Digital media trends has been saved

The authors would like to thank Kevin Downs and Shashank Srivastava for their knowledge and support developing this research.

Cover image by: Josh Cochran

Although the shift to streaming video services may seem inevitable, the media and entertainment industry is facing significant changes to more than just distribution and engagement. One of the most profitable business models appears to be fading. For decades, cable and satellite-based pay TV have enjoyed margins typically reserved for energy companies.1 In recent years, however, more of their audiences have been cutting the cord and subscribing to paid streaming video services. In the process, the historic margins sustained by pay TV subscriptions and advertising revenues have been challenged and may not survive the next generation of media and entertainment.2

It will not be easy for media and entertainment companies to navigate this change. Launching a streaming video service is only the first step toward engaging, acquiring, and retaining audiences—and finding revenues to support it all. In this article, we focus on the evolution of streaming video services that rely on subscribers for most or all of their revenue. Paid subscriptions are the dominant business model for streaming video services in the United States, although competition from free ad-supported services is growing. With more competition and subscriber churn, how can streaming video providers better understand where the industry is going and how to unlock enduring value?

In the near term, providers may need to spend more to make less, building the foundation for the new era of video entertainment. Their investments could also unlock new kinds of value, however; providers may be able to learn more about their customers, meet more of their diverse needs, and predict when they might leave. Content will always be king. But with the rising costs of producing TV and movies and the prevalence of “hit and run” subscribers who watch the hits then run for the door, streaming services may need more than great content.

How can streaming video services attract, and most important, retain subscribers when consumers have so many choices and can so easily switch services? Beyond great content, focusing on providing additional benefits to retain their customers could be key. If providers can treat their subscribers more like valued members of a club, they may be able to deliver more value and create more loyalty with privileges and personalization.

In our October 2020 Digital media trends pulse survey of US consumers,3 we saw a maturing market for streaming video: 76% of respondents said they subscribe to at least one paid service, a 21% jump since 2018. Remarkably, consumers who subscribe to a paid streaming video service now hold an average of five subscriptions—up from three just before the COVID-19 pandemic. Between stay-at-home norms and the launch of new premier services, the pandemic has amplified subscriber growth, not only for paid services but also for more ad-supported options. The use of free, ad-supported video has grown substantially since the start of the year, and free trials and discounts have boosted subscriber counts while driving up acquisition costs.4 Competition is stronger, the landscape is more dynamic, and consumers have more options to discover content and find value.

Paid streaming video services have become the new normal for most US consumers. In 2020, the “streaming wars” accelerated, with most major pay TV players deploying their own direct-to-consumer subscription services and spending heavily on content—and customers. Deloitte estimates customer acquisition costs for several top streaming video services by analyzing marketing expenses and net subscriber additions over time. This approach does not capture all expenses for acquiring customers, including the escalating costs of developing strong original content. But it gives us a ballpark estimate for understanding how much streaming video services spend on marketing to attract new subscribers. Depending on the service, providers can spend US$200 per year on marketing to acquire a single subscriber.5

To recoup that investment, providers must draw monthly subscription rates from a new subscriber for up to 15 months, depending on the subscription tier and cost. When consumers join a service that is offering free trials or discounts, or join to watch a specific show and leave, streaming services are likely losing money. Consumers are enjoying the fruits while providers must continually work to attract and retain them. With so many a la carte offerings—and little friction between viewing and cancelling—consumers are shuffling services with greater gusto, grabbing free trials, chasing original content, mining ever-shifting back catalogs, and balancing their costs between paid, premium, and ad-supported options. Perhaps more than ever, consumers are in command and providers are facing a harder fight to retain them.

Perhaps more than ever, consumers are in command and providers are facing a harder fight to retain them.

But now, almost a year into the COVID-19 pandemic, some US consumers are carrying greater economic burdens. In our October pulse survey, 29% of respondents reported a decrease in household income since the start of the crisis. In one promising sign, this number has dropped from 39% in May, suggesting some economic recovery for households. Yet, more are seeking ad-supported and free services, and more are reducing their paid services to find the most value for the least cost.

The pandemic has also impacted streaming video providers’ ability to lure consumers with original content. New original content is a major attraction for subscribers, but many productions have stalled due to COVID-19, making it harder for streaming services and the studios they rely upon to keep audiences engaged. Streaming services also face greater competition from other media. To paraphrase the CEO of a top paid streaming video service, providers are competing not just with each other, but with social media and video gaming.6

Deloitte fielded three surveys of US consumers throughout 2020 to better understand ongoing trends in media and entertainment, particularly under the influence of the COVID-19 pandemic.7 Overall, the trends we’ve seen in recent years have continued in 2020; in fact, some have been greatly accelerated by the crisis.

At the very start of 2020, US consumers subscribed to an average of three paid streaming video services. By October, that number rose to five (figure 1). On the surface, this looks like good news for providers.

But consumers are also cutting services more frequently. While they have more paid subscriptions than ever, they may not keep the same services for very long. In our January 2020 survey, only 20% of respondents who subscribed to a streaming video service had cut a service in the previous 12 months, but by October, 46% had cut at least one in just the previous six months. This may be partly driven by economic pressures.

In our January 2020 survey, only 20% of respondents who subscribed to a streaming video service had cut a service in the previous 12 months, but by October, 46% had cut at least one in just the previous six months.

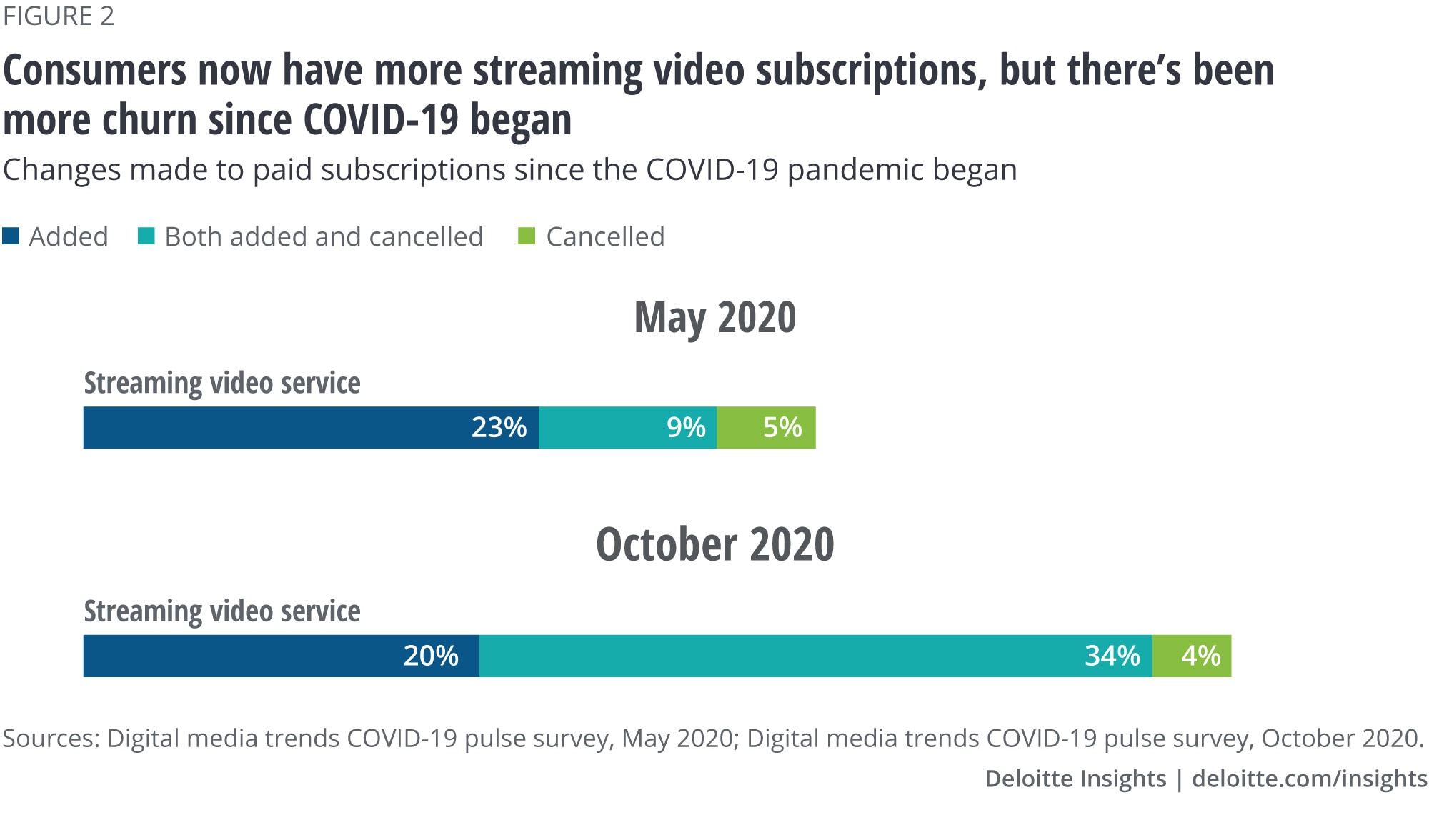

However, consumers are adding services as well, suggesting a much more dynamic nature to the streaming video landscape. In May, 23% of respondents had added a streaming video service since the start of the pandemic, and 9% had added and cancelled services. By October, 34% had both added and cancelled streaming video services (figure 2). The early part of 2020 saw greater acquisition, but the second half has been characterized by churn. While COVID-19 appears to have accelerated streaming video subscriptions, the dynamism we now see is likely the emerging characteristic of a more mature and competitive market.

Certainly, a handful of top providers have established a strong foothold in US households, emerging as the most favored streaming video services in our survey, well beyond the rest. If streaming is an analogy, these are the mighty rivers. They may be debt financed or leveraging other lines of business to subsidize their streaming efforts, but can afford to spend more to acquire subscribers and to offer discounts and free trials. Notably, we found that less than one-quarter of their subscribers are on free trials, and among those who are, many say they would pay full price for the service after the trial ended. To further incentivize subscribers, some providers are offering bundles with other entertainment options in their portfolios or inking partnerships with telecoms to offer free trials with wireless subscriptions.8

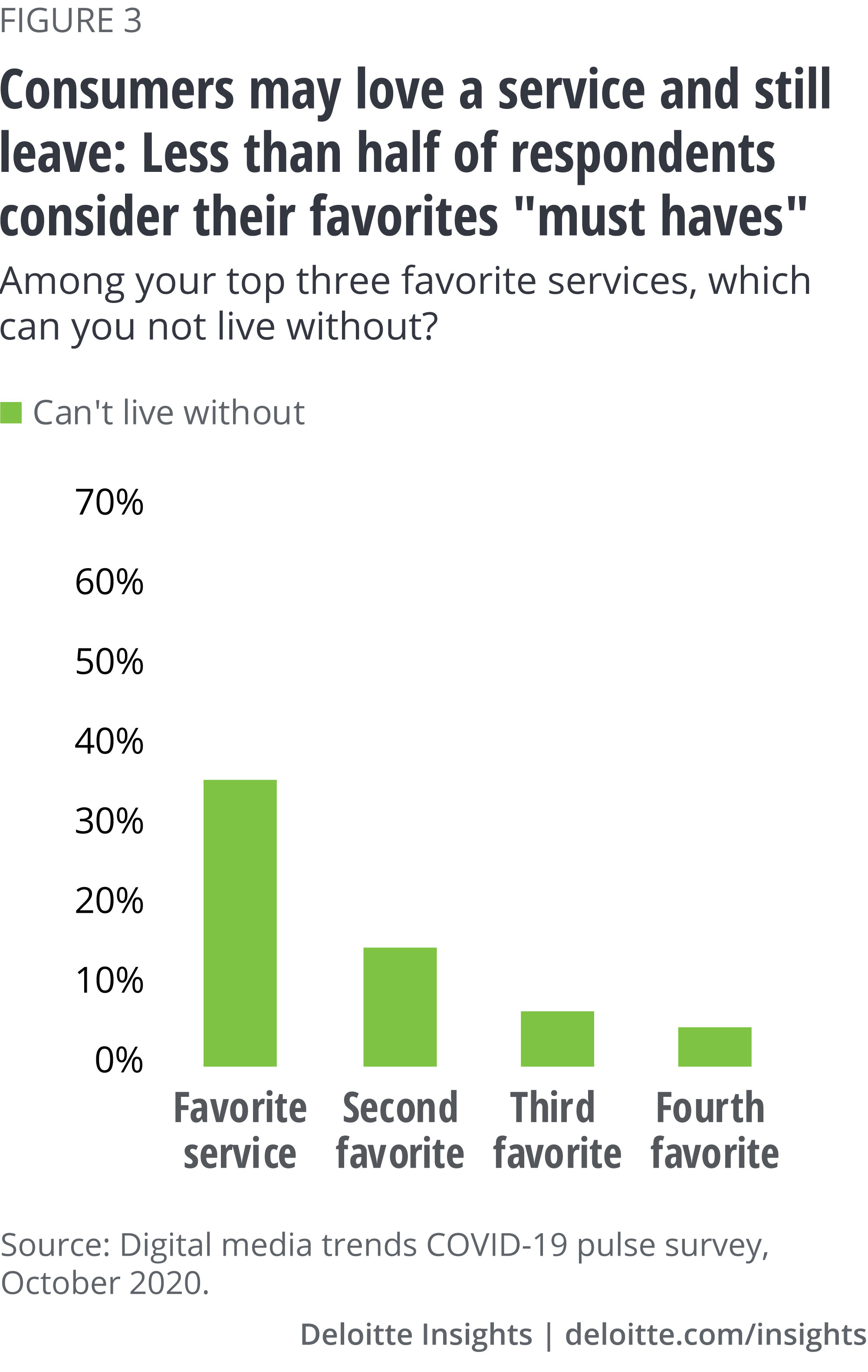

Leading providers may be positioned to continue delivering the clearest value to their subscribers, but they shouldn’t become complacent. Most of their subscribers say that they could live without their services, and a full 19% say they don’t feel strongly about any of their services9 (figure 3). Consumers have many entertainment choices and are more empowered than ever to regularly reassess the value they receive for their time and money. This challenges all providers to know their audiences well enough to keep delivering value.

Throughout 2020, the recipe for engaging subscribers has mostly stayed the same. They want a broad range of shows and movies, and new and original content unavailable on other services. More also want ad-free experiences: Around 35% to 40% of respondents said they prefer ad-free options. By October, 27% of respondents subscribed to a new service because it offered an ad-free viewing experience, up from 17% in May. However, more are also seeking subsidized and free ad-supported offerings. These are becoming less mutually exclusive as consumers add more varying kinds of streaming video services—at varying costs—to their personal baskets of entertainment (figure 4).

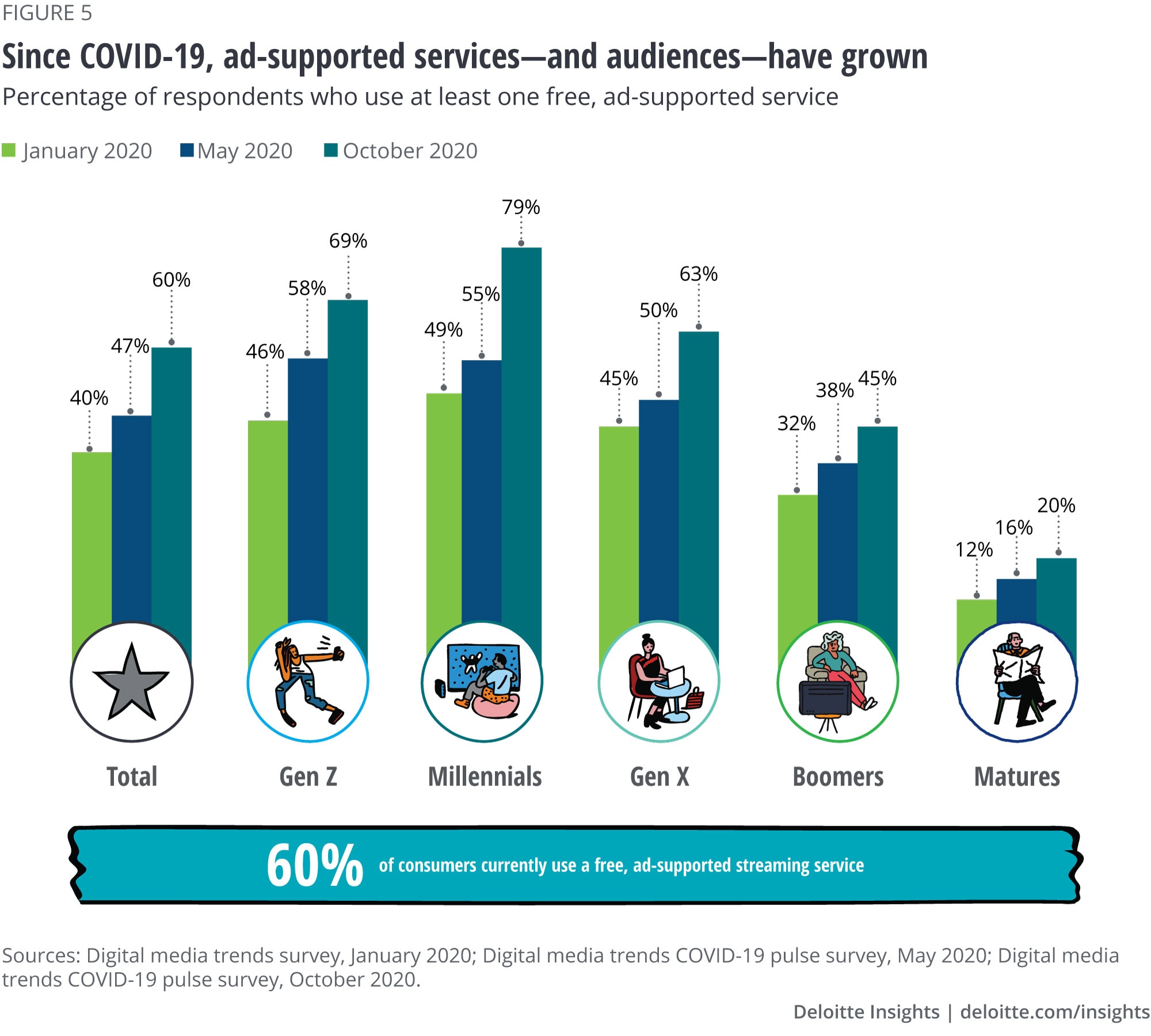

Content is still king, but cost may be the new queen. Among the reasons for cancelling services, the ability to access content on other free services rose from 14% in May to 23% in October. In 2020, the number of US consumers subscribing to at least one free ad-supported service grew considerably, from 40% in January to 60% by October (figure 5). In some cases, this may be due to cost sensitivities. Or it could be that more consumers are becoming aware of free ad-supported services.

As more providers seek to grow ad revenues from young streaming services, finding the balance between ad load and content may be critical to retention. If ad loads are reasonable, most consumers are willing to watch ads in exchange for entertainment. Our respondents say that about seven minutes of ads per hour are “just right.” Pay TV, on the other hand, may load 14 to 20 minutes of ads per hour. Some free, ad-supported video on demand (AVOD) services understand this, and limit ads to five minutes per hour.10

While a handful of premium streaming video services have gathered the bulk of US subscribers, we found that consumers with AVOD services are much more evenly distributed across the top 13 free services. As they manage their own baskets of streaming video services, they may commit to a couple of premium services, juggle more niche or ad-supported offerings, and keep a selection of free AVOD services.

US consumers are maturing and finding ways to maximize the value they get from an array of entertainment options. Among respondents who cut a streaming service since the start of the pandemic, 62% had signed up to watch a specific show and then cancelled once they were done. And they did it quickly: 43% cancelled the same day they decided they no longer wanted the service. This leaves streaming video services with little time to respond. How can providers know more about their subscribers to better match content to their segments and to predict who might churn before they leave?

62% had signed up to watch a specific show and then cancelled once they were done.

43% cancelled the same day they decided they no longer wanted the service.

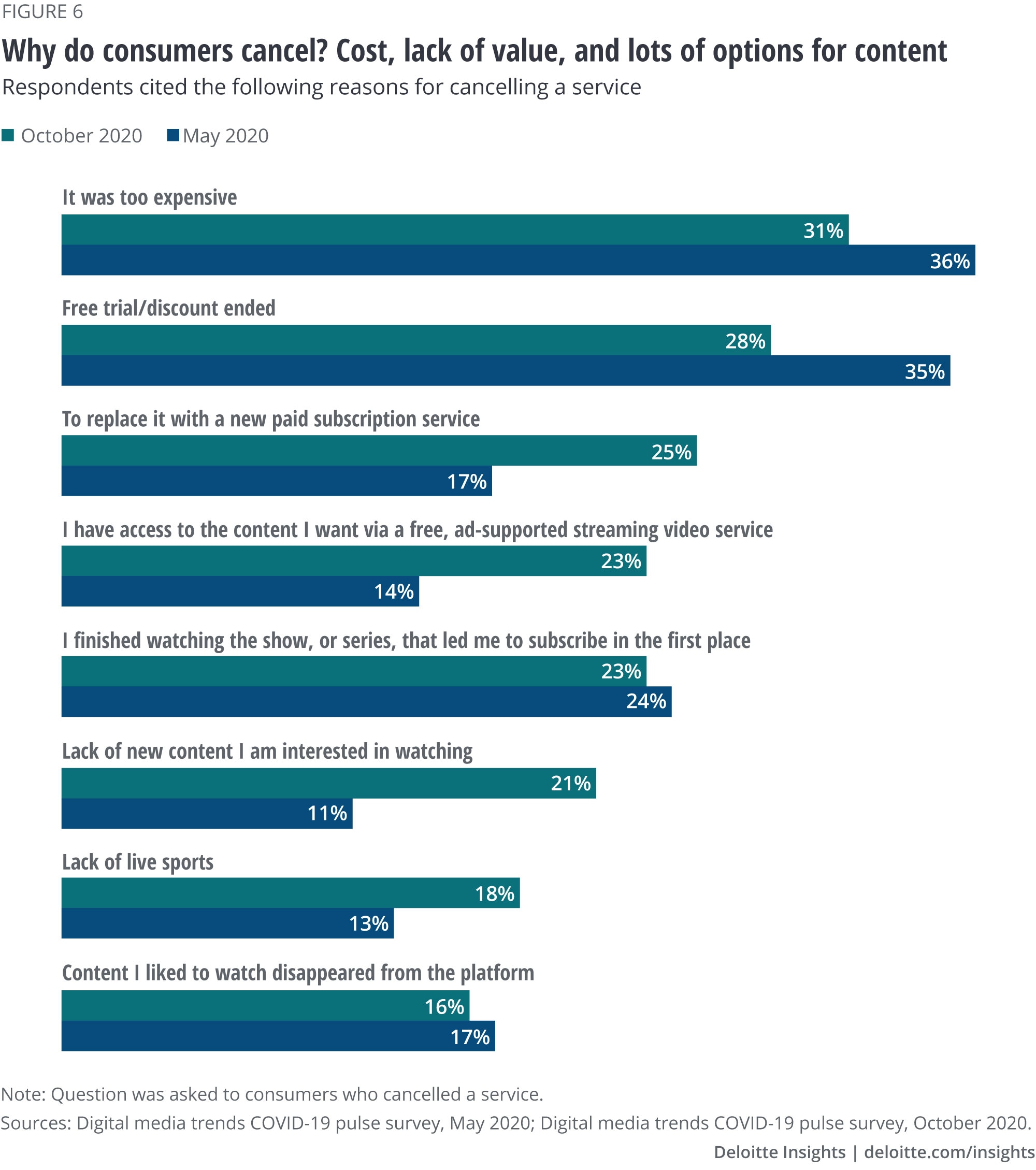

Overall, data from May to October suggests that providers may be getting better at demonstrating value to consumers. Those who cancelled due to cost fell from 36% to 31%, and those who left after a free trial or discount ended also decreased from 35% to 28% (figure 6). At the same time, 2020 was somewhat unique; more major providers launched new services with flagship shows and content catalogs. By October, 25% of subscribers had cancelled a service and replaced it with another new service, up from 17% in May. When all the major services are established, what will keep audiences engaged?

Content and cost: It’s a simple formula hiding a bedeviling complexity. Content development is expensive, especially for premium stories and talent in a highly competitive market, with massive spending from apex acquirers. The formula for hits continues to evolve and fragment into innumerable niches, putting pressure on content development. Meanwhile, audiences are increasingly finding value in ubiquitous online content, social streaming, and video games. Streaming subscriptions are relatively inexpensive, but customer acquisition is costly and streaming services have yet to draw the advertising revenues that have buoyed pay TV.11

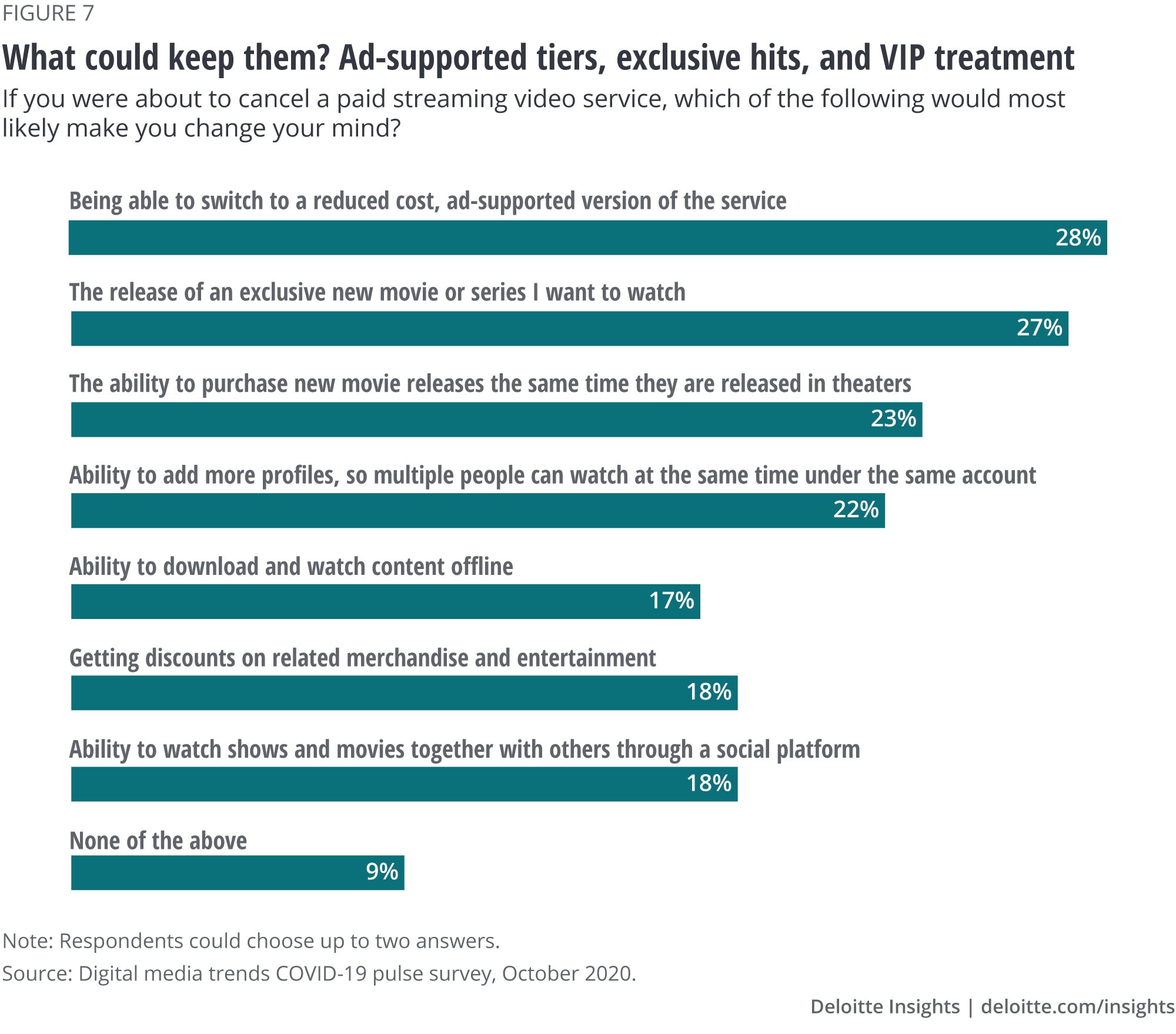

When we asked subscribers what would keep them from cancelling a paid streaming service, 27% would stay to see an exclusive new movie or series they were interested in, and 28% said they would stay if they could switch to a reduced cost, ad-supported tier of the service (figure 7). With climbing costs to develop or acquire content, it may be simpler for streaming providers to offer tiered pricing and then upsell with offers featuring more exclusive services. For example, 23% of respondents said they would stay if they could purchase new movie releases the same day they are released to theaters.

Theaters have been hit hard by the pandemic, and most have endured venue shutdowns and delayed productions of big releases. With consumers at home, some studios have tried to recover losses by releasing directly to streaming services. In May 2020, 22% of US consumers paid to stream a newly released movie at home. Of those who didn’t, cost was the biggest factor. Some consumers bristled at having to pay an additional fee on top of their monthly subscriptions. But by October, 35% had paid for a first-release movie at home. Overall, 90% of respondents who paid to watch new movie releases at home said they would likely do so again.

90% of respondents who paid to watch new movie releases at home said they would likely do so again.

Combining tiered pricing models and access to exclusives could expand audiences while enabling more to feel like members, rather than subscribers. If providers can get to know their audiences better and tailor options to segments, they may be able to show more value and drive retention. They could use the cost lever to attract and retain more subscribers looking for the most value for their dollars, and they could use exclusives to retain members seeking a VIP experience. Like retailers, streaming providers could embrace stronger customer relationship management enabling them to focus more on retaining their high-value customers, potentially lessening acquisition costs.

For providers with other assets across the media and entertainment landscape—or the means to assemble a cross-industry asset through thoughtful M&A—membership tiers could include discounts and exclusives among their properties. Such brands could offer lifestyle services that extend existing franchises and brand loyalty beyond their streaming video services. Consumers may be unwilling to return to the long-term contracts of pay TV, but providers could experiment with other ways to retain them, like rewards programs that lift lower-tier subscribers into premium content and experiences. For providers without such portfolios, direct-to-consumer distribution can help them better understand and anticipate their users’ needs. In each of these cases, accessing the data that digital services offer can help providers lower their own risk and better meet the needs of more of their customer segments.

Streaming video providers have an opportunity to develop systems that can get them much closer to their audiences. Data analytics can enable greater experimentation while lowering risk, helping providers make smarter decisions when developing or acquiring content. For example, they can better predict which combination of stories and actors will resonate with specific audience segments, then develop targeted marketing to get the content in front of those subscribers. Providers that improve modeling of subscriber segments can do a better job matching more relevant advertising to specific audiences, which could help them predict churn with more accuracy and detail. One of the largest and most mature paid streaming video services has used these tactics to effectively drive growth and retention.12 While streaming video providers work to better understand their audiences, they can also extend more targeted options, exclusives, and VIP experiences and, ultimately, provide more value to members.

In the internet age, the landscape of media and entertainment is inherently both networked and fragmented. Consumers may never aggregate the way they did with pay TV, and the industry may never recover their historic margins with the same formula that served them in previous decades. However, the shift to streaming and direct-to-consumer distribution can unlock new kinds of value that were not available before. It can help providers better understand differences among audience members and find ways to keep more of them engaged and entertained.

The disruptions driven by the streaming media revolution have mostly settled into the new playing field. As the market matures, leaders will likely be able to leverage new capabilities to help their companies succeed and grow. These are some of the questions they should consider:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}