As we approach the end of 2023 and begin to turn our focus onto next year, it is a good time to share some perspectives on the 2024 outlook for the Nordic banking sector. However, before we do that, we will wrap up 2023 based on the banks’ results during the first nine months of the year.

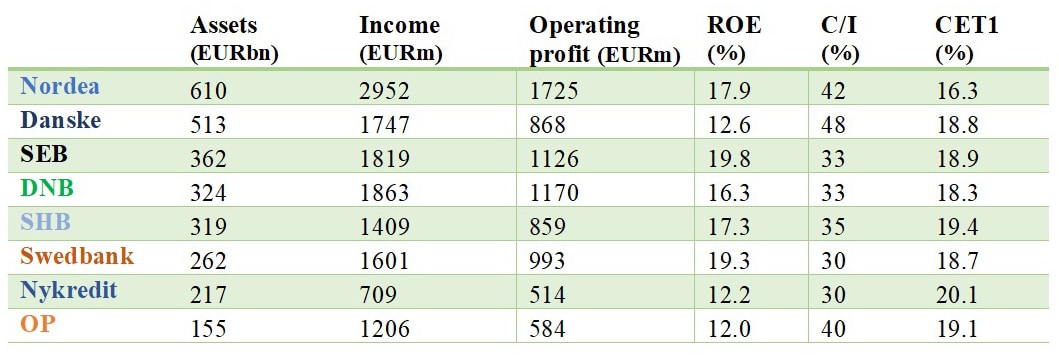

The large Nordic banks1 demonstrated the current strength of the banking sector, delivering an average return-on-equity (ROE) of 16% and cost-to-income ratio (C/I) of 36% with a Common Equity Tier 1 ratio (CET1) of 18.7% in the third quarter of 2023. This combination of profitability, efficiency and capital strength places the large Nordic banks as some of the best performing in the world.

Chart 1: The key financial figures for Q3/2023. Source: The sample banks’ Q3/2023 interim reports. FX rates as of 30 September 2023. Source: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/html/index.en.html.

However, we do consider the performance of the large Nordic banks to be at or near its peak right now and expect the whole global banking sector to be challenged next year due to a multitude of reasons. The Nordic banking sector will be no exception, although benefitting from, on average, stronger local economies.

We observe three main headwinds the banks will face in 2024 i.e., squeezed net interest margins, higher operating expenses and increasing loan losses. During the first nine months of 2023, the total income of the large Nordic banks grew by 20–50% compared to the same period in 2022 with almost all the growth resulting from NII expansion. However, in Q3/2023 the quarter-on-quarter NII growth was measured only in single digits reflecting the stabilisation of interest rates in the region. As we expect central bank policy rates in the Nordics to start declining in 20242, this will start to put pressure on revenue generation. Additionally, subdued loan growth is impacting lending margins negatively from the banks’ perspective with fierce competition. Finally, on the other side of the banks’ balance sheet, rising funding cost will squeeze net interest margins lower in 2024.

We are beginning to see economic growth across the Nordics cooling, with GDP growth negative in all the Nordic countries in Q3/20233. This will inevitably lead to challenges in loan amortisations and increased credit losses in the future. So far, this has not been an issue in the Nordics and most of the banks are well prepared for worsening economic conditions, being both well capitalised and retaining strong impairment levels which include management overlays which have remained higher since the start of the Covid-19 pandemic. It will be interesting to see how the banks deal with potential higher credit losses next year. Will banks start to release the overlays, something they have been reluctant to do during the past 3.5 years, as expected credit losses start to become write offs? Time will tell.

Performance of the large Nordic banks is at or near its peak right now.

Cost discipline to resurface as top priority

The third headwind hitting the large Nordic banks in 2024 is cost expansion caused by wage inflation and increased development budgets. During the last 12 months, the large Nordic banks have seen sizeable growth in their cost bases with 5 out of 8 Nordic banks in our sample group increasing their costs by more than 10%. Notably, only one bank has reduced its costs over that period. Given the current strong financial performance within the banking sector, investing makes perfect sense. However, cost discipline will have to become top of mind again if income growth slows down and loan losses begin to rise.

In such environment, the banks will have to find ways to lower their costs and that may prove challenging given that much of the current cost increases have been directed at new recruitment and long-term investments. Reducing staff is not an easy nor a quick solution and hence we do not expect the banks to take that route in an effort to reduce the cost base. We expect bank management teams to re-consider their investment expenditure and continue to prioritise – as major challenges still remain to be addressed. Cutting down on long-term investments prematurely could also mean leaving the work unfinished and depending upon the expected outcome this may come with significant unintended consequences.

Currently, many of the large Nordic banks are investing in two main themes i.e. technology and risk management. This is often to address regulatory pressures and compliance demands. Slowing down or stopping these investments means that the banks will have to live longer with legacy technologies or accept higher risk levels. Neither is a good solution so bank management teams will face many tough decisions next year.

Lead with agility and conviction

The challenges posed by the macroeconomic environment will require agility from bank executives as they navigate through the uncertainty. As the same time, they must demonstrate conviction to their fundamental beliefs regarding future competitiveness. Amidst all the challenges, the banks have opportunities ahead such as the rise of generative AI and continued increase in use of cloud technologies. These are significant enablers for delivering more cost-efficient operating models, improving customer service and creating a better employee experience.

The banks need to continue exploring these opportunities with a long-term strategic perspective in mind. This means commitment by the banks to modernise operations and ways of working, even during challenging times. Modernisation of banks’ end-to-end operations is a multi-year – or even a never ending – journey that cannot be started and stopped based on the prevailing economic cycle. We observe some of the Nordic banks to be on this journey but still consider that much more could - and should – be done. The adoption of generative AI seems to progress – albeit slowly – and whilst we recommend caution with the topic given the approval of the EU AI Act - we urge banks to start now and think big.

Top priorities for bank executives will be cost discipline and effective risk management, whilst continuing to invest in a resilient and sustainable future.

To wrap-up 2023

The large Nordic banks have had a very strong 2023 driven by higher interest rates that have pushed the banks’ net interest income significantly higher than in the past years. As inflation falls, we expect the central banks to stop rate hikes and even begin to consider lowering policy rates during 2024. This will slow the banks’ income growth. This factor, combined with rising expected credit losses and an elevated cost base, will create headwinds for the ability of banks’ to sustain this growth. Top priorities for bank executives will be cost discipline and effective risk management, whilst continuing to invest in a resilient and sustainable future. This will require both agility and conviction during 2024, to maximise the benefits from new technologies, seize emerging business opportunities and manage lower profit margins effectively.

_________________________________________

[1] Nordea Bank, Danske Bank, Skandinaviska Enskilda Banken (SEB), Svenska Handelsbanken (SHB), Swedbank, DNB, Nykredit, OP Financial Group (OP)

[2] Deloitte 2024 banking and capital markets outlook and sample banks own forecasts in their Q3/2023 interim results

[3] https://tradingeconomics.com/

Contacts

Mikko Leinonen

Mikko is a Partner and leader of Deloitte’s Banking Consulting practice in Finland. Mikko has +15 of experience in the Nordic banking sector as a leader and business advisor. He is specialised in people, business and technology transformations, including e.g., organisational change, new technology implementations and strategy design. Mikko has deep knowledge of the end-to-end operations of universal banks ranging from the back-end technologies to the front-end customer solutions. Mikko toimii partnerina johtaen Deloitten pankkialan konsultointipalveluita Suomessa. Hänellä on yli 15 vuoden kokemus Pohjoismaisesta pankkisektorista johtavana asiantuntijana ja yritysneuvojana. Mikko on erikoistunut ihmisten, liiketoiminnan ja teknologian muutoksiin, mukaan lukien organisaatiomuutokset, uuden teknologian toteutukset ja strateginen suunnittelu. Hänellä on syvä, kokonaisvaltainen tuntemus yleispankkien toiminnasta aina taustateknologioista asiakasratkaisuihin asti.