{kind=link}

{kind=link}

Embedding climate risk into banks’ credit risk management has been saved

Co-authors Val Srinivas and Jill Gregorie wish to thank Naz Asli Öncel for contributing to this report.

Cover image by: Willy Sions

United States

United States

United States

United Kingdom

Canada

United Kingdom

This report offers a roadmap for how banks can embed climate risk into the different stages of the credit lifecycle—including strategy, underwriting, portfolio management, and reporting and disclosure. One of the major highlights of the recent COP26 climate change conference in Glasgow was the pledge by the Net-Zero Banking Alliance, comprising nearly a hundred banks and representing roughly 40% of global banking assets, to transition greenhouse gas (GHG) emissions “from their lending and investment portfolios to align with pathways to net-zero by 2050 or sooner.”1

These ambitious commitments are essential to limit the rise in global temperatures to 1.5 degrees Celsius by 2050,2 and avoid the most severe and catastrophic effects of climate change.

By any measure, these commitments should transform how banks finance carbon-intensive businesses and the green economy.

According to a recent CDP report, while many banks have identified the effects of climate change on their operations, most have not yet measured the impact on their financing portfolios. This means most banks are likely underestimating their exposure to climate-related risks.3 At the same time, there are also huge opportunities for banks in facilitating the transition to carbon-neutral activities, such as clean energy production and storage, and carbon-capture technologies.

Integrating climate risk metrics into credit risk management could be an enormous undertaking for most banks, but it is a necessary step toward a carbon-neutral future.

Since no big journey starts without a roadmap, this report provides just that—a framework that can help banking leaders incorporate climate change considerations throughout the credit lifecycle. It also sheds light on the tools and processes that are becoming increasingly central to these efforts.

The steps outlined here can also provide a solid foundation for other enterprisewide climate change strategies and commitments, including reporting progress to regulators, investors, and other stakeholders.

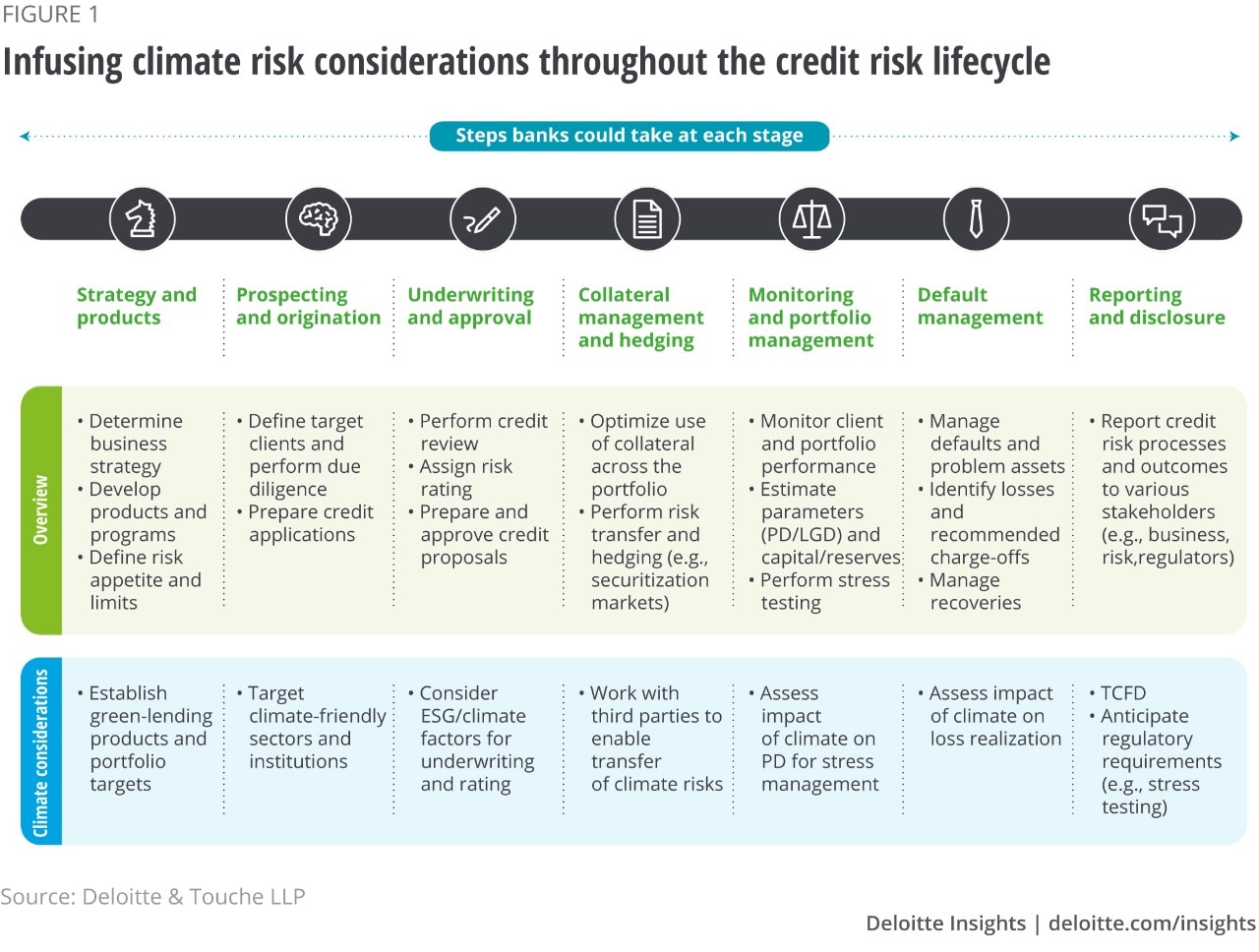

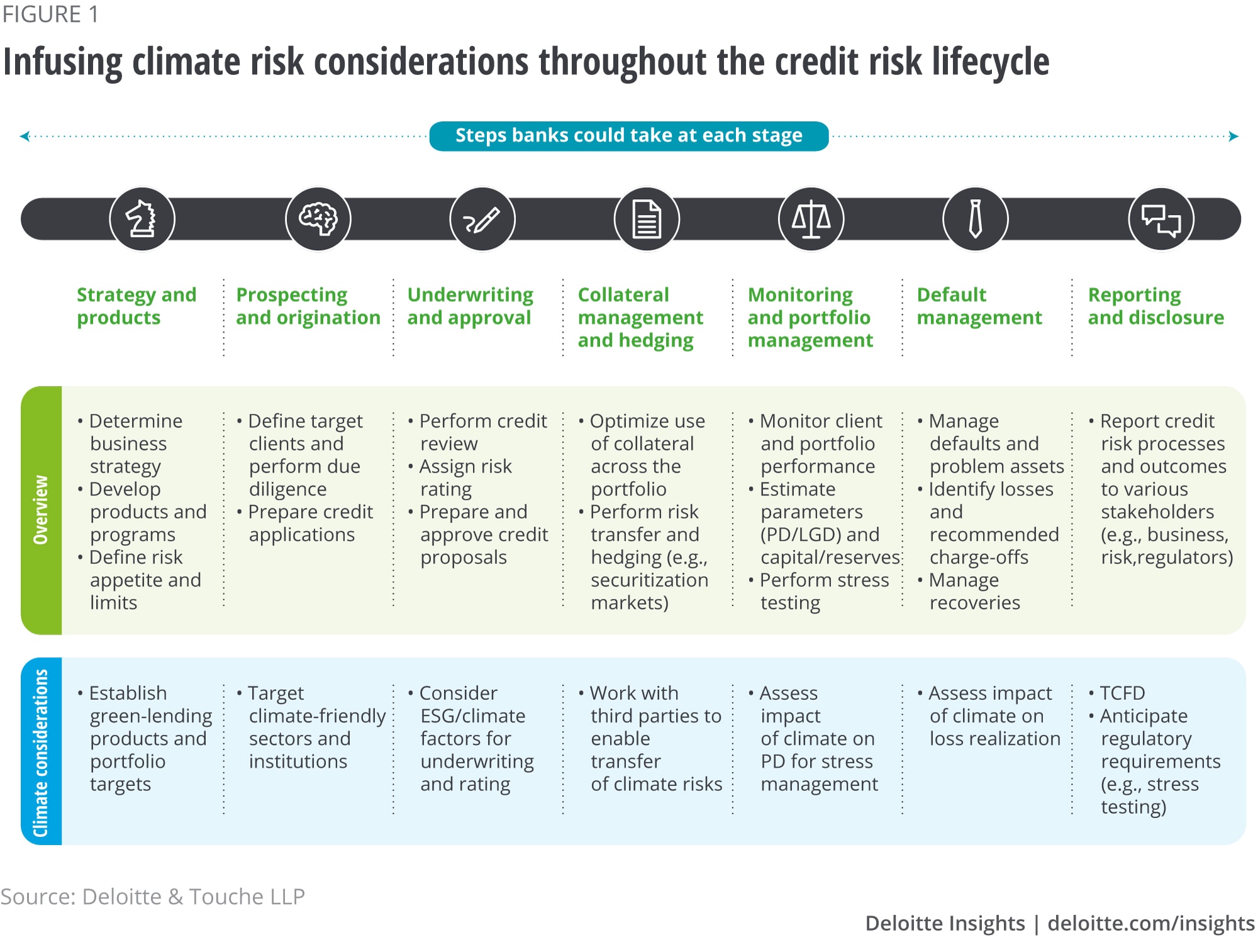

Virtually all stages of the credit lifecycle (figure 1) will likely be impacted by climate risk. Banks are beginning to infuse more climate-related considerations into each step of the credit management process.

As a starting point, banks should reassess their credit business strategies to address climate change issues: the markets, segments, and clients they will serve; the products they will offer; and the innovations they will bring to the market. The revised strategies may derive from the banks’ sustainability commitments, including goals for reducing financed emissions or overall risk exposure.

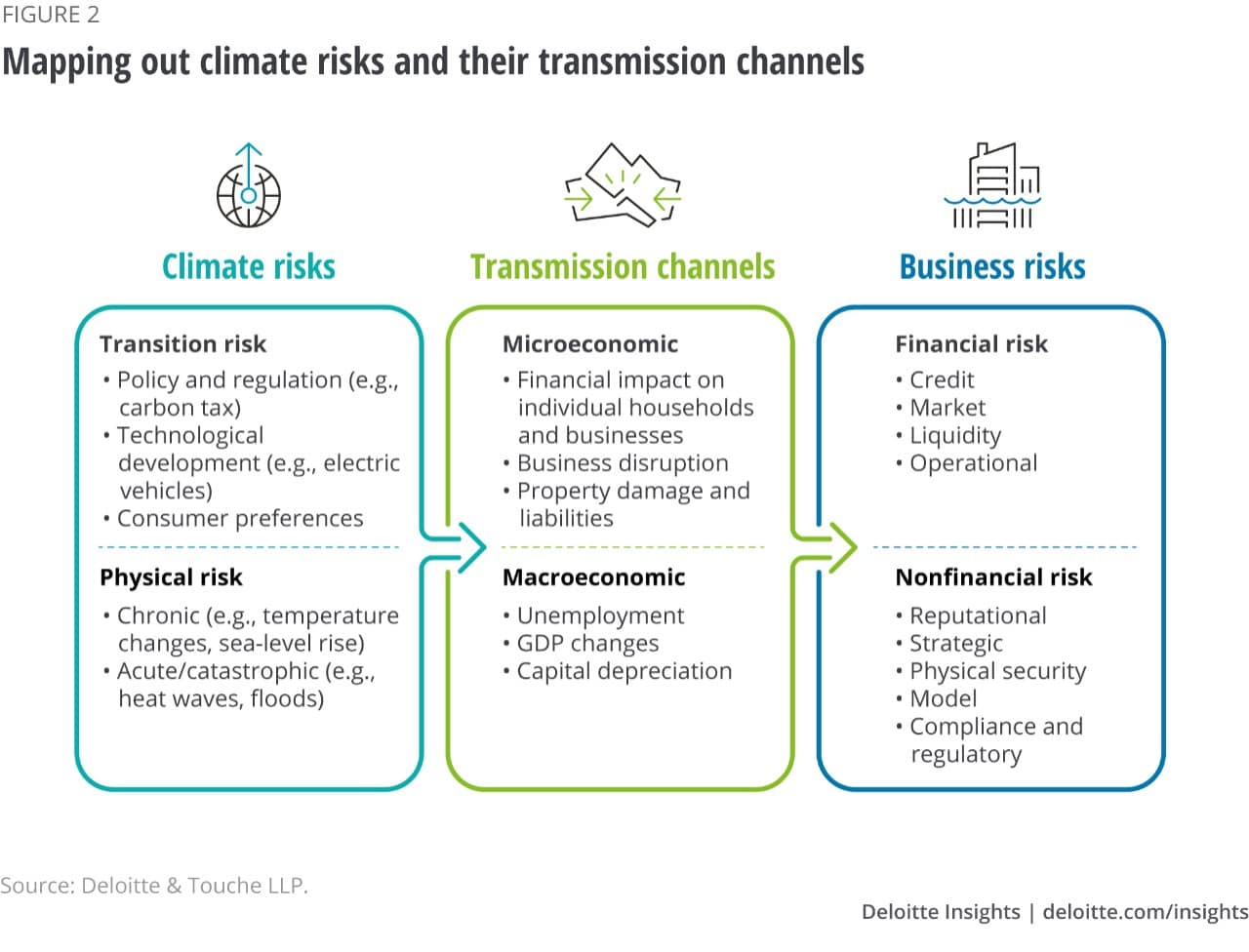

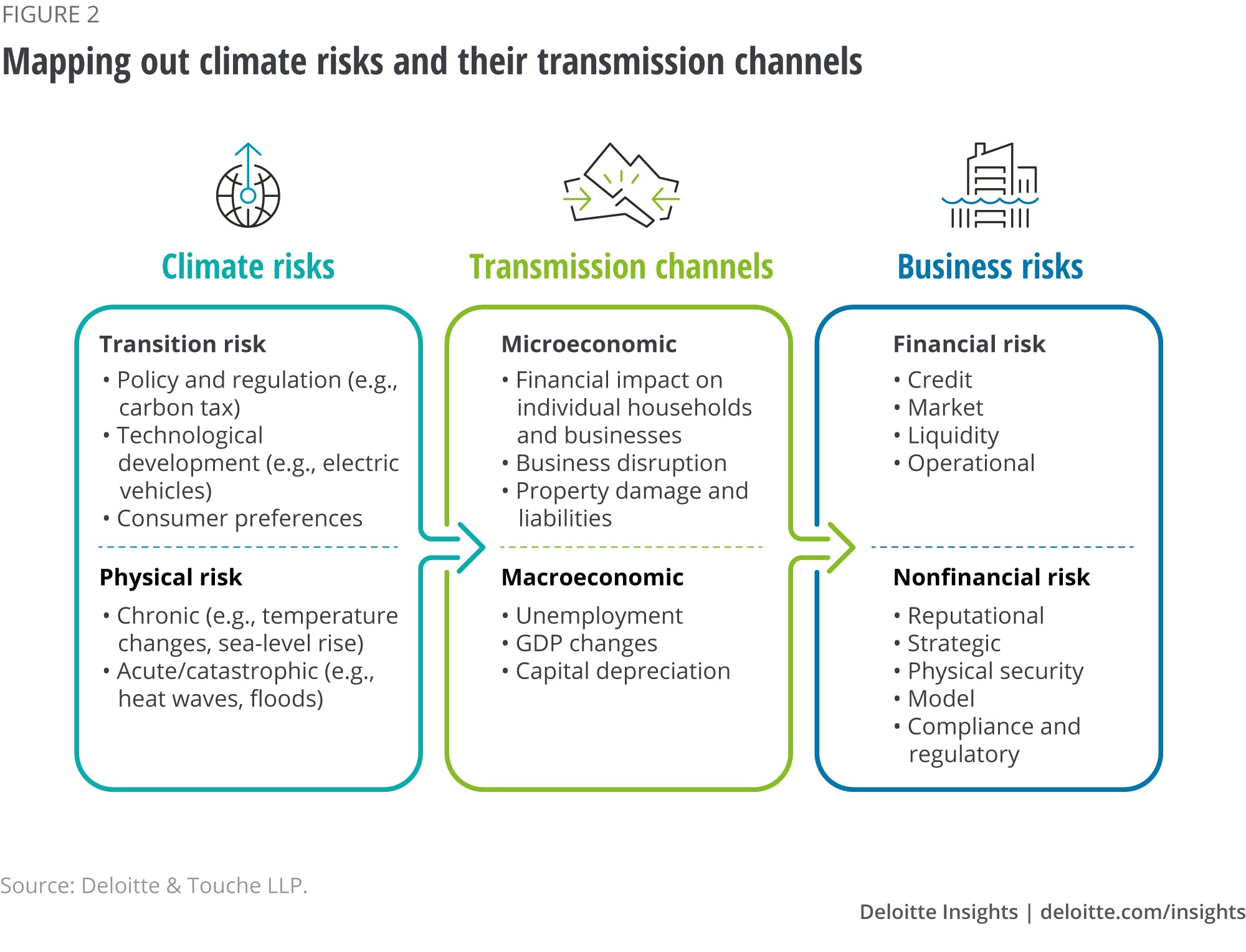

The consequences of global warming can manifest through physical risks and transition risks. Physical risks deal with the impact of extreme weather events like hurricanes, floods, or droughts; transition risks are those that result from changing policies, practices, and technologies as organizations shift toward a low-carbon economy. Physical risk and transition risk are not independent of each other—efforts to limit global warming may reduce physical risk but increase transition risk through higher market, technology, and regulatory costs.

In the short term, the magnitude of the impact of physical risks could outweigh the costs of transition risks. In 2020 alone, the physical risks manifested through severe storms resulted in more than US$220 billion in economic damage. But over the long run, transition risks could cost banks trillions of dollars. These risks can manifest in multiple ways, including potential reduction in revenues, increased cost of operations from higher carbon prices, and possibly greater regulatory burden. Collectively, they could cause a destabilizing effect on the financial system in the decades ahead.

Banks should first develop a taxonomy and map of climate risks and their transmission channels, such as macroeconomic outcomes, capital depreciation, new customer preferences, or business disruptions (figure 2). They could use a scoring system, based on emissions or other indicators, to visualize the magnitude of each risk on a heatmap. The heatmap would show risks across different dimensions, including industries/sectors, geographies, and client types.

The next step would be for banks to translate the overarching credit business strategy and product focus into appropriate risk appetite, credit risk processes and policies.

In addition, banks should accelerate product innovation to account for climate risk and decarbonize their portfolios. Many banks are expanding their green-lending products to offset financed emissions. Banks can use green mortgages, for example, to promote energy efficiency by offering better financing terms for borrowers who agree to build a home using sustainable materials or upgrade an existing property with clean energy sources.

Revamping market and product strategy has its challenges: Aligning enterprisewide climate goals with financial commitments may be difficult because of the uncertainty, complexity, and inability to translate climate scenario projections into microdecisions at the borrower or credit level. In addition, complexities can arise when teams must account for differences across jurisdictions, products, and counterparties (including correspondent banks) in models that forecast economic outcomes and sector impacts.

Ideally, banks should begin to assess the impacts of physical and transition risks on clients’ credit risks at the onset of new relationships. Prospecting and origination should be informed by the bank’s business strategy for targeting sectors and clients.

For large companies, environmental, social, and governance (ESG) metrics are often available from data vendors. For others, assessing climate risk may require an analysis of sector concentrations and exposure by region. As banks become more knowledgeable about data, pilot methodologies, and key sources of risk, models can be enhanced to create more precise risk profiles at an increasingly granular level.

The scope and extent of due diligence procedures will likely depend on a client’s economic sector, size, and geographic location. Many large banks are starting to scrutinize businesses more closely during the know-your-customer stage of documentation. They are asking clients to provide new types of data, such as energy usage attributed to new business activities, supply chain information, and data on emissions per unit of revenue.

Banks are also requiring enhanced due diligence for transactions involving certain sectors, such as oil and gas, timber, palm oil, or soy. In some cases, they may be formalizing plans to halt financing to businesses that specialize in Arctic drilling, mountaintop mining, or other practices that put biodiversity at risk. In fact, more banks are tackling natural risks and climate risks in tandem, since biodiversity loss can exacerbate climate change, which can then lead to more ecosystem destruction.

Determining the appropriate level of information required during prospecting and origination without making it too onerous on clients could turn out to be a delicate task for bank leaders. And some relationship managers (RMs) may lack the expertise to either communicate the bank’s strategy to clients and/or find the right product fit for them. Banks will need to engage extensively with heavy-polluting clients, in particular, to offer guidance about how they can transition out of fossil fuels. In addition, credit risk departments should work with other units to prioritize deals that reduce climate risk or present new opportunities in green technology.

Prospecting should also include evaluations of how climate risk factors impact potential risk transfer and hedging activities (see section, Collateral management and hedging). Ultimately, the practice of assessing and classifying current and new clients may result in customer attrition or a purposeful “derisking” by the bank itself. But this is the price to pay to future-proof the portfolio for climate risk.

The next step would be to infuse climate risks into the rating and underwriting process. Increasingly, banks are creating standalone borrower-specific climate risk scores. But they could also integrate climate risk assessments into the standard credit rating process.

These dynamic assessments should take the client’s physical and transition risks into account, as well as its resiliency to climate change, and the steps it is taking to mitigate climate-related threats to its business model. Banks should scrutinize factors including the client’s decarbonization progress, future production plans, and the availability of renewable energy technologies to power its operations. Since these evaluations tend to require technical knowledge of climate patterns and environmental trends, banks will likely need to hire specialists who have a scientific background.

Banks can use novel tech tools and data applications to assist with the risk assessment process and enable them to better grasp each client’s risk profile, given their climate response. For example, big data analytics can be used to map out nondisclosing companies according to carbon clusters, which groups companies that have similar levels of carbon intensity. Some banks are also creating shadow rating systems that report climate-related default probabilities alongside typical default probabilities, and adopting mitigation efforts when there’s a large differential between the two. Banks relying on third parties to get borrowers’ carbon intensity scores should note the differences across vendors in the methodologies they use to assess carbon intensity.

Another area that requires greater attention is collateral management and hedging. What are the new risks—direct or indirect—from climate change on credit risk transfer strategies and hedging?

Both physical risk, in the form of damages to physical assets, and transition risks, such as repricing stranded fossil fuel assets or changes in real estate values, could affect collateral values. But at present, banks have limited opportunities to transfer climate risks, since this market has yet to develop and market participants lack expertise and confidence in the underlying climate risk metrics and modeling. In addition, limited data on carbon intensity may make it difficult to develop hedging strategies. Another challenge could be modeling the indirect impacts of climate change, such as supply-chain disruptions, when developing new derivatives contracts or hedging instruments.

The Financial Stability Board also encourages banks to infuse climate risk assessments into collateral policies in addition to credit policies.4 The outcome of stress tests can shape those guiding principles and indicate where firms should adjust collateral requirements for borrowers or begin to demand credit insurance and other sources of risk mitigation from counterparties.

When measuring transition risk, one challenge banks have encountered is aligning climate change scenarios’ long-term timelines with the much shorter duration of loan book commitments.

Given that these practices have yet to mature, banks will likely need to develop new strategies to work with counterparties to hedge climate risk. This could include opportunities to collaborate with insurance firms and other entities to design derivative contracts for climate risk.

Ongoing monitoring and management of credit portfolios, including those of new and existing clients, will require banks to develop new methodologies to quantify climate risk at the borrower and portfolio levels, and conduct stress testing using different climate scenarios. Banks can refer to the Network for Greening the Financial System’s climate scenarios as a resource for assessing physical and transition impacts across six projections for climate policy, emissions data, and global temperatures. Its data includes macroeconomic variables and country- and sector-specific considerations.5

These complex exercises require a combination of statistical techniques and subjective judgment. The simulations should seek to make inferences on climate-related losses even if there may be limited historical data to draw from. As projections look further into the future, these challenges will likely become even more difficult.

Top-down and bottom-up methodologies can then be deployed to assess the quantitative impact of climate risk on default probabilities and expected losses. The top-down module starts with a fundamental analysis of the impact of climate scenarios on balance sheets and income statements. It then calculates what those outcomes could mean for borrowers’ probability of default (PD).

The bottom-up module combines forecasts related to fuel costs, carbon prices, energy demands, and borrowers’ characteristics to produce scenario-adjusted financial statements at the counterparty level. The borrower-specific data is then extrapolated up to the portfolio level to measure the impact of climate risks on portfolios’ expected losses. Banks can then apply macroeconomic and scientific expertise to calibrate top-down and bottom-up mechanisms, and fine-tune the risk drivers that indicate how sectors could evolve under different climate scenarios.6

The transmission channel of climate risks determines the choice of risk-related key performance indicators (KPIs)—probability of default (PD), loss-given-default (LGD), or exposure-at-default (EAD). KPIs can shift under different climate scenarios.

To better assess the impact of climate risk on borrower creditworthiness, banks will need additional data, such as emissions, carbon intensity, strategies to manage transition risk/decarbonization, and supply-chain exposure. There are several methodologies being developed to assess borrower creditworthiness, including examining how markets are pricing companies based on their exposure to transition risks, which can indicate what investors foresee for those businesses’ future cash flows. Another option is to modify Merton’s 1974 distance-to-default model, which treats a firm’s equity like a call option on its assets, to predict default events.7

Common techniques for integrating climate risks into banks’ portfolio management include negative screening, limiting exposure to certain risk sectors as a share of total financing, and installing automatic vetoes on the credit granting process if certain environmental protection issues are present.8

Multiple data sources can be used to better understand the global economic and market impacts of a climate shock, including those related to extreme weather events, crop-yield deficiencies, labor distortions, or adjustments to electricity generation. Scenario impacts can also test transition risk factors and different policy pathways, and the linkages between the two. Physical events, such as wildfires or floods, can heighten transition risk because policymakers often feel the need to respond with new laws and regulations. The impact analyses can also examine market repercussions, such as changes in equity risk premiums.

After completing these steps, banks can then distill the global scenario analyses down to more specific country-level impacts, and then to more localized, targeted regions. Once these variables are granular enough, they can begin incorporating the climate risk drivers into PD, LGD, and EAD models.

Accounting for stranded assets that suffered from unanticipated or premature write-downs, devaluations, or conversion to liabilities from environmental factors should be another critical consideration of these stress tests. Banks should account for holdings financed by long-duration loans that may have their productive life drastically cut short by shifting demand. In the case of a sudden and abrupt transition jolt to certain sectors—by policy, technology, or otherwise—loan defaults from stranded assets could pose systemic risks to banks and the financial system at large.

Banks should also consider nuances within secondary and tertiary impacts of climate change, and their potential repercussions for other markets. For example, inhospitable temperatures could spur widespread remigration, which would have implications for borrowers in sectors such as health care, tourism, and defense. Similarly, a drought could affect the economics for agricultural firms, which, in turn, could lower demand for farm machinery, affecting their creditworthiness.

To reconcile this “duration inconsistency” between the longer-term horizon of climate change effects and the shorter-term duration of loan portfolios, banks can retrofit their macroeconomic stress tests to assess climate risks. But they will likely need to tweak their methodology to forecast scenarios that extend well beyond the maturity of existing portfolios. In addition, banks should integrate more analysis of borrower and counterparty behavior and factor in the realities of climate risks emerging more quickly and with shorter-term implications than in years past.

The annual supervisory tests that US banks currently conduct only look ahead nine quarters. US banking regulators plan to administer climate stress tests, while also indicating they may look for novel approaches from other jurisdictions. The Bank of England’s projections must include scenarios that play out over a 30-year period.9

Credit departments may also need to refine their processes for monitoring credit portfolio performance, and managing covenants, payments, limits, and concentration risks and breaches. They should build climate risk metrics into their analysis of portfolio holdings, factoring in data on GHG emissions, loss assessments, and other indicators of environmental performance. Portfolio managers and analysts inhibited by a lack of data from clients who have not yet perfected their reporting mechanisms can try to find other ways of gathering information that would provide similar insights into that company. They can benefit from more frequent meetings or site visits, or increased security of accounts receivables, inventory, and fixed-asset capitalizations. The guiding objective, however, should be to capture data in an accessible manner alongside existing reporting metrics already used throughout bank functions.

Banks should also monitor whether clients are abiding by covenants linked to sustainability, which are increasingly being added to contracts to keep clients moving toward environmental goals. These covenants are especially important for banks that committed to net-zero ambitions. If borrowers lapse on their transition and resilience strategies, banks could fall behind in their own climate commitments. Green covenants also aim to improve corporate behavior through indicators of environmental performance, which can include installing energy-efficient lighting or transitioning to electric delivery vehicles. Covenants can also tie financing to certain projects, or require that borrowers only deploy loan assets for activities that use more renewable energy sources than fossil fuels.

Default management is another area that will likely require banks to make some changes as a result of climate risks.

Managing the recovery process, when the primary culprit is climate risk, might also pose fresh challenges. These may translate into other decisions, such as selling loans in the secondary market and negotiating a workout agreement.

Data capture and storage could also be critical to default management. Banks should be aware of the root causes for defaults, and assess whether climate was a factor, even if it doesn’t seem related to the loan losses. For example, a technology company may have failed to pay back the principal and/or interest due to supply-chain issues that link back to a devastating flood somewhere else in the world.

Banks should also incorporate data on late and default payments that result from climate change into credit risk appraisals. If they fail to incorporate root causes springing from climate, they will likely underestimate these risks in their credit models. They should also consider how defaults at other institutions may bring about second-round losses that impact their balance sheets due to interdependencies in the financial system.

Regulators, investors, and other stakeholders are demanding more detailed and timely disclosures of businesses’ climate-related risks and opportunities, and are increasingly scrutinizing plans for resiliency against short-term, medium-term, and long-term climate scenarios. While the private sector has not yet agreed upon a common framework for comprehensive corporate climate reporting, there are a handful of established standard-setters that watchdogs deem to be the most authoritative. In some jurisdictions, some have become mandatory for companies to follow.

Two bodies that are widely embraced around the globe are the Sustainability Accounting Standards Board (SASB), which issues guidance on ESG topics for investors, and the Global Reporting Initiative (GRI) Standards, which allows organizations to share how they’re managing impacts on society and the environment. In addition, in Europe, the Sustainable Finance Disclosure Regulation (SFDR) requires financial firms to classify products according to one of three defined categories, depending on their sustainability focus.10 Meanwhile, US regulators are weighing rules that would mandate more quantitative and qualitative reporting of climate risks, including an accounting of GHG emissions released by a company and its value chain.11

The Task Force on Climate-Related Financial Disclosures (TCFD) represents one of the primary methods of measuring, managing, and reporting climate risk within credit portfolios. The voluntary group includes nearly 300 global banks with a median asset size of US$66 billion.12

The TCFD framework requires reporting across four dimensions: governance, strategy, risk management, and metrics and targets. Many banks are building out their TCFDs as their climate risk protocols mature, and currently include risks and opportunities over different time periods, and the role of management and boards in managing both. Many of these analyses may be subjective in nature as judgment calls will likely play a large part in risk evaluations.

The TCFD’s recently updated guidance further delineates how banks should forecast the financial impact that climate change could have on a client’s operations within an estimated price range across short-term, medium-term, and long-term time horizons. The guidance calls for banks to explain the “significant” concentrations of credit exposure to climate risks in quantitative and qualitative terms, and disclose their processes for climate risk management in the same level of detail as they do market risk, liquidity risk, and operational risk.13 The group also calls on banks to disclose emissions according to standards established by the Partnership for Carbon Accounting Financials (PCAF), an industry-led effort to harmonize GHG accounting methodologies across institutions of all types and sizes.14

Other prominent disclosure methodologies include the UN-backed Science Based Targets Initiative (SBTi), which unveiled a pilot framework containing recommendations for drafting and validating emission targets.

Banks’ exposure to climate risk spans both their wholesale and retail sectors. The wholesale banking business is primarily susceptible to transition risks, since clients include companies, governments, and public sector enterprises that must take significant strides to reduce or offset carbon emissions. Many of these entities may also need to adjust to changes in consumer behavior and prepare for new policies from regulators.

Transition risks are elevated in sectors that still rely on carbon-intensive technologies, have limited insurance availability, or need significant effort to become more energy-efficient. These organizations are likely to be scrutinized by regulators, consumers, and environmental advocates, and effects on credit can vary depending on asset-level considerations.

Given that climate change has differential impacts on each sector of the economy, banks should adopt a sectoral approach to analyzing climate risk in their credit portfolios. For instance, the real estate sector and agriculture sectors may be more impacted by physical risks, such as hurricanes or droughts, than would other sectors. Similarly, the coal sector may be one of the most at risk from transition to a carbon-neutral economy because of new regulations, a spike in carbon tax, or its migration to greener technologies.

For mortgage lending, banks should consider both the direct and immediate ramifications of climate events, as well as the cumulative effects of environmental changes. These secondary effects can include changes to the cost of property insurance premiums, shifts in homebuyer awareness of climate perils, and the impact of government policies, such as remapped flood zones and higher anticipated flood insurance costs. Other entities can also contribute to cumulative risk, such as federal agencies instituting insurance-related policies for the mortgage market. When assessing risks, banks should also consider that climate hazards may be categorized differently within datasets, even if the events are highly correlated. Among natural catastrophes, for example, hurricanes may be listed as a separate category, distinct from coastal flooding or property damage.

Banks should also take steps to evaluate the ways in which extreme weather events could impact loan-to-value ratios within their portfolios. Differences in each property market will impact the way that property values in those locations will respond to climate events. Banks can use data from past weather events that occurred in their portfolios to guide those assessments.15

As highlighted above, each industry sector has certain unique elements/dynamics, and capturing those differences and nuances will be key. As is typical in other areas of climate risk analysis, gaining access to the right data and imposing the right assumptions may take some effort.

Banks will likely base their assessments of climate risks using both internal and external resources. Banks may need to develop internal capabilities to measure climate risk by coordinating efforts among specialists in sustainability, credit risk, stress testing, and investor relations. But given the shortage of expertise and talent in climate risk modeling, many firms supplement their work with third-party vendors that have extensive experience developing and validating climate models. Banks should be carefully vetting these vendors before they come on board by heightening due diligence of their data quality and process validity.

Credit rating agencies can help expand the climate risk dialogue through their use of new analytics, modeling, and insights. They are developing new metrics and methodologies to assess the impact of climate change on their credit rating models.16 Some credit agencies are also publishing standalone ESG scores that analysts and investors can use to understand how sustainability factors could impact credit quality. These scores take into account the potential for adverse effects from climate change, as well as the precautionary measures they’re implementing to shield against natural disasters. They also look at areas where firms may be liable for cleanup costs or capital costs, and ways they could be impacted by water shortages or other depleted resources. In addition, they consider each issuer’s ability to adapt to a carbon-neutral economy by evaluating characteristics such as scale, geographic concentration, experience handling regulatory issues, and trends in market demand.

Regulators, research institutions, and financial institutions are also collaborating on climate projections that can be used for scenario testing and analysis. For instance, last year, the NGFS released a user guide that instructs firms on how to begin analyzing climate risk. The guide included six scenarios that can kickstart the development of forward-looking assessments.17

Other joint ventures have produced instruments that are increasingly being integrated into risk management processes as well. These include the Paris Agreement Capital Transition Assessment (PACTA) software tool for corporate lending portfolios, which became publicly available in September 2020.18 The software allows users to perform scenario analyses across five sectors: power, fossil fuels, automotive, steel, and cement; new sectors will be rolled out periodically. US banks are also building pilot applications that embed strategies from PCAF and the United Nations.

While many proprietary tools and models remain far from perfect due to the suboptimal quality of data, uncertainty about the effects and interactions among variables, and the robustness of models, they are a good starting point.

In addition to gaining an understanding of their loan portfolio’s exposure to physical and transition risks, banks should also prioritize coaching and educating board members and/or senior managers on these topics, especially those who may lack the subject matter expertise necessary to grasp the full implications of climate change on credit, market, and operational risk. In some jurisdictions, board members may be legally required to adequately govern climate risk.19

Once bank leaders better understand these risks, they can begin crafting strategic objectives based on where they are most vulnerable. These goals can include setting emission reduction targets for lending and investing activities, enhancing disclosures to show which assumptions and methodologies will be used to decarbonize portfolios, and performing stress tests with longer time horizons. During the planning stage, banks should determine all the resources they will need to accomplish these tasks, which can include subject matter experts, vendors, data providers, and model development specialists. They could also consider specializing by sector and client type.

Each bank’s priorities for integrating climate risk into the credit lifecycle will typically depend on the maturity level of its risk management programs. Many financial firms share knowledge across risk functions, but may need to coordinate climate risk management across the entire organization. Under this more evolved model, the appetite for climate risk is explicitly defined, and the organization works cohesively to monitor, measure, and report on climate risk management. Ultimately, banks are expected to embed climate risk into strategic planning, product development, and other means of value creation. Leading banks will likely also link climate risk management to organizational performance and performance-based incentives.

While the specific responses to physical risks and transition risks stemming from climate change may vary, banks should follow the shared guideposts that can lead them toward a carbon-neutral future.

Embedding climate risk into banks’ credit risk management framework might not be an easy task, but it will increasingly be an essential element in fueling the transition to a net-zero economy.

Co-authors Val Srinivas and Jill Gregorie wish to thank Naz Asli Öncel for contributing to this report.

Cover image by: Willy Sions