{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Brazil has been saved

The authors would like to thank Patricia Buckley, US Economics, and Michael Wolf, DTTL, for their reviews.

Cover image by: Jaime Austin

Just when Brazil appeared to have shrugged off the worst of the pandemic through rising vaccinations, policymakers found themselves facing an old nemesis—inflation. And that too at a time when the economy entered a recession again, at the end of Q3 2021.1 Inflation has gone up sharply this year due to rising energy prices, drought-related disruptions, supply-chain constraints, and pandemic-induced changes in demand. While the Banco Central do Brasil (BCB) has swiftly changed gears to take inflation head-on, policymakers still have two risks to consider. First, the pandemic hasn’t ended, and the threat of new variants of COVID-19 with the potential to evade vaccine protection will remain a worry.2 Second, the BCB will be wary of any repercussions on debt and currency markets from potential monetary tightening in the United States over the next year. While the current account deficit is relatively low and the central bank has a sizeable chest of foreign reserves to counter any sharp currency depreciation, what will concern investors is Brazil’s fiscal health. High debt and the rising cost of borrowing have added to difficulties in the fiscal math at a time of slow growth in revenues. Any slip-ups in deviating from fiscal gains since 2016 may fuel an unwanted cycle of rising debt, higher borrowing costs, and liquidity outflow, thereby cutting off any hopes of a strong revival in economic growth.

Rising inflationary pressures are arguably one of the biggest worries for policymakers, given the recession, weakness in the labor market, and continued global uncertainty about the trajectory of the COVID-19 pandemic.3 Rising inflation also serves as a grim reminder of the period between 2014 and 2016, when elevated price pressures combined with a strong contraction in economic activity. Headline consumer prices have been edging up since June 2020 and went up by 10.7% year over year4 in October 2021, the highest pace of increase since January 2016. It was also the eighth straight month during which inflation overshot the upper bound of the central bank’s target inflation rate of 2.25–5.25% (figure 1).

In the past three months, inflation has averaged over 10%, with price pressures broadening across different parts of the consumer basket compared to trends in mid-2020. For example, prices of fuel for personal transport have grown by 41–48% between May and October this year, while inflation for fuel and energy for housing has hovered between 14–32% during this period; in contrast, in 2020, prices for both fuel categories contracted for much of the period between May and October (figure 2). This uptick in volatile food and energy prices is likely to have percolated into nonvolatile components of the consumer basket with core inflation, as shown in figure 1, steadily moving up since the end of last year to touch 7.3% in October 2021.

Three key factors are pushing up overall consumer inflation. First, global energy prices have been increasing over the past year due to rising economic activity after the initial shock of the pandemic. This is driving fuel inflation higher. Second, energy prices have also been impacted by climatic conditions. For example, a severe drought in Brazil has reduced water reservoirs in southeastern and midwestern states and consequently, impacted the production and supply of hydroelectricity.5 Hydroelectric power generation, which normally accounts for 60–70% of the country’s electricity needs, fell by 35% from the previous year.6 A cold and long winter in the Northern Hemisphere, meanwhile, has contributed to a surge in global prices of energy for household use, thereby pushing up prices in Brazil as well.7 Finally, the pandemic itself has brought about a profound change in the consumer basket, with rising demand for goods and supply constraints—part of it global—adding to goods inflation. For example, prices of housing goods have been rising by more than 12% every month since May this year.

The central bank is aware of the damage high inflation can inflict on the economy. First, high inflation eats into real income gains, thereby weighing on private consumption. That’s what happened in the middle of the last decade.8 This time around, it is even more worrying, given the deep shock to the economy and labor markets due to the pandemic.

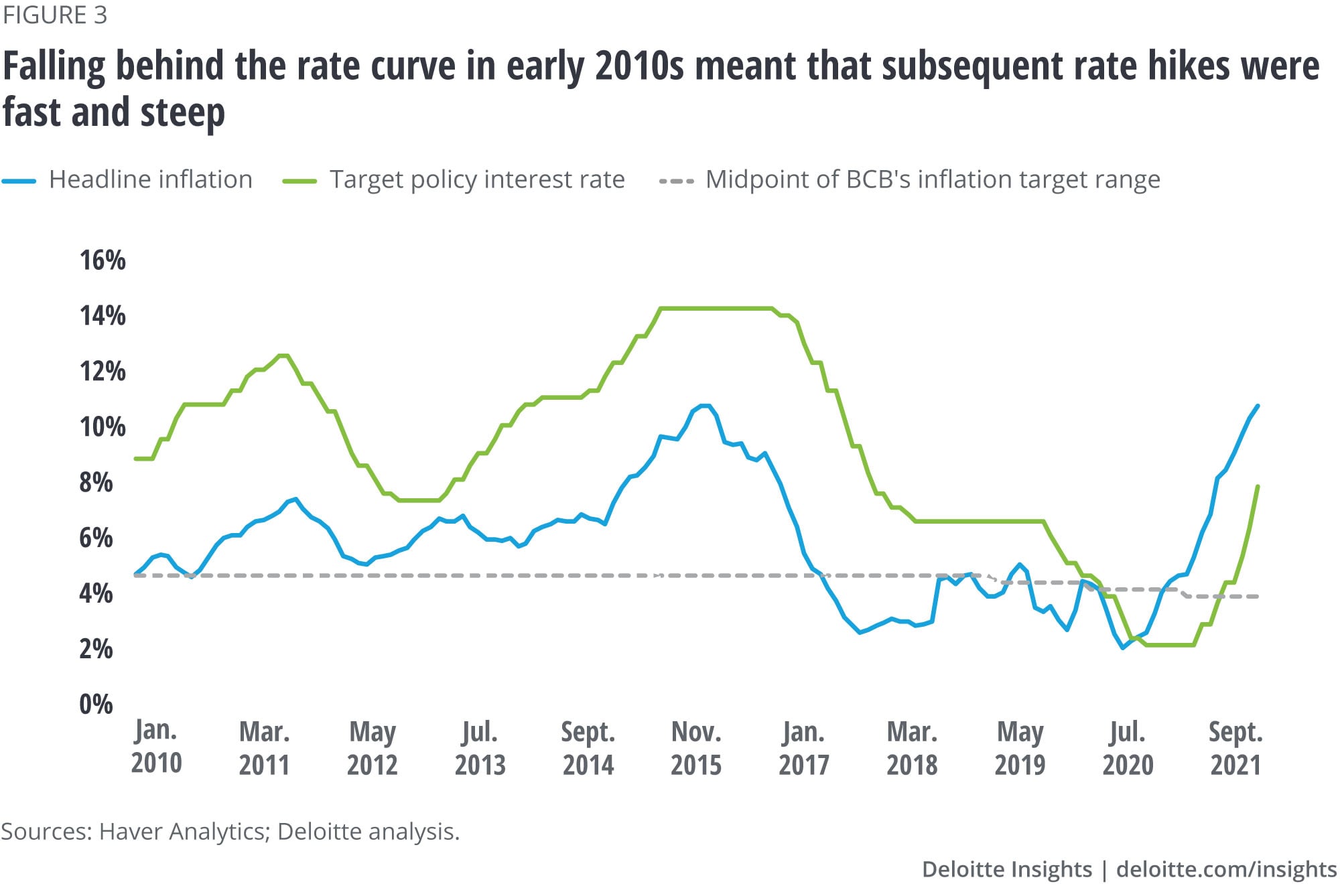

Second, the central bank will be wary of any potential loss of credibility if it leaves inflation unchecked for long. Again, it will remember the lessons of the last decade.9 Between 2008 and 2016, when the economy suffered long bouts of high inflation—headline figures were above the midpoint of the BCB’s target range for most of this period (figure 3)—the BCB likely fell behind the rate curve initially, thereby undermining financial market confidence in its ability to keep inflation in check and inflation expectations anchored.

Finally, falling behind the rate curve in the early part of the last decade meant that the central bank had to tighten monetary policy fast. And subsequent rate hikes were also steep. Between April 2013 and April 2014, the BCB hiked its key policy rate by 375 basis points, and then followed suit with another 325 basis points’ worth of hikes between October 2014 and July 2015. So, over the course of a little more than a year, borrowing costs went up sharply, thereby leading to surging debt-repayment costs for households and businesses, not to mention the government.10

To its credit, the BCB has acted swiftly this year to counter inflationary pressures. After easing monetary policy over 2020 to enable an economic recovery amid the pandemic, it hiked its policy rate by 75 basis points in March—the first hike in policy rates since July 2015. The central bank then followed with another 500 basis points of hikes by October. While it’s still early days to understand the impact of these rate hikes on inflation and the dynamics of domestic and global inflation, the BCB’s swift moves are in sync with its objective of keeping inflation in check. And the BCB will likely wait to see how the rate hikes so far impact inflation and inflation expectations before deciding its next course of action.

The uptick in inflation comes at a worrying time for policymakers in Brazil as they turn their eye toward near-term economic risks in addition to COVID-19. One such risk comprises potential capital outflows due to any monetary tightening by the United States Federal Reserve.11 Back in 2013, when the Fed was thinking of normalizing monetary policy after a strong run of asset purchases, global investors reacted by pulling money out of emerging markets and putting it into assets such as US Treasuries. This “taper tantrum,” as it was labeled back then, led to currency volatility in emerging markets, including Brazil. While the Fed has kept rates unchanged for now, it has cut down its monthly asset purchases by US$15 billion.12 And with inflation heading up in the United States, the Fed will likely be tracking data on prices closely to make adequate changes in policy should inflation show any signs of getting entrenched. Any sharp tightening may serve as a trigger for some portfolio outflows from Brazil and other emerging markets.

How is Brazil placed today to deal with capital outflows? And, is it better off today than it was in 2013? In the 10 months until October this year, Brazil witnessed portfolio outflows to the tune of about US$4.3 billion, much lower than the US$32.7 billion worth of outflows during the same period in 2013, which includes a period of the “taper tantrum” that year. So, portfolio outflows so far this year haven’t happened at the scale witnessed during 2013, despite the Fed taking the first steps in toning down the scale of its asset purchase program in November. Things may change, however, if the Fed takes a more aggressive stance in the coming months. Nevertheless, Brazil’s economy has three things going in its favor this time around.

First, the country’s external balances are more favorable now than in 2013. For example, according to the International Monetary Fund, the annual current account deficit is expected to be about 0.5% of GDP in 2021, much better than the 3.2% deficit in 2013.13 Second, currency weakness is lower now compared to eight years back. Between January and October this year, the real fell by 3.1% against the US dollar; the decline was much higher (10.8%) during the same period in 2013. Finally, compared to 2013—when the inability to counter inflation drew skepticism for monetary policy—the BCB has likely learned its lesson, given its proactiveness in hiking rates this year to counter rising inflation. Thankfully, the central bank also has a sizeable arsenal of foreign reserves to deploy, to support the real in the event of any potential rise in portfolio outflows this year, and the next arising out of any monetary tightening by the Fed. Foreign reserves have been rising since April 2020 and amounted to US$368 billion in November of this year.

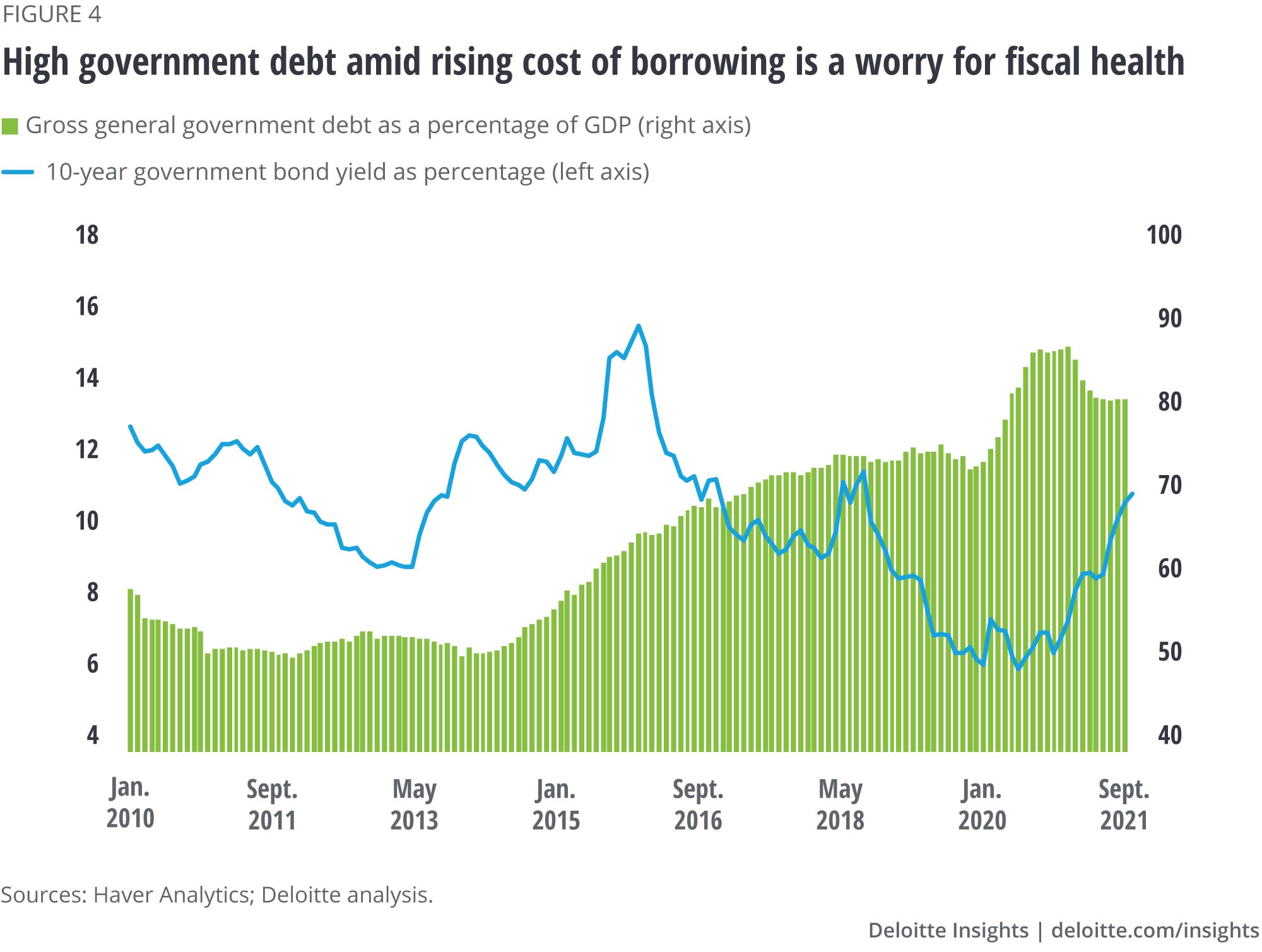

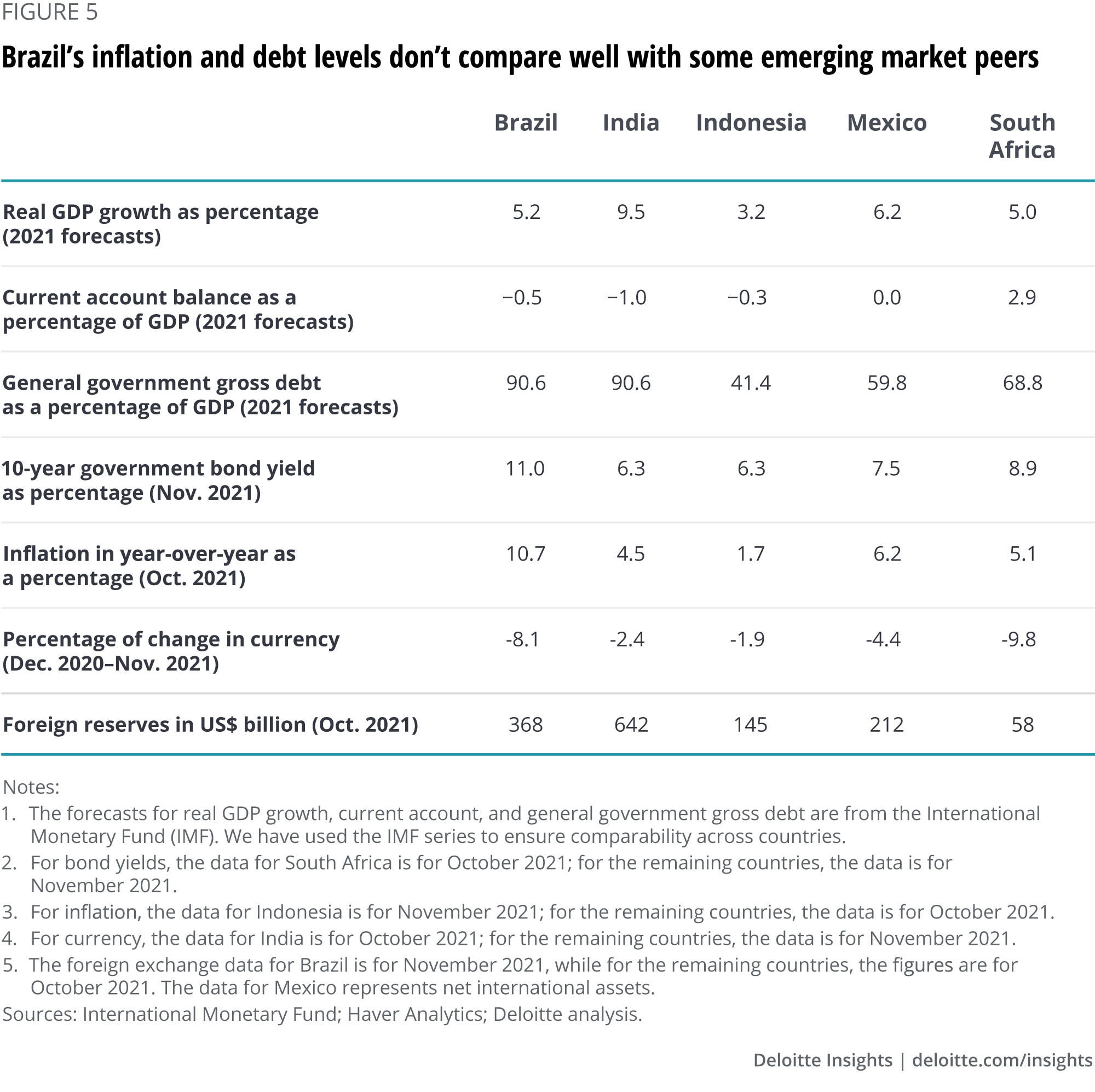

A major worry for Brazil, however, is its fiscal situation. Debt levels in Brazil have shot up since the last decade (figure 4), with gross general government debt averaging a little less than 80% of GDP this year. In 2013, at the time of the first “taper tantrum,” the debt-to-GDP ratio was much lower at 51%. Similarly, the fiscal deficit now is higher than what it was eight years back. While a surge in borrowing to finance spending during the pandemic has pushed debt and deficit higher—and is expected of governments during times of crisis—failure to move back to a path of fiscal prudence and reforms is what investors may frown upon. This is even more relevant in the current high-inflation, negative-growth scenario in which interest rates and, therefore, cost of borrowing, have shot up this year. And Brazil’s fiscal and inflation scenario isn’t favorable compared to some other emerging economies, thereby putting it at a likely disadvantage should global investors start rethinking their portfolio allocations across countries (figure 5).

No wonder then that financial markets reacted negatively to the news of US$5.3 billion worth of welfare spending exemptions from Brazil’s fiscal ceiling.14 Further deterioration in the fiscal math will likely push bond yields up further. Since the end of 2020, 10-year government bond yields have gone up by about 460 basis points,15 and deterioration in investor sentiment due to worries about fiscal prudence will likely drive bond yields up further. The result is expected to be higher debt-servicing costs for the government and worsening finances, a cycle (figure 4) that nearly put an end to Brazil’s economic ambitions in the last decade. It is a burden that policymakers and Brazil’s citizens can do without, especially in the time of a pandemic.