{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

“Transitory” inflation? When dizzying demand meets stifled supply has been saved

Cover image by: Molly Woodworth

Imagine a bunch of raucous friends arrive unexpectedly at your doorstep. They are hungry and demand that you whip up a storm in the kitchen. Not surprisingly, you don’t have all the ingredients and the malfunctioning chimney is likely to slow you down. Your hungry guests might be in for a long wait.

Global supply chains for everything from mobile phones to cars are a tad more complex than your most complicated recipe. And current global supply constraints are stickier and indeed more menacing than an understocked pantry. But whether it’s your kitchen or a global factory, a sudden jump in demand, especially when supply is constrained, is going to leave somebody—maybe a lot of people—unsatisfied.

In our analogy, central banks are akin to the empathetic friend who keeps the guests lively while they wait. Unfortunately, this friend is unable to lend a helping hand in the kitchen. They could curb the expectations of the famished lot, but they don’t want to be heavy-handed lest it be unnecessarily rude. So, they hold their horses. The situation is more likely to be transitory; the guests will eventually get fed and leave; you can restock the pantry and fix the chimney when the ordeal ends.

Producers across the globe are facing a situation in which stifled supply is being overburdened by very strong and lopsided demand. Prices for energy, food, housing, and goods, especially durable goods such as vehicles, have risen sharply as factories struggle to keep pace with strong consumer demand shaped by pandemic-induced behavior and buying patterns.1 Even though inflationary pressures are likely to persist for longer than we initially anticipated, we continue to believe that these pressures are more likely to be transitory than persistent. Nevertheless, central banks are very likely to be under pressure over the short to medium term.

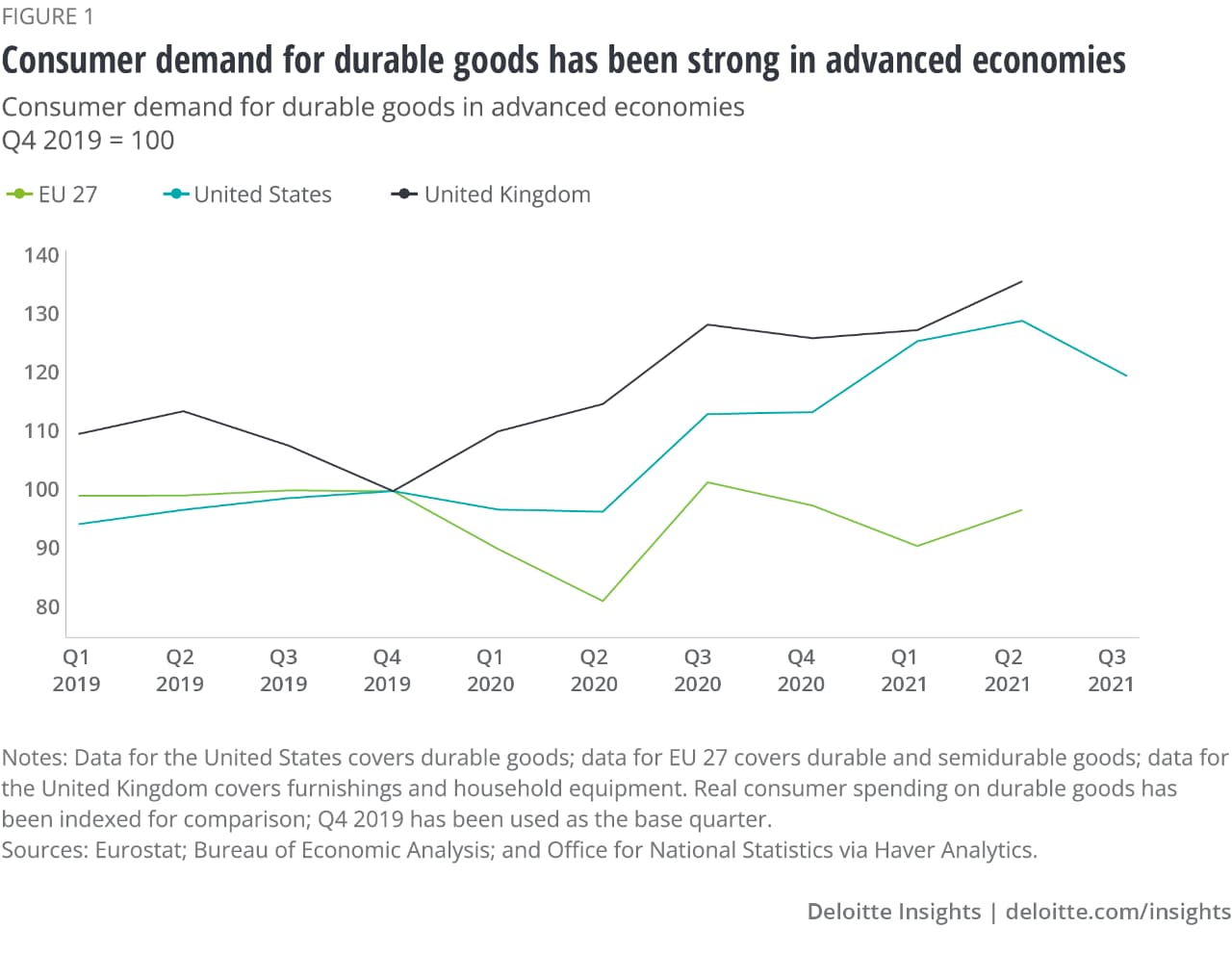

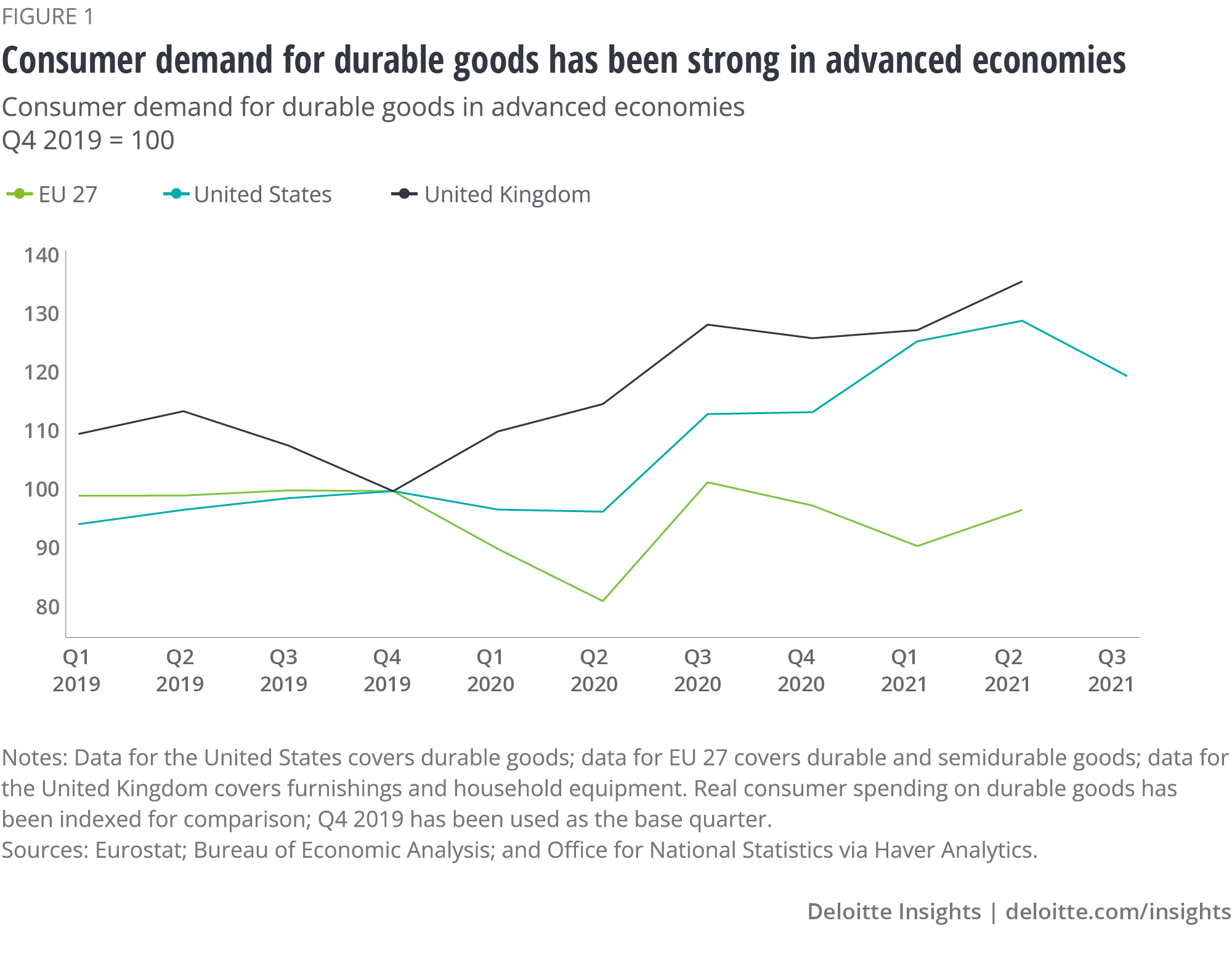

The economic recovery in advanced economies, which began in Q3 2020, has been marked by a surge in demand for goods, especially durable goods (figure 1). This is particularly evident in the United States and the United Kingdom. The European Union also saw a quick rebound in spending on durable goods relative to previous recessions. Demand for durables has been relatively muted in emerging markets where fiscal support was considerably weaker, however, this is likely to change as vaccine coverage improves and pent-up demand is released. Demand for durable goods in advanced economies has been fueled by high-wage remote workers who have been relatively unscathed by the financial impact of the pandemic.2 This demographic enjoyed relative job security, negligible impact on income, and benefited from an increase in household wealth as stock indices and home equity increased.3 Demand for larger homes spiked as virtual work and school became the norm. Spending was diverted to goods such as cars, home equipment, and gym equipment, while the service sectors remained shut.4 Lopsided demand from developed economies boosted capacity utilization in China’s factories after their initial struggle to restart due to a shortage of workers.5 Purchasing managers’ index (PMI) data between June and December 2020 indicates that manufacturing in China accelerated, benefiting from a prepandemic glut in the supply of energy. A relatively strong recovery in China’s manufacturing sector contributed to staving off a marked imbalance in supply and demand. Prices therefore stayed relatively stable through the end of 2020.

The narrative changed in 2021. Mass vaccination in developed countries in the first half of the year built up the expectation that pent-up demand in developed economies would shift from goods to services as people started to return to normal behavior. But the protracted impact of the Delta variant slowed this shift and reinforced pandemic-induced buying patterns—more goods, less services.6 At the same time, China and other parts of Asia experienced a slowdown in manufacturing activity due to a combination of several factors, including energy shortages and recurring waves of COVID-19. China’s official PMI dropped steadily after March 2021 and entered contractionary territory (below 50) in September and October ( figure 2).7 Manufacturing activity in the ASEAN region also contracted between May and September.8 The confluence of strong demand in developed economies and constrained supply in manufacturing hubs in Asia contributed to prices surging in 2021.

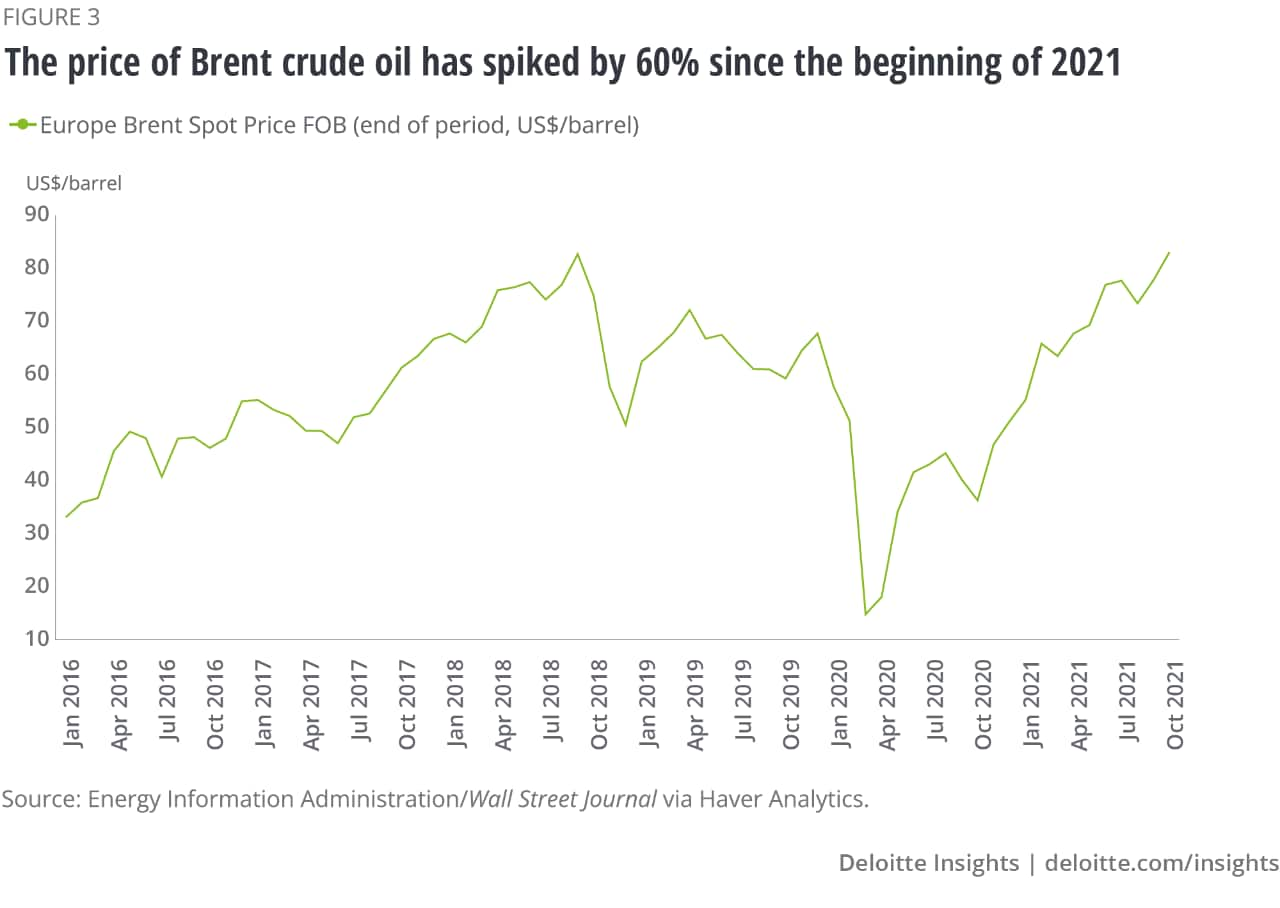

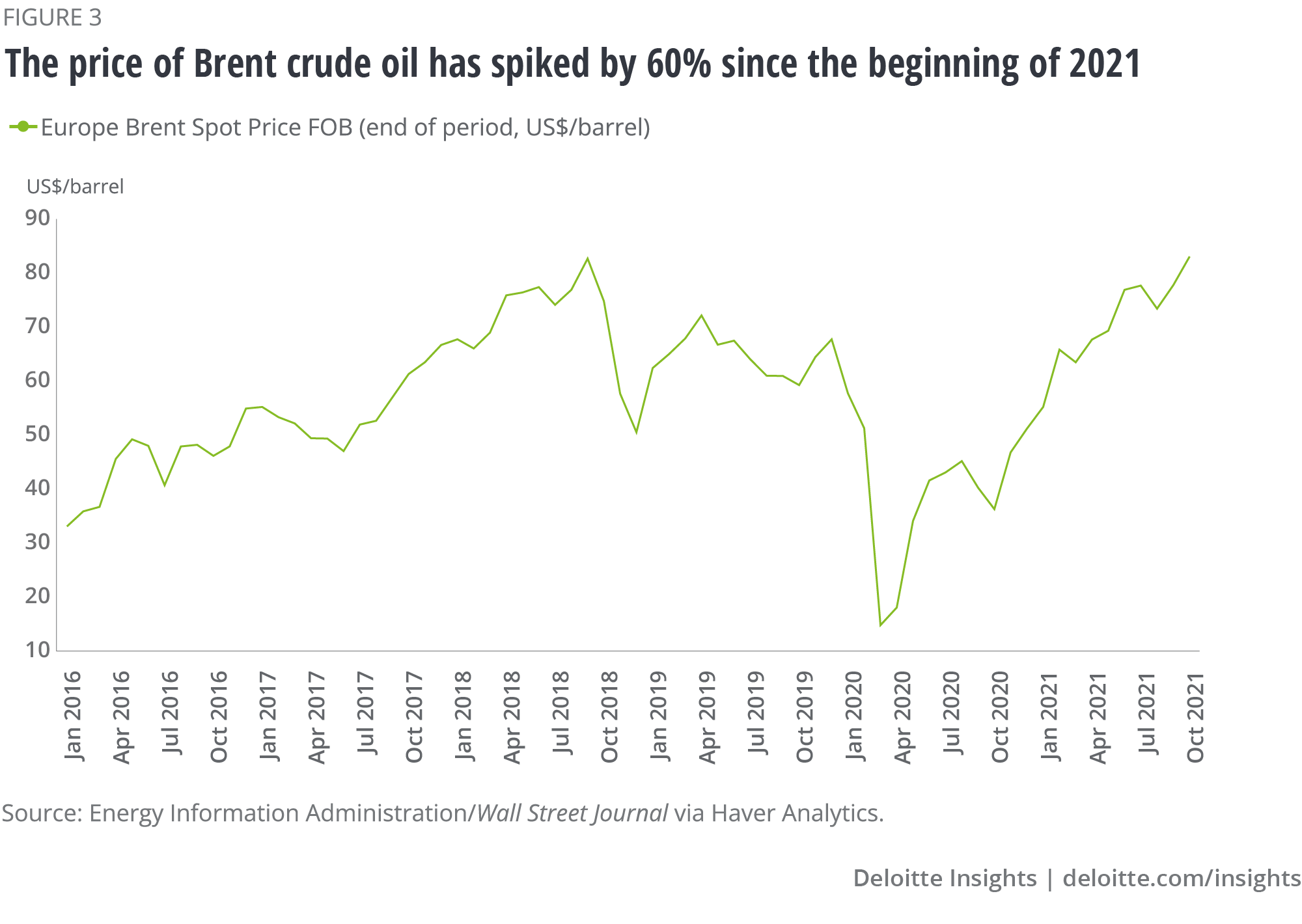

Energy shortages have been a major reason for constrained manufacturing. The demand for hydrocarbons—coal, oil, and gas—has increased sharply as the global economy returns to normal albeit at widely varying rates across regions. Hydrocarbon demand has also been boosted because of the relatively weak output of renewable energy such as wind and hydropower.9 Moreover, sharp reductions in hydrocarbon production in the wake of the pandemic, when there was concern about a supply glut, have made it difficult for supply to respond to the higher-than-expected increase in demand. Additionally, floods in coal hubs in Asia, and concerted yet slow efforts to shift to cleaner sources of energy, have also limited supply. These factors have combined to create a mismatch in the global energy industry. The price of Brent crude oil has spiked by 60% since the beginning of 2021, reflecting strong demand and constrained supply (figure 3).

Another major factor constraining manufacturing and adding to inflationary pressures, particularly for new and used vehicles, is the relative shortage of semiconductors. Semiconductor chips are essential to an array of consumer goods from mobile phones to laptops and modern automobiles. Demand for semiconductors grew during the pandemic, due to the increased use of electronic communication equipment.10 Activities such as e-gaming and cryptocurrency mining—both of which thrived through the pandemic—also added to the demand for semiconductors (and energy). Auto manufacturers boosted demand further to keep up with the steep bounce in orders for new vehicles. While electronic goods manufacturers preorder semiconductors for their products, auto manufacturers, which function on just-in-time production principles, are facing severe delays. The price of new cars has increased as a result. In the United States, the price of a new vehicle has increased by 8.8% since the beginning of 2021.11 The shortage of semiconductors has shifted demand from new vehicles to used vehicles, including among rental car providers who sold off their fleets during the height of the pandemic. Used cars in the United States are 27.1% dearer relative to the beginning of the year.12 This exposes the fragility of the supply chain for semiconductors—almost 80% of the chips are manufactured in Asia, and supply cannot be diversified very quickly since building a new semiconductor fabrication unit costs billions of dollars and could take up to five years.13

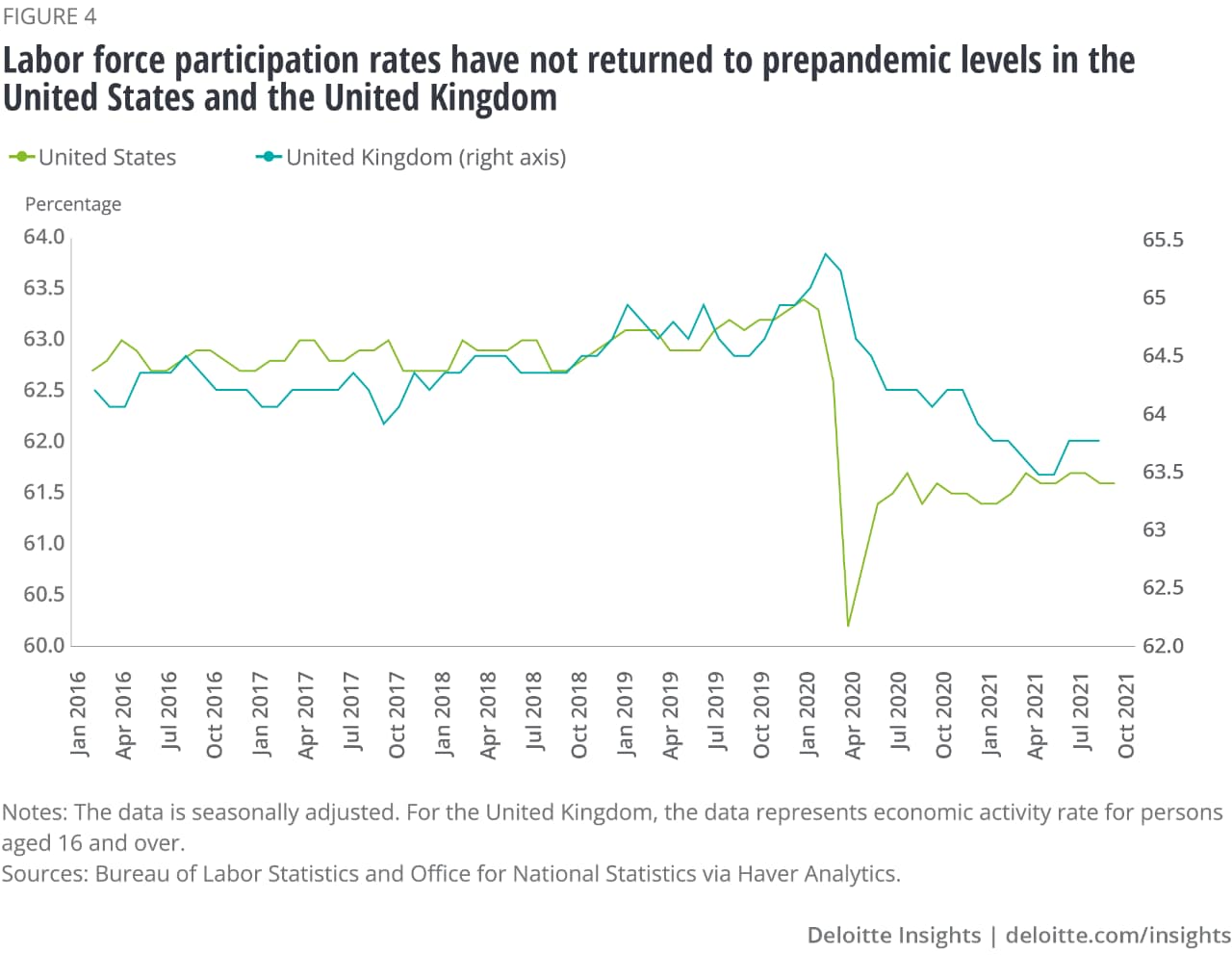

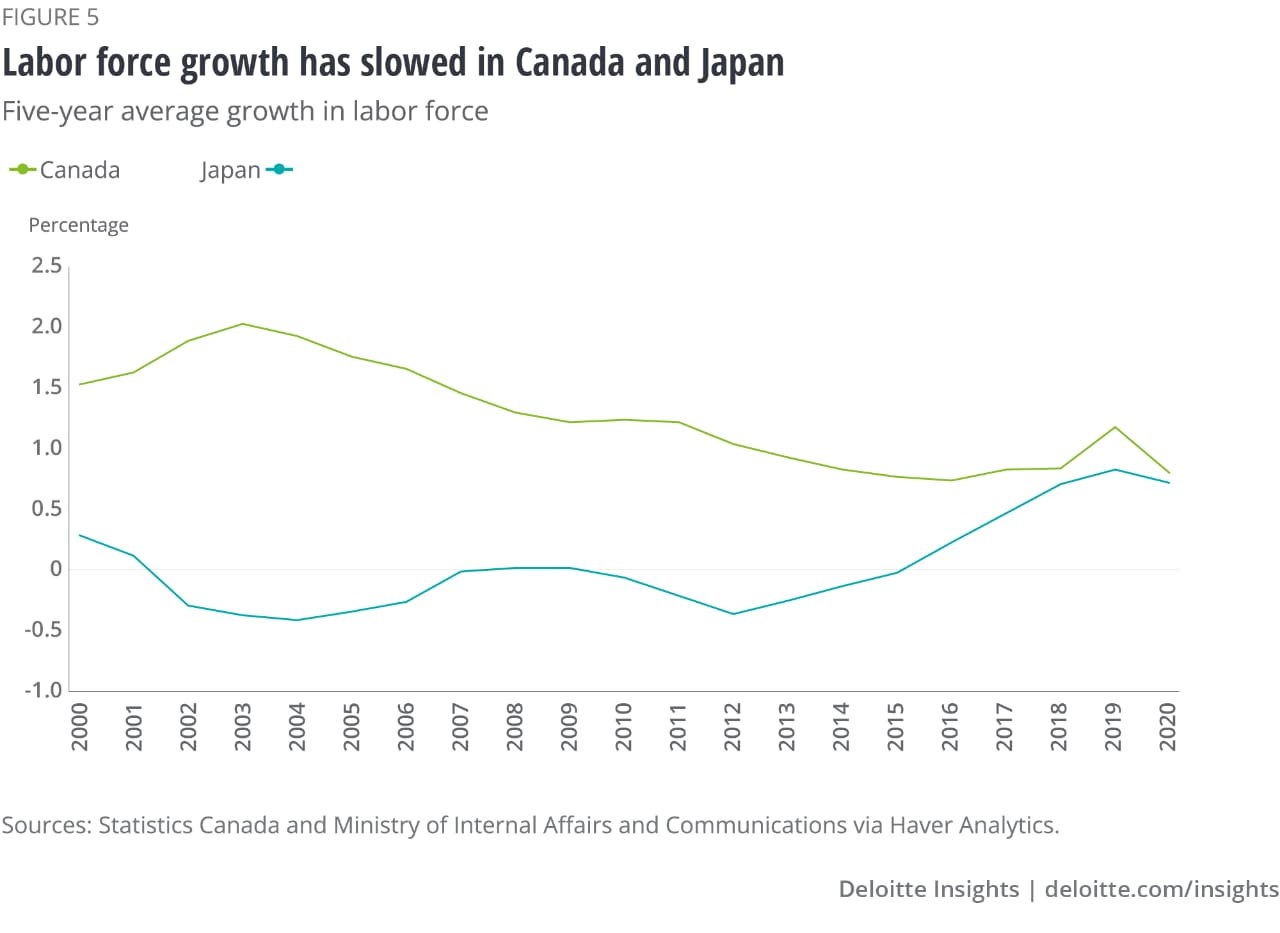

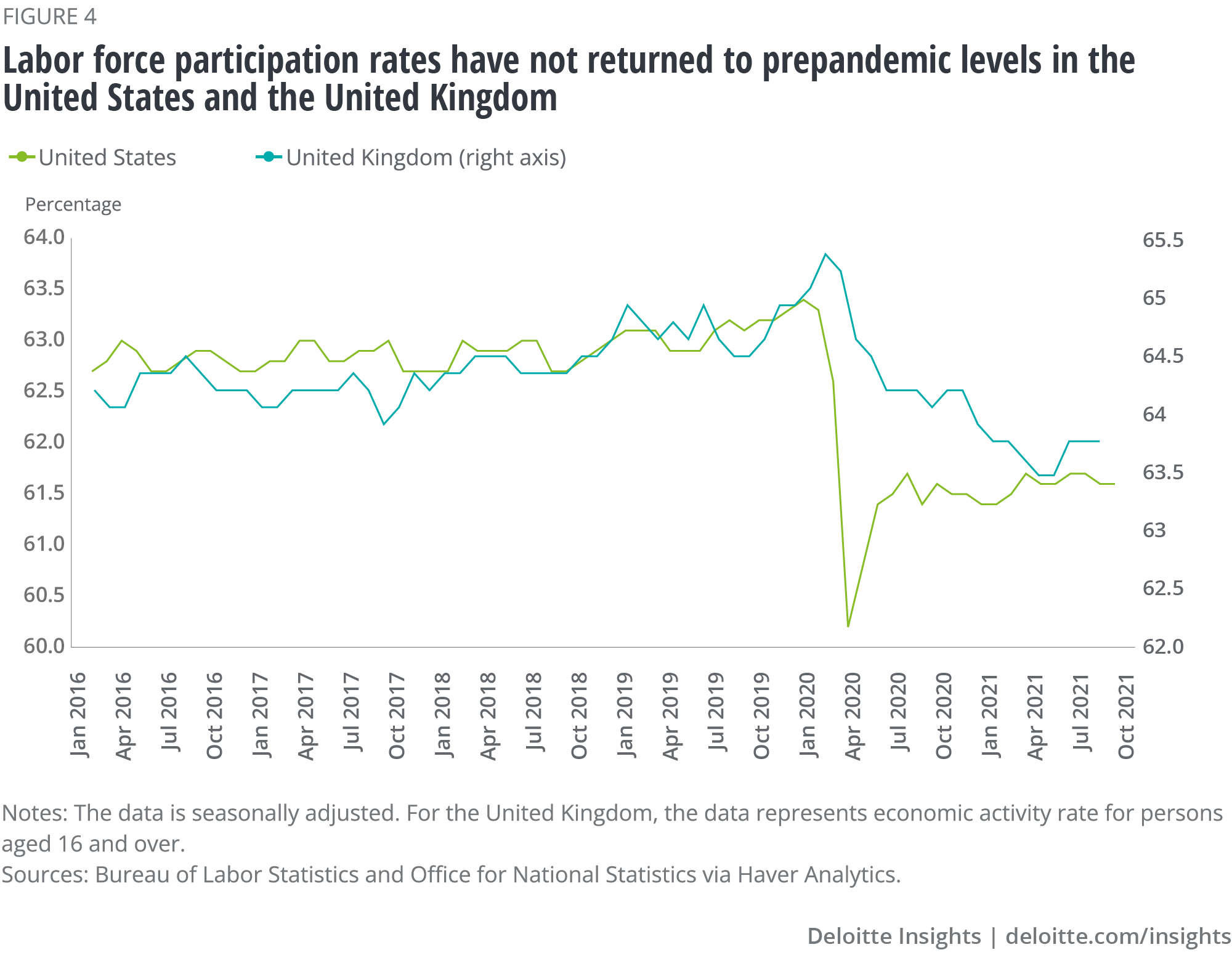

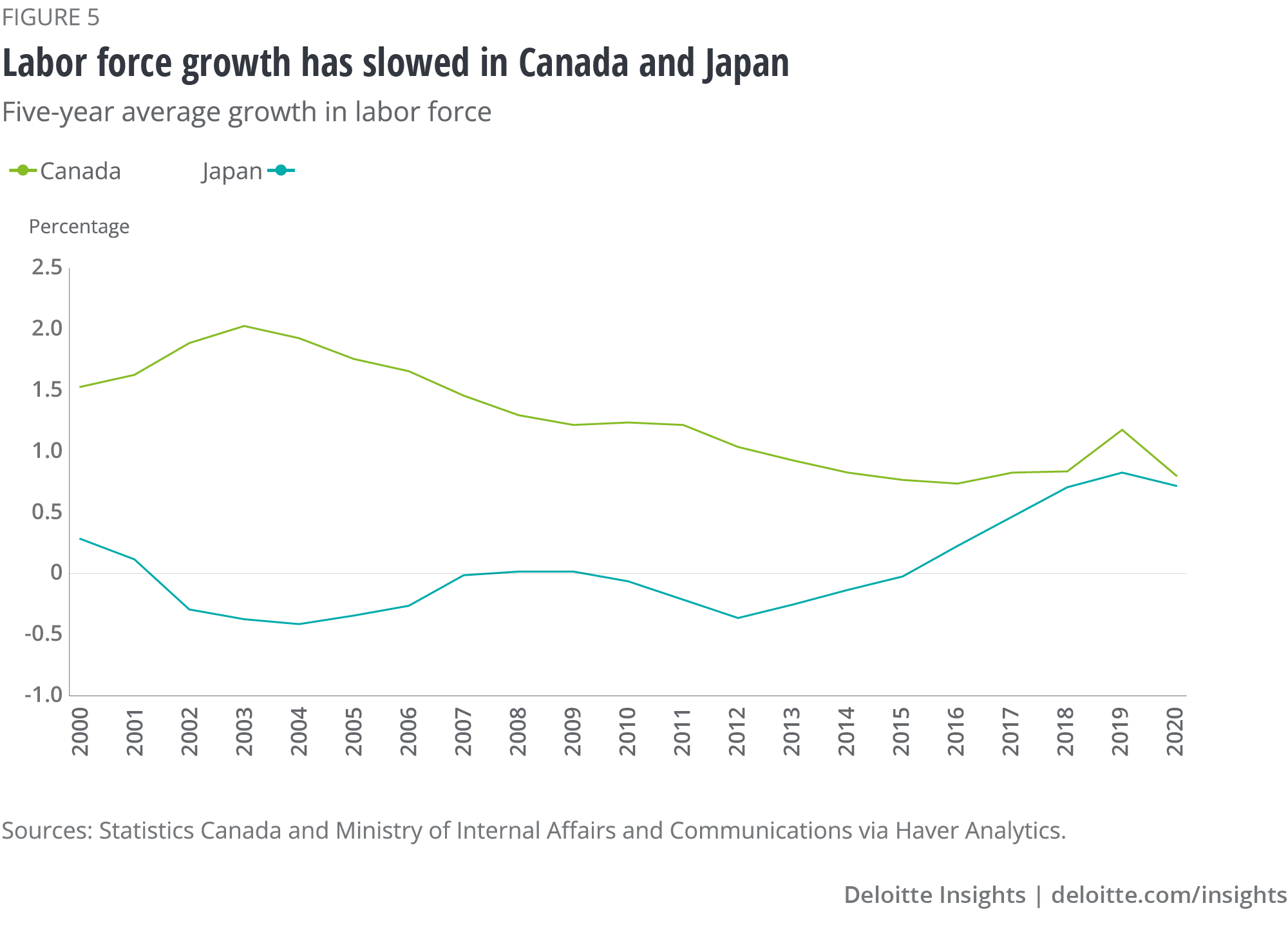

Finally, labor shortages across several countries have been a major supply constraint. In the United States, the labor force participation rate has moved sideways after an initial increase. Participation in October 2021 was almost 2 percentage points lower than that in January 2020. Total employment in the country is more than 4.5 million below what it was in the beginning of 2020. Several factors have kept people out of the workforce—early retirements, wariness about the virus, closed schools, and closed or understaffed child-care centers. In the United Kingdom, the economic activity rate is a whole percentage point lower than what it was in January 2020 (figure 4). A shortage of truck drivers in the country, partly due to Brexit, has affected the supply of fuel and consumer goods.14 In Canada, several industries are reporting labor shortages, despite the participation rate bouncing back to pre–COVID-19 levels, because growth of the labor force has slowed.15 Labor shortages are more pronounced in Japan, despite the relatively quick rebound in participation rates because the labor force, which was shrinking for many years, is now growing very slowly (figure 5).16 Worker shortages have been reported in various countries, including Vietnam, Malaysia, and Thailand, where workers in the manufacturing sector have returned to their hometowns due to lockdowns and recurring waves of COVID-19.

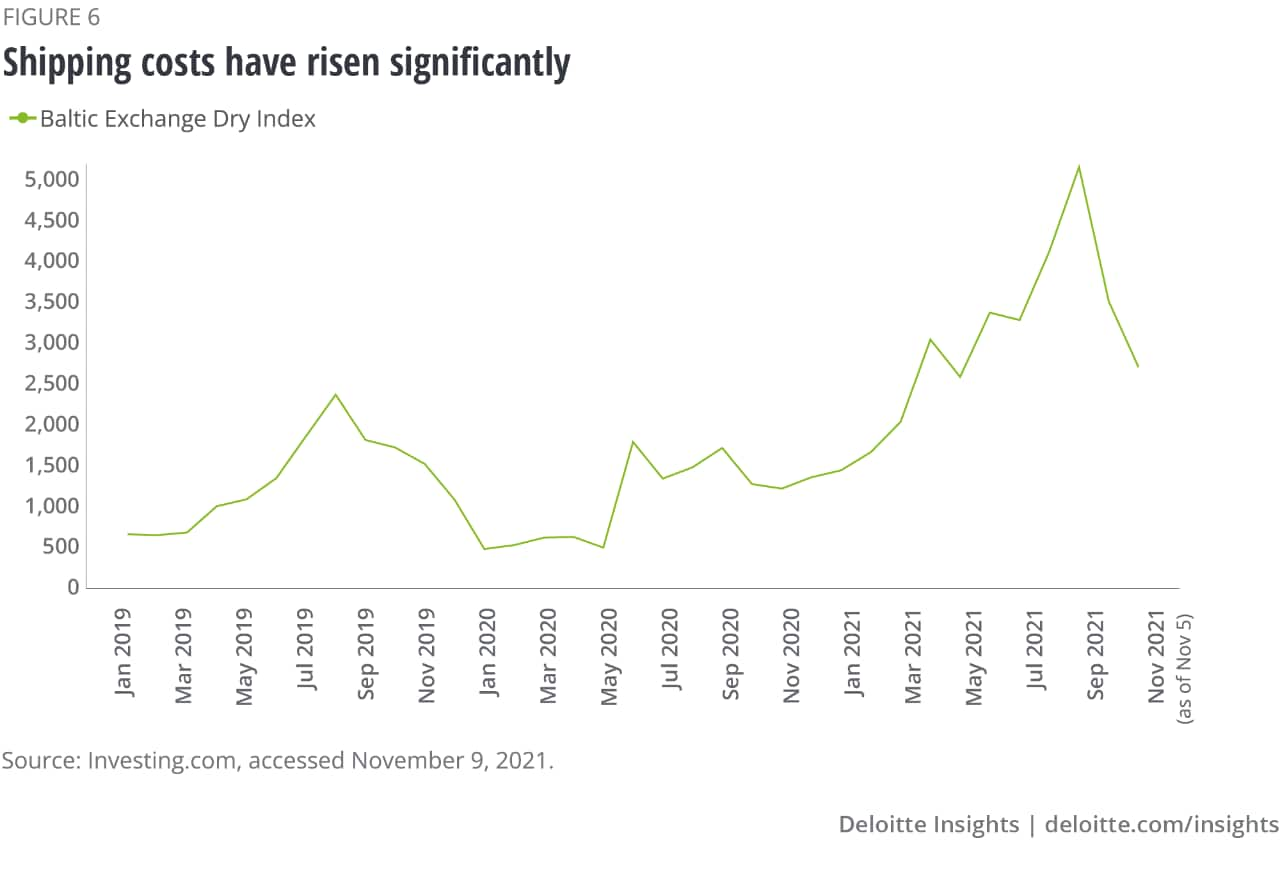

After strained global factories churn out new products, the next challenge is to transport them to the customer. Maritime transport accounts for 80% of global trade by volume.17 Shipping costs have risen dramatically as the demand for goods persists—from May 2020 to September 2021, the Baltic Dry Index, which indicates the cost of transporting goods by sea, rose almost 15-fold. Prices have fallen since the beginning of October but remain five-fold higher than prepandemic rates (figure 6).18

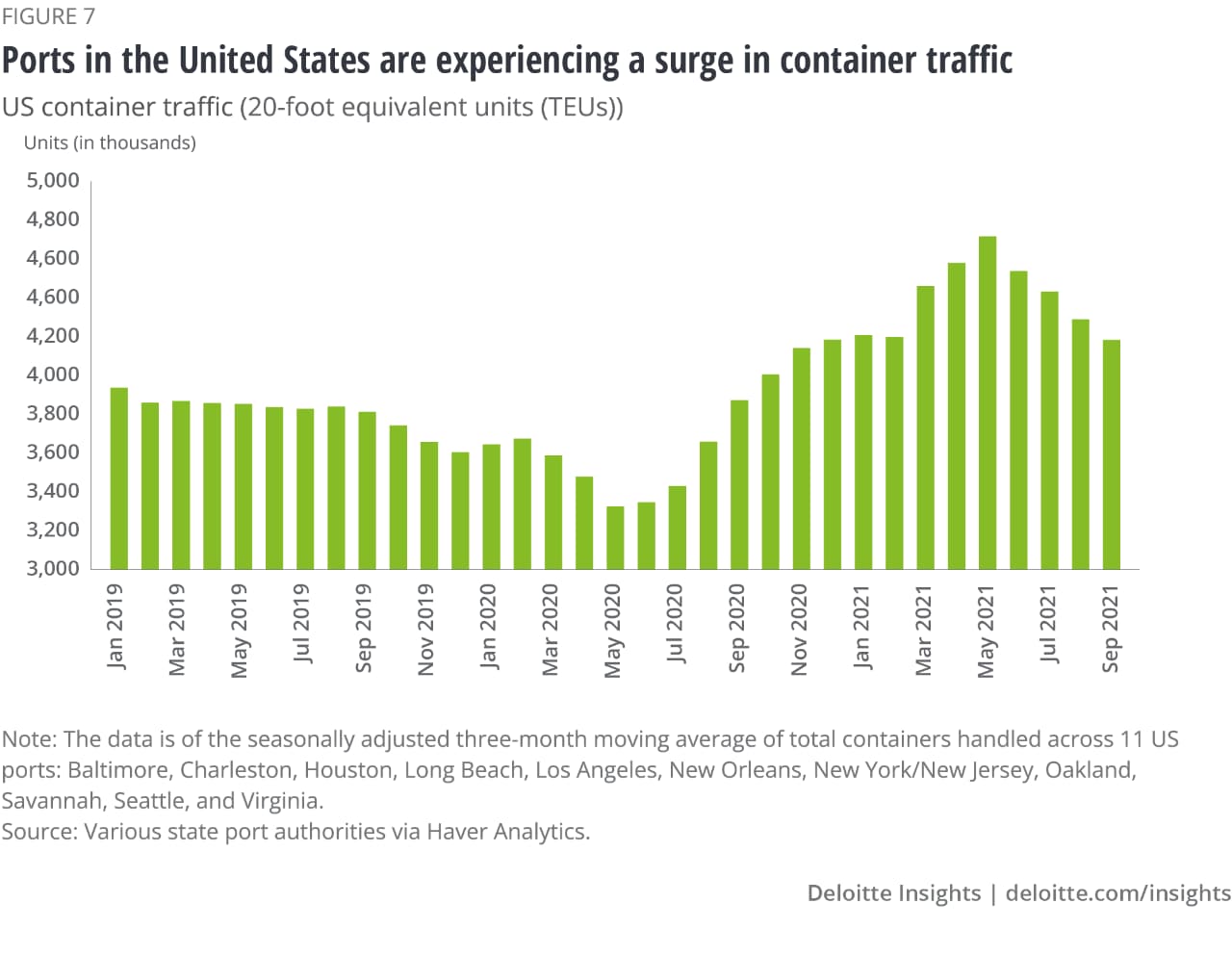

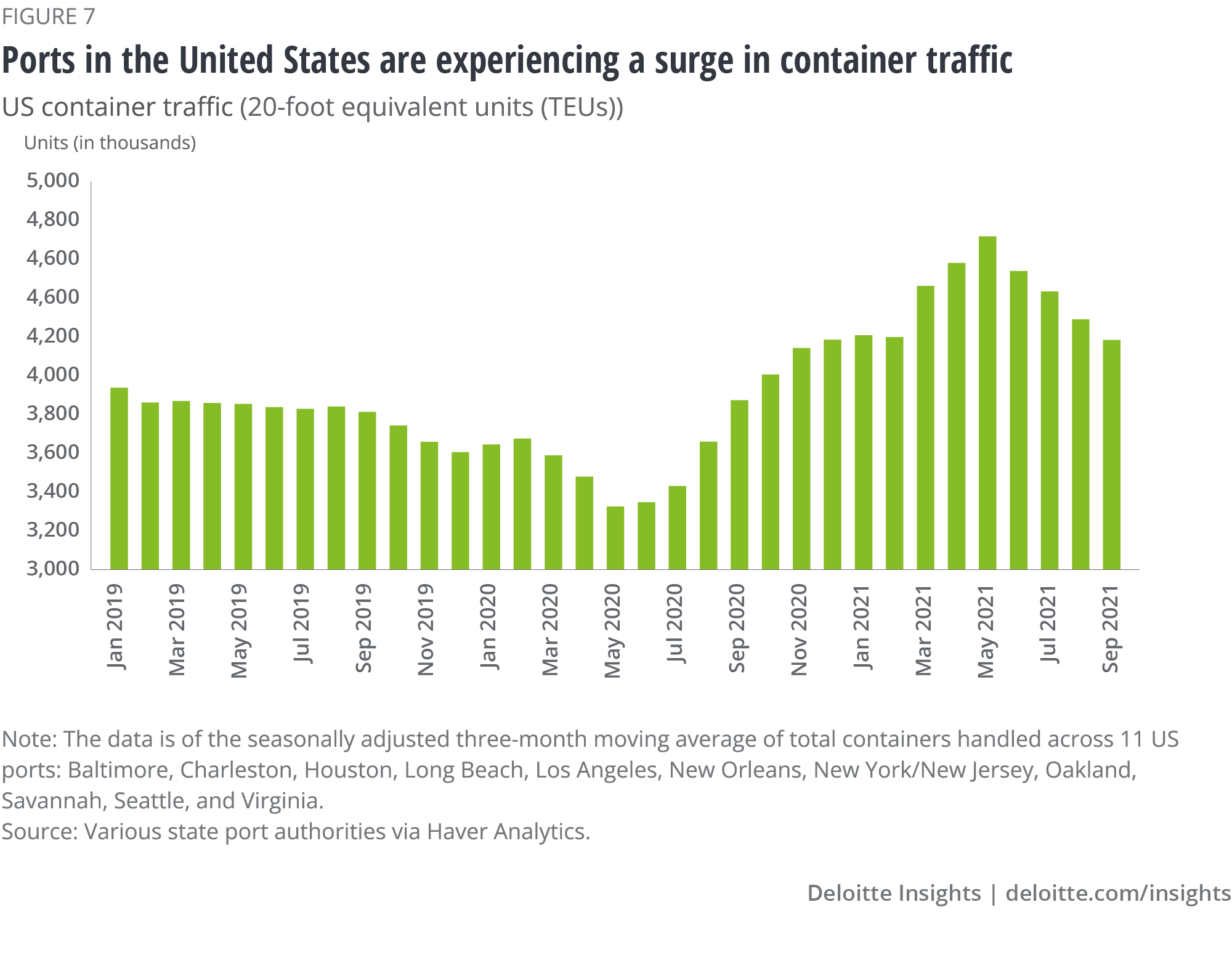

Congestion at ports present another challenge. In October, a tropical cyclone forced Shenzhen’s Yantian Port, one of the busiest in the world, and crucial to China’s exports to the west, to close. This resulted in a logjam of ships waiting to load goods.19 At the other end, the Los Angeles–Long Beach port has experienced a record number of ships waiting to unload goods (figure 7). The port, which receives 40% of all goods shipped to the United States, now functions 24/7 to ease the congestion of containers.20 Port authorities have resorted to issuing fines for backlogged cargo.21 Very strong demand for goods, as well as a shortage of port workers and truck drivers, has resulted in severe congestion. Ports in New York, Rotterdam, and Kelang in Malaysia have all experienced an increase in turnaround time due to higher volumes and supply-side constraints indirectly linked to the pandemic.22

Central banks across the world have an unenviable task. They must decide whether to tighten accommodative monetary policy to rein in price increases at a time when labor markets remain vulnerable, and economic output, particularly in services, remains below full employment. But inflationary pressures have already proved to be stickier than many economists initially thought. And the course of the pandemic remains unpredictable. The prevailing point of view, however, is that this inflationary wave is transitory. As the business world works out the kinks of producing under high demand, and as demand for durable consumer goods falls with the waning of the pandemic, pressures on pricing should dissipate.

The United States Federal Reserve, the European Central Bank (ECB), and the Bank of England (BOE) have indicated that inflationary pressures might persist well into 2022.23 All three are likely to slow the rate of their bond-buying programs over the next few months before considering an increase in interest rates. As the Fed chairperson, Jerome Powell, highlighted in August, the period from the 1950s to the early 1980s taught monetary policymakers not to react to temporary fluctuation. However, he also harked back to the 1970s when core inflation remained persistently high, likely due to higher inflation expectations.24 Therefore, central banks continue to track inflation expectations and subsequent wage increases. If wage increases exceed productivity, producers could pass on costs to consumers. Higher prices could beget higher wages, starting a wage-price spiral that will likely force central banks to intervene. Persistently high prices and a rapid tightening of monetary policy could kill the ongoing economic recovery.

Even though monetary policy cannot be used to solve the supply constraints that are contributing to inflationary pressures, it might need to be tightened moderately, depending on how long price pressures persist. The BOE is the first among major central banks to signal that moderately higher interest rates will be required to return inflation to its 2% target.25 The Fed and the ECB might also have to hike interest rates earlier than initially planned if prices accelerate and inflationary pressures persist for longer than revised expectations indicate.

Russia and a few countries in Latin America have hiked interest rates in recent months but they remain the outliers.26 On average, monetary policy continues to remain very accommodative. In October, the Council on Foreign Relations’ Index of Global Tightening or Easing, which includes data from 54 countries, stood at -9.65 on a scale of -10 (indicating that all countries are easing) to 10 (indicating that all countries are tightening).27

We believe that the current inflationary wave is more likely to be transitory for several reasons, outlined below. Unfortunately, we cannot be specific about how much time “transitory” implies. It is contextual, much like short, medium, and long terms, which assume varying lengths of time depending upon the economic issue being discussed.

Current inflationary pressures are the result of a global health crisis and the policy response it warranted. Vaccinating a sufficiently large percentage of the global population is the overarching solution to the health crisis and resulting problems, including the mismatch between demand and supply. Until widescale vaccination is achieved, the threat of recurring waves of infection, and the subsequent loss of life, remains an obstacle to the normal functioning of the global economy. A mismatch in vaccine coverage across countries can further complicate the supply-demand equation, especially if manufacturing hubs continue to be disrupted by recurring waves of infection. Therefore, the global distribution of vaccines is critical. The same holds true within countries as well: The threat of infection resulting in the mass loss of lives remains high if vaccine coverage is insufficiently wide. Limited vaccine coverage will continue to skew demand and constrict supply.

The adage “It will not be over anywhere until it’s over everywhere” is likely to hold true for the pandemic and the chaotic functioning of the postpandemic global economy.

Cover image by: Molly Woodworth