because the investment manager can be largely replaced with a customized basket of individual securities, supported by a technology platform operated by a wealth manager or registered investment advisor. According to a forecast, assets in direct indexing products are expected to reach US$825 billion, growing at a CAGR of 12.3% through 2026.52 If this approach proves to be an offering that helps firms gather AUM, then both active and passive managers would have fresh competition for AUM, one with a level of customization that can’t be built into either ETFs or traditional mutual funds. Investment managers do not want to miss out on this trend and so, over the last couple of years, many investment managers, including Morgan Stanley, BlackRock, Vanguard, Franklin Templeton, and JPMorgan Chase, have added direct indexing capabilities.53

As investment management firms strive to become more customer focused, they should consider investment vehicles used to house and distribute the investment intellectual property. Efforts to challenge assumptions and ask strategic investment vehicle questions could pay off:

- Why did the investor choose this investment strategy in this vehicle?

- Is there a lower cost way to provide investment intellectual property to the investor?

- Does the investment strategy provide tax efficiencies for the investor in the current vehicle?

- Are the fees associated with operating the investment vehicle commensurate with the value they offer to the investors in that vehicle?

- Does the vehicle provide liquidity that is appropriate for executing the investment strategy and for the investors?

As investment managers evaluate such strategic questions, the pace of change among investment management products will likely accelerate. Enabling technologies tend to be undergoing change faster than investment product development.

Inside the investment vehicle

Theme-driven portfolio construction is emerging as another vector for product development. The age-old classification of investment strategies into scales of growth versus value, large cap versus small cap, and by industry sector are not likely going away. That said, investor-centricity is helping to drive development of new classification schemes. ESG and its myriad varieties are investment themes that resonate with many investors. Emerging technologies is another theme that might interest a segment of investors. These themes address the client’s holistic desires by answering their noninvestment-oriented question: What is the nature of companies you want to invest in? Some investors will likely respond with “companies that have the highest growth potential,” or “investments that provide strong and steady dividends.” However, increasingly, investors want to invest in companies with values that aren’t typically found on the balance sheet or the income statement—for example, those that positively impact the environment, society, or equity.

A subjective values approach, when applied to ESG investing, places the judgment of positive impact into the hands of investment managers. It represents a meaningful departure from the way corporate behavior has been evaluated throughout history. ![]() The competitive marketplace for products and services historically judged firms through Adam Smith’s invisible hand, supported by distribution of information by capable, objective journalism.54 Corporations that maintained a clean reputation developed brand value and subsequently had healthier financial results.55 Investment managers were absolved from evaluating the ESG characteristics of companies under this approach, with the financial results presumably telling the whole story.56

The competitive marketplace for products and services historically judged firms through Adam Smith’s invisible hand, supported by distribution of information by capable, objective journalism.54 Corporations that maintained a clean reputation developed brand value and subsequently had healthier financial results.55 Investment managers were absolved from evaluating the ESG characteristics of companies under this approach, with the financial results presumably telling the whole story.56

ESG product development is adapting to regulatory refinement. Globally, while several new ESG or sustainable funds have been launched, many others have either changed their names, dropped their classification, or closed altogether due to regulatory changes.57 Product development is proving difficult for both investment management firms and the companies they are evaluating for potential investment because what is “good” is often a matter of perspective or personal preference. This problem will likely be difficult for the investment management industry to solve. In the meantime, ESG investment portfolios will likely indicate that the firm is evaluating ESG characteristics in the portfolio according to a set of guidelines and priorities established by that investment manager.

Firms that excel at investing for both financial and more esoteric ESG returns will likely use advanced technologies and alternative data to capture information on corporate behavior, evaluate it in a disciplined way, and connect corporate behavior to stock price performance. The technology for this approach is most likely active at only those firms further down the digital maturity path. For example, Candriam uses a proprietary database to coordinate and monitor engagement with investee companies.58 The database supports collaboration, a tangible building block in the virtuous cycle, between the ESG and investment teams, with easily accessible granular detail.59

Another thematic investment approach focuses on emerging scientific advancements. The themes are similar to ESG in that they deliver on the investor’s desires for these companies in their portfolios. Examples of investment themes include space exploration, health care, and the farming value chain. The difference between these themes and ESG is that participation in the ecosystem or the value chain of the theme qualify the investments into an index for evaluation. Then, based on financial results or potential, the portfolio companies are chosen to be part of a thematic portfolio. As of July 2023, thematic ETFs numbered 1,234 and had a total AUM of US$280 billion, accounting for just over 2.6% of the global ETF industry’s total AUM.60 The number of thematic ETFs globally increased by 10% from 1,119 at the end of December 2022 to 1,234 in July 2023.61 The investment management industry is adapting its products and services to meet client preferences.

Excellence in execution for investment solutions

For active managers, providing alpha or risk-adjusted performance that is superior to a lower-cost index approach can be a strategic pillar for their firms. Investment management firms routinely face the question: Why should your firm be selected to manage this investment portfolio?

Winning answers often describe an operating model that is designed specifically to create investment portfolios with unique value propositions. There are many, widely divergent successful investment management operating models. The latest trend is to seek alpha through robust evaluation of more data related to company and market performance and to incorporate more advanced analytical approaches. These approaches could include AI, for example, to correlate massive amounts of data and investment performance, creating an information advantage over the market.

This is easier said than done. The concept of getting more data and better analysis is no surprise to investment management firm leaders, but executing this strategy includes many complications. First, both new and traditional data can have low signal-to-noise ratios, which may produce more static than song. Another possible complication is the dramatic change in the process of finding data sources with potential investment signal. There are literally hundreds of small firms, and many large ones, that offer data products with potential for alpha for various strategies and markets. In addition, the process for finding the investment insight in a dataset may require the close collaboration of a data scientist and an equity analyst, people with extensive—but very different—vocabularies. Having the right people in the right role is one of three top challenges that organizations face during the operational digital transformation journey, according to this year’s survey respondents.62 This is where talent models, by fostering collaboration, cross-training, and shared success, can develop people to overcome the difficult and wide-ranging issues that arise when working to generate investment signals from new data sources. Leadership can also contribute to this success by reinforcing the firm’s purpose, which tends to help foster strong collaboration. Our survey found that firms with stronger senses of purpose were significantly more likely to have much stronger collaboration capabilities (26%) compared to firms that don’t (18%).63

Achieving excellence in customer experience

Excellent investment performance generally has a halo effect on customer satisfaction, but customers typically expect more than that from their investment vehicles. Beyond investment performance, expectations often include personalization and timeliness of interactions, and technology plays an important role in staying aware of customer needs.64 It’s important to note that customer expectations do not necessarily originate within the investment management industry; often the expectations are established outside the industry by firms that provide leading edge customer service.

Investment management firms with significantly better revenue prospects are more likely to become industry leaders in CX.65 Understanding the customer (likely multiple personas) is one of the first steps to becoming a leader in CX.66

Investment managers with a high quality, differentiated CX, often start with a strong foundation by effectively managing the daily aspects of the client-manager relationship, seeming to follow a “walk before you run” approach.67 Edward Jones, for example, is investing in increasing personalization, enhancing tax management capabilities, and expanding the list of eligible investments to increase CX.68 Many investment management firms have created senior positions responsible for improving CX.69 The drivers for positive CX, apart from investment performance, are: 70

- Clear and transparent fund performance and disclosure reporting

- Timeliness and clarity in customer communication

- Frictionless onboarding and customer grievance resolution

- A long-term relationship approach as opposed to short-term customer acquisition strategies and upselling

- Genuine consideration and application of client preferences and feedback

CX is one of the areas that generative AI will likely transform over the next few years. Generative AI—coupled with customer segmentation, past interactions, and access to portfolio information—could conceivably supply speed, accuracy, and personalization to the CX, directly addressing the first two of the five components of nonperformance-linked CX.

One of the early iterations of generative AI was actually developed before generative AI became a household word; it was called natural language generation (NLG). Interestingly, NLG appeared before there were observations of hallucinations in AI, which likely result from the new large language model (LLM) approach. NLG was able to, in a structured and limited way, fully create performance attribution reports from structured investment performance data.71 Adding to this approach, LLMs enhanced efficiency and control, and provided new levels of sophistication and customization to the portfolio reporting process.72 Additional training on the performance reporting parameters coupled with proprietary performance data can partially mitigate the risks of hallucinations.

Generative AI can help transform the timeliness and clarity of customer interactions. Imagine a customer asking the names of top drivers of alpha in their portfolios’ funds over each of the prior four quarters, showing how each performed compared to their industry sector peers. A fully developed, generative AI capability could perhaps answer that question in a matter of seconds, which might be hours faster than pre-generative AI processes could generate. However, like many transformational changes, this one would likely require close collaboration across the organization—including, front, back and middle office, finance, information technology, and risk management—to become operational. One such example is T. Rowe Price, which is undertaking investments in AI pilots across business operations—including distribution channels and technology units—to try to capitalize on the benefits of machine learning.73 With many investment firms investing in this, generative AI-enabled CX capability is expected to advance rapidly in 2024.

Solving the larger, more difficult modernization challenges likely requires collaborative, cross-functional teams to develop effective solutions, coupled with leadership’s communication of the vision and talent, which places the right people in the right positions and reinforces the right behaviors.

Meeting management expectations

Efficiency and control

Delighting customers is a goal of almost every firm, but doing so inefficiently without control can be a recipe for disaster. Competitive pricing and profitability typically demand efficiency, and the highly regulated investment management industry does not tolerate lack of governance and controls. In a fast-paced and highly competitive industry, balancing these often-competing priorities is difficult under normal conditions, but when new disruptive technologies enter the picture, the complications grow. In 2024, some investment management firms will likely develop two such game-changing technologies, generative AI and quantum computing, into their digital transformation journeys. The industry is making progress, with 50% of survey respondents reporting that they have fully or almost fully realized the potential benefits of digital transformation, a rise from 44% last year.74 The standard for comparison is moving, and firms without generative AI or post-quantum encryption capabilities in 2025, will likely be much less optimistic about their digital transformation progress.

“Generative AI will likely modernize many aspects of the investment management sector but not without bringing new risks. Firms that build an AI risk management program, focusing on fairness, reliability, accountability, transparency, privacy, and security, will be more effective at mitigating these new risks.”

―Clifford Goss, PhD, partner, Deloitte & Touche LLP

Generative AI adoption will likely accelerate through 2024. With many potential applications that can either save time or create new capabilities, and with the initial investment in generative AI usage generally being low, many firms will likely be able to benefit from generative AI. Examples of leveraging generative AI range from customized stock picking, writing performance reports, writing proxy letter, enhancing advisor platforms, and enhancing digital assistants to have more natural language capabilities.75 With the rapid adoption of the technology, there is sufficient evidence to speculate that a broad and shallow adoption is happening. Generative AI’s rapid adoption is in stark contrast to distributed ledger (blockchain) technology in its early phase wherein enterprise application was costlier, and its installation was generally high code, compared to the relatively low code path to implement generative AI. However, generative AI also brings with it risks, such as cyber risks and LLM hallucinations, which typically warrant new controls—another example of the importance of pairing technological advancement with checks and controls.

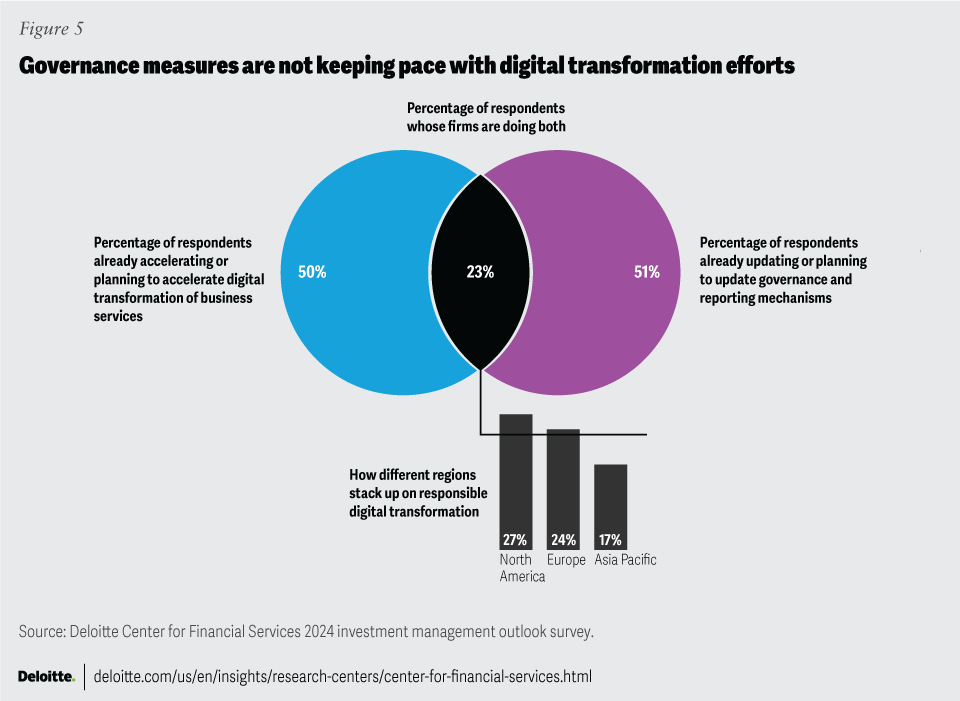

With the advent of these disruptive technologies, digital transformation in the investment management industry is likely to accelerate, even in the wake of progress made over the past several years. Perhaps next year, investment management firms may change the pattern of behavior that they generally have exhibited for the past three years, wherein acceleration of digital transformation was not tightly linked to modernization of governance and controls (figure 5).

Regulators are taking notice of new processes and technologies and developing new industry requirements, most notably on T+1 settlement, cybersecurity, and ESG. In the United States, the shift to T+1 settlement is expected to cost the industry US$3.5 billion to 5.0 billion.76 However, the SEC expects the benefits of a shorter turnaround cycle, mainly reduced counterparty risk and improved liquidity management, to outweigh the costs.77 While many firms are concerned about the shift to a shorter settlement cycle, some firms are even relocating talent and operations to the US West Coast to allow for additional time to facilitate settlements.78

The SEC’s new cybersecurity regulation requires a short four-day incident reporting deadline. These new requirements are likely to initiate new policies and procedures as well as potential technology enhancements to help mitigate risk and control the cost of breaches and subsequent disclosures.79 Breaches already cost an average of US$4.45 million per breach, and the new SEC regulation may draw attention to this risk and get firms to address the root causes.80 Cybersecurity is increasing in emphasis, not decreasing, as new technologies emerge.

New and pending ESG name rules in the United States have led many firms to reassess their fund naming conventions.81 In the United States, many firms have dropped ESG or related terms from fund names.82 In Europe, the clarification between Article 6, 8, and 9 funds have kept investment management firms busy.83

With changing regulation and ever-advancing technologies, maintaining a strong governance posture is an ongoing effort. With the advent of generative AI, governance should be incorporated into each use case. Due to data privacy issues, partitioned implementations will likely be required from a governance perspective in early generative AI implementations, giving firms with well-developed data infrastructures a head start over their less advanced peers.84

Quantum computing and cybersecurity

Adoption of quantum computing-focused technologies could increase dramatically as they grow out of infancy. Investment in quantum computing for growth may be less urgent, but some firms are preparing nonetheless to generate revenue and delight customers with quantum computing-enabled capabilities.85

Investment management firms are also using quantum computing for Monte Carlo simulations, portfolio optimization, risk minimization, and complex derivative calculations to try to get ahead of their competition.86 Quantum computers may also be used to improve AI’s ability to process large volumes of data and to elevate the CX by processing client inputs and behavior to predict their needs in near real time.87

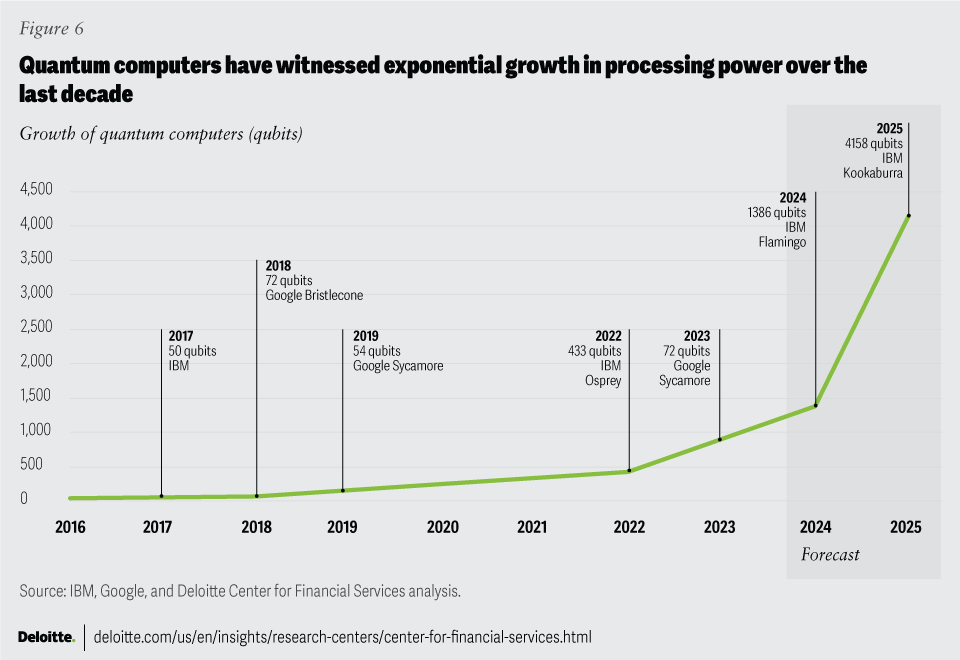

Google announced in mid-2023 the creation of a supreme quantum computer that is reportedly millions of times faster than the current fastest supercomputer.88 Google’s quantum computer can also perform functions significantly faster than supercomputers.89 Recent announcements by Google and IBM mark another milestone for the exponential growth that has been taking place over the last few years in quantum computing capabilities (figure 6).

Even though quantum computers are still in the early stages of development, some firms have already started developing and exploring their quantum capabilities since it requires a different skill compared to traditional IT systems.90 A few notable FSIs including JPMorgan Chase, Goldman Sachs, Barclays, and HSBC have formed teams to explore and figure out use cases for adoption of quantum computing technology.91 Organizations with quantum computing capabilities may have an information advantage over competing FSIs at least for the initial adoption phase, which may last several years.

But before these ambitious goals can be achieved, firm leaders may need to play defense first. The cybersecurity threat of quantum computing is a pressing problem. Hackers are currently storing encrypted data, with plans to decrypt it when they have access to quantum computing.92 But help is on the way—the National Institute of Standards and Technology has published draft standards for a few post-quantum cryptography algorithms for public comment starting in August 2023.93 The final standards are expected to be published in 2024.94 For investment management firms, the threat of a quantum-enabled hack is a potentially existential problem for three reasons:

- The sensitive nature of the data they hold

- The importance of reputation to their brand value

- The potential for disruption of financial markets

Given the risks that future quantum computers hold, firms should start preparing today. That includes having a complete inventory of data, its sensitivity, where it is stored, and how it is secured; learning about the upcoming switch to post-quantum cryptography; and working to validate that existing systems and data are properly secured.

Leading a purpose-centric firm

Navigating organizational model changes can become easier when the organization is aligned with a strong sense of purpose. When survey respondents agree or strongly agree that their workforce is aligned to their organization’s sense of purpose, they are also more likely to report that their organization’s culture became much stronger.95 Let’s explore how modernizing the talent model, striking the right balance with workplace flexibility, and aligning employee incentives to reflect the upskilling of talent can help drive a firm’s purpose, creating a more agile organization that can more effectively transform itself.

Modernizing the talent model to match new opportunities

The challenges of operating under the constraints of the pandemic are now transitioning to modernizing the talent model, advancing a firm’s culture, and cultivating a work environment that prioritizes work-life balance and flexibility. Yesterday’s challenges are today’s opportunities; lessons learnt from the pandemic are transforming how firms assess and invest in their operating models. In 2024, we expect firms to continue investing in talent modernization by aligning intrinsic and extrinsic value throughout the investment life cycle with new industry certifications and diversifying talent skillsets, in addition to exploring the oversight of process management.

Upskilling to develop more generalists

The ideal postpandemic talent model in the investment management field continues to challenge how firms grow and upskill their talent pool. Investment management firms can encourage employees to be generalists first and specialists second, especially in the nonportfolio management talent pools. A generalist-first model allows employees with diverse skillsets to generate ideas and efficiently address client needs and be more effective participants in large cross-organizational projects. To achieve the ideal generalist model, investment firms will likely need to invest in cross-functional training programs that activate knowledge-sharing and employee growth opportunities. In line with this approach, firms may also want noninvestment professionals that work alongside investment teams to understand and communicate in the common investment language. Firms can leverage self-paced foundational courses by organizations such as CFA Institute, Yale University, and Global Association of Risk Professionals to train professionals from marketing, sales, talent, information technology, and compliance teams about the basics of the investment management industry.96 Employees, especially in generalist roles, are encouraged to equip themselves with industry essentials to work efficiently with investment teams.

Training front office professionals in ESG principles

Within the portfolio management talent pool, demands for ESG funds and products may necessitate additional talent strategies. ESG-driven investing can often serve as a proxy for clients’ ESG investment values. To hedge against the uncertainties of ESG-related products and blurred marketplace parameters, firms should consider external training and certificates that build competency in ESG-related portfolio management decision-making. Because clients and regulators will likely continue to challenge how ESG investment decisions are managed, comanagement of sustainability-themed funds by accredited ESG professionals may be a possible solution to assuage potential greenwashing suspicions.97

Educational institutions offering sustainability related degree courses

Many educational institutions have started offering degree programs on sustainability. New talent hiring criteria may include professionals with a degree in sustainability and related courses.

Some notable degree programs:

- A one-year MSc in Sustainability course offered by Oxford University, Oxford

- A one-year ESG Management MSc degree offered by King’s College, London

- A one-and-a-half-year MS in Sustainability Management course offered by Columbia University, New York

- A two-year MSc Transformative Sustainability degree offered by Bocconi University, Milan and Politecnico di Milano, Milan

Sources: Deloitte Center for Financial Services analysis and Oxford University, King’s College, Columbia University, Bocconi University.

Talent model modernization and business operations outsourcing

Another postpandemic lesson is the benefit of building resiliency into daily operations, which led investment management firms to explore transitioning in-house operational processes to outsourced middle- and back-office service providers. To meet the need for transforming operations, 29%, 23%, and 28% of survey respondents indicated that their firms are planning to pursue outsourcing for front, middle, and back-office processes, respectively, over the next 12-18 months.98 In stark contrast, only 4%, 5%, and 5% of survey respondents indicated that their firm plans on pursuing a “build” strategy for front-, middle-, and back-office processes, respectively.99 In 2024, asset managers will likely face the challenge of how to incrementally measure the transformational benefits of outsourcing processes and business capabilities in the long run as opposed to managing talent and business capabilities in-house. The long-term costs of outsourcing operations can quickly add up if internal talent is not upskilled with the controls and processes for effective oversight management. Modernizing the talent model may include management training for an array of outsourced investment management service providers. When assessing existing talent models, investment management firms should convey a clear vision of how to strategically align onshore, offshore, and nearshore talent models. In addition to managing process changes, investment management firms can expect to invest in more certifications that meet client demands.

Remote, hybrid, or in-office…what suits you the best?

To determine the most effective work environment (remote, hybrid, or in-office), investment management firms should identify which learning and development opportunities will likely facilitate talent modernization efforts. Last year, we noted that the pandemic was a catalyst for workplace model transformation, with remote work gaining prominence.100 This year, more firms have adopted some form of return to office plan than last year.101 However, employers that mandate return-to-office experience higher employee attrition and struggle with recruitment.102 According to a recent Deloitte Center for Financial Services 2023 employee engagement study, two-thirds of the respondents who were remote at least part of the time say they will likely leave their current role if five days a week return to office becomes mandatory.103 Moreover, our survey suggests that firms across regions that adopted a more flexible hybrid or remote work model are more likely to experience stronger improvement in their culture (figure 7).104

Increasing collaboration and productivity in a hybrid workspace

In 2024, investment management firms will likely have to continue to create collaboration opportunities that coalesce all three working environments into one talent modernization plan. There is evidence to suggest that self-selected work environments and working hours are more conducive to happiness—even in a sector that continues to undergo significant shifts.105 According to Deloitte research, self-selected work environments can foster happiness, which engenders greater collaboration among employees.106 As firms continue to explore how remote, hybrid, and in-office environments impact their culture, they will likely have to assess how horizontal and cross-functional teams optimize their experiences and time together. Overall, firms that prioritize employee preferences for remote work experience a better culture and talent model for orchestrating training and education.107

Examples of investment management firms with notable actions to advance diversity, equity, and inclusion (DEI) efforts

Here are a few examples of DEI actions that investment management firms have taken:

- Fidelity, Schroders, BlackRock have removed or reduced academic requirements for early-career applicants as part of their socioeconomic diversity goal.

- The ‘BeST’ program at JPMorgan Chase provides a platform for neurodivergent individuals to utilize their skillset at the workplace.

- 43% of new hires in 2022 at Fidelity were people of color and 42% of the new hires identified as women.

- AQR provides 10-week rotational programs for first generation college students and undergraduates from lower economic background as part of their socioeconomic diversity goals.

- AllianceBernstein offers adoption and surrogacy reimbursement for employees along with gender affirming care.

- At The D. E. Shaw Group, almost 40% of the 2023 intern class and more than half of 2023 sophomore fellowship program participants were women and nonbinary students. They also run the “Prism” program for experienced professionals from underrepresented backgrounds.

Sources: Deloitte Center for Financial Services analysis, Ignites Europe, FundFire, JPMorgan Chase, Fidelity, BlackRock, AllianceBernstein, and The D. E. Shaw Group.

Striking a balance

As they inch closer toward 2024, investment management firms can expect to add new threads to the fabric of their firm’s culture by advancing talent modernization and workplace enablement, while refining the dimensions of their DEI efforts. Globally, the industry will likely advance when DEI efforts can collectively amplify marginalized voices. According to a cross-industry survey, employees at companies that are striking the balance report less stress (74%), more energy at work (106%), higher productivity (50%), fewer sick days (13%), more engagement (76%), more satisfaction with their lives (29%), and less burnout than people at less balanced organizations (40%).108 These factors likely apply to the investment management industry as well. Finding purpose and living up to your firm’s vision, practices, and investments is likely to be a contributing factor to success in 2024 and beyond.

When the going gets tough, the tough gets going

For the investment management industry, 2024 brings with it exciting opportunities, urgency to take action, and reasons for caution. With intense competition for AUM, investment management firms are working to differentiate themselves, particularly in the areas of emerging technologies, talent modernization, client experience, purpose and ESG, and workplace environments.

We hope this outlook informs a road map for growth through financial performance, but also through the nonfinancial factors that current clients and employees increasingly expect and value. There is no one way forward––navigating the future should include a nimble, holistic approach––but at its most foundational level, success will likely require leadership in understanding and delivering on stakeholder and marketplace demands in a disruptive and dynamic world.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}