Article

Sound Compensation: Implications of Brexit for Branches of EU institutions

Application of UK remuneration rules and InstitutsVergV

The end of the Brexit transition period on 31 December 2020 has brought about numerous changes for the ways in which industries and firms operate – for many, this is perhaps an understatement. From a Financial Services reward standpoint, the end of the Brexit transition period means that, for the first time, Branches of EU banks operating in the UK will have to take account of the UK remuneration rules and the detailed UK regulatory guidance that accompanies these rules, as well as ensuring that their remuneration policies and practices continue to comply with the revised version of InstitutsVergV (IVV 4.0).

Prologue

The end of the Brexit transition period on 31 December 2020 has brought about numerous changes for the ways in which industries and firms operate – for many, this is perhaps an understatement. From a Financial Services reward standpoint, the end of the Brexit transition period means that, for the first time, Branches of EU banks operating in the UK will have to take account of the UK remuneration rules and the detailed UK regulatory guidance that accompanies these rules. In addition, UK Branches of German banks will have to ensure that their remuneration policies and practices continue to comply with the revised version of InstitutsVergV (IVV 4.0), which implements the Capital Requirements Directive V (CRD V) into German law, and further consider the revised version of EBA Guidelines on Sound Remuneration Policies under Directive 2013/36/EU (EBA GSR), which are currently in the consultation process and are due to be published by 26 June 2021.

UK remuneration rules at a glance

From a UK standpoint, key considerations will include:

Application of transitional relief in the UK

The UK regulators have provided former passporting firms with transitional relief which will allow them to defer the application of the specific UK remuneration rules which go beyond the CRD remuneration requirements until the first performance year starting at least three months after 31 December 2020. For calendar year-end EU firms, this means that their UK branches will become subject to the UK remuneration rules in full for performance years starting on 1 January 2022.

For the period in relation to which transitional relief is available (for calendar year-end firms, the performance year starting on 1 January 2021), a UK Branch will not be required to apply the elements of the following UK rules that go beyond the core CRD requirements:

(a) Deferral

(b) Clawback

(c) Buy-outs

(d) Risk Adjustment

(e) Personal Investment Strategies

However, care will needed in relation to assessing the specific components of each of the above rules to ensure that the Branch complies with the components that do not go beyond the CRD requirements, as firms will still be expected to ensure compliance with these for the 2021 performance year.

Application of other UK remuneration rules and UK regulatory guidance

UK Branches will be expected to apply all other UK remuneration rules in relation to their first performance year starting after 31 December 2020 (i.e. 1 January 2021, for calendar year-end firms).

This will include, for example, identifying Material Risk Takers at the level of the Branch itself for the first time, with reference to the new Regulatory Technical Standards (RTS) on Material Risk Taker identification under CRD V.

The UK regulators have set out their expectations in relation to firms’ application of these RTS, and their assessment of other risks for the purposes of identifying risk-taking staff beyond those risks set out in the RTS, in detailed regulatory guidance. Branches should take this guidance into account when developing their Branch-level identification policies and Branch Material Risk Taker list.

The UK regulators have also issued specific regulatory guidance in relation to the application of the remuneration rules to staff who are identified as Material Risk Takers for only part of the performance year (including how the UK individual de minimis proportionality thresholds can be applied in this context) and the process for submitting approval requests to the UK regulators for Material Risk Taker exclusions.

Detailed UK regulatory guidance also relates to other areas, such as remuneration governance, the role of local risk management and control functions, the assessment of performance for the purposes of determining variable pay, and retention awards

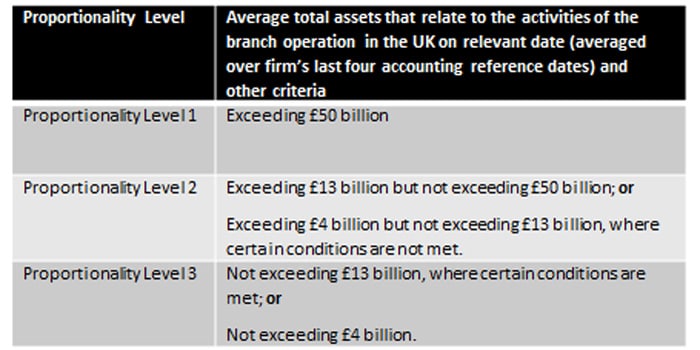

Determination of UK “proportionality level”

Key to a UK Branch’s application of the UK remuneration rules will be its “proportionality level”, with a Branch’s categorisation determining whether the rules on deferral, payment in instruments and discretionary pension benefits can be disapplied, and whether a remuneration committee is required to be established.

There are three proportionality levels in the UK, as summarised below:

Branches whose average total assets exceed £4 billion but are less than £13 billion will need to take particular care in ensuring that the specified conditions are met in order to be categorised as a proportionality Level 3 firm in the UK.

Remuneration systems at German based institutions: Modifications under IVV 4.0 (draft) at a glance

From a German standpoint, firms will need to ensure that they take into account the amendments to the German remuneration rules under IVV 4.0 (relating to remuneration systems and remuneration governance) and under the revised German Banking Act (Kreditwesengesetz, KWG, relating to, inter alia, risk taker analysis).

IVV 4.0 is still in the legislative process. According to currently available information, the German legislator will finalise IVV 4.0 at the end of first quarter 2021. The draft of the IVV 4.0 published on 12 November 2020 provides for the following material changes to the regulatory requirements:

Risk Taker analysis for all institutions

All CRR institutions and all other institutions that are significant institutions must conduct a risk taker analysis. Sec. 25a (5b) s. 1 KWG defines a catalogue of persons that have to be identified as risk takers. Significant institutions must further conduct a comprehensive risk taker analysis in accordance with Commission Delegated Regulation 604/2014.

Extended scope of application of special legal requirements for variable remuneration of risk takers

Special legal requirements will not only have to be observed by significant institutions, but - with the exception of particular provisions relating to the variable remuneration of the management board and the provisions relating to the remuneration officer - will also have to be applied by non-significant institutions that fall into one of the two groups specified under Sec. 1 (3) s. 2 IVV 4.0.

The first group covers consolidating institutions in a group with (partially) consolidated total assets of more than EUR 30 billion; the scope of application also includes consolidating institutions which have total assets of less than EUR 15 billion at solo level, but exceed EUR 30 billion in their (sub-)consolidated group.

The second group includes institutions with a balance sheet of more than EUR 5 billion on average in the last four financial years and which belong to one of the groups in Sec. 1 (3) s. 2 no. 2 IVV 4.0 (i.e. neither claim exemption under Sec. 20 (1) SAG nor the simplified requirements under Sec. 19 and 41 SAG, or have trading book activities that go beyond a small scale in the sense of Art. 94 (1) CRR, i.e. trading book activities of at least 5% of the institution's total assets and at least EUR 50 million, or whose total value of derivatives positions held for trading purposes exceeds 2% of total on-balance sheet and off-balance sheet assets and whose total value of all derivatives positions exceeds 5%).

Extension of general requirements for remuneration schemes: gender neutral remuneration principle

Under CRD V, institutions have to observe the principle of having a gender neutral remuneration policy, as defined by the EU legislator in CRD V. The provision does not introduce any additional material requirements for remuneration systems in Germany, as institutions are already obliged to pursue a gender neutral remuneration policy under the current law (inter alia under Sec. 1 of the German Equal Treatment Act and the statutory provisions of the German Transparency Act). However, the EBA has set out in its draft amended Guidelines on Sound Remuneration Policies its specific expectations on (a rather comprehensive) governance processes to ensure an appropriate application of the principle.

Modification of the special requirements for the variable remuneration of risk takers

Modifications of the special requirements follow the requirements of CRD V:

(a) The retention period for the variable remuneration has to amount to at least four years.

(b) The exclusion of risk takers with variable remuneration of a maximum of EUR 50,000 in the reference period from the scope of application of special requirements will additionally require that the variable remuneration should not account for more than 1/3 of the total remuneration.

Further remarkable modifications

Disclosure requirements for non-significant institutions will be modified. Listed small and non-complex institutions must disclose on the remuneration system - in addition to the information from Article 450 para. 1 lit. a) to d), h) to j) CRR - the total amount of all remuneration (divided into fixed and variable remuneration) as well as the number of beneficiaries of the variable remuneration. All other small and non-complex institutions with a balance sheet total of no more than EUR 5 billion that also meet the other requirements of Article 4 (1) No. 145 CRR) are not subject to any disclosure requirements with regard to their remuneration systems.

The EBA has in its public hearing of the consultation on the revision of the Guidelines on sound remuneration on 13 January 2021 pointed out that it also expects the inclusion of individual performance parameters for the content of retention bonuses in the future. This requirement is not provided for in the draft of the IVV 4.0 (nor in the current IVV version). The EBA's position in the final version of the Guidelines on Sound Remuneration Policies remains to be seen.

Focus on Germany and upcoming virtual discussion forum on 4 February 2021, 11.30am CET

We will be holding a virtual discussion forum on 4 February 2021, at 11.30am CET where we will focus on the practical steps that EU firms with UK Branches should be considering, both in the UK and in Germany, with the opportunity for discussion and debate.

If you would like to join us, a link to the registration can be found here.

Your Contact

.jpg)

Your Contact in UK

|

Tax |

Tax |