Support for Application of Carbon Neutral (“CN”) Tax Incentives Bookmark has been added

Services

Support for Application of Carbon Neutral (“CN”) Tax Incentives

New tax incentives have been established for companies investing in realization of a decarbonized society

As part of its 2021 tax reform package, the Japanese government introduced new tax incentives related to investments in carbon neutrality (“CN”). The applicable date for the new incentives was upon the revision of the Industrial Competitiveness Enhancement (“ICE”) Act going into effect, which occurred on 2 August 2021. As a result, a tax credit or special depreciation is provided for capital investment leading to corporate decarbonization (temporary measure until 31 March 2024). Deloitte Tohmatsu Group provides one-stop support for the process, from confirmation of various prerequisites to submission of an application for the CN tax incentives.

Explore Content

- Overview of the CN Tax Incentives

- Details of the tax incentives

- Support services offered by Deloitte Tohmatsu Group for application of the CN Tax Incentives

Overview of the CN Tax Incentives

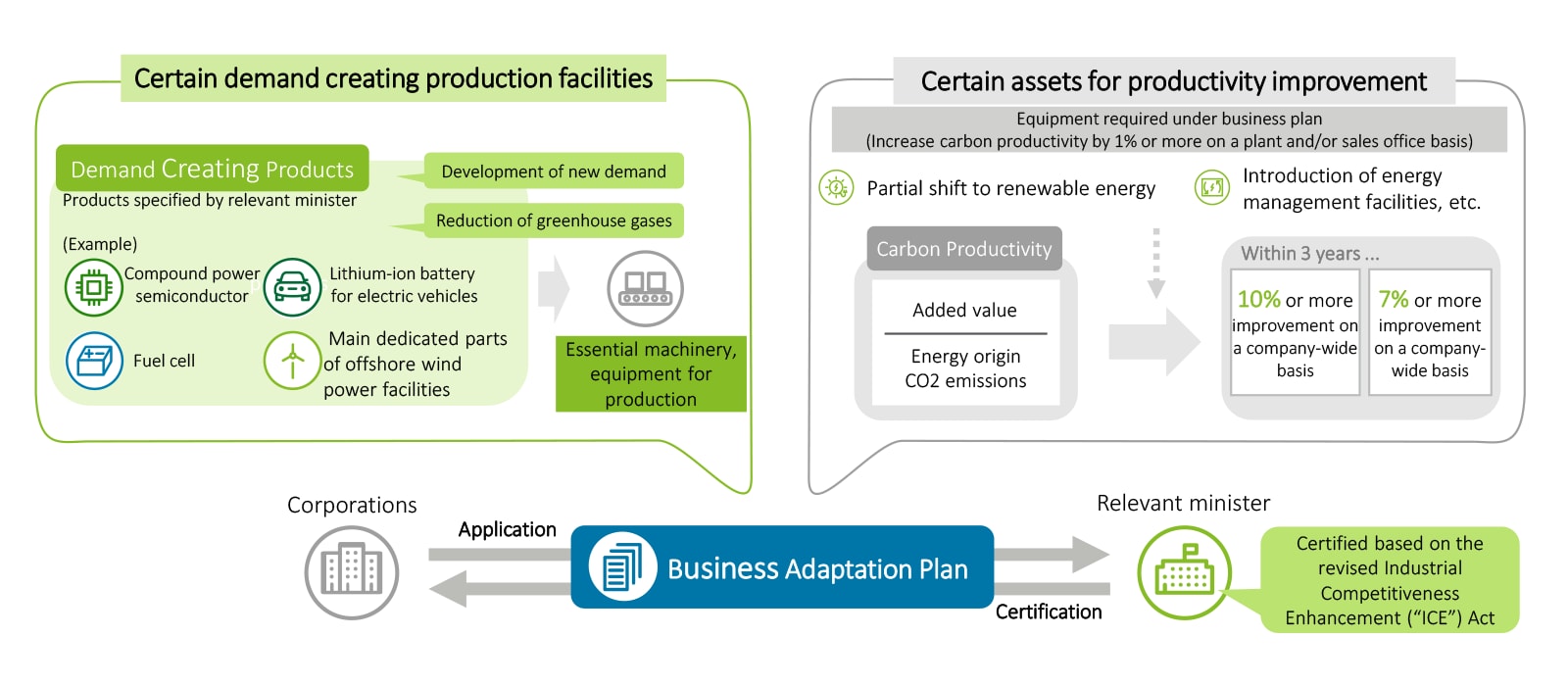

■Certification requirements

In accordance with enforcement of the revised ICE Act, the application process began on 2 August 2021. In order to qualify for the CN tax incentives, the first step is to prepare and submit a business adaptation plan for investments in "certain demand creating production facilities" or "certain assets for productivity improvement" aimed at decarbonization. In applying the tax incentives, it is a prerequisite to obtain certification of the business adaptation plan, based on the process described in the revised ICE Act.

Details of the tax incentives

Applicable companies that qualify for the CN incentives and invest in certain assets that make production processes more carbon efficient, or in production facilities for manufacturing certain carbon efficient products, may choose to take either special depreciation of 50% or a tax credit of 5% (10% for certain assets that significantly contribute to the reduction of greenhouse gases) of the acquisition cost of such assets - up to JPY 50 billion - if acquired based on a business adaptation plan certified under the ICE Act.

Support services offered by Deloitte Tohmatsu Group for application of the CN Tax Incentives

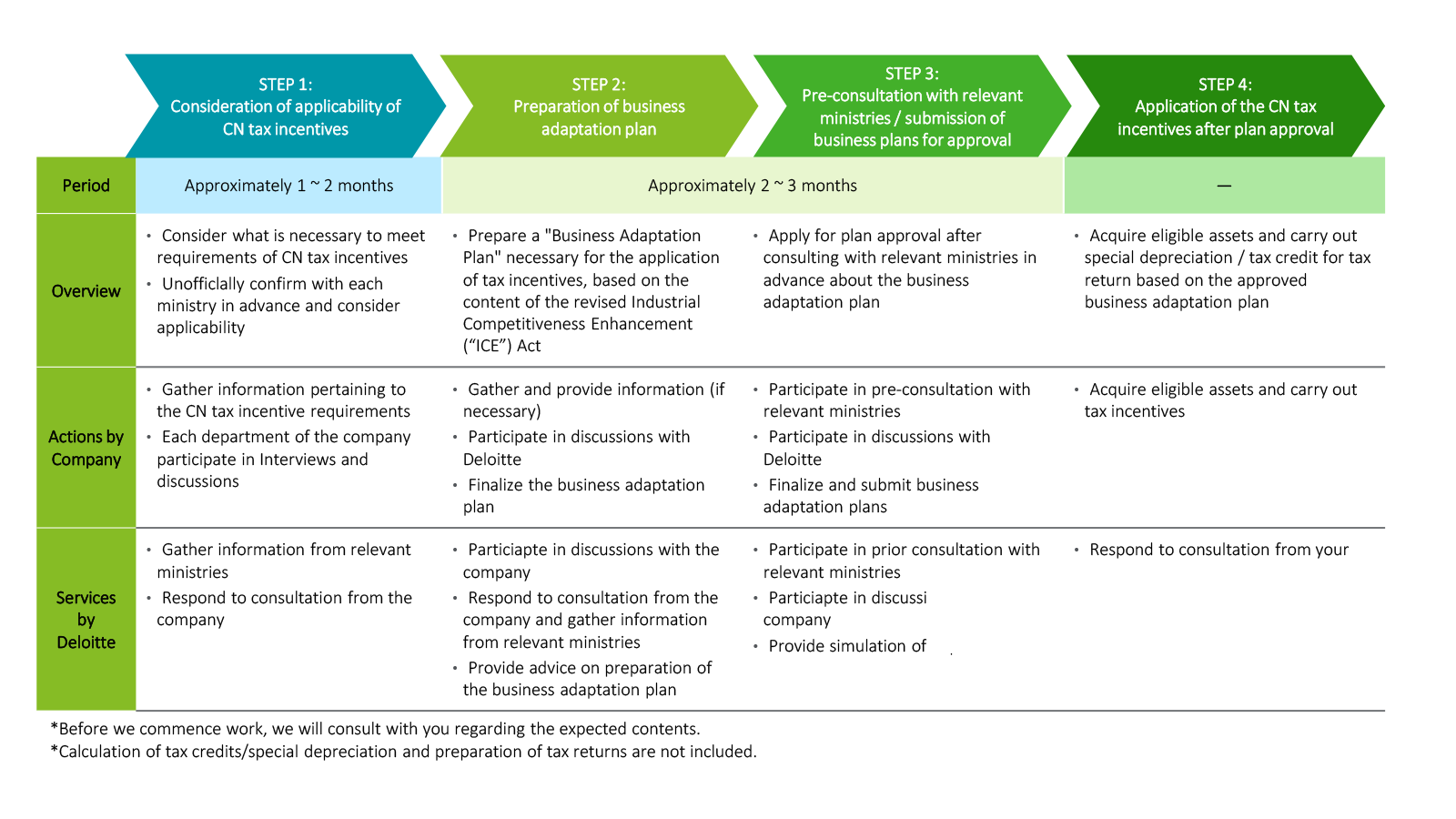

The CN tax incentives will apply to investments made in eligible assets under a certified business plan between the date of enforcement of the ICE Act (i.e., 2 August 2021) and 31 March 2024. Companies may need more than six months preparation to complete the processes to qualify for the CN tax incentives, and in order to meet the requirements, the involvement of multiple departments may be required. Therefore, it is recommended to start the preparation process early and proceed with the processes efficiently.

■CN tax incentives application process

Deloitte Tohmatsu Group offers one-stop support from confirmation of various prerequisites to submission of the application for the CN tax incentives which enables companies to apply the tax incentives with an efficient and effective approach.

Recommendations

Global Investment and Innovation Incentives (Gi3)

Identifying credits and incentives available globally to help secure resources to improve cash flow and reinvestment

Support for Application of DX Tax Incentives

New tax incentives have been established for companies that engage in corporate transformation using digital technology (“DX”)