2024 Deloitte holiday retail survey

Embracing a season of ‘doing’ and discounts

Brian McCarthy

Stephen Rogers

Lupine Skelly

Kusum Raimalani

Our 2024 Deloitte holiday retail survey found that shoppers surveyed are more optimistic and plan to increase their spending by 8% compared to last year.

Learn more

But that’s not what caught our eye.

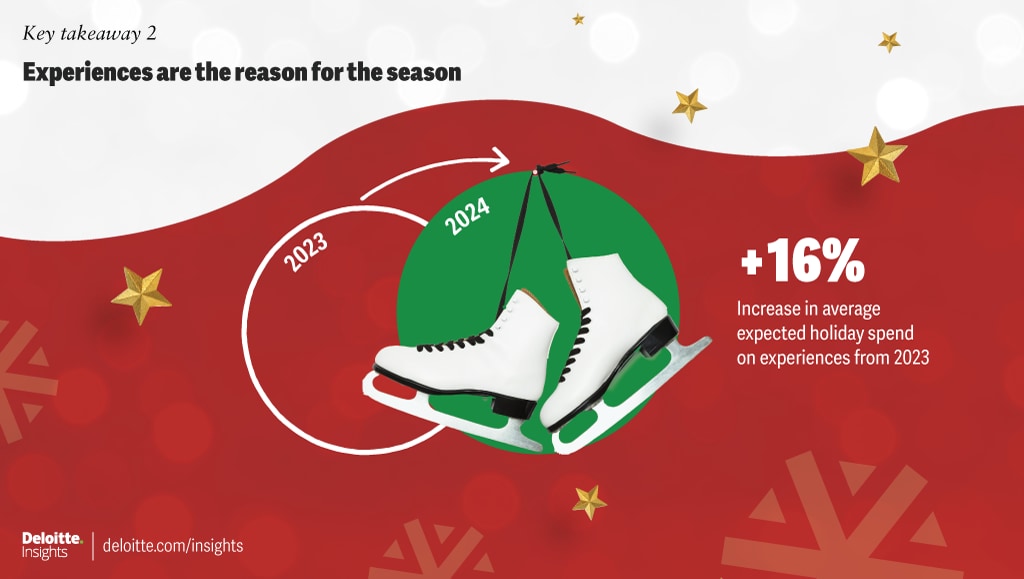

There’s a notable shift toward experiences this season. Our ConsumerSignals data has shown over the last year and a half that consumers surveyed are favoring experiences over goods. The trend is coming through with holiday shoppers as well, as spending on experiences is expected to increase 16% this year.

That’s just one part of the story, however. Consumers surveyed are willing to loosen their purse strings this season, but a cost-of-living squeeze continues to weigh on holiday shoppers. Survey findings indicate that consumers in all income groups are showing frugal and value-seeking behaviors despite optimism around the economy.

To keep the holidays festive, they’re making tradeoffs and seeking out deals with 75% planning to participate in October and November promotional events (versus 61% in 2023). With five fewer shopping days this year, these promotional events may be crucial to tempt consumers to purchase early.

Read on for key takeaways and what they mean for retailers. Download the full survey findings.

The outlook is merry and bright

After expressing record holiday spending intentions in 2023, respondents are yet again planning to up their purchases, and expect to spend $1,778 (+8% year over year) this holiday season. The uptick in spend is attributed to a rosier economic outlook (+9 percentage points [PP]), perceived higher prices (70%), and an increase in spend by the $100K to $199K income group (+17%).

What it means for retailers

Retail executives surveyed echoed consumer optimism, with 80% expecting sales growth this holiday season aided by anticipated traffic growth in both in-store and online channels. However, 78% felt that earlier promotions are pulling sales forward, emphasizing the need for retailers to have the right products and prices early in the season.

Experiences are the reason for the season

As respondents contemplate where to spend their holiday dollars, they are prioritizing experiences (+16% YoY) like holiday events and socializing with loved ones, while gifts spending is expected to be relatively flat (–3% YoY), and nongift purchases such as party apparel and decorations continue to gain in importance (+9% YoY).

What it means for retailers

Given that consumers are looking to travel, host events at home, or participate in holiday concerts and activities, it may be an important time for retailers to take stock of shifting priorities. Having a strong assortment of nongift items like holiday décor and apparel may give retailers an opportunity to gain mindshare with consumers when they choose gifts.

Sugarplums and deals dance in their heads

With 70% of respondents expecting higher prices this season, all income groups are showing signs of frugality. They’re planning to cut back on self-gifting (–16 PP), trade down to more affordable brands (62%) or retailers (48%), and shop promotional events (75% versus 61% in 2023).

What it means for retailers

Of the retail executives surveyed, 76% believe most consumers will value lower prices over brand loyalty. To stand out in a value-focused environment, retailers could consider shoring up loyalty programs and investing in omnichannel experiences to provide the value and convenience that price-wary consumers will likely be looking for.

Watch the video below for more on how retailers can prepare to address consumers’ shifting priorities.

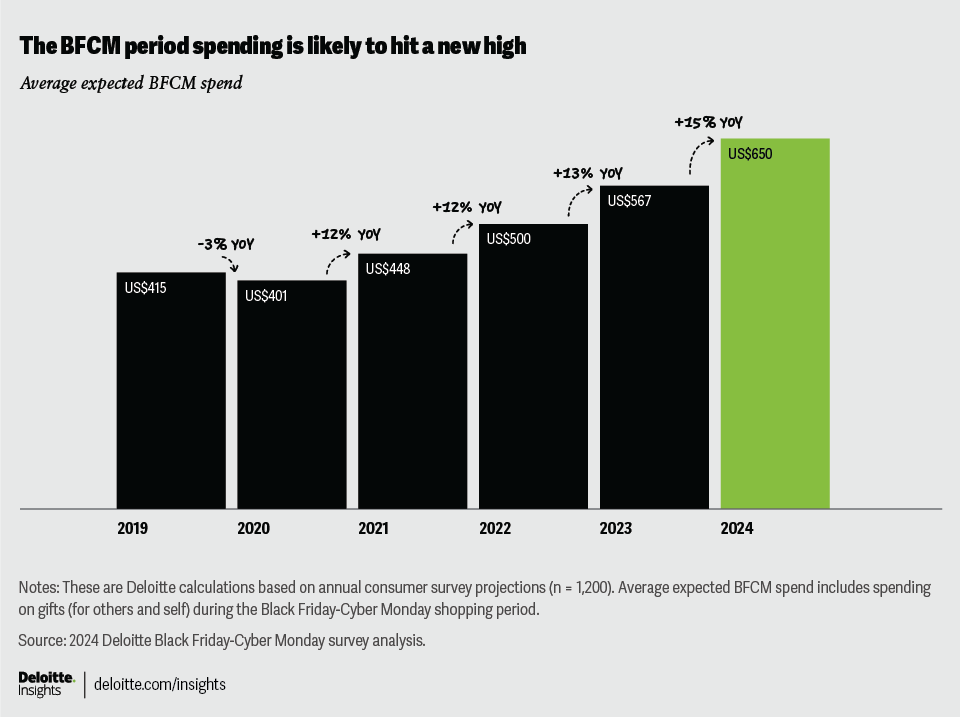

2024 Deloitte Black Friday-Cyber Monday survey trends

Seeking ways to get the most bang for their holiday buck, 80% of those surveyed plan to shop during Black Friday-Cyber Monday (BFCM)—similar to 2023—but spending is set to reach a new high of $650 (+15% versus 2023).

We want to hear

from you!

Complete a brief survey to provide your views on thought leadership content.

{kind=link}

{kind=link}

{kind=link}

{kind=link}