United States Economic Forecast

The Q3 2024 forecast indicates how robust consumer spending, high business investment, and lower interest rates have kept optimism about the US economy intact. However, risks like geopolitical tensions and persistently high inflation remain.

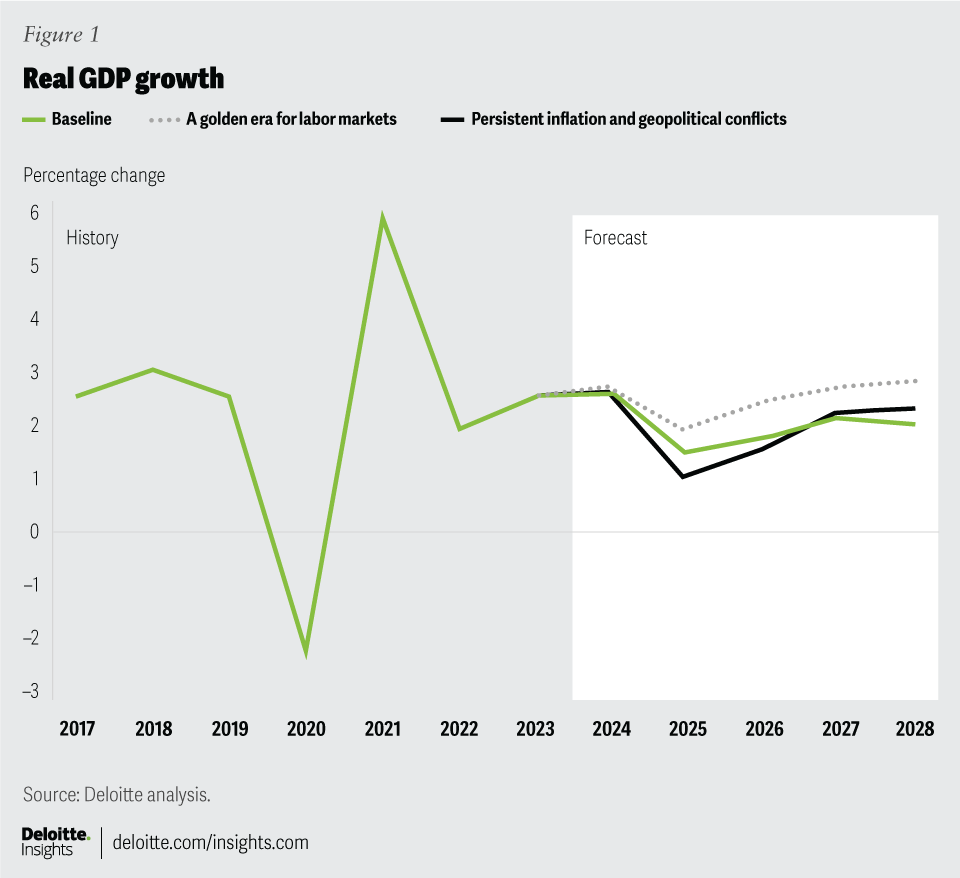

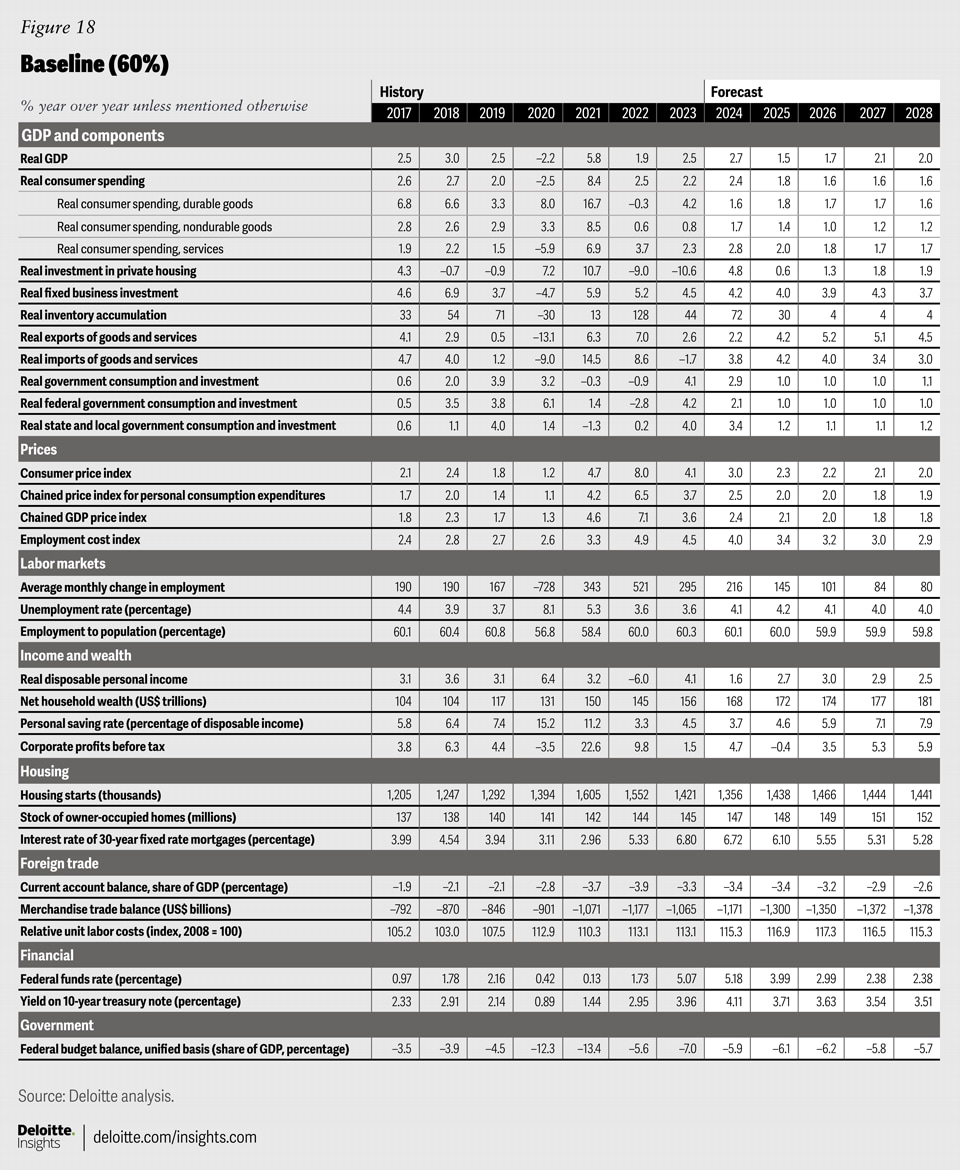

Despite persistent concerns surrounding the durability of growth and interest rate policy, the US economy remains fundamentally strong. While real gross domestic product growth slowed in the first quarter of this year, growth rebounded to a strong 3.0% in the second quarter. All available evidence suggests policymakers may have managed to bring inflation under control without causing a recession.

Deloitte’s baseline scenario remains relatively positive. The boom in factory construction will continue to boost the economy’s potential in the coming years. In the short term, a faster pace of interest rate cuts by the Fed should allow households to take on more debt and support continued growth in consumer spending. Coupled with elevated government consumption, we expect the US economy to grow by 2.7% this year.

In addition to this relatively positive baseline scenario, we include two alternate scenarios: an upside scenario where positive structural changes to the labor market occur in the long run and labor productivity gains exceed our baseline forecast, and a downside scenario that highlights the potential of geopolitical conflict and trade policy to stoke persistent inflation.1

Scenarios

Baseline (60%): Real GDP growth came in stronger than expected in the second quarter of 2024, after slowing in the first quarter. The contrasting results were caused by a big drawdown in inventories in the first quarter, followed by their replenishment in the second quarter; on average, GDP grew at a reasonably strong pace of 2.2% through the first half of this year. We expect GDP to continue growing at a similar pace throughout the remainder of this year before slowing in 2025.

Overall, the story for the US economy remains positive. Consumer spending keeps coming in stronger than expected and is forecasted to rise 2.4% in 2024, slightly more than the 2.2% increase recorded last year. Business investment is predicted to rise 4.2% in this year, down only slightly from the 4.5% growth recorded in 2023. The Inflation Reduction Act and the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act are predicted to keep driving strong gains in structures and machinery and equipment investments, while firms continue to heavily invest in software and other intellectual property like artificial intelligence. On the trade front, growth in exports is expected to slow to 2.2% in 2024 before picking up again the following year, while imports are forecasted to increase 3.8% this year. Government spending is predicted to rise 2.9% in 2024.

Consumer price index (CPI) inflation finally fell below 3.0% in July and is expected to continue decreasing, hitting 2.7% by the fourth quarter. Job growth is forecasted to continue slowing, and we expect demographic changes to continue driving down the labor force participation rate. The unemployment rate has risen to its highest level since October 2021. With inflation on the decline and the unemployment rate on the rise, the Federal Reserve is on track to begin cutting rates in September. We predict the target rate to fall 100 basis points this year and a further 100 basis points in 2025.

Overall, real GDP is expected to increase 2.7% in 2024 and by 1.5% in 2025. Between 2026 and 2028, real GDP growth is forecasted to hover between 1.7% and 2.1% per year.

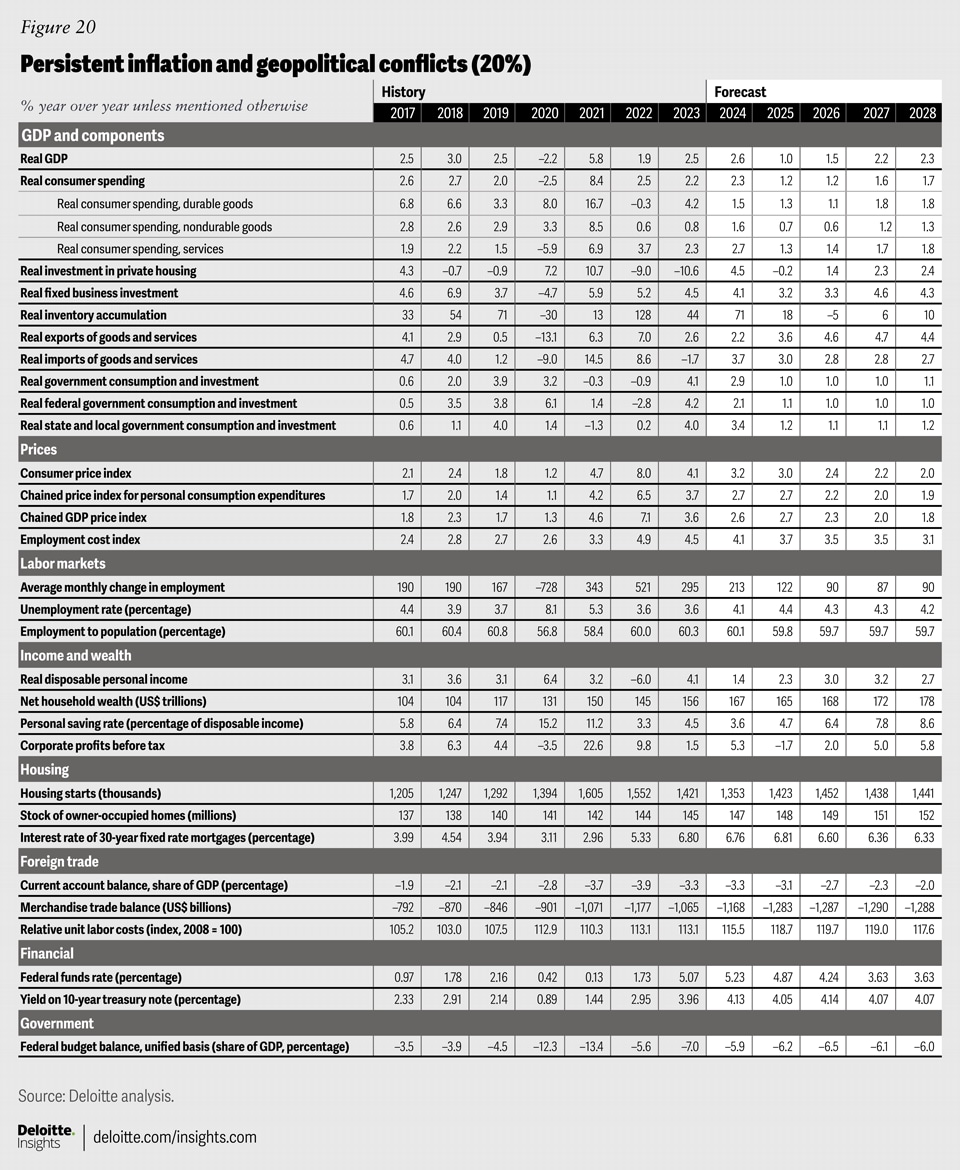

Persistent inflation and geopolitical conflicts (20%): While our baseline remains positive, there are always downside risks to any forecast. We see risks centering around two interrelated issues: 1) geopolitical conflicts and 2) trade policy, which could combine to yield persistent inflation.

Conflicts in Ukraine and the Middle East are at risky stages, and the possibility of escalation is high. Both conflicts are in regions with major petroleum production, and so one likely outcome of escalation could come in the form of higher oil prices. In this scenario, the price of oil rises and remains about US$10 above baseline throughout 2025.

Geopolitical conflicts are not just fought with weapons; trade policy is increasingly a battleground for competition. The US presidential election is in full swing, and both major party candidates appear poised to pursue some degree of tariffs on foreign imports. Though the precise effects depend on the tariff design and implementation, these policies will likely impact prices faced by American firms and consumers. Therefore, in this scenario, we model tariffs that increase the cost of imported intermediate inputs by 1% and of imported final goods by a further 1%.

As a result of the tariffs and the oil price shock, CPI inflation persists above 3% until the third quarter of 2025. Although this scenario still has the same September rate cut as in the baseline scenario, the increased inflationary pressures in late 2024 and 2025 mean the Fed is unable to cut rates further until the end of 2025.

In this scenario, GDP growth is lower compared to the baseline scenario, particularly over the next two years. Growth in 2024 is 2.6%; by the following year, the tariffs are fully implemented and growth in 2025 is just 1.0%. Growth then averages 2.0% per year from 2026 to 2028.

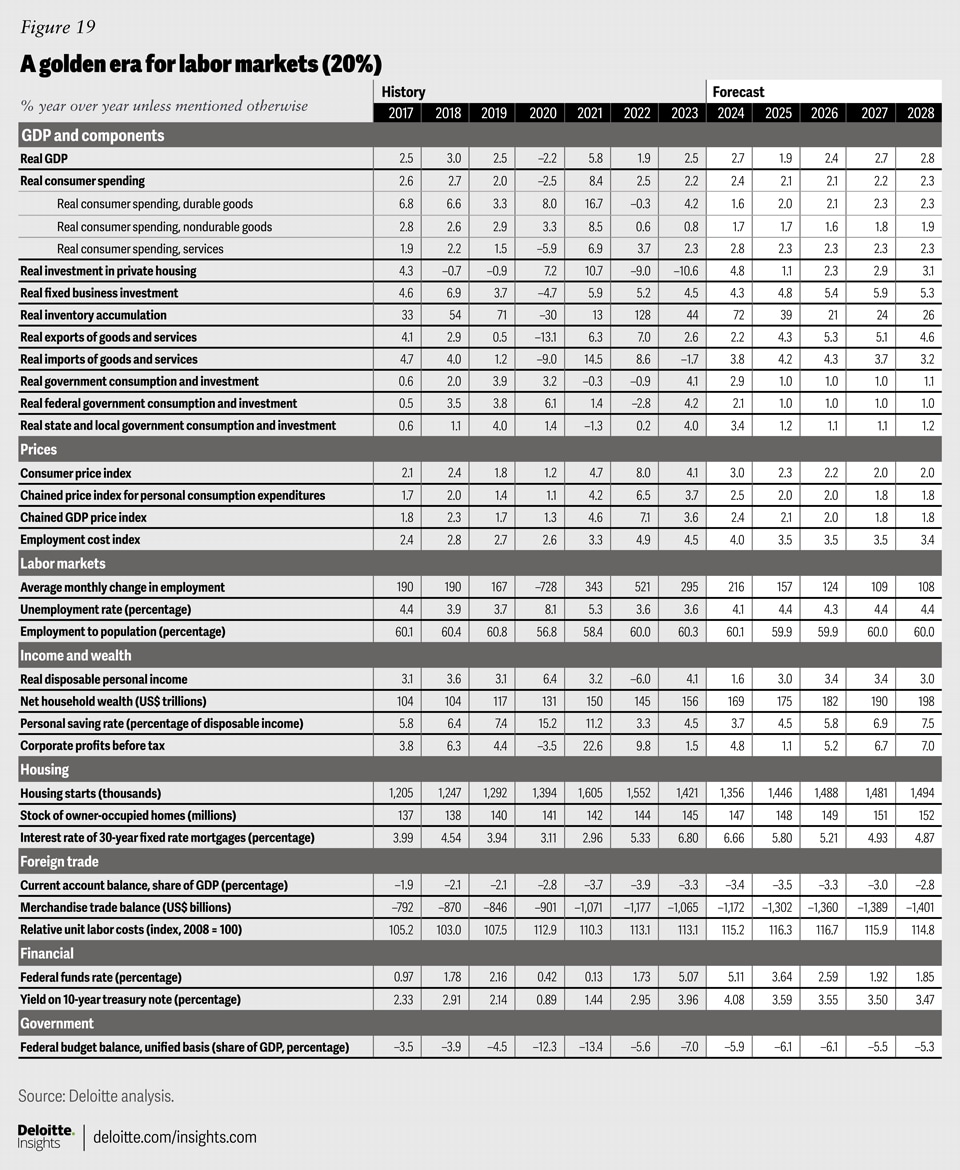

A golden era for labor markets (20%): Over the past few years, firms have been investing heavily in software and technology. Some of these investments—like those in AI—offer the potential to transform certain types of work. Based on an optimistic view of the uptake and usefulness of new technologies, this scenario sees productivity growing by an average of 1.8% per year from 2024 through 2028, compared to 1.5% in the baseline.

In addition to the productivity dividend, this scenario sees higher population growth, contributing to an overall population that is 1.1 million larger than in the baseline scenario by the end of the forecast. Along with a bigger population, we model a higher labor force participation rate, as workers continue to delay retirement. Together, these dynamics result in a higher supply of labor for the economy. More workers lead to more output and more spending in a virtuous circle that lifts the overall economy.

In this scenario, GDP will rise faster than the baseline forecast over the entire forecast horizon. From 2024 through 2028, GDP will increase at an average annual rate of 2.5% per year, 0.5 percentage points higher than the baseline forecast. This scenario also results in higher long-term potential for the economy at 2.8%, compared to 2.2% in the baseline. In that sense, this scenario shows what it would take to make recent rates of economic growth sustainable in the long run.

{kind=link}

Sectors

Consumer spending

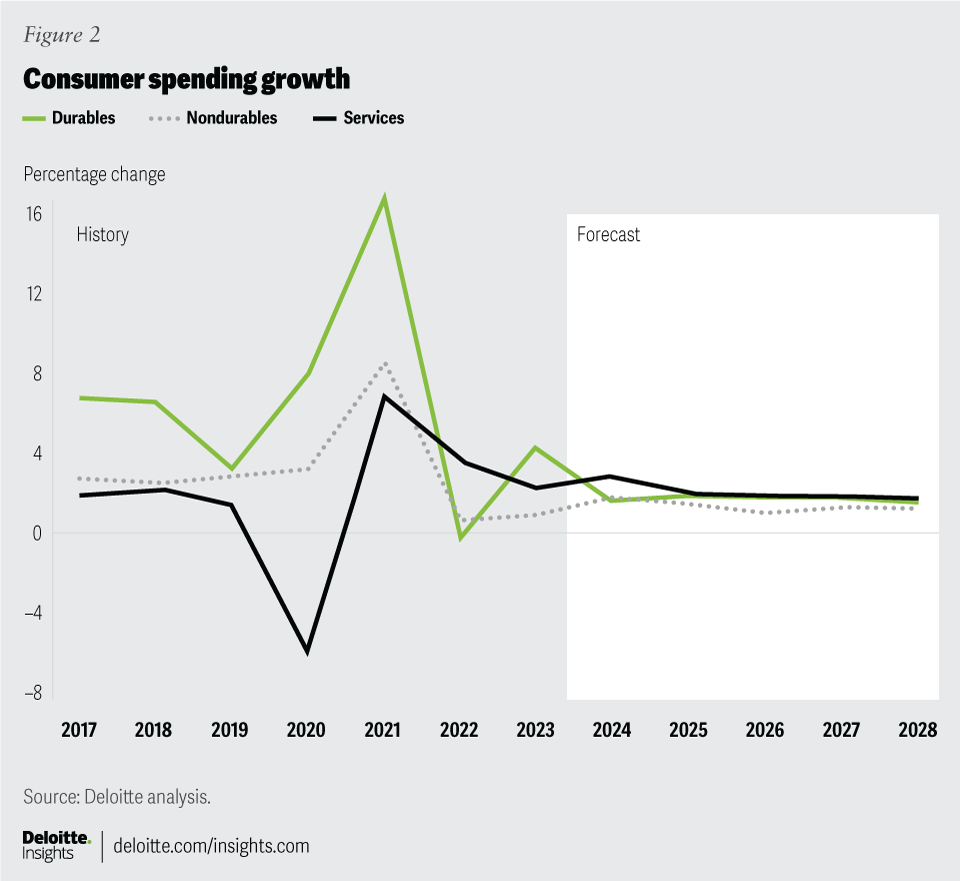

Real consumer spending continues to exceed expectations. In July, real personal consumption expenditure (PCE) rose 0.5% following a 0.3% increase in June. For the second quarter of 2024, overall PCE grew by 2.9% (at annual rates). Spending on durable goods increased 4.9% during the second quarter after falling 4.5% in the first quarter. Increased spending on durables is often seen as a signal of rising consumer confidence.

Households depleted their pandemic-era excess savings in March of this year, 2 and as a result, continuing gains in consumer spending is expected to be driven by growing income and the ability of households to add new debt. Household debt increased US$109 billion in the second quarter, which helped boost consumers’ ability to spend.3

Interest-rate cuts later this year should provide even more room for consumption to rise as households will be able to comfortably take on more debt. We forecast growth in consumer spending to rise again in the third quarter before slowing at the end of the year. Overall, for 2024, we predict real consumer spending to increase 2.4%. Spending on durable goods is expected to rise 1.6% in 2024, and spending on nondurable goods is expected to rise by 1.7%. Interest-rate cuts should drive stronger demand for durable goods next year and throughout the remainder of the forecast. Spending on services is predicted to increase more rapidly than spending on goods, rising 2.8% this year and 2.0% in 2025.

Our headline numbers are already in real (inflation-adjusted) terms, but inflation has an impact on the composition of spending baskets. The Conference Board’s survey of consumer confidence shows that uncertainty around elevated prices, specifically food and grocery prices, remains a key concern for consumers.4 If consumers still feel the price of essentials like food items are rising too rapidly, they could potentially reduce their spending on discretionary goods or services, posing a threat to our consumer spending forecast.

{kind=link}

{kind=link}

Housing

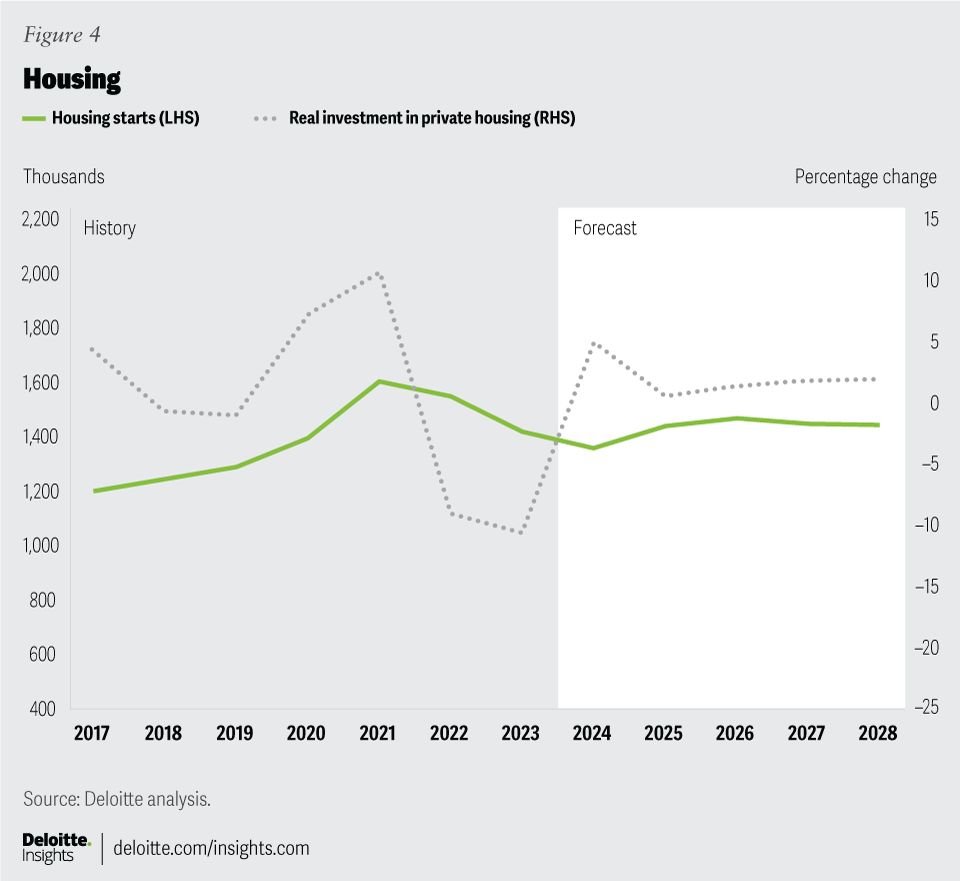

Home sales and construction have been limited so far this summer as interest rates, and consequently mortgage rates, remain elevated. In July, both housing starts and the volume of permits were down, with particularly large declines recorded in the South.5 Furthermore, according to the National Association of Realtors, existing home sales rose 1.3% in July and the median sales was US$422,600, up 4.2% from the same time last year.6

The slowdown in the housing market is expected to cause housing starts to fall in the short term, but as home prices continue to rise, builders may respond with higher starts. We project 1.35 million housing starts this year, down from over 1.4 million recorded in 2023, but in 2025, housing starts are expected to rise to over 1.4 million and remain around that level over the longer term. In 2025 and 2026, the housing stock is expected to rise more rapidly than total population. However, that trend is expected to reverse in the later years of the forecast period. Despite a strong level of construction in the medium term, for there to be a real impact on affordability, more of this new construction will need to be “starter homes” and will need to be built in parts of the country experiencing the largest increases in population. We expect this to remain a challenge. Consequently, the house price index is forecasted to rise 5.0% in 2024, with growth expected to slow to 2.6% in 2025 and remain between 2.2% and 2.4% from 2026 to 2028.

{kind=link}

{kind=link}

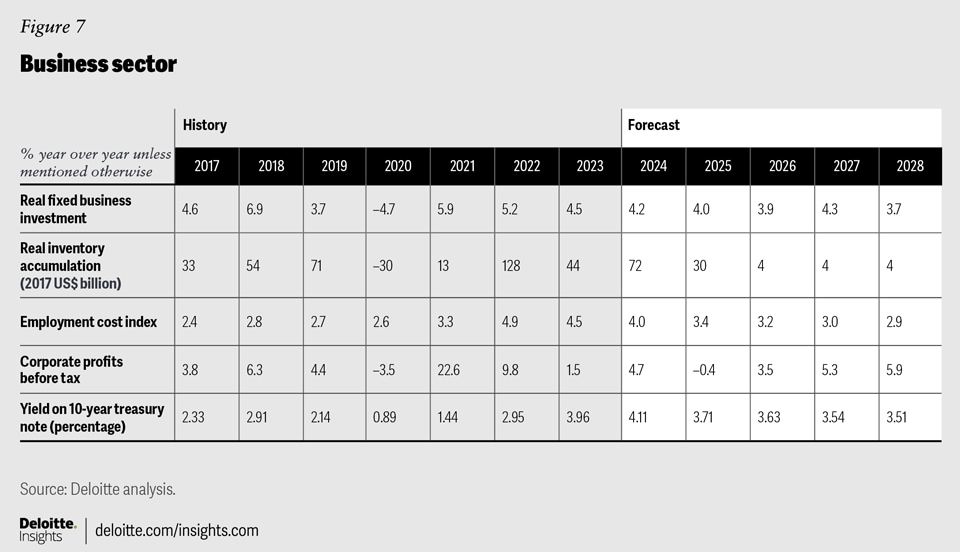

Business investment

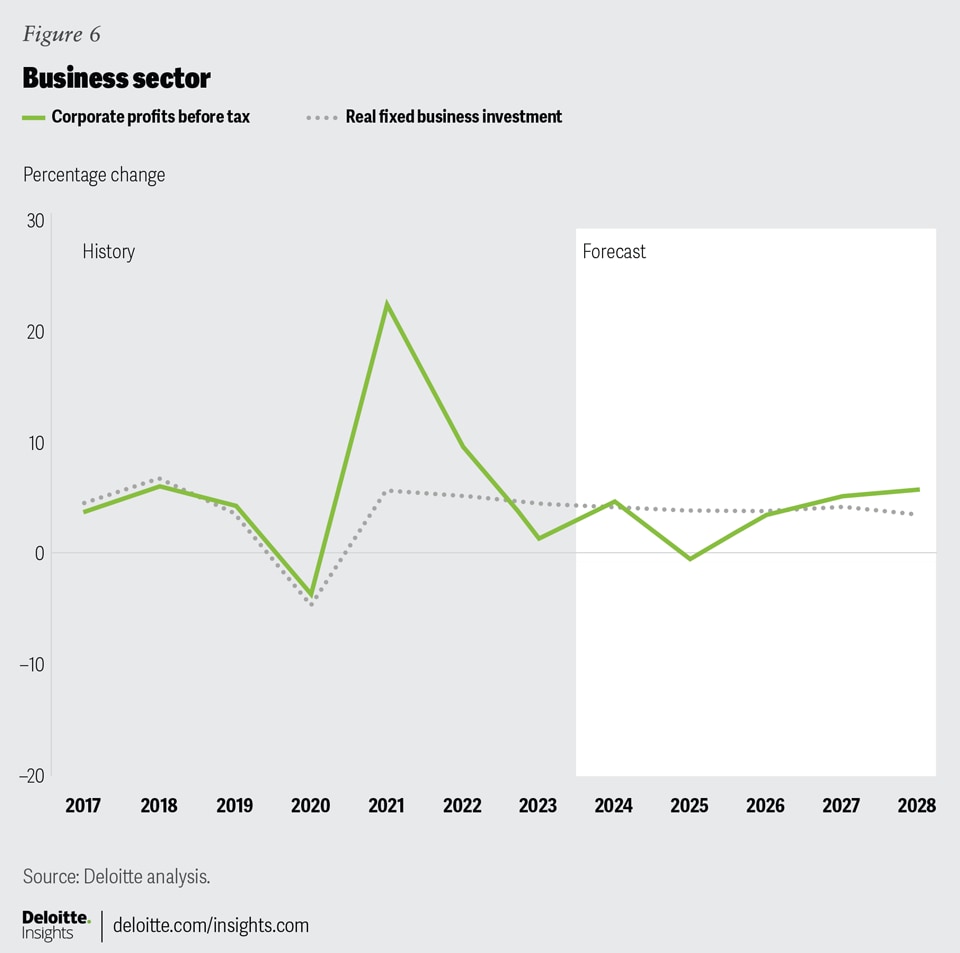

Investment is spending that helps grow the long-term productive capacity of the economy, and as such is the most important sector for understanding an economy’s potential. While higher interest rates are used to combat inflation by reducing demand, they can paradoxically cause inflationary pressures to persist for longer by making it more expensive for firms to invest in the capacity to produce more and relieve supply pressures. The average corporate borrowing rate increased to nearly 7% by the end of 2023 and remained elevated through the first half of 2024, presenting a barrier to firms who need to borrow to invest. However, many firms have cash on hand7 and can avoid borrowing at these rates, and thus, business investment has been coming in stronger than expected since the start of the year. With the Fed predicted to start cutting rates in September, corporate borrowing costs are also expected to fall, which should help further drive growth in business investment. We predict business investment to increase 4.2% in 2024 and another 4.0% in 2025. In the longer term, growth in business investment is expected to remain elevated.

Investment in structures, which includes both buildings and engineering structures such as power plants and oil platforms, has typically followed a cyclical pattern, and is often driven by commodity price booms and economic cycles. However, another factor that has been driving growth in this investment class, especially in manufacturing construction investment, is the passage of the Inflation Reduction Act and the CHIPS and Science Act. These pieces of legislation aimed to increase US production of strategic technologies like electric vehicles, batteries, renewable energy, and semiconductors.8 Since their passage in August of 2022, spending on manufacturing construction has skyrocketed, with investment in structures rising 13.2% in 2023. While the outlook isn’t as rosy for all subsectors (with office space prices down and vacancy rates up, the office segment of the commercial real estate market is expected to remain under stress),9 we forecast that overall investment in structures will rise 5.3% in 2024 and 2.9% in 2025.

As factory construction increases, so does equipment investment and intellectual property investment—categories that capture everything from plant machinery and computers to software has increased since the start of 2024. We predict the rise in manufacturing construction activity to continue to increase investments in equipment and intellectual property throughout this year and next. Overall, the forecast shows spending on business equipment rising 2.6% this year and 4.6% in 2025. This type of spending has seen a strong upward trend over time, and we expect that strong trend growth to remain throughout the rest of the forecast period.

Business investment in intellectual property, which includes not only software purchases but also research and development spending, increased significantly during the pandemic as firms worked to adapt to a new reality of remote work. Growth in intellectual property investment is expected to slow compared to the gains observed in 2021 and 2022 but will remain elevated over the course of the forecast period as many sectors incorporate AI and other technologies.

{kind=link}

{kind=link}

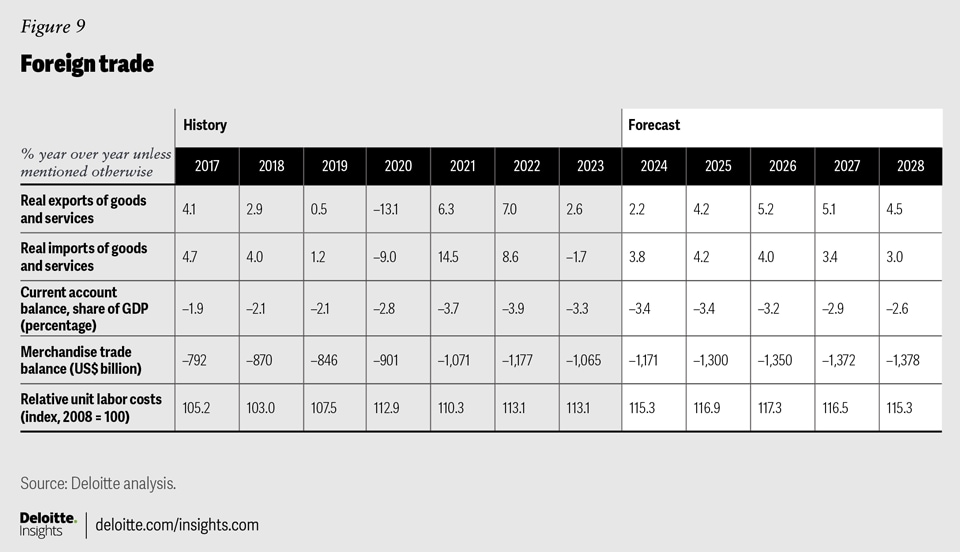

Foreign trade

Export volumes have been hovering around pre-pandemic levels since 2022, while import volumes rose well above pre-pandemic levels starting in 2021. These trends continued into the first half of this year; export growth has slowed while imports continue to rise, widening the trade deficit. Into this context, the US administration announced significant new tariffs on Chinese imports—notably steel, aluminum, and EVs—earlier this year.10 At the time of writing, details of the tariffs had not yet been published. Both the Democratic and Republican presidential candidates are promising further increases in tariffs. In general, the impact of tariffs on Americans will depend on the specifics of their design and implementation. Either administration will be hoping that they can protect American producers of these goods from being undercut by Chinese products without causing significant price increases for American consumers.

It is also worth remarking briefly on some other major trade stories that have fallen out of the headlines. In late 2023 and early 2024, the Panama Canal Authority reduced the number of transits allowed due to low water levels. The drought situation there has now resolved, and as of Aug. 5, 2024, the number of transits allowed through the canal increased to 35, bringing the number of available slots close to the average number of daily trips before water levels started to fall.11 However, climate change may continue to pose similar drought-related risks to this key shipment route in the future.12

At the same time, since the beginning of the Israel-Palestine conflict in October 2023, Houthi forces in Yemen have launched more than 110 attacks on vessels transiting the Red Sea toward the Suez Canal.13 In response, global shipping companies reduced the volume of Suez Canal crossings by 66% between November 2023 and April 2024.14 Vessels have had to be rerouted around the Cape of Hope in South Africa, significantly increasing travel time between Asia and Europe. While US exports and imports are not as reliant on the Suez Canal route, rerouting vessels has caused global transit times to rise, consequently increasing shipping rates and creating capacity shortages as extended voyages reduces the number of ships available.15

Our baseline forecast expects growth in exports to pick back up toward the end of this year and the start of next. However, we expect imports will continue rising faster than exports as consumers continue spending. Overall, in 2024, exports are expected to increase 2.2% and imports are predicted to rise 3.8%.

{kind=link}

{kind=link}

Government policy

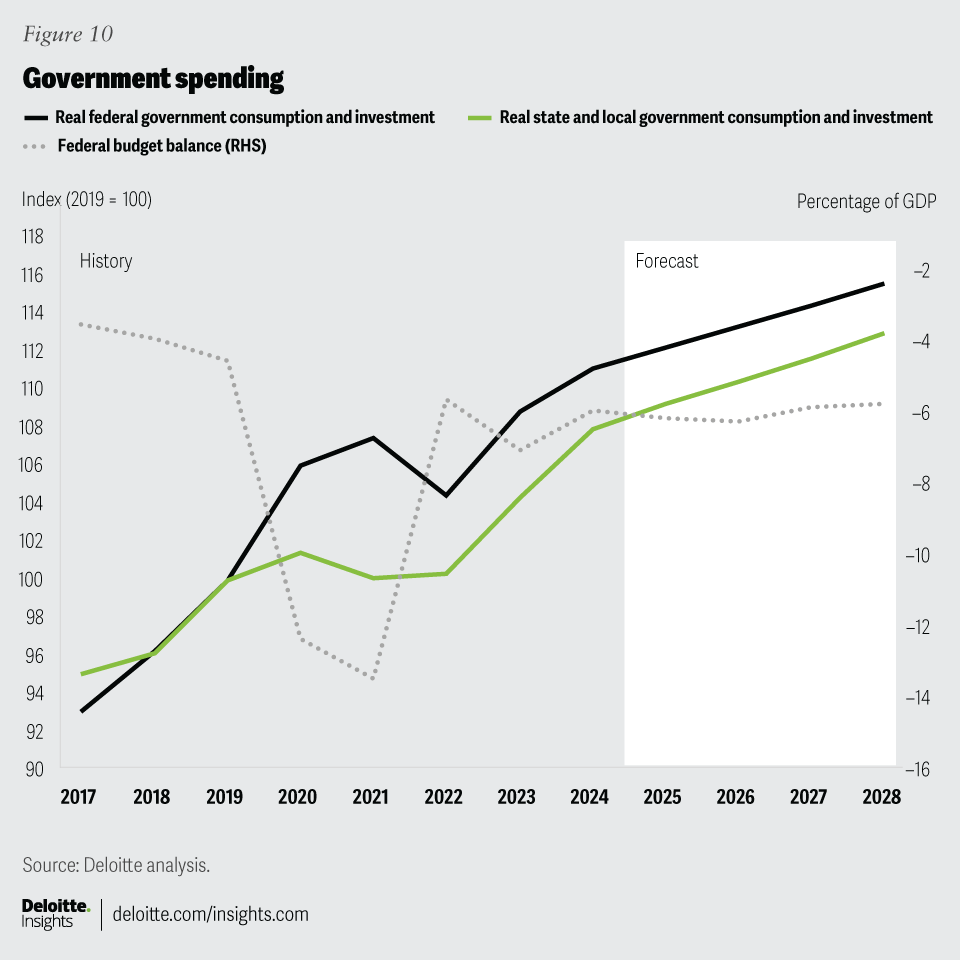

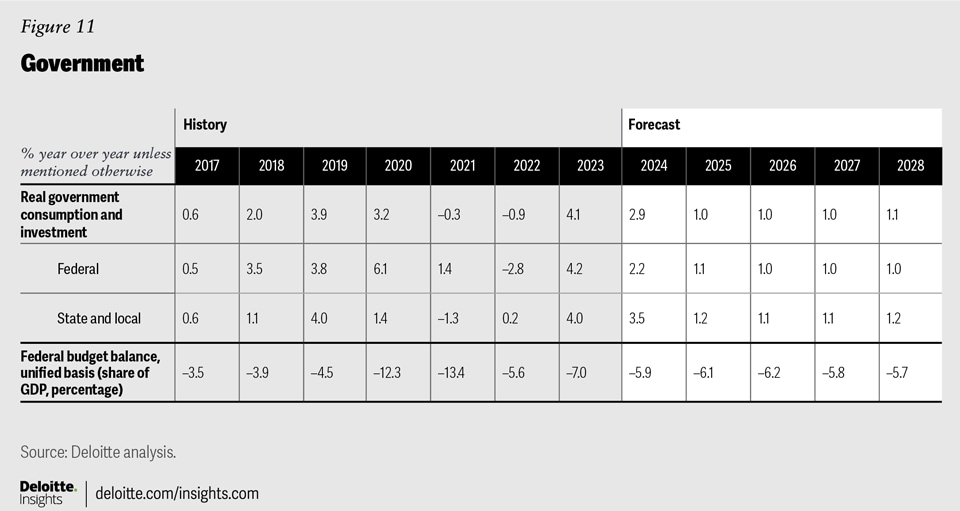

One of the most important policies in recent years has been the Inflation Reduction Act. It aims to reduce the federal deficit, increase investments in domestic manufacturing and energy production, and decrease greenhouse gas emissions by 40% by 2030.16 This 10-year plan is the single largest investment in tackling climate change in American history.17

Despite the Inflation Reduction Act aiming to reduce the federal budget deficit, we predict the deficit as a share of GDP will fall only temporarily, hitting 5.9% in 2024 before rising in 2025 and 2026. The federal government’s future capacity to borrow at current levels will rely on two key factors: investor confidence and the availability of excess savings worldwide. Our forecast anticipates that the 10-year federal bond rate will remain high, but will fall slightly compared to the elevated rates recorded in recent quarters, fluctuating between 3.5% and 4.0% throughout the forecast period.

{kind=link}

{kind=link}

Labor markets

Markets were concerned with the weaker-than-expected July jobs data from the Bureau of Labor Statistics.18 The unemployment rate increased 0.2 percentage points to 4.3%, the highest level recorded since October 2021.19 The rise in the unemployment rate in July was large enough to trigger the Sahm rule, an indicator used by economists as an advance warning that a recession has begun. Our view, and indeed, Claudia Sahm’s view, is that the broad spectrum of data suggests that the July data are not a cause for immediate concern, and that the US labor market remains relatively strong. We predict employment to continue rising over the coming quarters, although at a slightly slower pace than the beginning of the year. By the second quarter of next year, the unemployment rate is expected to start falling slowly, returning below 4.0% by the end of the forecast period. Wage growth will also continue to slow along with inflation.

In the longer term, the demographic shift will play a crucial role in shaping labor supply dynamics. Similar to other developed nations, the United States has an aging population and is experiencing a decline in population growth. However, unlike certain countries, the United States has not reached a stage where the population growth rate is negative. Nevertheless, the slower rate of growth will limit the availability of workers. We believe participation rates within many age groups will continue to rise, especially among the 55-plus age cohort. However, aging will outweigh the increase in participation rates, meaning we expect the overall participation rate to slowly fall over the remainder of the forecast period. Historically, relatively low rates of job growth reflected economic weakness. However, given the new demographic realities, the economy’s sustainable pace of job growth will be limited by the relative lack of available workers.

{kind=link}

{kind=link}

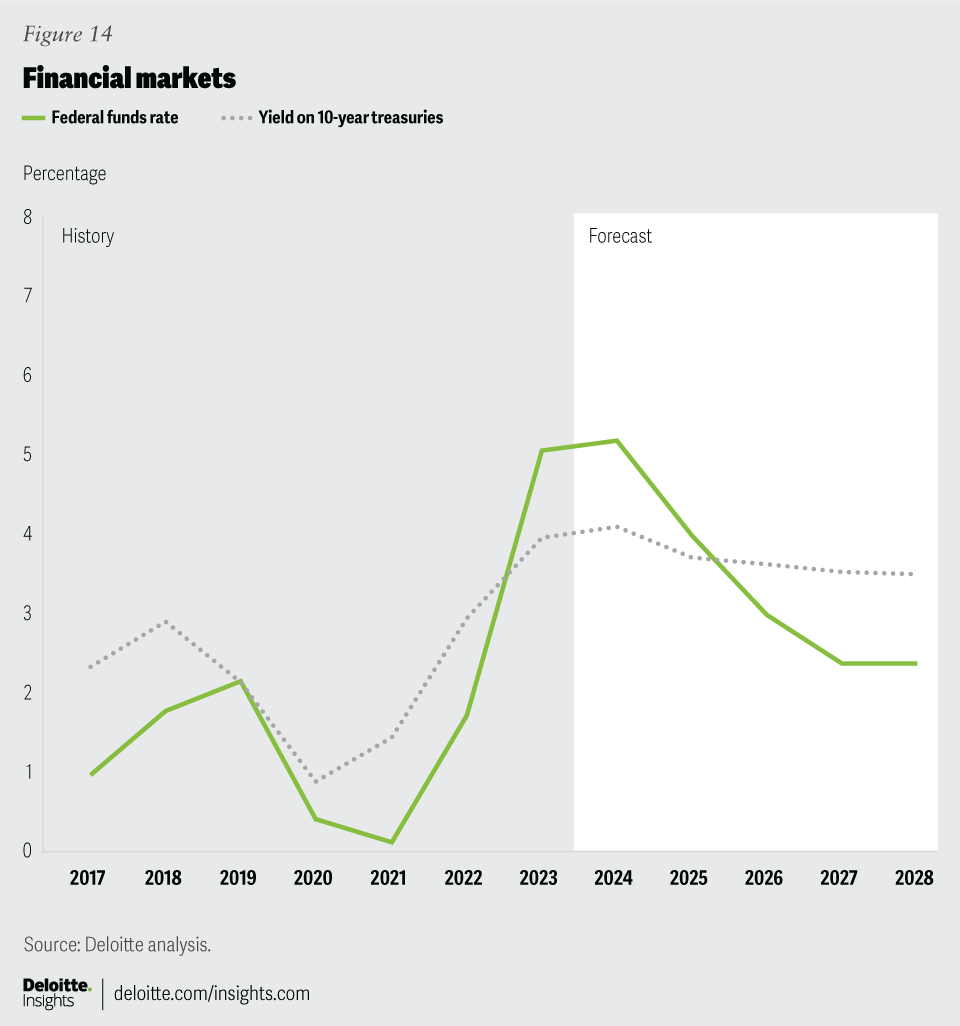

Financial markets

The Federal Open Market Committee has held firm on rates so far this year, but with inflation finally nearing the 2.0% target, the general sentiment in markets is that the Fed will begin cutting rates in September. Our forecast includes a 50-basis-point cut in September, followed by two 25-basis-point cuts in November and December, bringing the Fed’s target rate range to 4.25% to 4.5% by the end of 2024.

One concern noted by some commentators is that the Fed might want to avoid making rate-cut decisions if they are perceived to have an impact on the US presidential election this fall. We don’t believe this is a concern; past evidence suggests that the Fed does not allow election cycles to influence its rate policy.20

However, the Federal Open Market Committee will be closely monitoring the labor market to determine the size of the cut in September and the pace of cuts thereafter. Should July’s uptick in unemployment prove to be a trend rather than a blip, Fed policymakers may feel an even faster pace of cuts is appropriate. We expect rate cuts to continue in 2025 and 2026 as inflation continues to fall, with rates settling at a range of 2.25% to 2.5% by the first quarter of 2027.

{kind=link}

{kind=link}

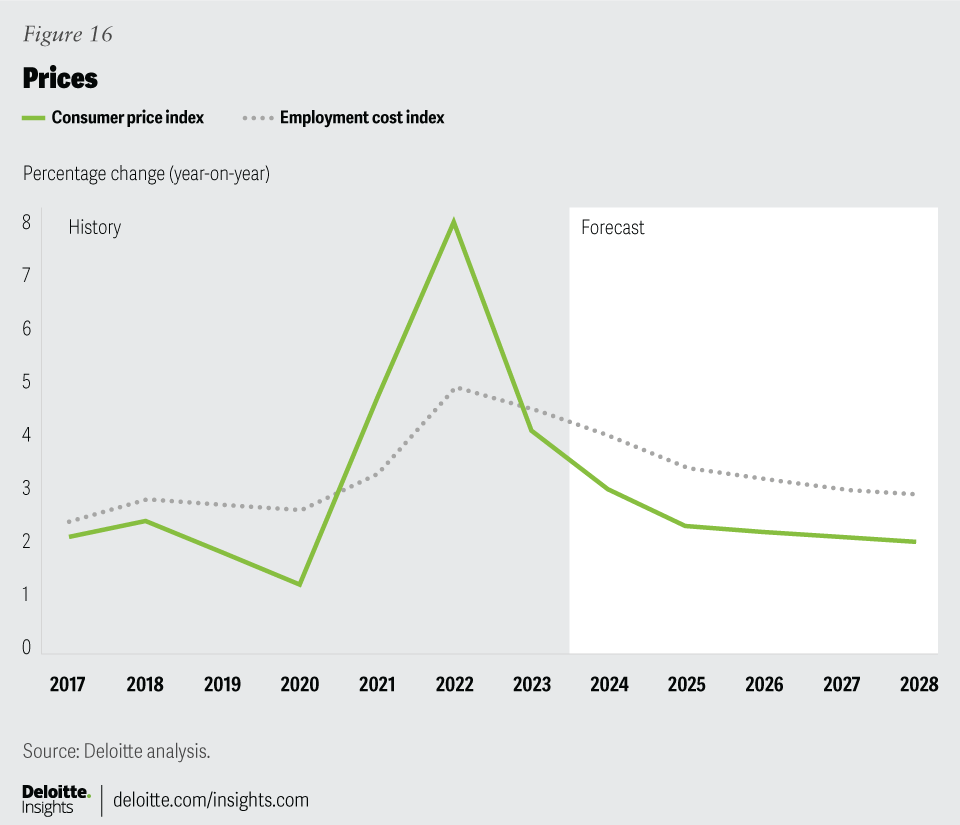

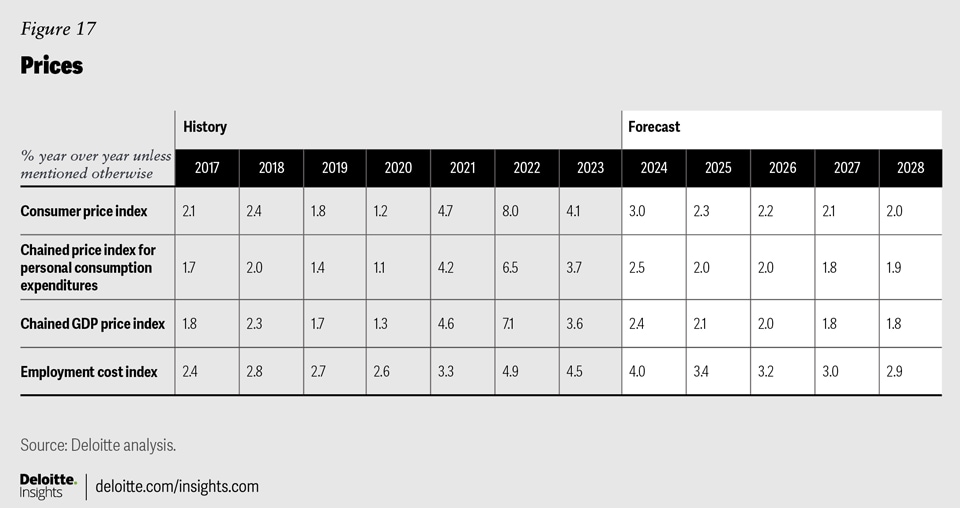

Prices

CPI inflation continues to decline from its peak in the second quarter of 2022. Year-on-year CPI inflation for all items fell to 2.9% in July, finally ticking below the 3.0% mark for the first time since early 2021. The Federal Reserve’s preferred measure of inflation, the PCE deflator, came in at 2.5% year over year in July, inching closer to the Federal Reserve’s target. However, the pace of PCE inflation decrease remains slow, indicating that inflation may not cross the 2.0% threshold for some time.

Our forecast predicts that headline CPI inflation will remain below 3.0% and continue to fall over the coming quarters, in part due to falling energy prices. Core inflation will remain above 3.0% until the first quarter of 2025, as the pace of rate cuts relieves some of the downward pressure on price growth. Overall, our forecast is based on an assumption that long-term trend inflation will converge to 2.0%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}