Article

New thresholds for company size classes under German commercial law

Increase of the thresholds “balance sheet total” and “revenues” for company size classes in the German Commercial Code

On 17/04/2024, the second act amending the DWD act and amending German commercial law provisions (“Zweite Gesetz zur Änderung des DWD-Gesetzes sowie zur Änderung handelsrechtlicher Vorschriften”) became effective. This act has raised the thresholds “balance sheet total” and “revenues” for determining company size classes in the German Commercial Code (“HGB”). This increase leads to a reduction in reporting requirements, and in some cases to an exemption from the statutory audit obligation, in particular for companies (corporations) which are now classified in a smaller size class as a result of the reclassification.

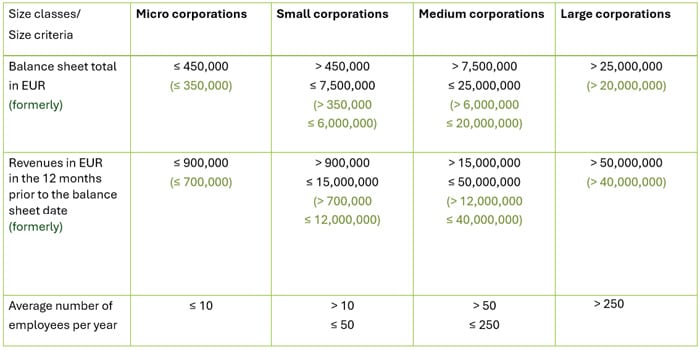

Companies are categorized into the following four size classes under German commercial law (sections 267, 267a HGB): micro, small, medium and large corporations. Assignment to a size class is based on the three criteria “balance sheet total”, “revenues in the twelve months prior to the balance sheet date” and “average number of employees per year”, for which certain threshold values apply. Two of these thresholds must be exceeded or fallen short of in two consecutive financial years in order to be assigned to a new size class. The respective size category determines the requirements for the obligation to prepare and disclose annual financial statements and to have them audited.

In October 2023, the European Commission issued a directive amending the thresholds for determining company size classes in line with inflation (Commission Directive (EU) 2023/2775 of 17/10/2023). This provides for increased thresholds for the criteria “balance sheet total” and “revenues” for the individual size classes.

The Second Act Amending the DWD Act and Amending Commercial Law Provisions, which became effective on 17/04/2024, implemented the increase in the thresholds in Germany as follows:

Thresholds for determinin the size classes (sections 267, 267a HGB)

Thresholds for exemptions from the obligation to prepare consolidated financial statements and a group management reports (section 293 HGB)

The increased thersholds are binding for financial years beginning after 31/12/2023; there was an option for financial years beginning after 31/12/2022. When the standard is first applied, the new thresholds will therefore have to be used to assess the applicable size category mandatory from 01/01/2024 onwards; this will have to be done with reference to all past reporting dates. The fact that the increased thresholds also apply to previous years may result in situations in which there is an immediate allocation into a new size category.

It can be expected that many companies will “fall down” into a lower size category. The change appears to be particularly relevant for medium corporations which are on the threshold of becoming small corporations, since small corporations are no longer subject to an audit requirement. The application of the new thresholds may also result in the immediate elimination of the obligation to prepare consolidated financial statements.

With regard to the effects of the retroactive first-time application of the new thresholds on the audit of the annual financial statements, a distinction must be made as to whether the auditor has already started the audit or not. If the auditor has not started the audit and there is no contract yet, the company can refrain from assigning the audit engagement. If the audit agreement has already been concluded but the auditor has not start the audit yet, it can be assumed that the contractual basis for the audit agreement has subsequently ceased to exist and that it is no longer reasonable for the company to adhere to the agreement. As a result, the company can withdraw from the contract in accordance with section 313 III German Civil Code (Bürgerliches Gesetzbuch, “BGB”). If, on the other hand, the auditor has already begun its work but has not yet completed the audit, the company can also withdraw from the contract in accordance with section 313 III BGB (ex nunc). As the termination of the audit contract has no retroactive effect, the auditor is entitled to a fee for the services already rendered. Beyond this, the fee claim lapses. The company remains free to continue the audit as a voluntary audit or to have it carried out despite the cancellation of the audit obligation. If, on the other hand, the audit has already been completed, the audit, including the auditor’s opion and the audit report, remains unchanged; a subsequent change to an voluntary audit is not possible.

It should be noted that the obligation to prepare a sustainability report in accordance with the “Corporate Sustainability Reporting Directive” (Directive (EU) 2022/2464 of the European Parliament and of the Council of 14/12/2022, “CSRD”) is also linked to the abovementioned thresholds. It can therefore be expected that the number of companies affected by the CSRD reporting requirement will also decrease. CSRD is currently an important topic; see also other Deloitte pages (e.g. Corporate Sustainability Reporting Directive (CSRD), Umsetzung der CSRD-Anforderungen).

Published: March 2025

Your Contact

Recommendations

Anti-Money Laundering Compliance | The EU Anti-Money Laundering (AML) package

Part 2: The expansion of the scope of companies subject to notification obligations to the transparency register

General Corporate Law

Start-Up Requirements | Corporate Governance | Trading Activities | Expansions | Financing | Dissolving | Day to Day Advice