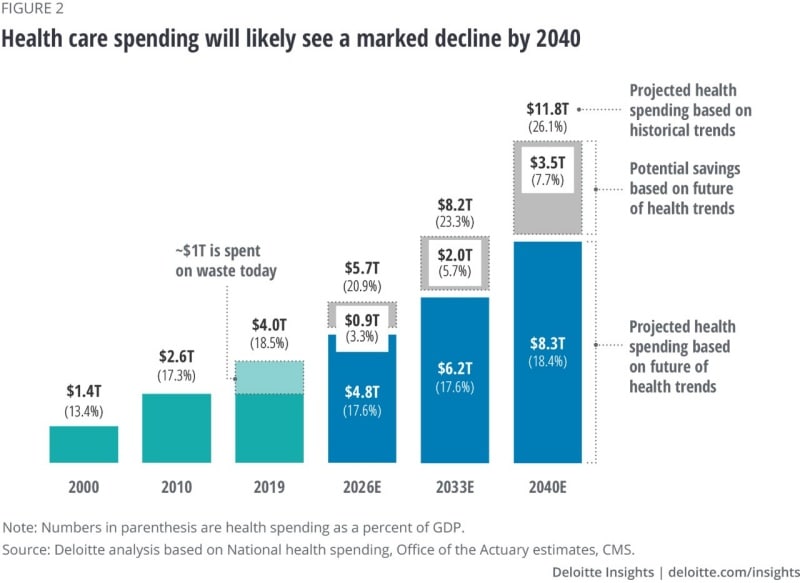

While Deloitte’s projection runs counter to historic trends, we believe the US health care system has already entered the first stage of the Future of Health—a dramatic transformation that we expect will take place over the next 20 years. This future will likely be driven by new business models, scientific and technological breakthroughs, consumers armed with highly personalized data, and regulations that encourage change. We see this as an unstoppable transformation, meaning that it will happen regardless of policy or the actions of individual stakeholders.

Has change already arrived?

It has been two years since Deloitte published Forces of change: The Future of Health, which provides our perspective on how the business of health will transform by 2040. Since that publication, we have experienced COVID-19, a global crisis that has not only accelerated the changes we outlined in our vision, but also identified where our ecosystem still requires significant progress. Rather than focusing on clinical care and symptomatic diagnoses in 2040, the enterprises making up this new health system will likely be hyper-focused on early engagement with consumers. We expect this will drive new business models that integrate data and support overall well-being. COVID-19, for example, is highlighting some of the weaknesses in the health system, pushing capacity to the brink, and testing the very definition of wellness. It has also revealed how vulnerable the health care industry is to change and its need for structural and technological transformation.

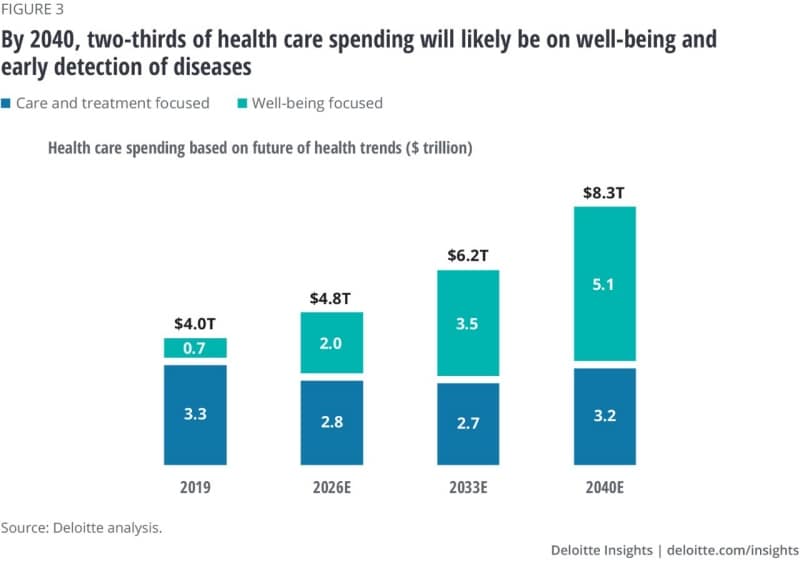

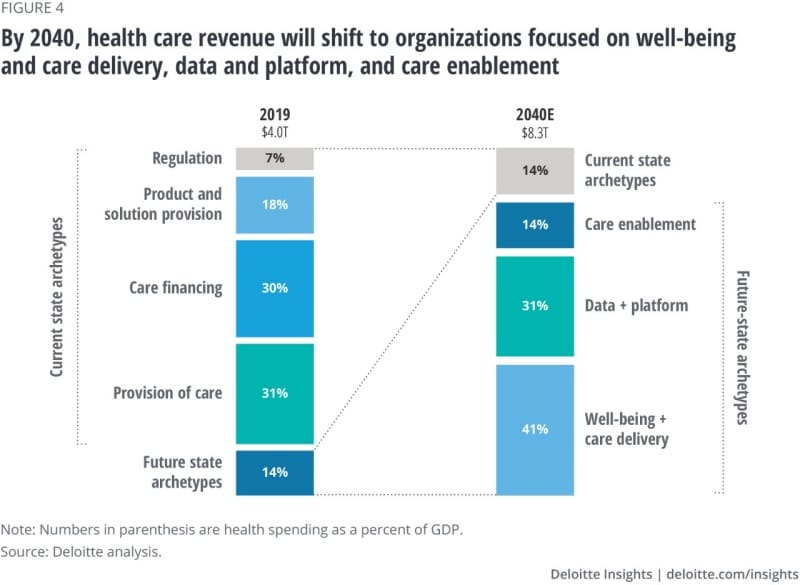

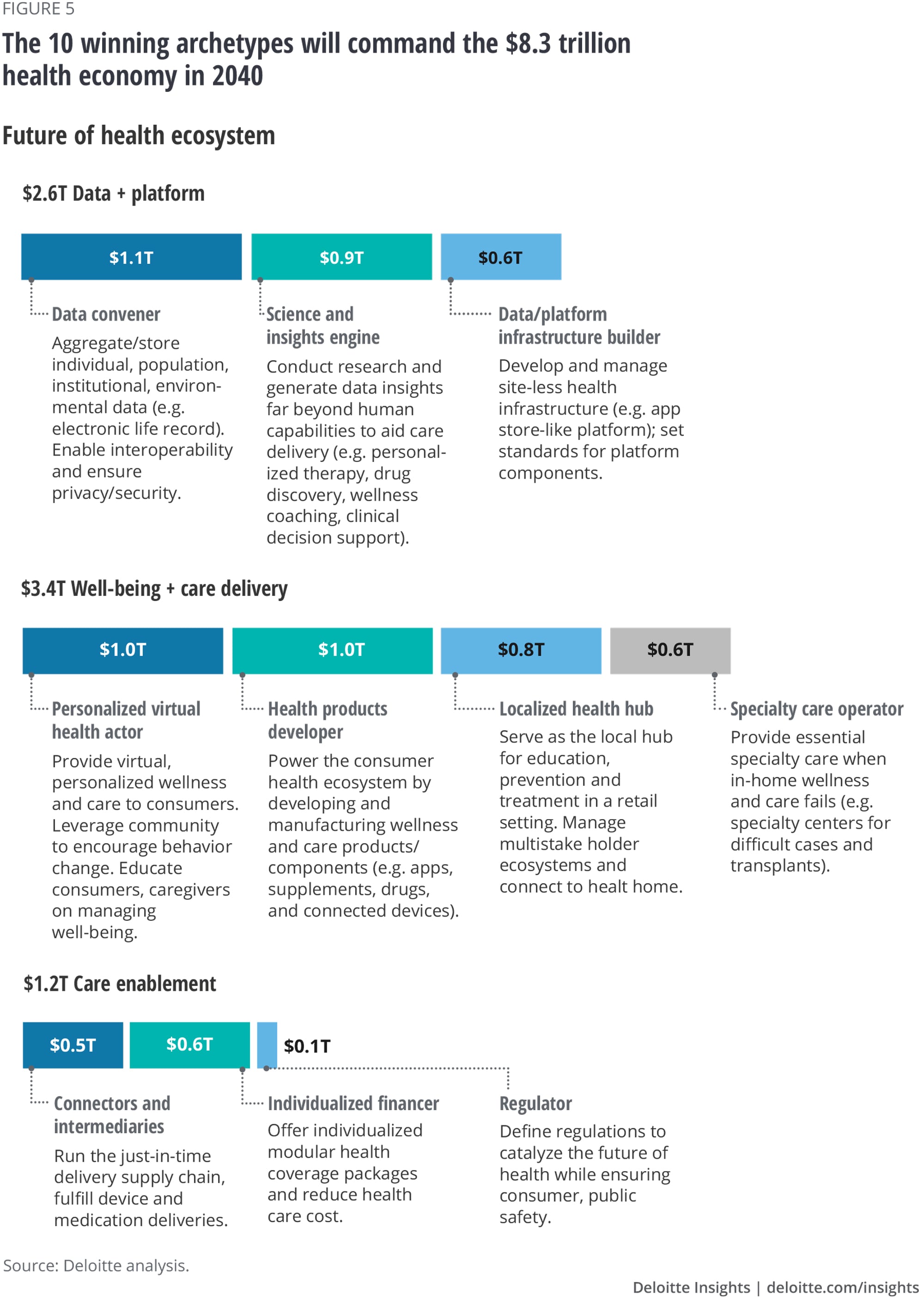

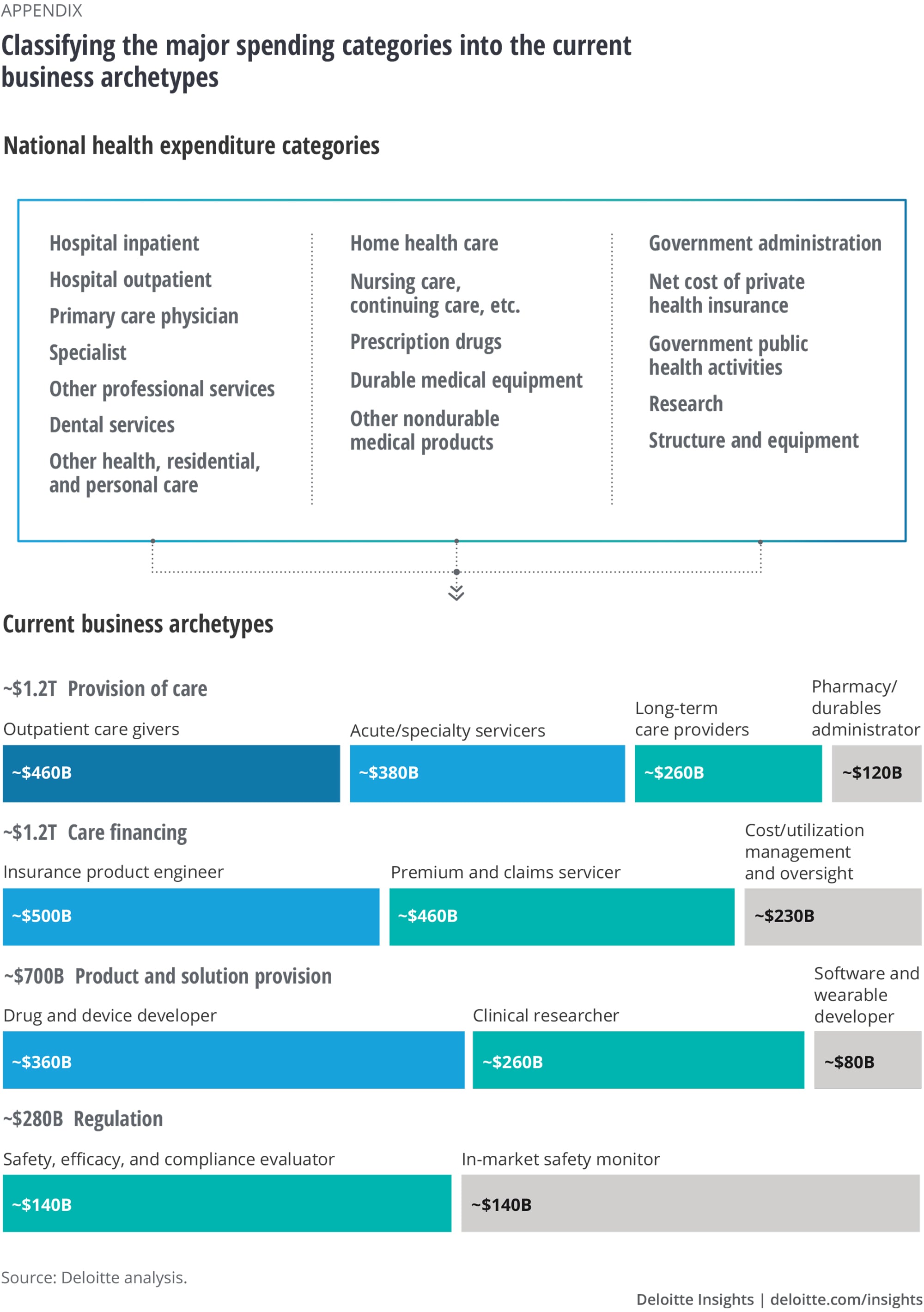

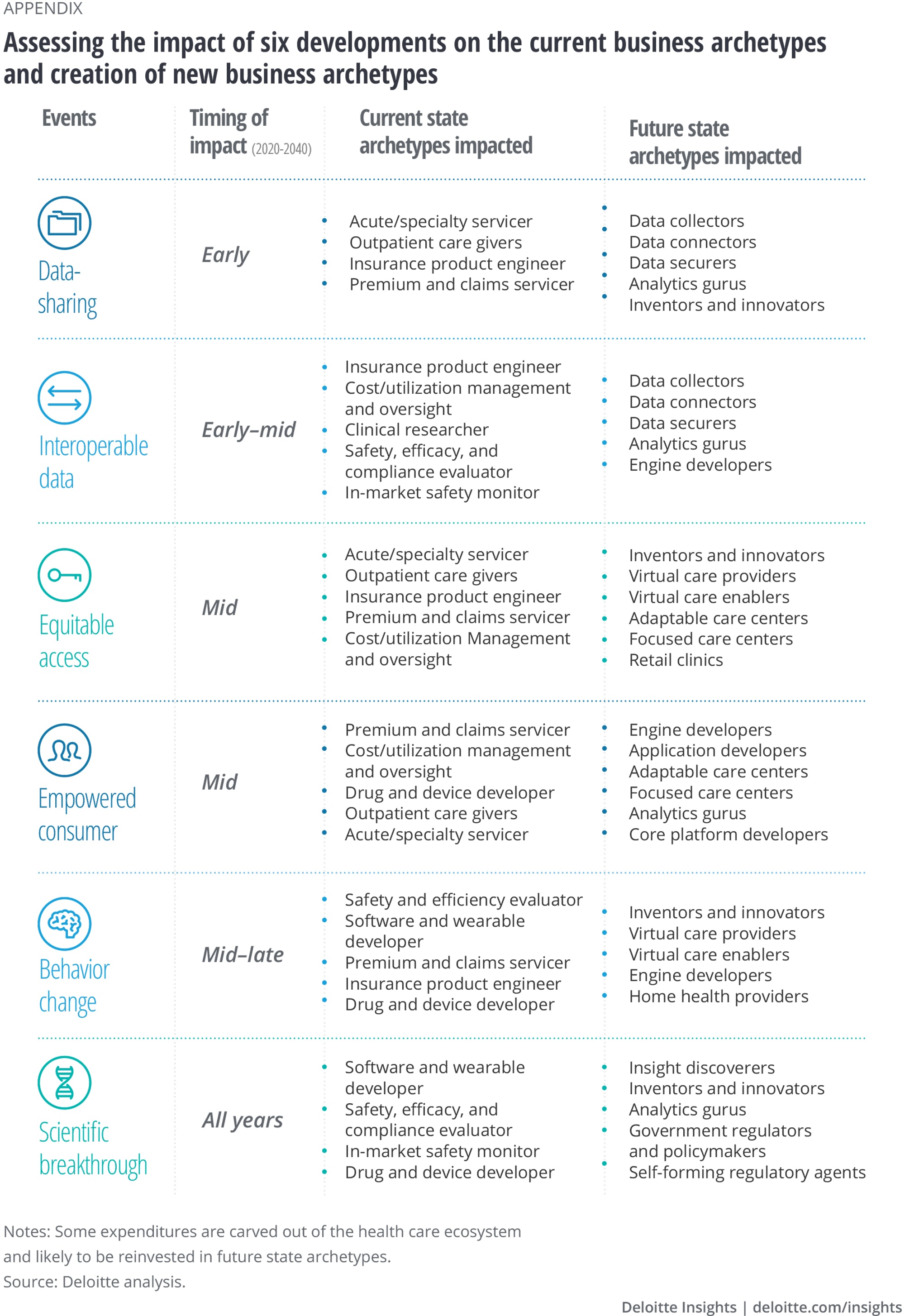

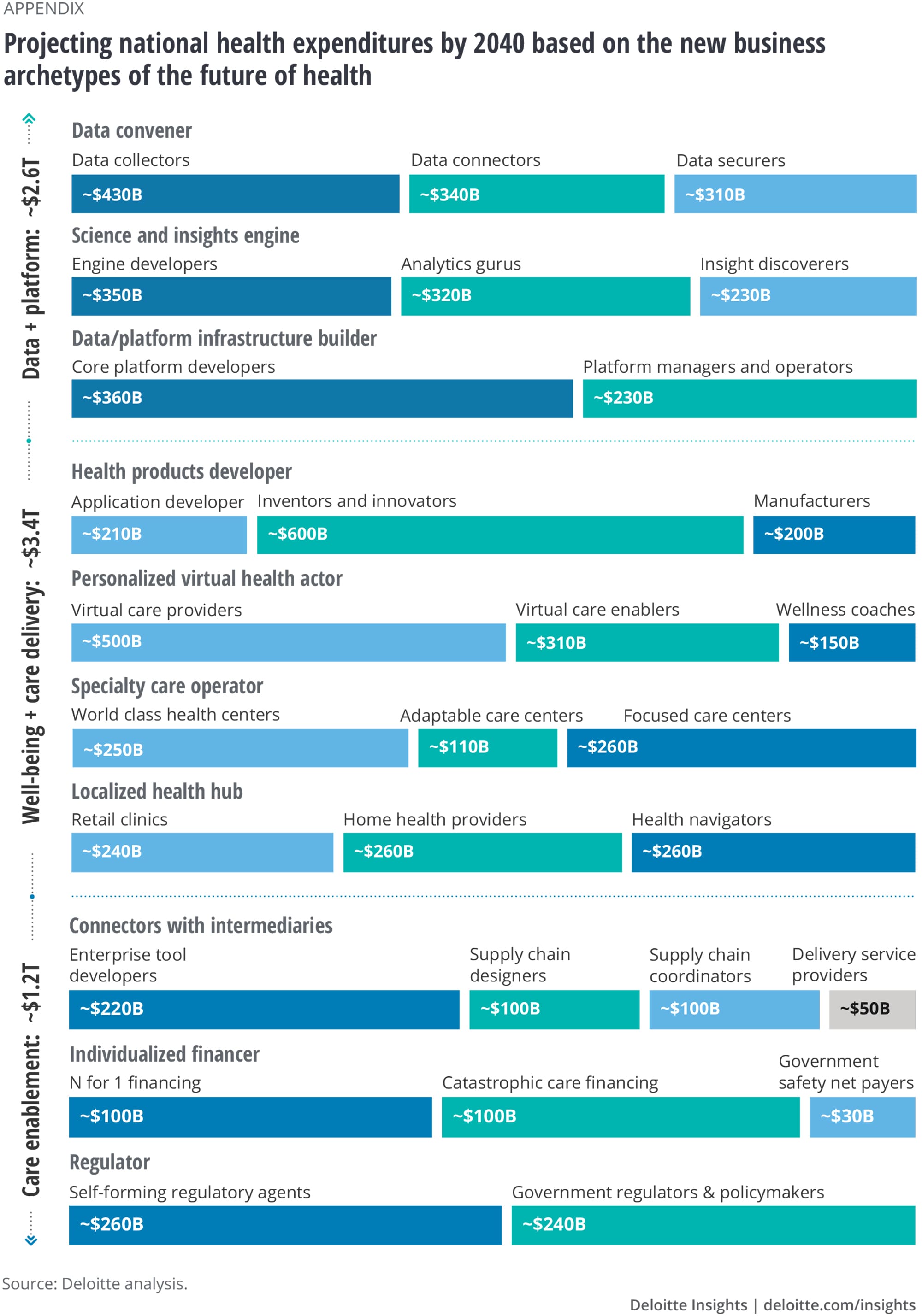

A team of Deloitte actuaries analyzed the financial implications of this Future-of-Health vision. The team started with the most recent NHEA categories, as well as spending on wearables, fitness apps, DNA testing, genetic services, weightloss/nutrition/diet, alternative therapies (e.g., acupuncture), and other mental health–related services (e.g., meditation, couple’s therapy). That information was then used to model the impact of the six key areas—data sharing, interoperability, equitable access, empowered consumers, behavior change, and scientific breakthrough—that we expect will collectively transform the existing health system from treatment-based reactionary care to prevention and well-being. In our recent research paper, Six keys to measuring health care disruption, we discuss the activities already underway in each of these areas. The financial impact of each area will likely differ based on timing, intensity, and the expenditure category. Based on these trends, the team projected the shift from current businesses to newer archetypes—roles, functions, and businesses that will drive the Future of Health. (See appendix for detailed methodology.) Here are the six areas that we expect will have a profound impact on the health sector over the next 20 years:

1. Data sharing: Data sharing is already underway and will likely continue to advance. In the years ahead, always-on sensors—embedded in everything from our shoes and clothes to our bathroom mirrors and toothbrushes—could continuously gather detailed information about our health. (Imagine a toothbrush that uses biomarkers to identify heart disease years before symptoms develop.) As we collect more health data from a far deeper pool of consumers, we will likely learn more about the nature of illness, how to detect it, treat it, or avoid it. Our research indicates that 46% of consumers are willing to share their medical information with health plans and clinicians, and 20% have used technology to measure and share medication data with their doctors. Example: The Apple Health records feature is now open to all US health care organizations with compatible EHRs.2 This feature will allow more than 100 million iPhone® consumers to link their health data from several sources and share it with their care teams.

2. Interoperable data:On March 9, 2020, the US Department of Health and Human Services (HHS) finalized its interoperability rules, which HHS Secretary Alex Azar called “the start of a new chapter in how patients experience American health care.” The new rules took effect on January 1, 2021. Through interoperability, the disconnected components of health care (e.g., hospitals, clinicians, pharmaceutical companies, device manufacturers, researchers, and health plans) could be replaced by a system where data is securely shared among stakeholders to create a multifaceted and highly personalized picture of every consumer’s well-being. Example: Real-world evidence (RWE) based on interoperable data could lead to more personalized and effective treatments for cancer and other high-cost diseases.

3.Equitable access:Consumers who aren’t able to access the health system when needed might wind up with more serious (and costlier) health conditions. Urgent care facilities, retail clinics, and a growing acceptance of virtual care are making it easier for patients to meet with care providers in person or via electronic device. Traditional barriers to health care access, like geography and lack of resources, could be significantly reduced. Consumers might also have access to tools that help them achieve their wellness and health goals. Stay-at-home mandates and risks (real and perceived) related to seeking in-person care have increased demand and adoption of virtual care, especially among vulnerable populations. Example: Deloitte’s COVID-19 survey as of April 2020 showed that 26% Medicare Advantage members used telehealth or virtual health through the first four months of 2020, compared to just 13% for all of 2019.3

4. Empowered consumers: We expect clinicians will work closely with each other, supported by health plans, to coordinate care for consumers. But highly personalized health information can allow consumers to take a more active role in their well-being. Ownership of their health data can increase people’s sense of responsibility for their well-being. Example: In 2020, more than 40% of surveyed consumers used devices and technologies to measure fitness and health improvement goals, compared to just 17% in 2013, according to the Deloitte Center for Health Solutions’ Health Care Consumer Surveys.4

5. Behavior change: In 2019, 600 Deloitte employees (from 40 states) began a 36-week randomized clinical trial to determine if a wearable activity-tracker—combined with goalsetting, competition, and gamification—would increase physical activity among overweight and obese adults. We learned that data science and behavioral economics—if applied correctly—can lead to positive behavior changes. Example: Mango Health is a patient-adherence platform that uses gamification and rewards to improve drug adherence, especially among those under chronic care with proven clinical results.5

6. Scientific breakthrough: The pandemic forced some researchers to rely more on digital technology for clinical trials. We have seen an unprecedented level of collaboration among pharmaceutical companies to develop a COVID-19 vaccine and rapidly bring it to market. Some regulatory processes have been streamlined to make it easier to get diagnostic tests and therapies to market more quickly. During the next 20 years, we expect new preventive and curative advances will emerge at an exponential pace. We expect biopharmaceutical companies will continue to develop new ways to prevent, treat, and possibly cure a range of diseases through vaccines and advancements in cell and gene therapies. At the same time, actionable health insights—driven by radically interoperable data and smart artificial intelligence—could help clinicians and consumers identify illness much early than we do today. Example: Biopharmaceutical companies Pfizer Inc. and Moderna Inc. developed their COVID-19 vaccines using messenger RNA (mRNA)—a technology that had never been used before to develop a commercialized vaccine. Both companies, based on the clinical trials, reported efficacy rates above 90%. This was significantly higher than the Food and Drug Administration’s (FDA) requirements of at least 50% efficacy.6

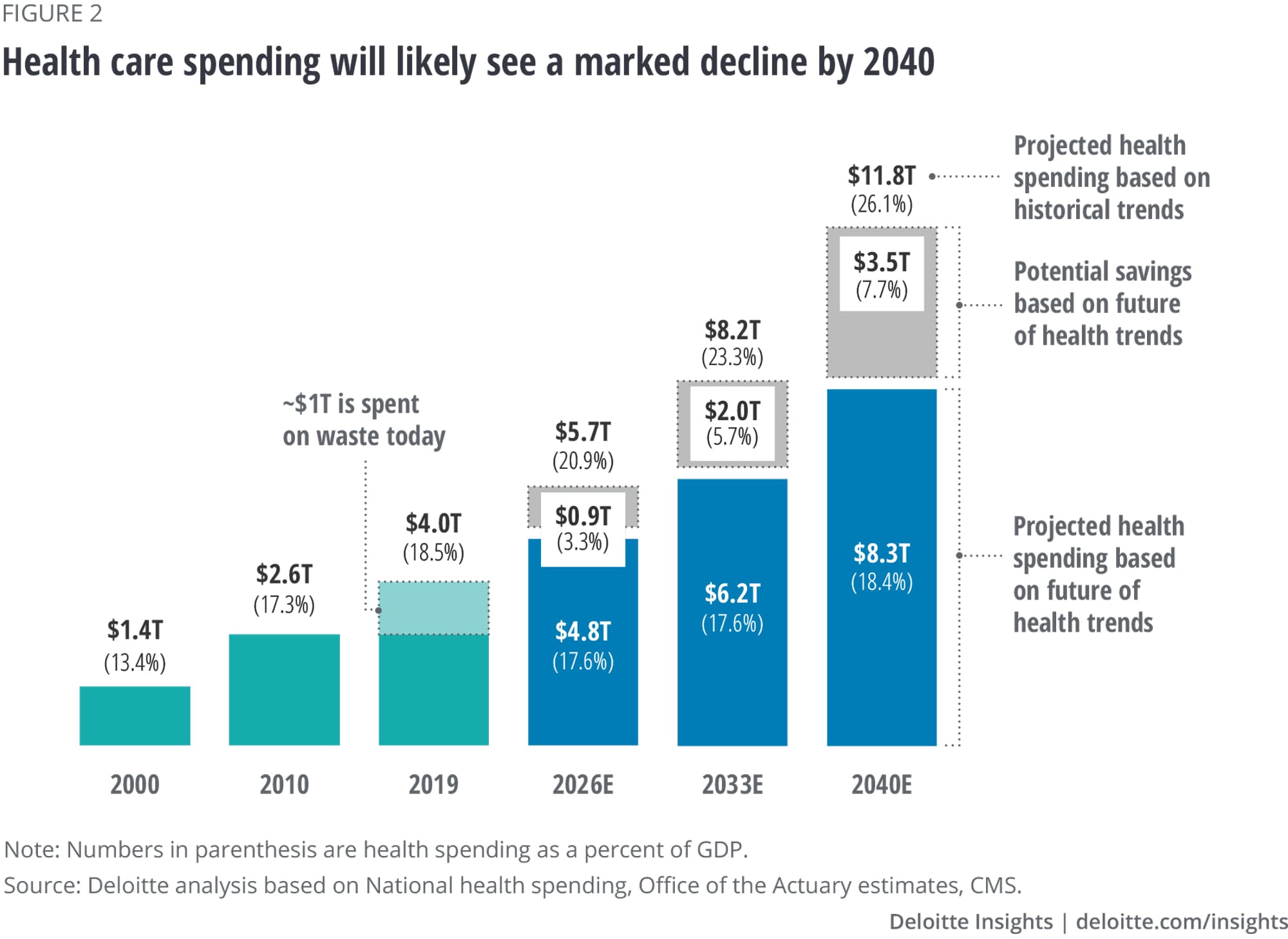

We assume these six developments will help shift the spending from areas of waste to investments that improve individuals’ long-term well-being, helping to curb growth in health spending (figure 1).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}