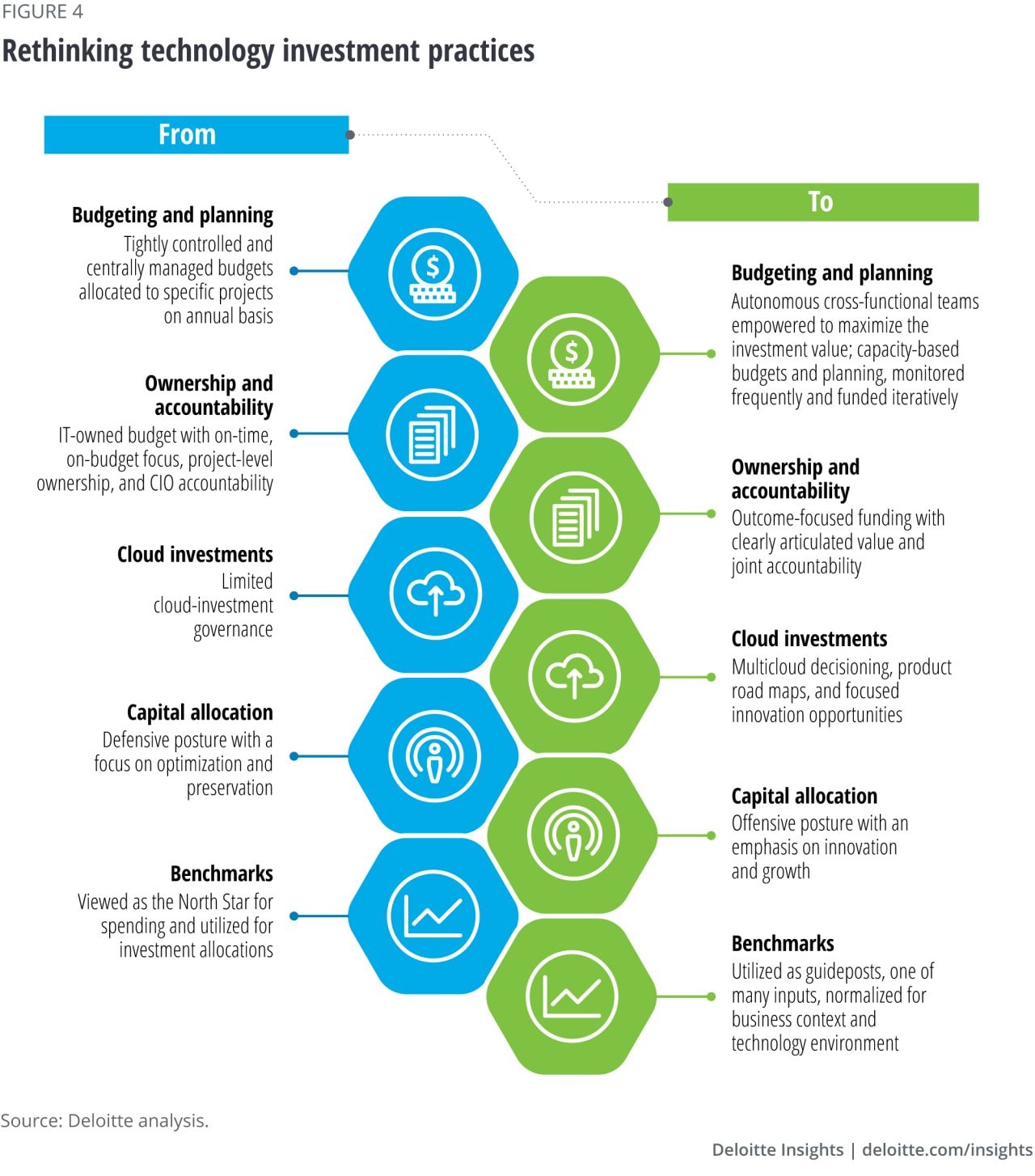

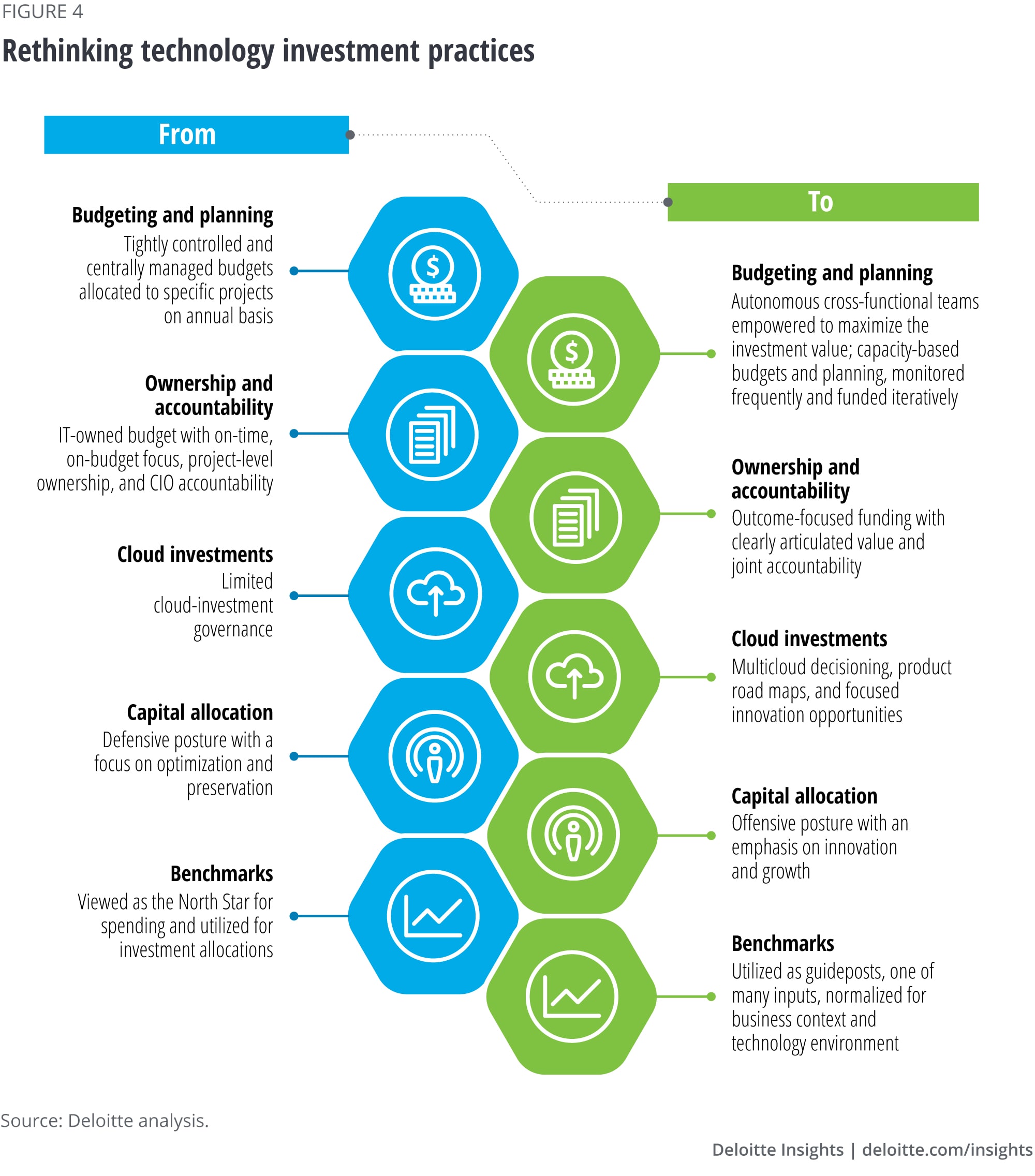

Rethinking technology investment practices

Traditional technology investment practices can sometimes produce investments that are siloed, inflexible, and opaque. To maximize the value of technology investments, practices related to budget planning, accountability, cloud, capital allocation, and benchmarks should be adjusted.

Agile planning and budgeting. Belabored planning efforts, in-depth forecasts, customer preferences, and detailed task lists with strict deadlines—together with requirements gathering, solution development, and testing—can stretch project deployment into months or even years. By the time IT delivers the project, the world has moved on; the business may now face new headwinds, evolved customer preferences, or shifts in demand. This is where technology vanguards play the field differently.

For many technology vanguards, rapid prototyping, design and testing, and iterative development is becoming the norm. Their delivery teams—including both business and technology stakeholders—aim to minimize the time between the idea and execution, deliver the solution incrementally, and quickly course-correct based on customer feedback and how the solution is being used.

Savvy technology leaders are shifting their investment practices to give more autonomy to cross-functional teams, enabling them to maximize the value delivered from technology investments and holding them accountable for delivering this value. They are also often more engaged in oversight, course corrections, and budget reallocation across multiple competing options.

Joint ownership and accountability. Historically, the success or failure of technology implementations rested squarely on the shoulders of the CIO and IT team. However, as organizations move from siloed projects with functional ownership to cross-functional business solutions, project success and failure are also jointly owned.

For example, the CIO of a large services company fostered joint accountability and ownership by offering “unlimited capacity” to business leaders. Every solution in development is staffed with a collaborative team of business and technology people who are responsible not only for developing the solution but also for delivering value. Business and technology leaders are jointly responsible for overseeing the investments and the value delivered. Incentives, bonuses, and rewards depend on outcomes, not on staying within budget or meeting certain deadlines. Effective implementation in this scenario required that the organization develop competencies, agility, and a network of ecosystem partners that can flex based on demand. The CIO is also responsible for a budget category known as “tech for tech,” which are investments in collaboration and productivity tools and other common enterprise infrastructure. As a result of these policies, business leaders are far less likely to build or buy shadow IT solutions.10

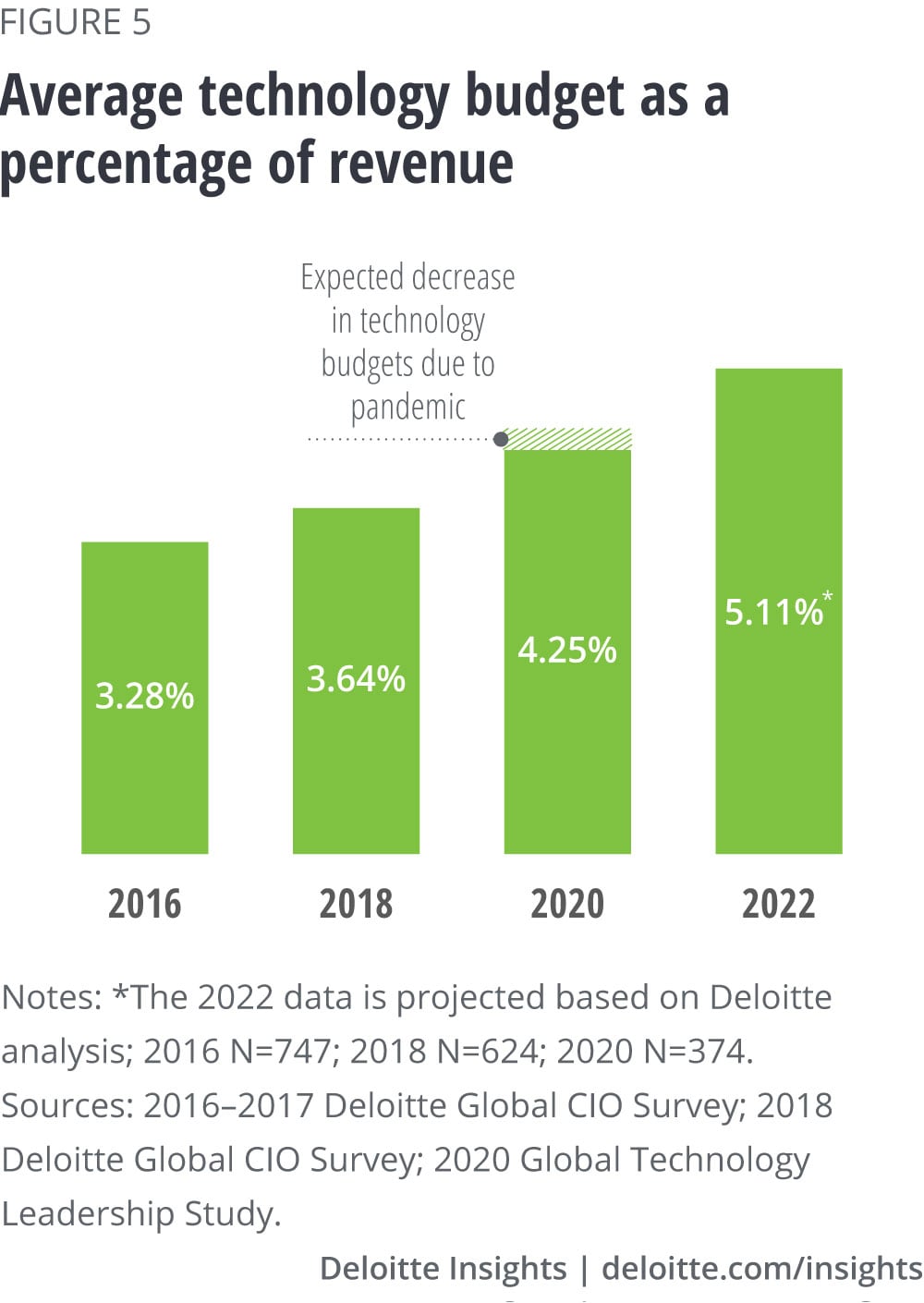

Deliberate cloud investments. The pandemic is accelerating cloud demand, with 59% of enterprises expecting cloud use to exceed plans due to COVID-19.11 Deloitte predicts that cloud revenue growth will be greater than 30% from 2021 through 2025.12 Cloud adoption can help companies realize significant cost savings, but only if CIOs have visibility into cloud usage across the organization and provide ongoing oversight and adjustments to manage costs, monitor workloads, and ensure value realization.13 Merely pushing a cloud-first approach could substantially increase costs, diminish value, and lead to unchecked usage, orphaned resources, oversized infrastructure design, redundant software subscriptions, or complex architectures. On-premise deployments may be better suited for workloads that have high resource utilization and complex integrations that can run up deployment and operational expenses.

Balanced capital allocation. COVID-19 highlighted the need for organizations to be lean and resilient. Many technology leaders were asked to cut significant portions of their budgets and reallocate existing investments to build resilient technology environments and boost security, infrastructure, and collaboration tools. Such defensive investments—related to the protection and preservation of the organization’s business and assets—are critical, but for business leadership, they’re a table-stakes expectation.

Savvy CIOs are also focusing on business innovation and other offensive technology investments—those that create and enable new opportunities, business models, and revenue sources. Research suggests that high-performing companies disproportionately spend discretionary budget dollars on growing the business while others focus primarily on protecting the business.14

Using benchmarks as guideposts. In calibrating technology spending, some organizations solely rely on industry benchmarks to assess if they are over- or under-spending and to allocate technology budgets. As lines between industries blur, these benchmarks should be used as guideposts, not gospel.

Companies in the same industry can have vastly diverse business strategies and models, leading to very different investment profiles. Using benchmarks without context could be dangerous. It is important to align spending with the organization’s corporate strategy, current and future competitive landscape, and technology ambition (figure 4). Above all, it is imperative to ensure that budget dollars can be reallocated quickly to maximize value. Proper oversight can allow technology leaders to continually monitor technology investments to ensure ongoing value delivery and enable them to ruthlessly reallocate funds if the investment is underperforming.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}