Artikkeli

Digital customer experience in the Nordic banking sector

– what is the current pulse?

Changes in all markets and industries have impacted customer expectations regarding digital banking services. Deloitte’s recent Digital Banking Maturity study also indicates that when it comes to digitalization, the gap between the best and the rest has widened. Globally, leading banks are becoming multiservice platforms with offerings in areas such as mobility and healthcare. Simultaneously e-commerce is on the rise, advisory role of banks is growing and UX is becoming a main differentiation.

How do Nordic banks fare in the global comparison? Where should they focus and what could they learn from the global digital leaders?

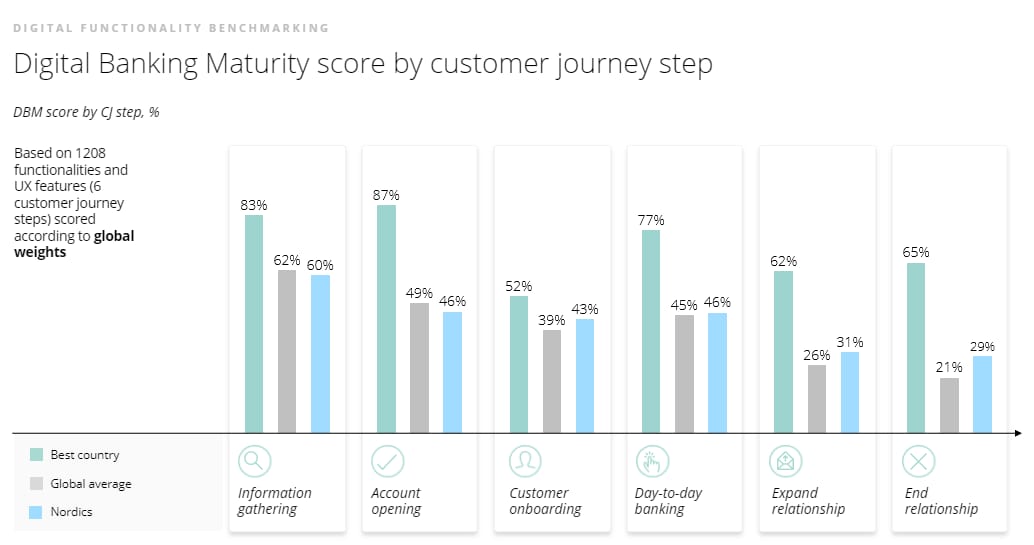

The Digital Banking Maturity study was conducted by following the users through their banking experience journey, from opening an account, through day-to-day banking activities, up to closing an account. Altogether six customer journey steps were under review: information gathering and availability, account opening process, customer onboarding including guidance for new users, day-to-day banking activities, expanding relationship and ending relationship.

Overall, the digital banking maturity scores of the Nordic banks were near the global averages. However, when compared to the global digital leaders, we observed major gaps in almost all assessed categories. This means that the Nordic banks have a lot to learn from their global peers and significant opportunities to improve their digital services.

The biggest advantage digital leaders have built over their competitors is in functionalities that help them expand their customer relationships, e.g., via cross-selling of products and bancassurance. We see this as one of the key areas of focus for the Nordic banks as they pursue their relationship banking strategies. Additionally, while the Nordics banks are not far from their global peers in digital customer onboarding, there is still much improvement opportunities in this area.

“The global digital leaders have separated from the rest especially in card management, personal finance management and cross-selling of products and services. These are all areas we consider critical also for the future competitiveness of the Nordic banks. In addition, fully digital onboarding of customers is a major advantage for any company, and we expect to see improvements also in this domain in the Nordic banking sector in the near future.”, Mikko Leinonen, Banking Consulting Practice Lead from Deloitte Finland says.

Norwegian banks are the digital leaders in the Nordics

The study revealed differences between the various individual Nordic banks and the Nordic banking markets. The Norwegian banks came on top in the comparison demonstrating above average digital capabilities in almost every step on the customer journey.

“The Norwegian banks were frontrunners in creating a cashless society in Norway almost a decade ago, so I am not surprised to see them coming on top also in the overall digital banking experience.” Leinonen contemplates.

Behind the Norwegian banking market were Island and Sweden followed by Finland and Denmark. In all countries there were differences between the individual banks. However, no specific trends or root-causes emerged from the study to explain the differences. Hence, we see this as a prioritization topic for the banks in their overall journey to create end-to-end digital banks where the differences are explained by their current position in the maturity curve. Interestingly, size is not an indicator of success in this area as the study shows both smaller and bigger players reaching the leader category but also falling into the laggard category and anything in between.

"Maturity differences can be explained in multiple ways. Firstly, there are a lot of variances on where these banks stand with their technology platform renewals as they can be seen as major enabler to drive also the experience in digital fronts. Despite this burden, some players have been able to create workarounds to develop modern digital solutions, still using older assets under the hood, while others are still focusing on fixing the fundamentals. Another factor to impact the speed of maturity improvements could be the ability to decide and execute accordingly, pointing to differences in company leadership and development behaviors”, Mikko Helin FSI Industry Lead from Finland states.

The digital transformation of banking will – no doubt – soon push their offering to go beyond banking. In the Nordics we already now see examples of banks providing their customers guidance, paths, and clear descriptions regarding non-financial products and services. Some have even introduced the opportunity to purchase gift cards and take on healthcare and medical packages. Yet, the global digital leaders have taken the game even further by offering agile everyday conveniences such as parking and transport tickets, chance to book hotels, flights, or trains as well as apps to pay with in vending machines.

“Even if some of the global best practice examples of the study such as gamification and the broader ecosystem plays may now seem distant to the Nordic banks, I do believe they should take inspiration from those and stay open to new innovations that could help serve their customer better. That is the only winning recipe in today’s constantly changing world”, Leinonen concludes.

The digital future of customer journey in banking sector – global trends and insights to keep an eye on

The key trends that are shaping banking industry are, among others, development of banking ecosystems, cross-platform solutions and growing advancement of investment and PFM functionalities

Fully digital banking processes

Growing customer expectations encourage more and more banks to enable users to go through processes, such as product opening, in a fully remote way. While for some areas and markets digital presence is becoming a standard (e.g. remote account opening is present in a majority of researched banks), other activities and products are often not yet available online, giving users digital access to only part of the functionalities.

Banking apps as a platform

Best in class banks go beyond providing traditional financial services and offer new value propositions to their customers through third party service providers. This way, financial institutions can increase customer interactions with the bank, as banking apps can become much more than a tool for managing finances, but also platforms covering multiple areas of customer life.

Cross platform and ecosystem solutions

Banks take advantage of cross platform solutions provided by third parties, so they can offer services which make banking more convenient and efficient for the customer.What is more, banks develop APIs and enter into cooperation with FinTechs in order to further strengthen their digital channels and allow ecosystem creation.

Personal finance management

Personal finance management (PFM) functionalities help customers to control the money they spend, predict how they will spend it, save, invest or analyse it. They provide customers easy-to-understand options for managing their money at their fingertips.

Facilitating app usage for all clients

Solutions in social media, on mobile devices and on other non-banking platforms, have become sources of inspiration for banks, which can use, and „copy” gestures and patterns present and known from other apps. Facilitating usage of apps does not only mean implementing patterns familiar to users but also including solutions supporting accessibility – e.g., for clients with hearing or eyesight impairment.

Liberalization of investments

Many banks have realized the potential behind investment services and enable investing in the simplest products after just a few clicks, without the need to engage in lengthy registration processes or paperwork at the branch. Leading players go beyond offering a seamless investment experience and help their clients make better informed decisions. Some example areas are: offering educational content and rewarding users who complete their trainings, setting up an investor profile after the user answers a few questions about their investment goals, financial knowledge, and risk appetite, and recommending investment options that best suit the customer needs.

Challenger banks

Challengers are relatively small banks competing with large long-established banks. Those banks and FinTechs differ from their Incumbent peers and constitute an important share of researched entities (11% out of all researched banks and 19% of Digital champions in the study were challengers).

Mobile catchup

Digital maturity of the mobile channel has grown faster than for internet banking since the 2020 edition of DBM. The mobile channel is still less developed, but the gap is narrowing. Despite those changes, there are still areas where clients prefer to perform banking activities via PC or even by visit in a branch (for example, applying for complicated products like a mortgage).

Digital Banking maturity – full global report available here.

Contact us