{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Mexico economic outlook, June 2022 has been saved

Cover image by: Jaime Austin

“A black swan,” according to the writer Nassim Nicholas Taleb, “is an unpredictable event that is beyond what is normally expected of a situation and has potentially severe consequences.”1 The global economy has been jolted by two such events in the last couple of years: the COVID-19 outbreak in 2020 and Russia’s invasion of Ukraine in February this year.

Most countries, including Mexico, have yet to reverse the heavy losses suffered during the pandemic, and those that have somewhat recovered had to implement considerable fiscal expansions that pushed debt levels to record highs. This year, however, economies around the world were preparing to progressively withdraw fiscal and monetary support and instead rely on higher interest rates. And just when they were about to take first steps in this direction, Russia invaded Ukraine.

The war has led to a surge in the prices of a range of commodities to multi-year, or even all-time, highs, as both countries are major exporters of these commodities. This has added considerably to the pandemic-induced inflationary pressures. In such an uncertain business environment, central banks globally have revised their outlooks substantially, confirming the fear that the current rise in inflation is far from transitory.

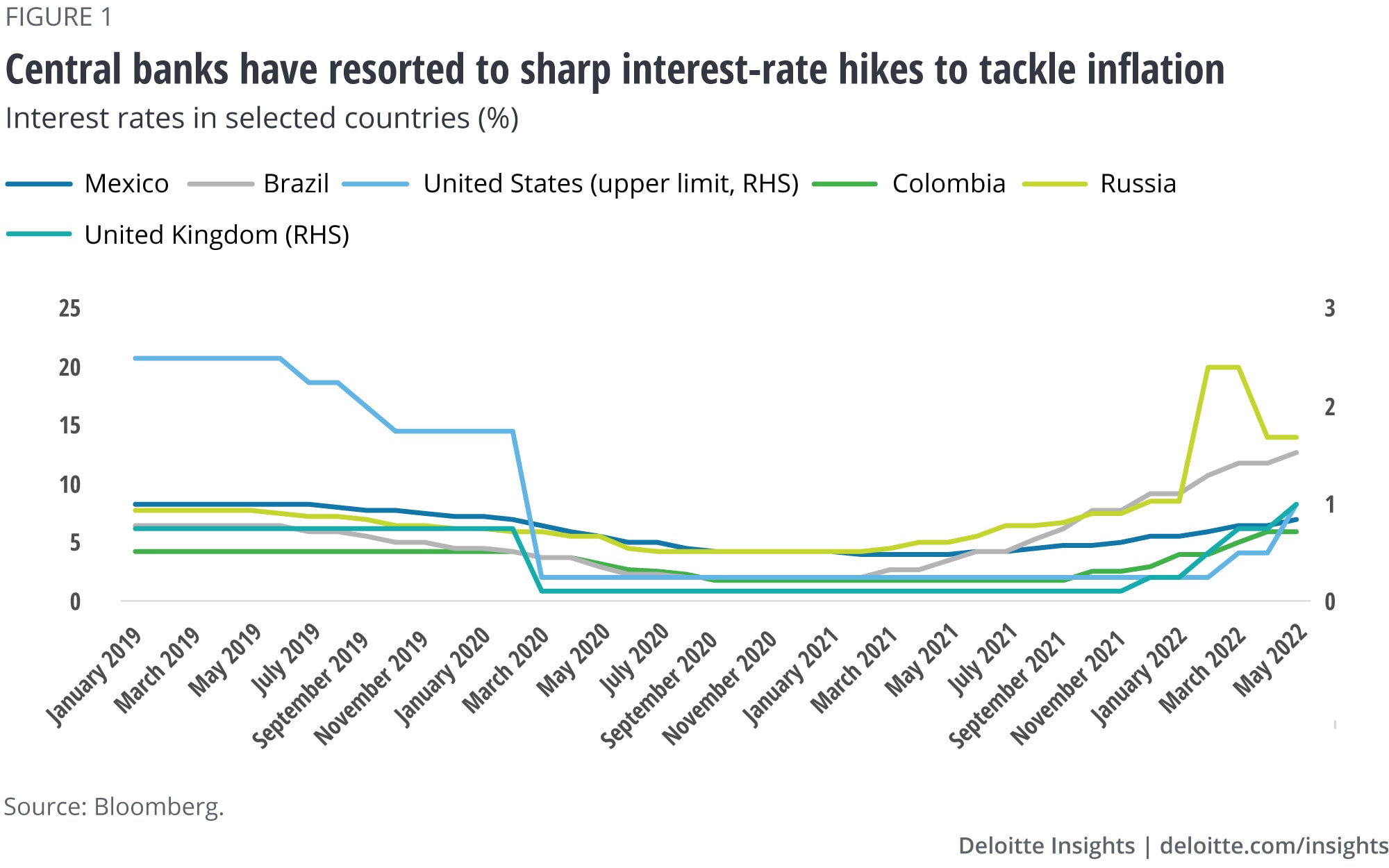

To bring prices back under control, central banks are moving toward a policy of sharp interest-rate hikes. Although in many emerging economies, including Mexico, this trend started last year, central banks of some of the largest economies joined in this year, with the Bank of England and the United States Federal Reserve (Fed) leading the way (figure 1).

This acceleration in rate hikes has increased fears of a recession. In fact, many international financial organizations have started to contemplate the recession scenario in their forecasts; they have begun to reduce their GDP growth projections while increasing those for inflation. The International Monetary Fund (IMF), in its latest publication, reduced its forecast of global GDP to 3.6% from the 4.4% it anticipated in January 2022, while projecting inflation at 5.7% in advanced economies and 8.7% in emerging markets and developing economies—1.8 and 2.8 percentage points higher than that projected in January, respectively.

After experiencing a sharp contraction in 2020 (–8.2%), the Mexican economy grew 4.8% in 2021. This figure, however, masks the variation in growth seen across different economic sectors. For example, agricultural (which account for 3.5% of GDP) and industrial activities (32% of GDP) have resumed growing at prepandemic levels, while services are still running below that threshold. Despite the uptick in 2021, the outlook for this year is not very promising: The economy is estimated to post an annual growth of merely 1.8%. It is only in 2023 that Mexico will likely reach prepandemic levels of growth. GDP per capita, meanwhile, has witnessed a greater setback—at the end of 2020, it was close to what it was in 2009 (figure 2).2 And we expect GDP per capita to recover only from 2023 onward—a scenario that is bound to exacerbate inequality and poverty in the country.

The pandemic pushed a large number of people out of the workforce. Although the number of unemployed has come down considerably from the height of the pandemic in 2020 and 2021, some indicators of the labor market are still depressed. Moreover, considering the economy is expected to expand by only approximately 2% in the next few years, employment will continue to remain an area of concern for Mexico in the near term.

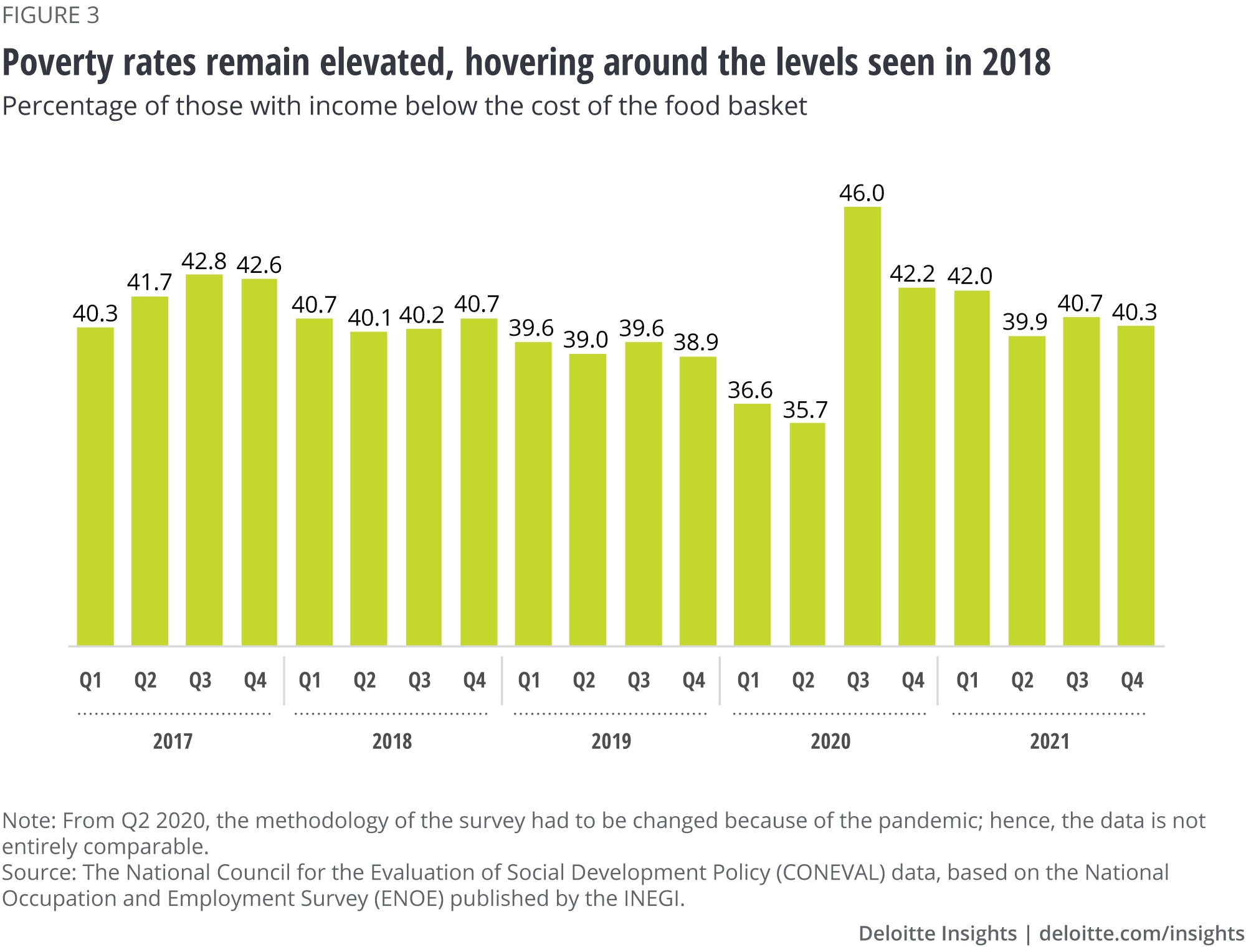

According to the National Institute of Statistics and Geography (INEGI), the number of people with part-time jobs reached 9.0% of the employed population in April 2022. Although a significant improvement compared to May 2020 (29.9%), it is still above the 6.9% recorded at the end of 2019, just before the outbreak of the pandemic.3The National Council for the Evaluation of Social Development Policy (CONEVAL), meanwhile, signaled that the percentage of the population with income below the minimum cost of the food basket slipped to 40.3% in Q4 2021,4 from 46.0% in Q3 2020 (when the pandemic was at its zenith) but still higher than the 38.9% at the end of 2019 (figure 3).

Another factor interrupting Mexico’s economic recovery is the rise in inflation. As in many other parts of the world, inflation is damaging Mexican consumers’ purchasing power by causing a deterioration in real wages. Last May, general inflation in Mexico jumped to 7.65%, the highest in 21 years and only 3 basis points lower than in April. Core inflation, excluding prices of energy and agricultural products, which tend to be more volatile, has also increased since January 2021. Within it, the pressures have been generalized both in goods and services, but it is food prices that have risen the most. Prices of practically all food items are growing at annual rates of more than 4%, and around half of these items are registering variations in excess of 10%. In addition, noncore inflation (agricultural and energy products) continues to be subject to external pressures.

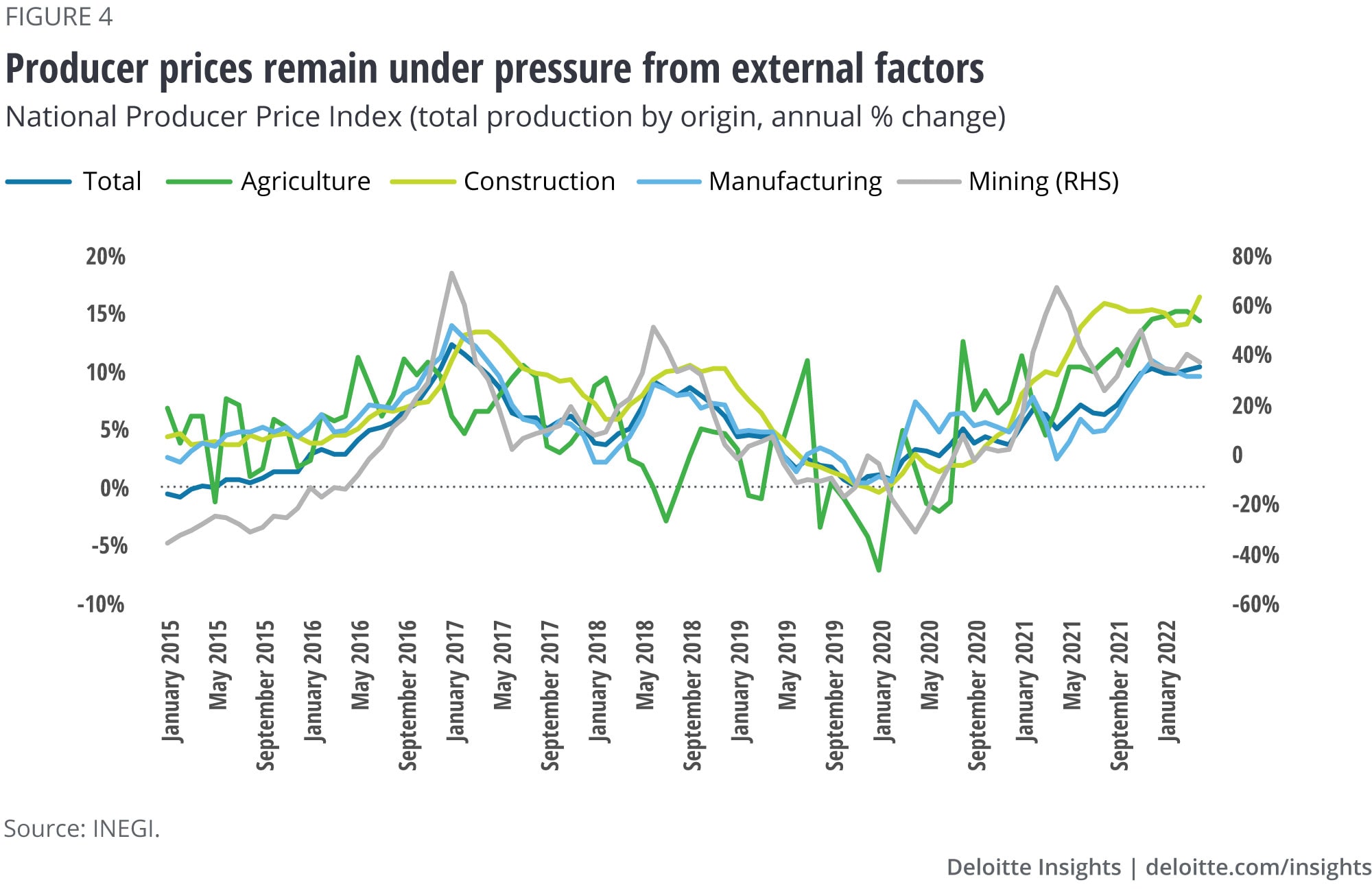

Production costs, meanwhile, remain elevated. Producer prices jumped to an annual rate of 10.5% in May from 9.8% in January5 (figure 4). This is a direct consequence of the rise in the prices of raw materials (such as corn, wheat, soybeans, oil, and other inputs such as fertilizers) due to the Ukraine war.

The central bank of Mexico predicts inflation will peak at 7.0%–8.0% in Q2 20226, and then start a gradual downward trend to close the year at around 7%. Nevertheless, inflationary pressures remain severe, primarily because of the ongoing conflict in Ukraine, but also because of the lingering effects of COVID-19: China, as part of its zero-tolerance policy toward the spread of the virus, recently implemented strict lockdowns in 70 of its cities. This resulted in significant disruptions in Chinese supply chains, which in turn led to delays and shortages globally, likely fueling inflation in key industries.

The Central Bank of Mexico (Banxico) started raising its reference rate in June 2021 in an attempt to keep inflation manageable—between January and June 2021, inflation had jumped from 3.5% to 5.9%. The initial rate hikes were relatively modest at 25 basis points each, but from December 2021 onward, Banxico started acting more aggressively, raising rates by 50 basis points. As a result, the interest rate in Mexico jumped from 4.0% to 7.0% in less than a year. Further, in Banxico’s last meeting, one member suggested that it was imperative to raise interest rates by 75 basis points given the current context, which shows the magnitude of the problem. Given this context and signs of a faster tightening by the Fed, the reference rate in Mexico might finish the year above 9.0%, its highest level since Banxico started keeping records in 2008.

Recently, the Mexican government also unveiled a policy program to tackle inflation.7 The strategy aims to stimulate grain production and support its distribution, write off import tariffs on certain inputs, and reach agreements with businesses to cap product prices. The government expects these measures to have a positive effect on prices of 24 basic products (22 food items and two essential goods) that account for 13.03% of total inflation.8

This policy supplements the actions already implemented on the energy front: fiscal stimulus in response to rising gasoline prices. Last year, the Mexican government found itself in a dilemma. On the one hand, subsidizing fuel prices would have resulted in lower public revenue, which would have negatively impacted public investment. On the other hand, an unchecked rise in fuel prices would have likely had dire social costs and further fueled inflation. It is no surprise, then, that the administration decided in favor of the subsidy—even though, if the current subsidy is maintained throughout 2022, the cost to public finances would be approximately US$16.5 billion, which is equivalent to 5.5% of all public revenue collected in 2021 (1.26% of GDP).9

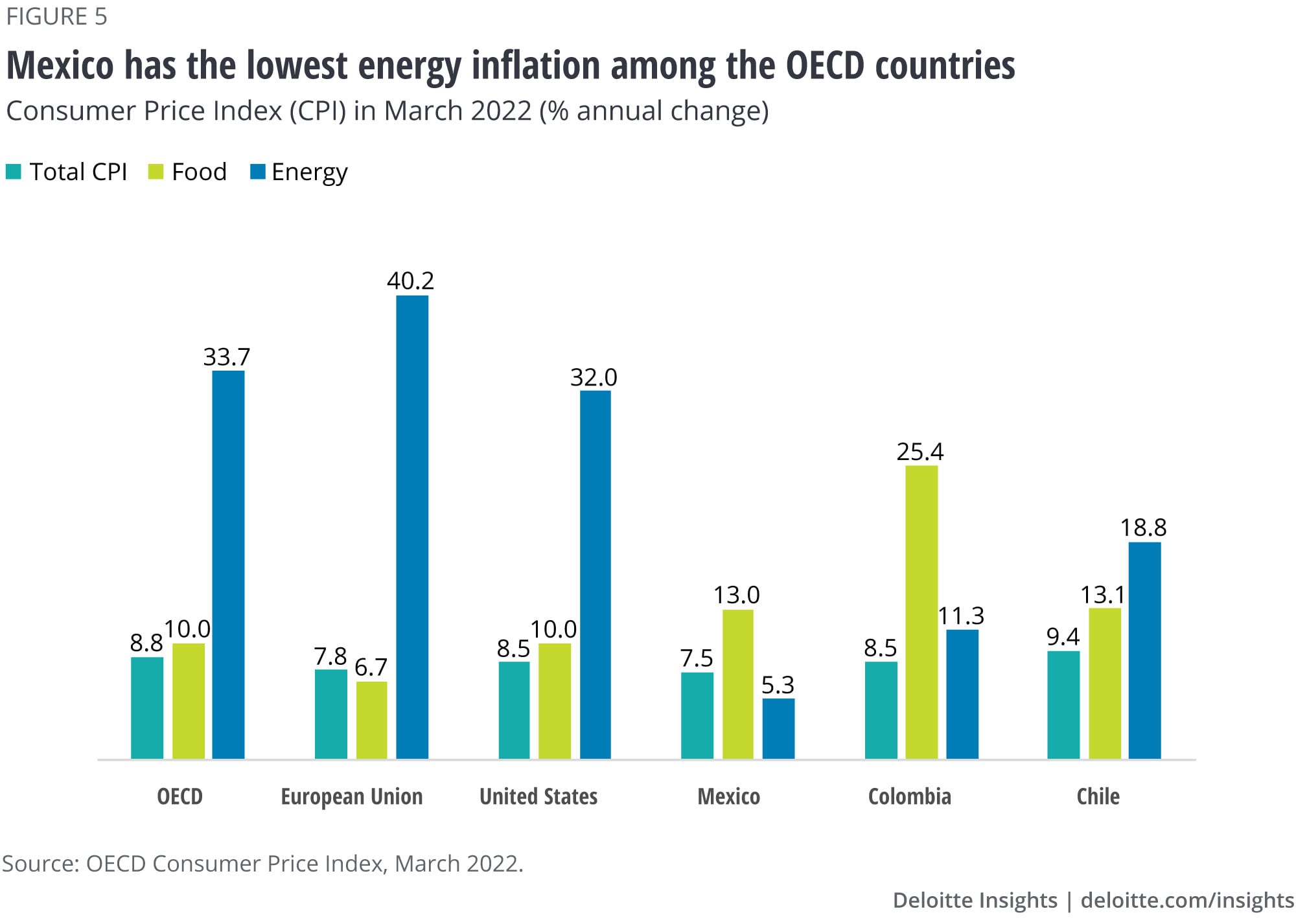

With the subsidy, the government absorbs part or all of the tax charged on gasoline to prevent consumers from paying higher prices. With the additional rise in global oil costs this year, the subsidy has been increased as well, and since the beginning of March, no special tax has been levied on gasoline.10 Recent data published by the Organisation for Economic Cooperation and Development (OECD) shows that, because of government subsidies, Mexico’s energy inflation rate was the lowest among the OECD’s 38 members in March 2022 (figure 5).11 In fact, according to the Ministry of Finance, without a subsidy on gasoline, general inflation in Mexico would have reached 10%.12

The expectation is that lower tax revenues could be offset by profits from oil sales, as Mexico is an important exporter of petroleum products (in 2020 it was ranked fifteenth in the world).13 However, even if elevated oil prices generate higher public revenues, the country is also a major importer of gasoline (it imported 56% of its total gasoline consumption in 2021).14 It looks likely that the net impact on public finances would be negative. Forecasts indicate that if the average price of Mexican crude remains at US$90 this year, public revenues would suffer a net fiscal loss of US$7.7 billion.15 To place this number in perspective, the fiscal loss could exceed the budget allocated to the Ministry of National Defense for 2022 of US$5.2 billion.16

In sum, the anti-inflationary policies and oil subsidies seem to be steps in the right direction, although because of the current geopolitical situation, shocks to commodity prices will continue and logistics issues will take time to solve.

Even before the COVID-19 outbreak, geopolitical and economic changes such as rising protectionism,17 were slowing down the internationalization of production. However, the pandemic—by exposing latent vulnerabilities in global value chains—has made the problem more acute. For example, the stringent lockdowns imposed by China in January 202018 resulted in the suspension of exports of inputs for a range of industries such as automotive, electronics, pharmaceuticals, and medical supplies. Given China’s position as the world's leading exporter of parts and components used in these industries (it accounted for 15% of global shipments in 2018),19 the suspension triggered the closure of factories for several weeks in North America, Europe, Asia, and Latin America.

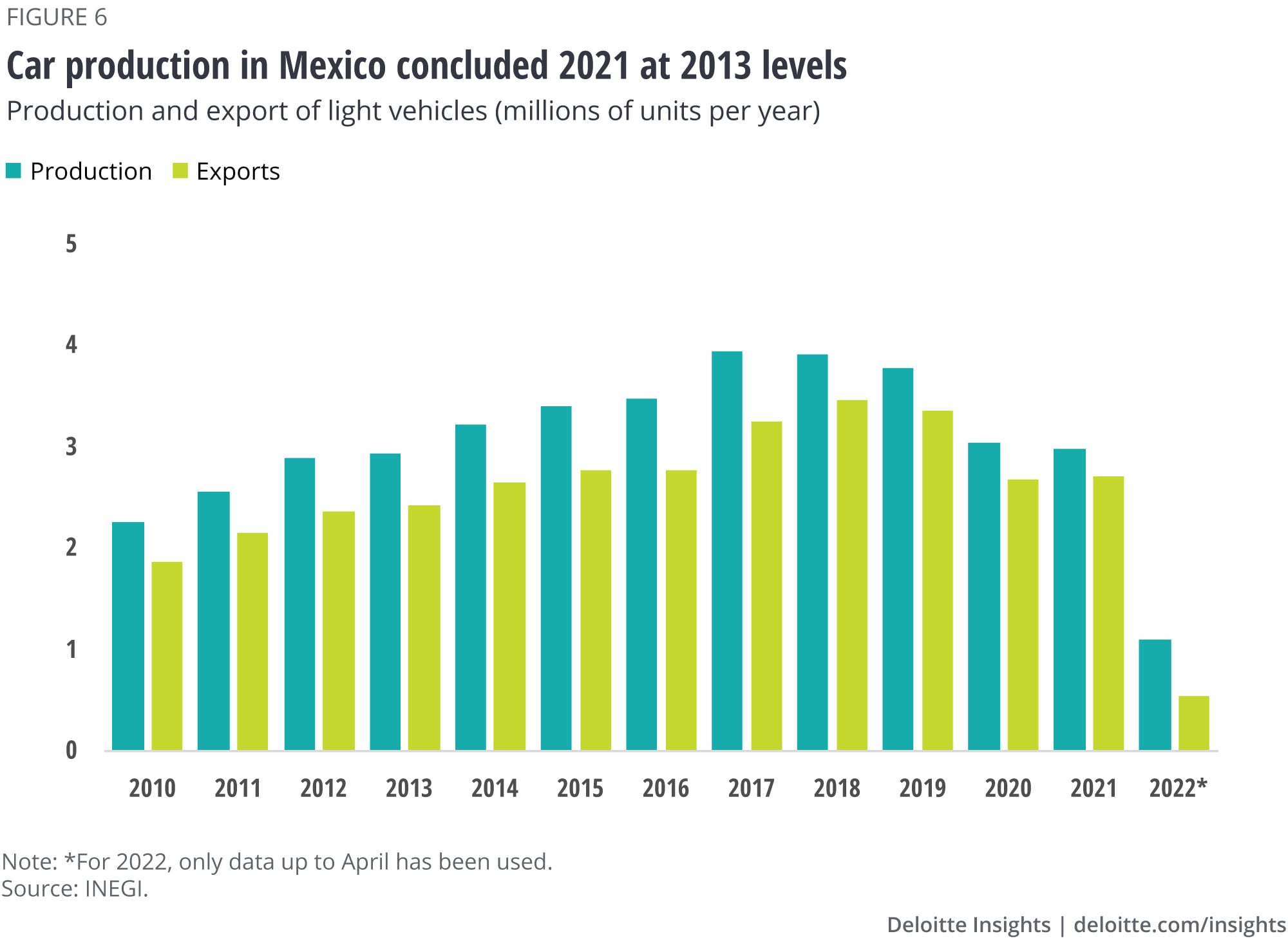

The contraction in intra-regional trade was particularly hard on manufacturing, especially the automotive sector. According to AlixPartners, the chip shortage cost the global auto industry approximately US$210 billion in revenues in 2021 and manufactured 7.7 million fewer vehicles.20 In Mexico, too, the chip shortage’s impact was notable given the important role the automotive sector plays in the national economy: It accounts for 2.8% of GDP and 17% of FDI inflows. Due to the pandemic, the number of cars produced in the country fell by 19.4% in 2020 compared to 2019, and as a result of the chip shortage, the industry could not recover in 2021 and saw production fall by another 2.0%. Car manufacturing in Mexico currently stands 21% below 2019 levels (figure 6).

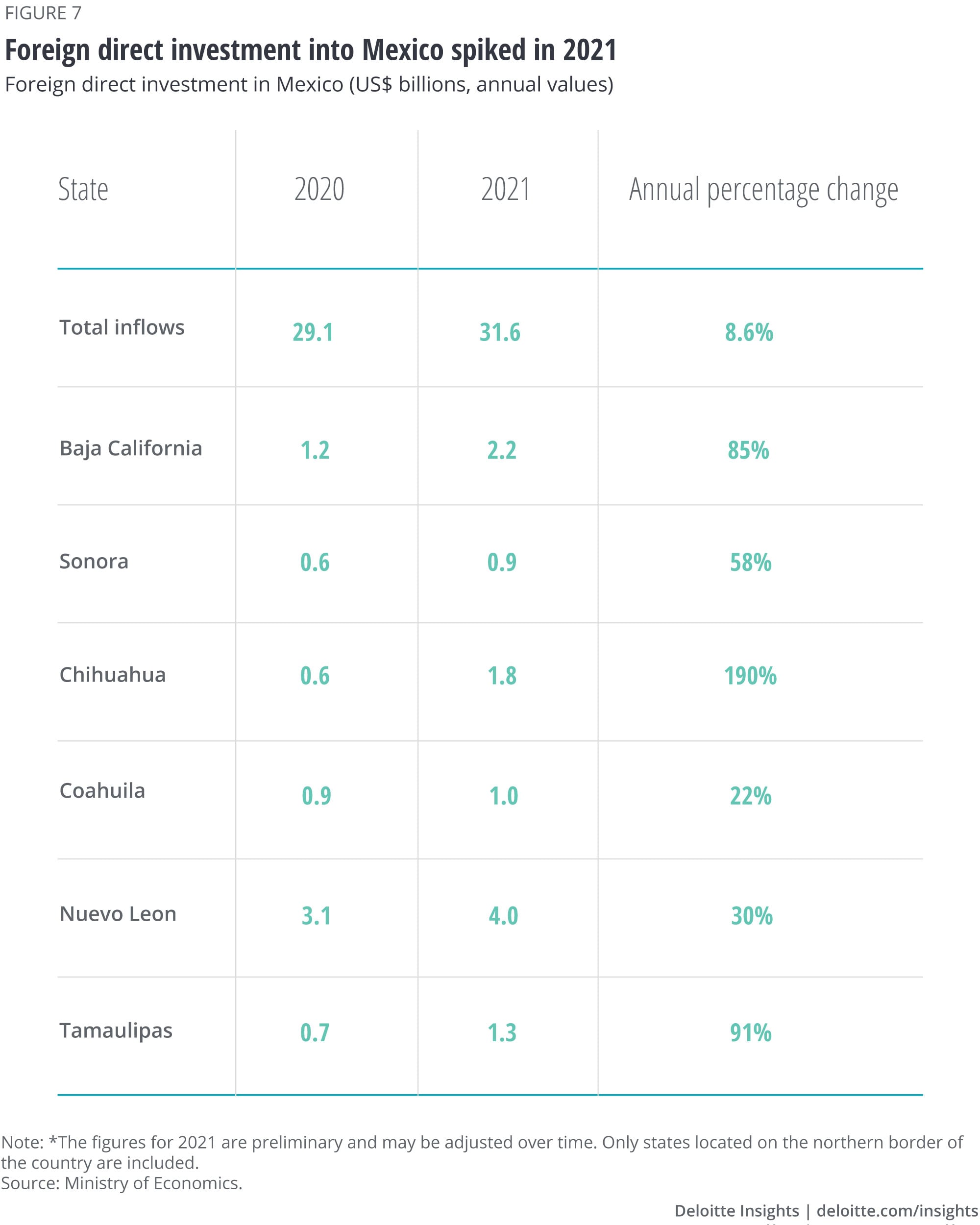

To reduce their vulnerability to supply shortages and bottlenecks, companies have started to reconfigure their global value chains. The net result would not entirely reverse globalization but give rise to a more regionalized world economy organized around three major productive hubs: North America, Europe, and East and Southeast Asia.21 This shift has already started to prove beneficial for the Mexican economy. For example, FDI inflows into Nuevo León (a northern state bordering the United States) went up from US$3.1 billion in 2020 to US$4.0 billion in 2021, an annual increase of 30%. To place this figure in perspective, total FDI inflows into the country increased by 8.7% annually in 2021 (figure 8). These investments, led by Germany, China, the United States, and France, were made mainly in metal products manufacturing (+314% annually), machinery and equipment (+176% annually), computers (+236%), electrical appliances for domestic use (+1,210%), and auto parts (+125%)—industries that have been hit hard by supply shortages and bottlenecks.

Similarly, in Baja California, FDI grew by 85% annually, going from US$1.2 billion in 2020 to US$2.2 billion in 2021. These investments, mainly by the United States, Korea, Germany, and Sweden, focused on the steel and iron industry (+287% annually), metal parts manufacturing (+191%), audio and video equipment production (+275%), auto parts (+108%), and electrical appliances for domestic use (+76%). Many other states, mostly in the north, have seen similar levels of investment (figure 7).

In our last edition of the Mexico economic outlook,22 we stressed that its geographical proximity to the United States makes Mexico an attractive nearshoring destination for US businesses. We now have data that presumably shows how nearshoring has benefited Mexico. Nevertheless, Mexico should continue to work on improving its domestic business environment to realize its full economic potential, considering that some domestic policy decisions that had been focused on restricting private participation and expanding the role of the state in the affairs of the economy, could prove to be barriers to long-term growth.

In summary, the global economy will continue to suffer as long as the war in Ukraine, the economic slowdown in China, supply-chain disruptions, and high inflation and interest rates continue. This is bound to have a negative impact on the Mexican economy. Although Mexico can do little to control these external shocks, it can improve the investment environment domestically and implement major industrial-policy efforts to overcome global market fragmentation. Regional integration remains a potential opportunity to diversify the productive structure and achieve higher productivity growth.