Latin America economic outlook, January 2023 has been saved

Cover image by: Jaime Austin

Mexico

Colombia

Mexico

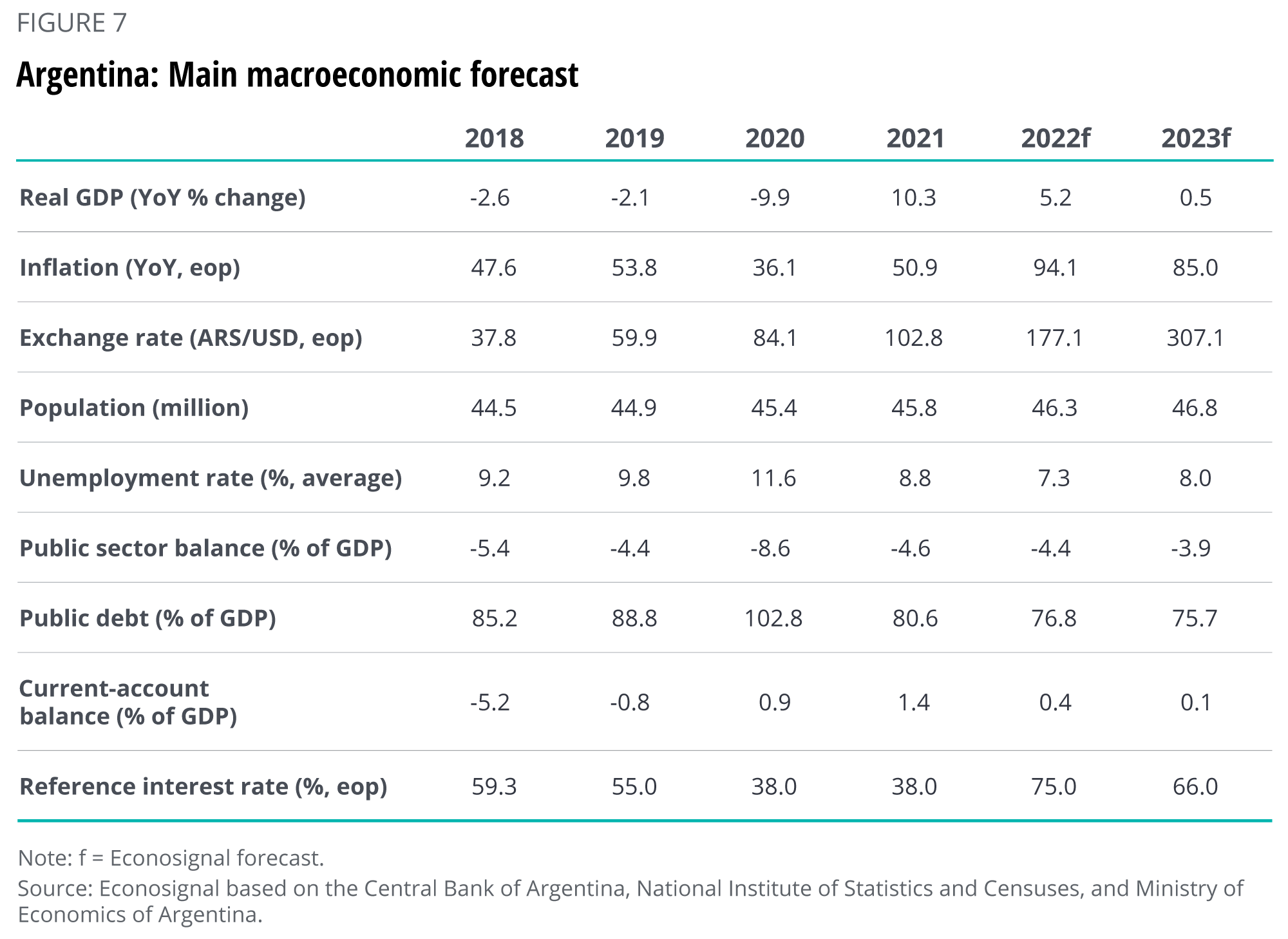

Argentina

The far-reaching impacts of the ongoing war in Ukraine, such as persistently high energy and food costs, have further weakened a global economy already reeling under the lingering economic challenges of the COVID-19 pandemic. Most economic forecasts in recent months have reflected this sentiment. The International Monetary Fund, for example, recently downgraded its global growth forecast for 2023 to 2.7%—0.9 percentage points lower than its April 2022 estimate. This bleak panorama also involves negative economic perspectives for the United States (1.0%, down from 2.3% in April) and China (from 5.1% to 4.4%)—two of the world’s largest economies.1

Such weakening economic activity is bound to dampen growth prospects in Latin America (Latam). Consequently, we at Econosignal (the economics unit at Deloitte Spanish-Latin America) have revised our forecast for the region’s growth in 2023 from 2.0% to 1.7%.2

Moreover, aggressive monetary tightening in advanced economies to rein in inflation could spell trouble for Latam, mainly through the effects of higher borrowing costs and a more expensive US dollar. The latter could in fact worsen the region’s inflation woes.

In this article, we take a closer look at these issues and try to answer two questions: Is Latam heading toward a recession? And how likely is Latam to face a debt crisis? We will also discuss the potential growth opportunities on the horizon for Latam economies that could help the region withstand a global economic downturn. Our forecasts for individual Latam countries can be found in the appendix.

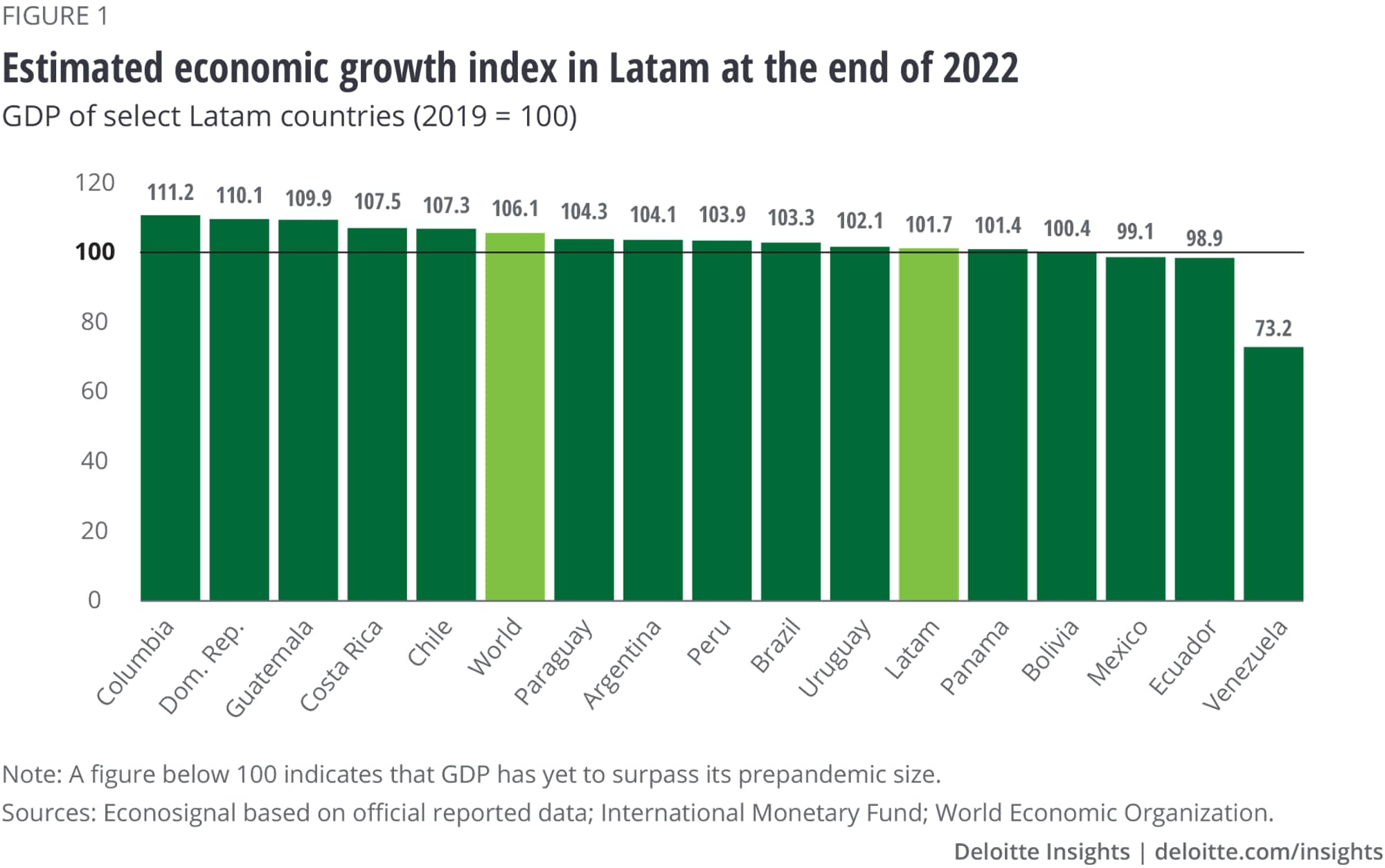

In 2021, Latam rebounded from a pandemic-induced economic contraction. The region benefited from a surge in commodity prices driven by strong demand when the global economy reopened. The result: The region grew by 6.8% in 2021,3 with GDP of half of its countries surpassing prepandemic levels. Then, in 2022, the war in Ukraine broke out, which has decelerated this recovery. However, we still forecast an economic expansion of 3.4% for Latam in 2022.4 Highlights of this overall recovery include countries such as Chile, Colombia, Costa Rica, and the Dominican Republic, which witnessed better postpandemic recovery than the rest of the world. Conversely, economic growth in the three largest Latam economies—Argentina, Brazil, and Mexico—lag the rest of the globe. Furthermore, GDP growth for Mexico, Ecuador, and Venezuela, from 2019 to the end of 2022, is not likely to be sufficient to bring those economies back to their prepandemic levels (figure 1).

Prospects for 2023 are less rosy than those for 2022, as several headwinds cloud the regional outlook. There is an increasing belief that a recession (or a larger slowdown) is set to hit the US economy within the next 12 months: A survey by Bloomberg in October pins the odds of a downturn in the United States at 60%.5 This has tapered global demand, which in turn has depressed the prices of oil and other commodities (figure 2). For example, compared to 2022 peaks, oil is down 27%, copper 24%, zinc 28%, nickel 33%, silver 25%, gold 14%, wheat 29%, soybeans 10%, and maize 10%.6 The conspicuous exception is gas, whose price has soared since the start of the war in Ukraine—up 79% in the US market and 109% in Europe.7

A drop in commodity prices is usually a harbinger of economic hardship in Latam because commodities are the region’s main exports and constitute a crucial source for incoming international reserves and government revenue.

Nevertheless, are these factors enough to lead to a recession in Latam? Not necessarily. In fact, Chile is the only Latam country where a slight contraction of GDP is forecasted.

Although the expected decline in prices may spell the end of the commodity-led boom in Latam, it could also help moderate inflation. The war in Ukraine, by creating a shortage of key agricultural inputs, has triggered food inflation the world over, while the economic reopening after the COVID-19 crisis signaled the beginning of strains in global production networks, manifested by delivery delays and expensive maritime transport costs. As a result, several Latam countries are now experiencing inflation rates not seen in decades (figure 3).

However, these challenges have somewhat subsided in recent months: Commodity prices, as discussed above, have come down substantially. Supply chain disruptions, too, are easing, as various economic indicators show. For example, the global supply chain pressure index—a metric that estimates how backed up supply chains are worldwide—decreased in September 2022 for the fifth straight month and reached its lowest value in 22 months. This is largely due to a drop in Chinese supply delivery times.8

Despite these recent trends, price pressures are proving quite stubborn, and inflation has remained high worldwide. It is estimated to have peaked in late 2022 but will remain elevated for longer than previously anticipated.9

This is, for example, the case for the United States, where inflation is easing more slowly than expected. It has shed 1.96 percentage points since its peak in June, and currently the annual inflation rate stands at 7.1%. The Federal Reserve increased its funds rate several times in 2022, and Fed Chair Jerome Powell recently stated that the Fed will keep raising interest rates until inflation is under control. Powell indicated that the Fed may have to raise interest rates as high as 4.6%—or maybe even higher—in 2023 to beat inflation. This announcement and the rate gap between the US dollar and other currencies increased the value of the US dollar. The DXY index—a benchmark to measure the gap between the US dollar and other advanced-economy currencies—reached a two-decade high of 114.10 in September 2022. It has receded since mid-November but has remained high, currently standing at 103.4.

Central banks of most advanced economies, such as the Fed and the European Central Bank, are currently going through a monetary-tightening cycle. The rate hikes make US and European assets more attractive to investors and, consequently, have apparently led to capitals outflows from emerging market economies. Data from the Institute of International Finance (IIF) partially supports that argument. It shows that, as of September 2022, Latam had already witnessed two months of negative capital flows, compared to one month last year.

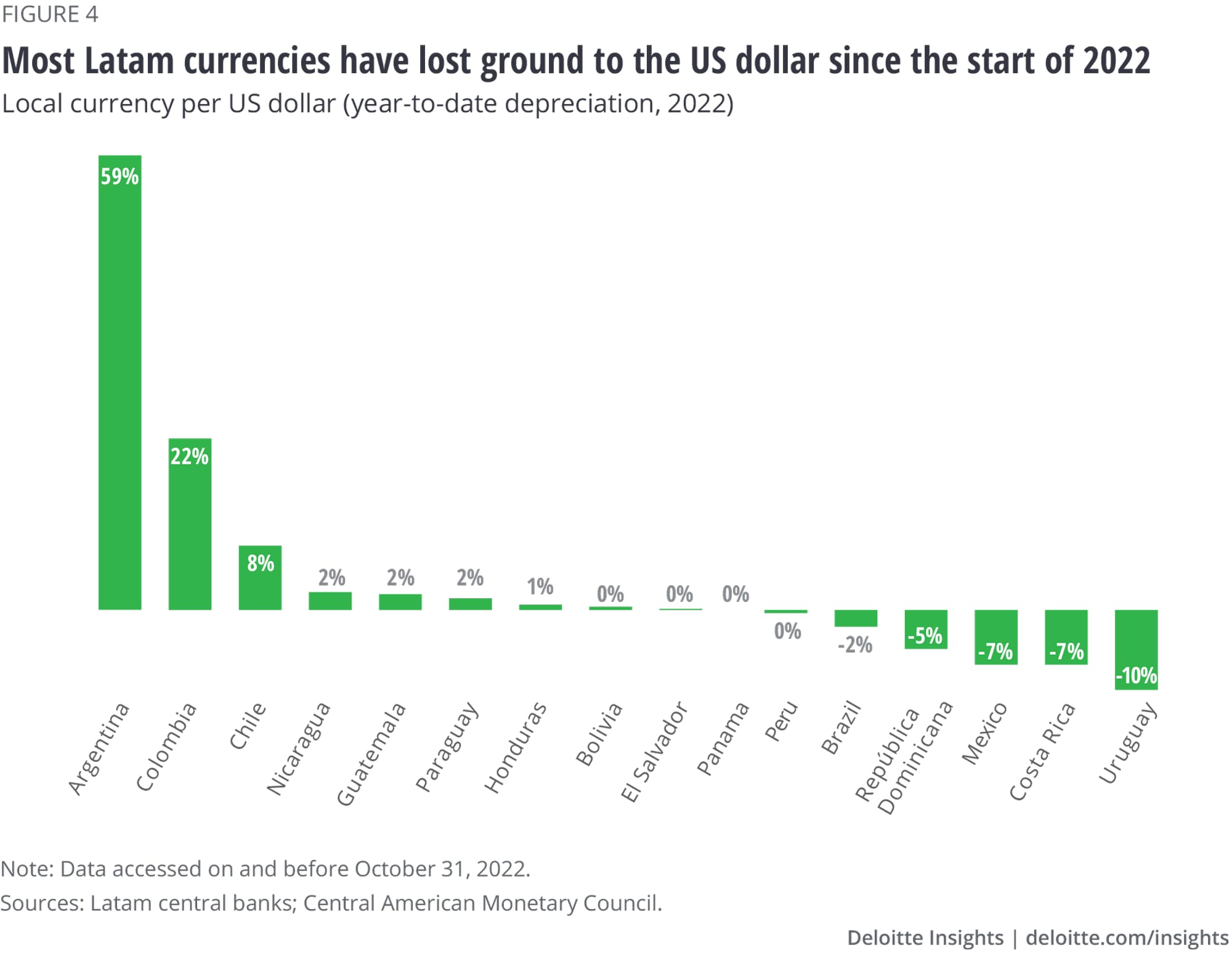

In addition, the Economic Commission for Latin America and the Caribbean (ECLAC) concurs that capital inflows to Latam have declined in 2022.10 It reported that in the first quarter of 2022, the four-quarter moving average of total capital inflows was down 13% year over year (YoY) from 2021. This was driven by a decline in portfolio investment, particularly bond-related flows. The ECLAC also reports that during the first four months of 2022, sovereign debt issuances declined 42% YoY from 2021. This has led to a shortage of US dollars in some economies, as central banks use international reserves to defend their currencies against the surging dollar. This forces down local currencies and most have lost ground to the US dollar since the start of 2022. Colombia and Chile are noteworthy examples as their currencies have contracted 22% and 8%, respectively, by November 2022. Only a handful of currencies appreciated in 2022, such as those of the Dominican Republic, Costa Rica, Uruguay, Mexico, and Brazil.

A strong US dollar is a concern for Latam for several reasons: It drives up inflation due to more expensive imports, makes borrowing more onerous, and increases the cost of servicing dollar-denominated debt.

The combination of a tight monetary policy in the United States and a strong dollar has sparked comparisons to the early 1980s. Back then, Fed Chair Paul Volker pursued an aggressively restrictive monetary policy—through rate hikes—to contain mounting inflation in the United States, which, afterwards, fell from 11% in early 1980 to 4% by the end of 1983. It, however, came at the cost of two recessions—a short one in early 1980s and a deeper and more far-reaching one over 1981–1982.11

This had profound consequences for the nations of a heavily indebted Latam. The region had seen a period of considerable borrowing in the 1970s, because of low interest rates and liquidity excesses worldwide. According to the World Bank, the external-debt-to-GDP ratio increased from 22.6% in 1975 to 42.9% in 1982. Then, in the aftermath of the 1981–1982 recession, economic growth rates of indebted Latam countries slowed down and international interest rates rose, as a result of Volcker’s policy. Interest payments on external debt rose from 15% of exports in 1975 to 33% in 1982 for Latam. What became known as the debt crisis was triggered in 1982, after Mexico announced it could no longer service its debt and several sovereign defaults ensued. All in all, 16 Latin American countries had to restructure their debts, including the four largest debtors, Mexico, Brazil, Venezuela, and Argentina. Consequently, loans to the region decreased by more than 20%, and sharp devaluations followed.12

Fast forward to the present: Latam’s debt has risen over the past decade as global interest rates have dropped since the 2008 financial crisis. The government-debt-to-GDP ratio increased from 47% in 2012 to 69% in 2021, peaking at 74% in 2020.13 However, Latam’s policy framework is different this time around, thanks to the changes that the 1980s crisis brought about, especially for the independence of central banks.

The 1990s saw a wave of reforms that modernized central banks. Most notably, most Latam countries passed laws aimed at reducing central banks’ financing to governments and adopted new policy regimes, such as inflation targeting. In general, the results proved satisfactory as countries achieved price stability, and inflation rates converged to a single digit within a decade.

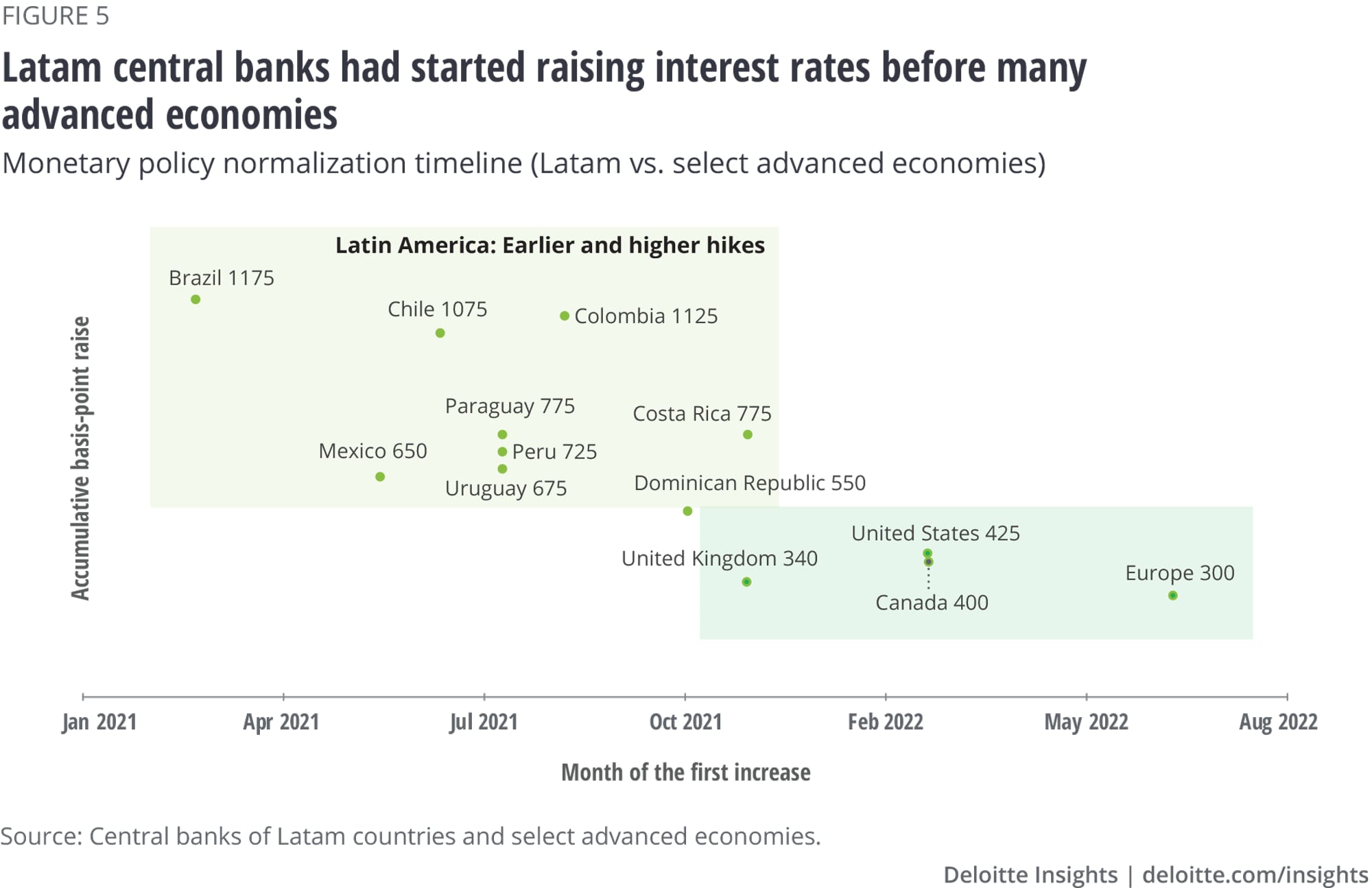

Another key difference has to do with the return to monetary policy normalization, a return to precrisis levels of interest rates.14 Like in many other countries and regions of the world, all Latam central banks were compelled to implement interest-rate hikes to defend local currencies against a surging US dollar. The higher rate not only avoids the outflow of capital, because local assets are more profitable, but also helps to ease inflation. The timing of these hikes has also been crucial: Latam central banks started raising rates much before advanced economies (figure 5). With this move, Latam central banks signaled that fighting inflation is a key priority, anchored expectations, and saved valuable international reserves.

However, that does not mean that there are no concerning signs. First, higher interest rates will dent economic growth. It remains to be seen what path rate hikes take after the Fed announces its policy decisions in its future meetings. Second, international finance markets are becoming skittish toward Latam. The emerging markets bond index (EMBI), a benchmark for emerging market sovereign bonds, has risen 6% for Latam since November 2021, reflecting that borrowing in dollars has become more expensive, especially in Venezuela, Argentina, El Salvador, and Ecuador. Moreover, countries such as Colombia have seen an increase in their risk premiums and refrained from issuing bonds in 2022.

This leads to a third concern—the need to adjust fiscal balances. As of 2021, all countries in Latam exhibited a negative fiscal balance, averaging –4.44% and ranging from –1.48% in Ecuador to –9.26% in Bolivia. A tighter fiscal policy may prove to be a daunting task for policymakers. During the pandemic, governments substantially increased their spending to support affected households and businesses. In some countries, financing this additional spending ate away some of their fiscal space—as is the case for Costa Rica. According to the World Bank, current debt repayments are mainly concentrated in 2023 and will surge to 2.1% of GDP.15 Moreover, some governments are subsidizing consumer spending in this current inflationary stage. Eliminating those subsidies could be unpopular and may even spark social unrest.

Not everything, however, is gloomy. Disruptions caused by the pandemic and the war in Europe have also given rise to some growth opportunities for Latam.

The strain on global production chains over the pandemic exposed the risks of the offshoring strategy. The prime example of such risks is the delays and suspension of exports after China implemented stringent lockdowns in January 2020. Since then, companies have internalized these risks and adjusted accordingly, for example, by moving their global value chains closer to end markets—in other words, by adopting the “nearshoring” strategy. The result is a reshaping of global economic activity around three regional production hubs: North America, Europe, and East and Southeast Asia.

Geographical proximity to any of the three hubs is of prime importance in nearshoring. Naturally, among Latam countries, Mexico stands to gain the most from this new development, because of its vicinity to the United States. In fact, it has already started to reap the benefits, reflected in high foreign direct investment (FDI) inflows into Mexican states bordering the United States. While Mexico as a whole reported a 4% decrease in FDI in 2021 against the average from 2015 to 2019, its northern states of Baja California, Chihuahua, and Nuevo León recorded increases of 54%, 6%, and 4%, respectively.16 The Inter-American Development Bank estimates that nearshoring could add US$78 billion to Latam’s exports every year, from which US$35 billion would go to Mexico and US$7.8 billion to Brazil. Industries such as automobile, textiles, pharmaceuticals, and renewable energy could benefit the most.17

Digital nomads are remote (and mostly self-employed) workers whose flexibility allows them to work from different cities and countries. They work on their laptops or phones and use wireless networks in places such as coffee shops, libraries, or coworking spaces. Such a lifestyle was already trending before the pandemic, but it has exploded since then. There are an estimated 35 million digital nomads worldwide, and half of them come from the United States alone, where their numbers doubled from 7.3 million in 2019 to 15.5 million 2021. They are seen as a potential source of additional income to the economy because they stay longer and spend more money than regular tourists. Ever since the number of international tourists dropped because of pandemic-related restrictions, countries have been actively targeting digital nomads. There were 21 countries with digital nomad visa programs in February 2021—the number is now 49. Argentina is the latest country in the Latam region to introduce such visa programs, joining six other nations—Costa Rica, Mexico, Panama, Brazil, Ecuador, and Colombia. The migration office in Argentina estimates that a digital nomad spends US$3,000 per month—twice as much as the average tourist.18

Latam offers several advantages to digital nomads, such as proximity to the United States, low cost of living, and warmer weather during winters in the northern hemisphere. Four Latin American countries, according to website Two Tickets Anywhere, feature in the list of top 10 destinations for digital nomads in the world: Mexico (no. 1), Colombia (no. 4), Costa Rica (no. 8), and Brazil (no. 9). As for cities, Mexico City (no. 3), Medellin (no. 5), and Buenos Aires (no. 9) are among the top ten destinations. There is room for expansion in the other countries that are yet to implement digital nomad visa programs, but international competition is steep. Countries such as Thailand or Malaysia offer tropical weather with substantially faster mobile internet. For example, Thailand’s mobile internet speed of 67.35 Mbps is almost the double than Mexico, at 34.63 Mbps.19

The wave of sanctions on Russia’s products in the wake of its invasion of Ukraine has opened the door for several Latam countries to step in and supply select commodities to international markets. For example, in the fossil fuels market, Russia has been the main supplier of petroleum oil and natural gas to the European Union. The latter is now preparing to stop importing Russian gas from 2027 on. This development would open up opportunities, for example, for Argentinian gas, among others.

Vaca Muerta, located in the Patagonia region of Argentina, is the world’s second-largest shale gas reserve and fourth largest in terms of shale oil. Even in a conservative scenario, this reserve alone could position Argentina among the top 20 oil-exporting countries within the next 10 years, may reduce natural gas imports by 60% in the next two years, and would help the country achieve self-reliance in gas in the next 10 years. To realize this potential, Argentina needs more infrastructure spending to move its natural gas reserves to cities and ports. This is a major challenge since the country has a very unstable macroeconomic environment. However, after various roadblocks—some political in nature—and several years, the much-needed gas pipeline “Nestor Kirchner” will be completed in mid-2023. It is expected to save LNG imports close to US$3,000 million, which would significantly alleviate the country’s balance of payments.

Because of the geopolitical divisions created by the war in Ukraine, the increase in demand for gas from Southeast Asia, and the global transition to cleaner energies, LNG consumption and imports will keep increasing in the near term, which is an opportunity for Argentina to become an important supplier. If a specific regulatory framework is developed in the sector, to protect investors from changes in local legislation and ensure the availability of their dividends, it could raise investments to generate up to US$27 billion in export revenues starting 2027–29 (30% of projected exports for 2022). Considering the estimated resources of Vaca Muerta, the uninterrupted supply of unconventional oil and gas in Argentina would be greatly benefitted for a long time to come. The rate of fossil fuel extraction, both gas and oil, from the Neuquén basin (where Vaca Muerta is located) has been growing. In 2022, the cumulative volume of oil exports grew by 178% annually compared to the previous period.

Lithium-ion batteries are a key part of the world’s clean-energy transition, particularly in the electric car and consumer product industries. An estimated 106,000 metric tons of lithium was mined in 2021 alone—an all-time high and a 258% increase from 2015.20 And almost half of the world’s lithium comes from a region in the Andes Mountains known as the “Lithium Triangle,” jointly governed by Argentina, Bolivia, and Chile.

Global lithium production is expected to grow up to 420,000 tons by 2031. With an increase of 250%, Australia, with an output of 141,000 tons in 2031, will remain the largest lithium-producing country in the world. Chile and China will more than double their outputs, and Argentina’s production will rise nine-fold to 57,000 tons, making it the second-largest global producer between 2027 and 2028. If these projections materialize for Argentina, the credit will go to increased foreign investment in the sector and better economic policies compared to its neighboring countries.

In addition, Argentina could become the world’s leading exporter as it has 13 projects in its pipeline in different salt-flat brine basins with proven lithium content, more than any other country in the world. The focus behind these projects is potential high-grade, large-scale lithium extraction with favorable access and infrastructure. Looking to encourage investment, the Argentinian government lowered export taxes for the mining sector. In the coming years, this industry is expected to generate US$4 billion in exports annually (4.5% of 2022 exports).

What about the other two countries of the Lithium Triangle? Production in Bolivia is not expected to skyrocket despite being the country with the world’s largest resources of the metal.21 In Bolivia, state control over lithium has long been prioritized, and recently, contracts with foreign companies were canceled due to protests in Potosí demanding higher royalties for the country. According to the vice minister of Altas Teconología Energéticas de Bolivia, the country extracted only 0.2 tons of lithium (compared to 6,000 tons by Argentina or 26,000 by Chile in 2021). Chile is currently the world’s second-largest producer of lithium. However, considering the many challenges the country’s mining sector faces, such as increased regulation and protests by environmental and indigenous groups, lithium production is expected to grow at a slower pace in the coming years. Moreover, business confidence is low and many companies, including major Chilean producers, are seeking tax incentives and a friendlier regulatory framework outside the country, especially in Argentina.

Latam continues to be affected by the seemingly unending wave of global economic setbacks, such as logistical difficulties caused by the pandemic, inflation resulting from the war in Ukraine, and capital outflows due to the global monetary tightening. As such, 2022 was a year of decelerating growth for Latam, with the prospects for 2023 being even more moderate. Inflation, although showing signs of improvement in recent times, is expected to remain above central banks’ targets. Much will now depend on what the Fed decides next, because that’s what will determine the path of the current global monetary tightening.

In the short term, the main challenge for Latam countries is coordinating public policies to ensure inflation subsides. Central banks have already done their part, but the external lag of monetary policy means that price increases will remain above the inflation targets, even though most countries may have already experienced their inflation peaks. Going forward, policymakers should continue policy tightening until inflation is brought under control. Governments, meanwhile, will benefit from fiscal discipline, to keep inflation expectations down and to keep debt ratios under check. At the same time, it is crucial to avoid an extreme contraction of monetary and fiscal policies to prevent Latam from entering a deep economic slowdown.

Nonetheless, there are glimmers of hope in the form of unexpected opportunities. A reconfiguration of the global economy could: first, help Latam increase its manufacturing exports to the United States; second, generate additional sources of revenue by attracting digital nomads (although not as sizable as the first one); and third, increase oil and gas exports to the world, as well as inputs associated with the world’s transition to clean energy (such as lithium).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}