{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Latin America economic outlook, June 2022 has been saved

Cover image by: Jaime Austin

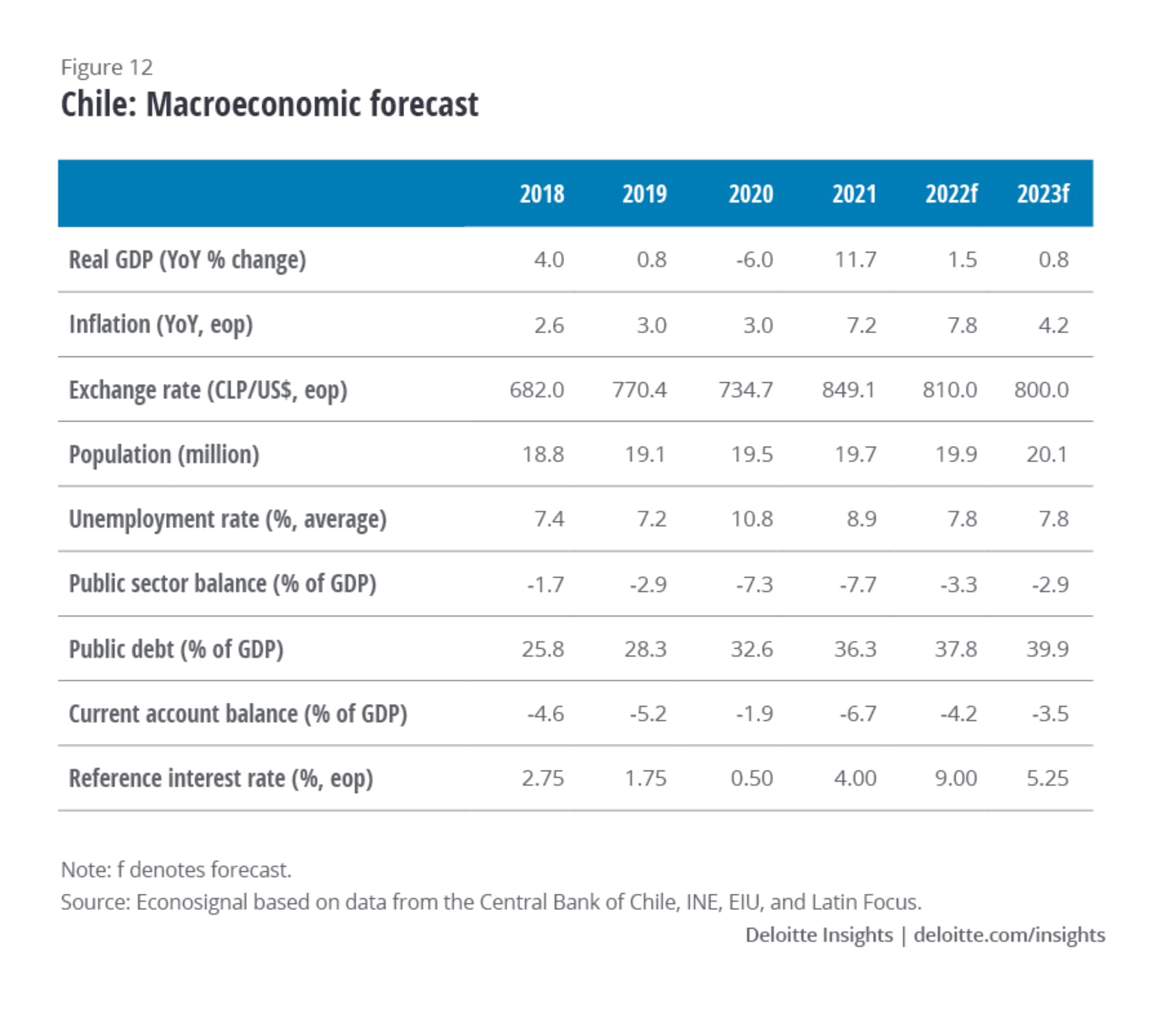

Mexico

Colombia

Mexico

Mexico

In 2021, Latin America (Latam) rebounded from the pandemic-induced economic contraction of the last two years. Growth prospects, however, remain moderate this year, because of a less favorable base effect and a series of domestic and international challenges.

Inflation is showing no signs of abating, which runs contrary to what we expected at the end of 2021. The lingering disruptions caused by strained supply chains globally are now compounded by the aftermath of Russia’s invasion of Ukraine. The most visible fallout of this situation has been a spike in commodity prices, which has heterogeneously affected trade balances and fiscal accounts within the region. However, in terms of GDP growth, most Latam countries have been barely affected.

High commodity prices have also forced the region’s central banks to accelerate the upward trend of interest rate hikes—this is true not only for Latam and other emerging regions but also for the developed countries such as the United States and the United Kingdom. This policy response to high prices will make financing more expensive and economic growth slower.

Nonetheless, the prevailing economic environment, shaped largely by high commodity prices, presents an opportunity for many Latam countries, especially for major exporters of commodities, to invest the additional incoming dollars in productivity-increasing capabilities and, in the process, lay the groundwork for long-term economic development.

The first half of this report, building on the aforementioned topics, presents an overall analysis of the current economic situation in Latam. In the second half, we present a brief overview for each economy of the region.

Russia’s invasion of Ukraine—by contributing significantly to the sharp rise in energy and commodity prices globally—has impacted the economic performance of nearly all countries in Latam, albeit to a lesser degree compared to many other regions of the world.

Even though the price rise is boosting the region’s exports, it also poses several critical challenges. For instance, the region faces a deficit in gasoline global trade, which in some cases offsets the positive effect generated by increased revenue from exports. In addition, the rise in food and energy prices, by impacting consumption and production costs, has accentuated inflationary pressures.

This has, in turn, forced the region’s central banks to accelerate interest rate hikes, jeopardizing growth and making private and public financing more expensive. This situation may prove to be risky for the macroeconomic stability of the region, considering the debt-to-GDP ratio in Latam has reached its highest level since the early 1990s, as many countries were forced to implement a substantial and necessary fiscal expansion during the pandemic.

The current scenario in Latam countries, therefore, resumes the debate about the region’s high dependence on commodities.1 The debate focuses on how public policy can address the long-term adverse effects of such dependency, and how to profit from periods of high commodity prices.

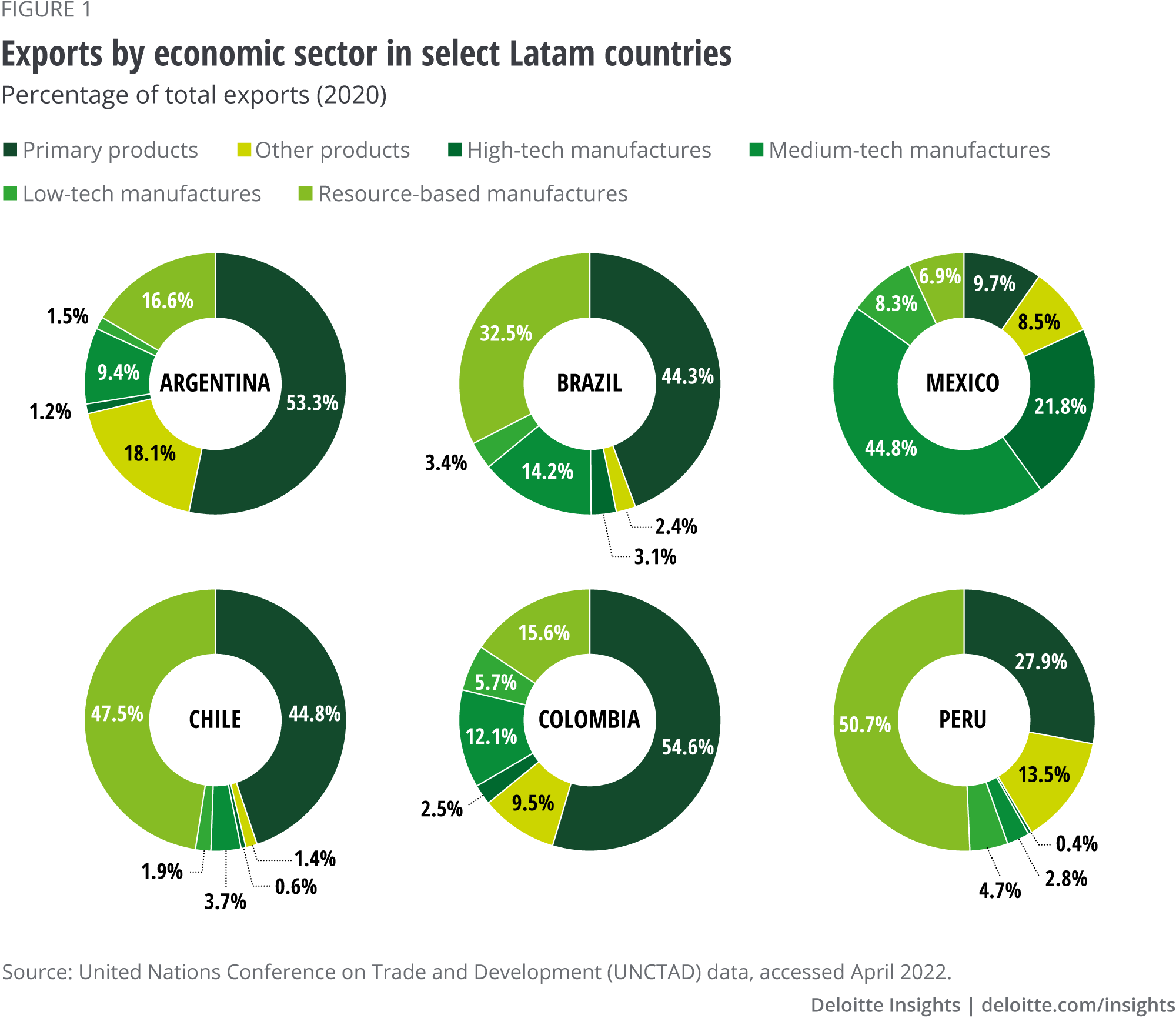

Revenues from Latam exports have historically depended on commodities. In 1995, the exports of primary products represented 32% of overall exports. In 2020, this figure had come down to only 29%.2 Moreover, most Latam countries’ export baskets lack high added value products. This partly explains why economic growth for Latam lags behind other regions such as Asia.3

At present, approximately half of the exports of Brazil, Argentina, and Colombia are classified as primary products. In the case of Chile and Peru, their main exports are copper ore and refined coppers, which are classified as primary products and resource-based manufactures, respectively. The big exception in the region is Mexico, where two-third exports, mainly destined for the US market, are high- and medium-tech manufacturing products (figure 1).

Export commodity dependence, referred to in the economic literature as the “The Natural Resource Curse,”4 is a source of economic vulnerability for the Latam region. Reasons include: (1) extreme weather events affecting crop yields; (2) exploitation of minerals depending on the maturation of mines; (3) reliance of oil production on the discovery of new deposits and on shifts in geopolitical realities; (4) fluctuating commodity prices in international markets affecting macroeconomic stability; and (5) increases in government spending discouraging private investment (the so-called crowding-out effect).5

Furthermore, the primary sector does not create as much employment as manufacturing does, hence exacerbating the overall unemployment woes for the region.6 Finally, the revenues from exports of volatile commodities—such as sugar, coffee, soy, and oil—are big contributors to tax revenues, thus posing a continued risk to fiscal and economic stability.

These issues do not necessarily suggest that Latam should turn its back on natural resources. On the contrary, the region should take advantage of the revenue derived from natural resources to invest in productivity-boosting capabilities, which in turn can help the region achieve the goal of long-term economic development.

Currently, because of the ongoing conflict in Ukraine, the region once again is experiencing a commodities boom. This situation comes with its benefits as well as challenges. In the following sections, we will take a closer look at them.

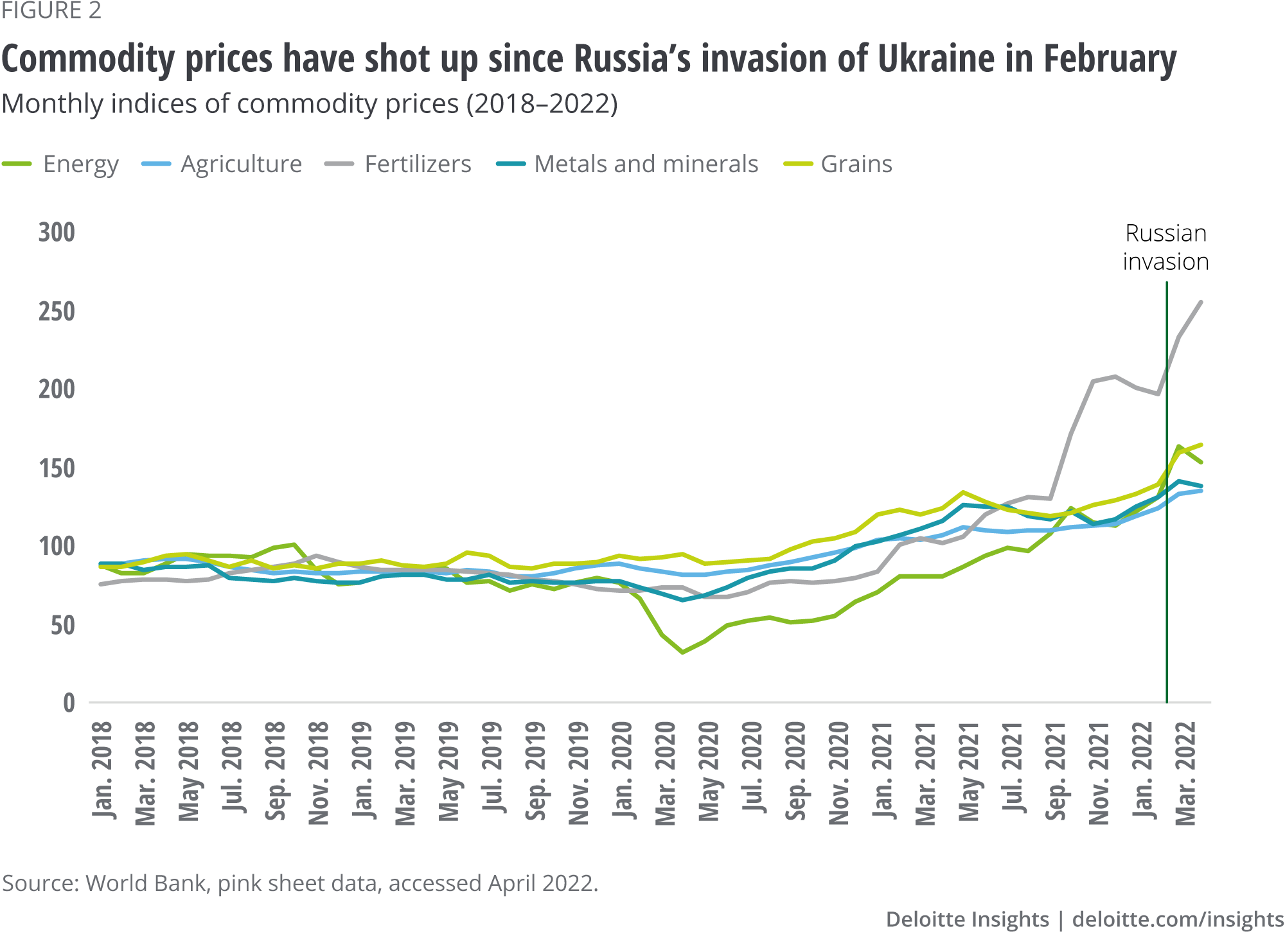

Ever since Russia invaded Ukraine in February, economic growth predictions have turned more pessimistic for 2022. The International Monetary Fund (IMF) lowered the 2022 growth forecast for the global economy from 4.4% in January to 3.6% in April.7 This downgrade was a response to the fallouts of the war—economic sanctions on Russia by Western powers, uncertain geopolitical realities, surge in key input prices, and accelerating interest rates.

The economies of Russia and Ukraine are crucial suppliers of raw materials for many countries and regions around the globe—ranging from energy products and metals used in technology industries to basic agricultural commodities. As a result, the prices of several commodities have soared since February, reaching multi-year highs or even record levels in some cases (figure 2).

The EU has emerged as the most affected region, due to its heavy dependence on Russia to meet its energy needs (24.7% of its oil and 46.8% of its natural gas).8 The EU also depends on Russia for its supply of metals such as aluminum, gold, and platinum. Moreover, Russia and Ukraine are major exporters of grains and fertilizers, as a result of which the prices of agricultural commodities such as wheat, corn, and seed oils have shot up.9

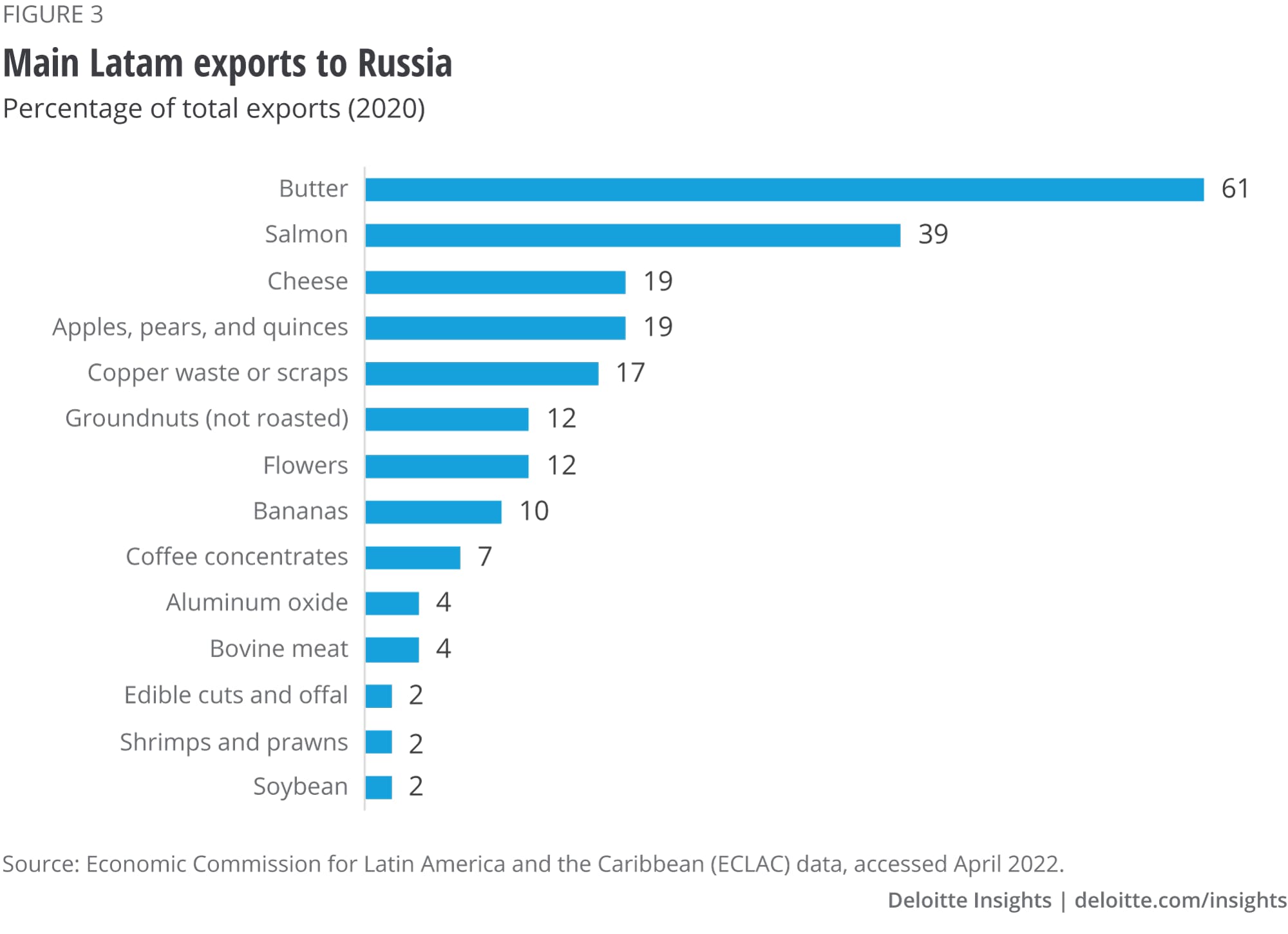

Latin American trade, on the other hand, has not been severely affected by the conflict, because Ukraine, Russia, and Belarus receive merely 0.6% of the region’s exports.10 Affected products include butter, salmon, cheese, apples, pears, and quinces11 (figure 3). Paraguay, Jamaica, and Ecuador have the highest stakes. In 2020, their exports to these three countries comprised 4%–6.6% of their total exports.12

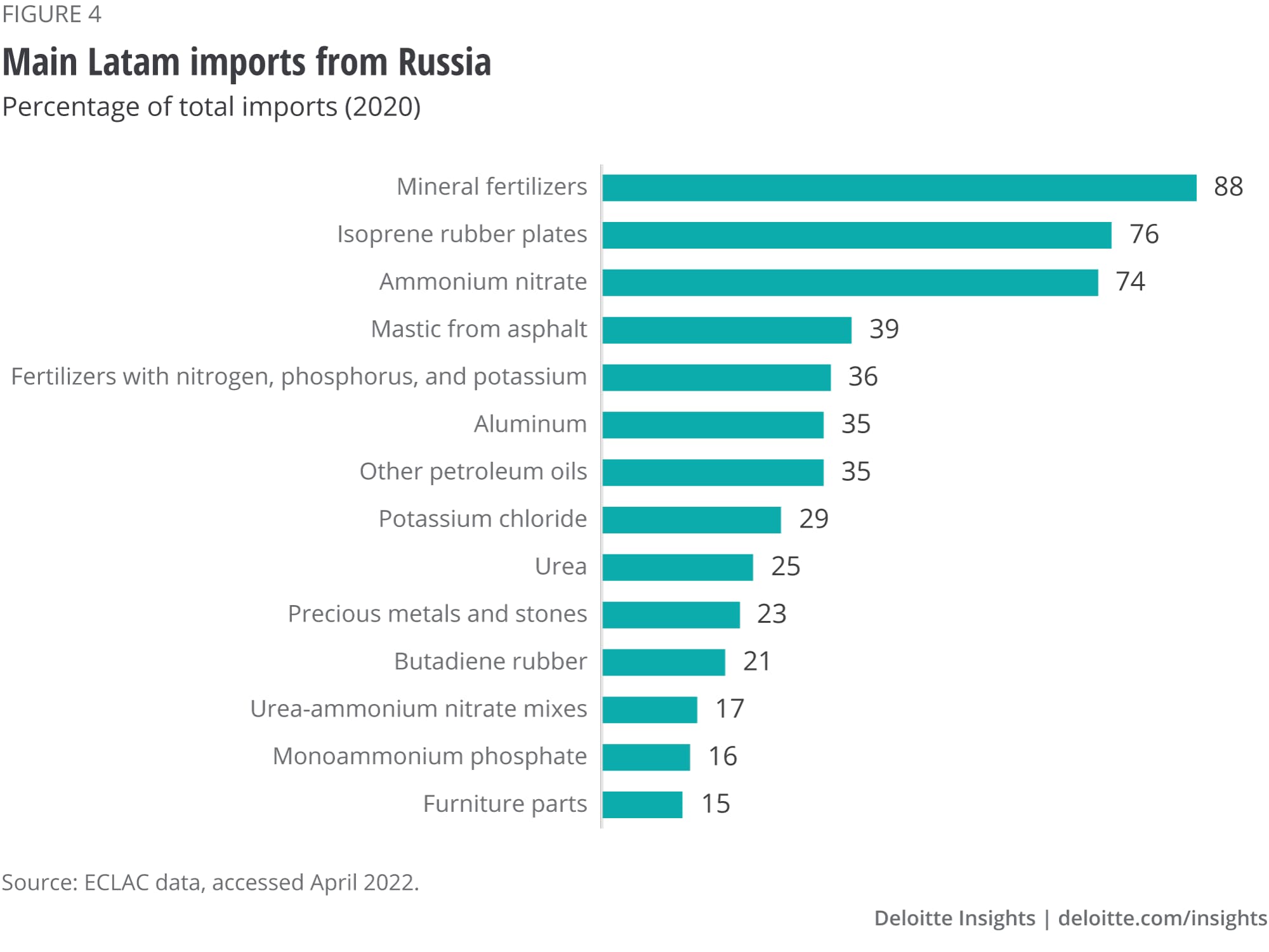

Meanwhile, imports from Russia, Ukraine, and Belarus accounted for merely 0.7% of all Latam imports in 2020. Brazil is the biggest partner as it receives 1.8% of its imports from these three countries. However, despite their small proportion, imports from those countries are concentrated in key industries. In 2020, for example, 88% of the region’s mineral fertilizer purchases came from Russia (figure 4). Additionally, critical inputs for the automotive industry originate in Russia. These include isoprene rubber plates (76%), aluminum (35%), and butadiene rubber (21%). Thus, agriculture, manufacturing (e.g., automotive), and construction industries are directly affected by the decline in the supply of raw materials from those countries.13

The surge in the prices of raw materials may likely benefit net commodity exporter countries. Some of their imports, in contrast, are considerably affected. To understand what this means in detail, let’s take a closer look at Argentina, Colombia, and Mexico.

Commodity prices, given their impact on trade and fiscal balance, play a significant role in the Argentine economy. While the trade effect is positive, the fiscal one is negative. As regards the former one, the rise in commodity prices is boosting agricultural exports (the country’s main source of foreign currency), but it is making gas imports more expensive during the winter. According to Deloitte estimates, the trade net effect is positive and slightly more than US$5 billion (1.0% of GDP). As for public finances, tax revenues will benefit from a higher collection of withholdings. However, higher energy subsidies can be problematic, if the tariff adjustment scheme contemplated in the agreement with the IMF remains unchanged. If this is the case, the net impact on public finances would be negative, at around 0.6% of GDP, because the increase in subsidies would exceed that of withholdings.

Colombia stands to benefit from the commodity price increase. Colombia exports crude oil and imports refined fuel, but exports are approximately two times bigger than imports. So, the trade surplus for oil-related goods in the first quarter of 2022 is 68% larger compared to the previous year. When it comes to public finances, the result is also positive, but not as straightforward. The price of petrol in Colombia is regulated and has not increased as much in the midst of the ongoing trend of rising oil prices internationally. According to Global Petrol Prices,14 out of a sample of 170 countries, the local oil price in Colombia is the 19th cheapest in the world. A petrol subsidy, which amounts to roughly US$5 billion per year (COP 20,000 billion) with the current prices, explains why the local value is only 55% of the international price.15 Despite the cost of the subsidy, the country is a net winner when oil prices go up. Estimates vary, but for every dollar increase in the price of oil, the Colombian government receives an additional US$130 million per year.16 Since the government budgeted a Brent price of US$70 for 2022, considering the current price is US$114, the added revenue would be US$5.7 billion and would offset the size of the subsidy.

Finally, Mexico is a net importer of crude oil and its derivatives. In 2021, hydrocarbon exports (mainly crude oil) reached US$28.9 billion.17 However, the imports of gasoline and other petroleum products totaled US$53.9 billion during the same period. The net balance has been negative since 2015, reaching US$24.9 last year, approximately 1.9% of GDP.18 Thus, the recent increase in oil prices and derivatives may induce an additional deficit in the country’s oil trade balance in 2022, of around US$7.48 billion (0.58% of GDP). The agribusiness trade balance, meanwhile, has remained in the positive territory since 2015. Its surplus in 2021 was US$7.19 billion, and the additional price effect would total around US$1.77 billion (0.14% of GDP) in 2022. All this implies that the net effect of the price increases on the Mexican deficit trade balance, at least for crude oil, its derivatives, and agribusiness, would be around US$5.71 billion (0.44% of GDP).

As for public finances, Mexico enjoys higher revenues from the export of crude oil, but also larger subsidies for gasoline consumption. A local policy dictates that gasoline price variation must be kept below inflation. So, when prices are high, the government stops charging an excise tax on gasoline and even subsidizes it, which runs a risk of becoming a tax burden. Assuming an average annual price for 2022 of US$70 per barrel for the Mexican blend, and a stable oil production (1,687 thousand barrels per day on average for 2021),19 the negative net effect of this growth in prices on public finances would be MXN 119.3 billion,20 approximately 0.5% of GDP.

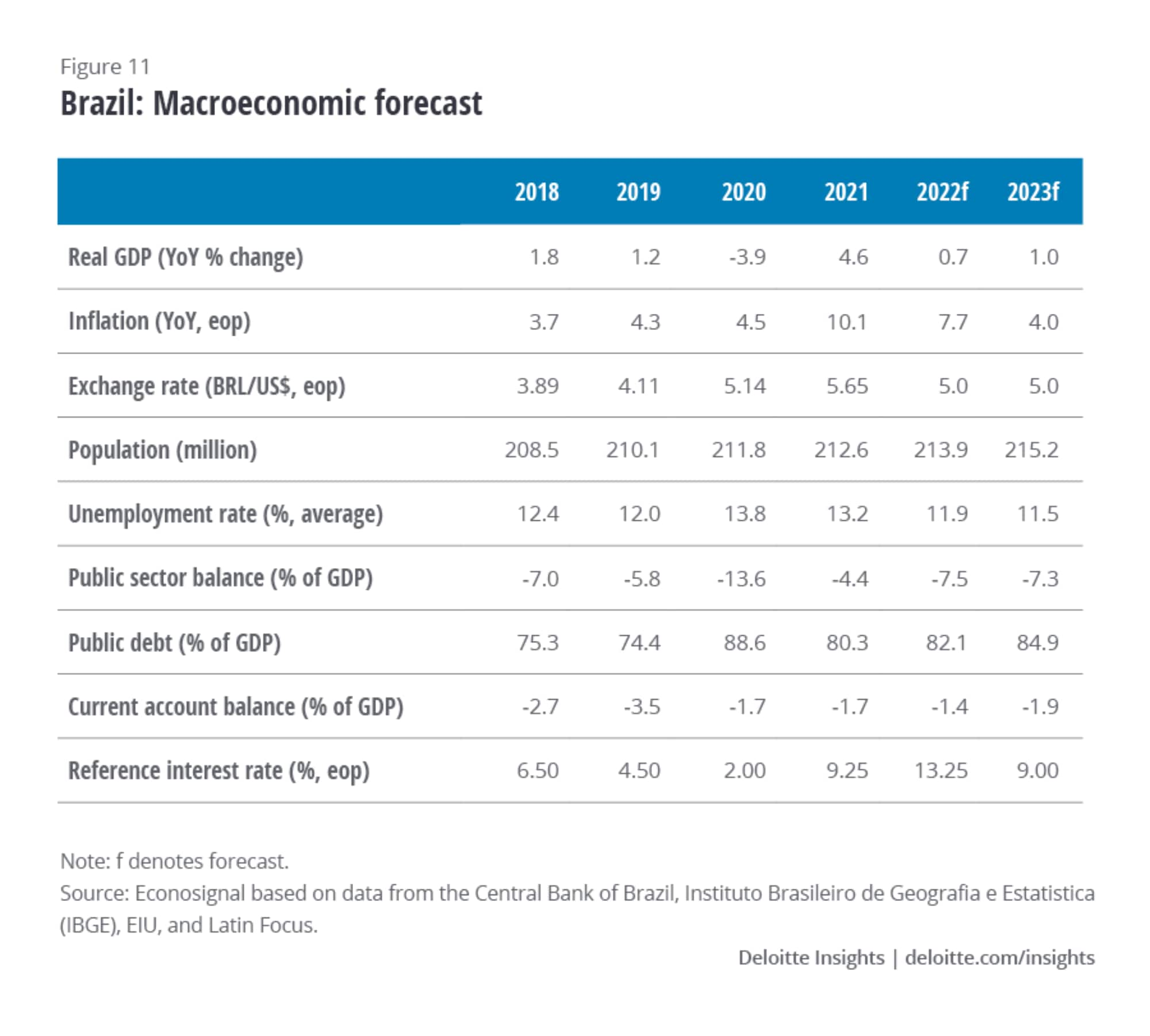

In 2021, Latam economies rebounded from a dismal performance in 2020, but this was insufficient to make up the lost ground. After contracting 7% in 2020, the economy expanded 6.8% the following year. However, disruptions emerging from the war in Ukraine have dented the economic outlook of the region and the shape of its public finances.

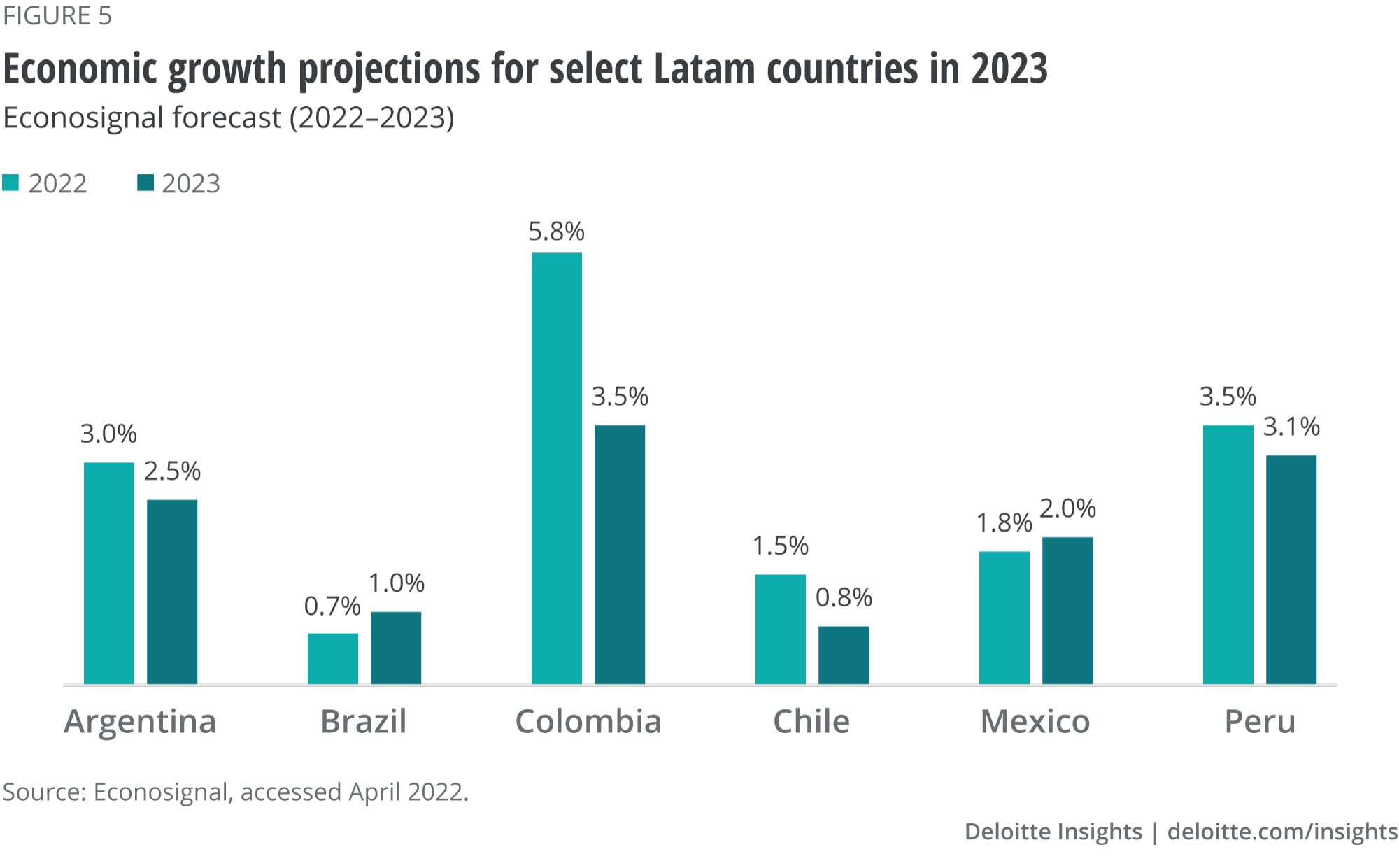

We forecast the Latam region to grow by 2.1% in 2022 and 2% in 2023. Notably, the two largest economies, Brazil and Mexico, are expected to underperform in 2022, as their growth is expected to be 0.7% and 1.8%, respectively.21 In 2023, however, these two countries will post a slightly better economic performance (figure 5).

Another challenge for the region comes in the form of global surge in inflation (figure 6). Major reasons for this surge include the supply logistics disruption caused by pandemic-induced lockdowns, China’s recently implemented zero-tolerance policy toward COVID-19, and the conflict in eastern Europe. In light of this, governments are spending more on trying to stabilize those prices.

Higher inflationary pressures have prompted central banks worldwide to accelerate interest rates hikes (figure 7). This tighter monetary policy and higher interest rates are making financing more expensive for governments, which in turn compromises debt sustainability.

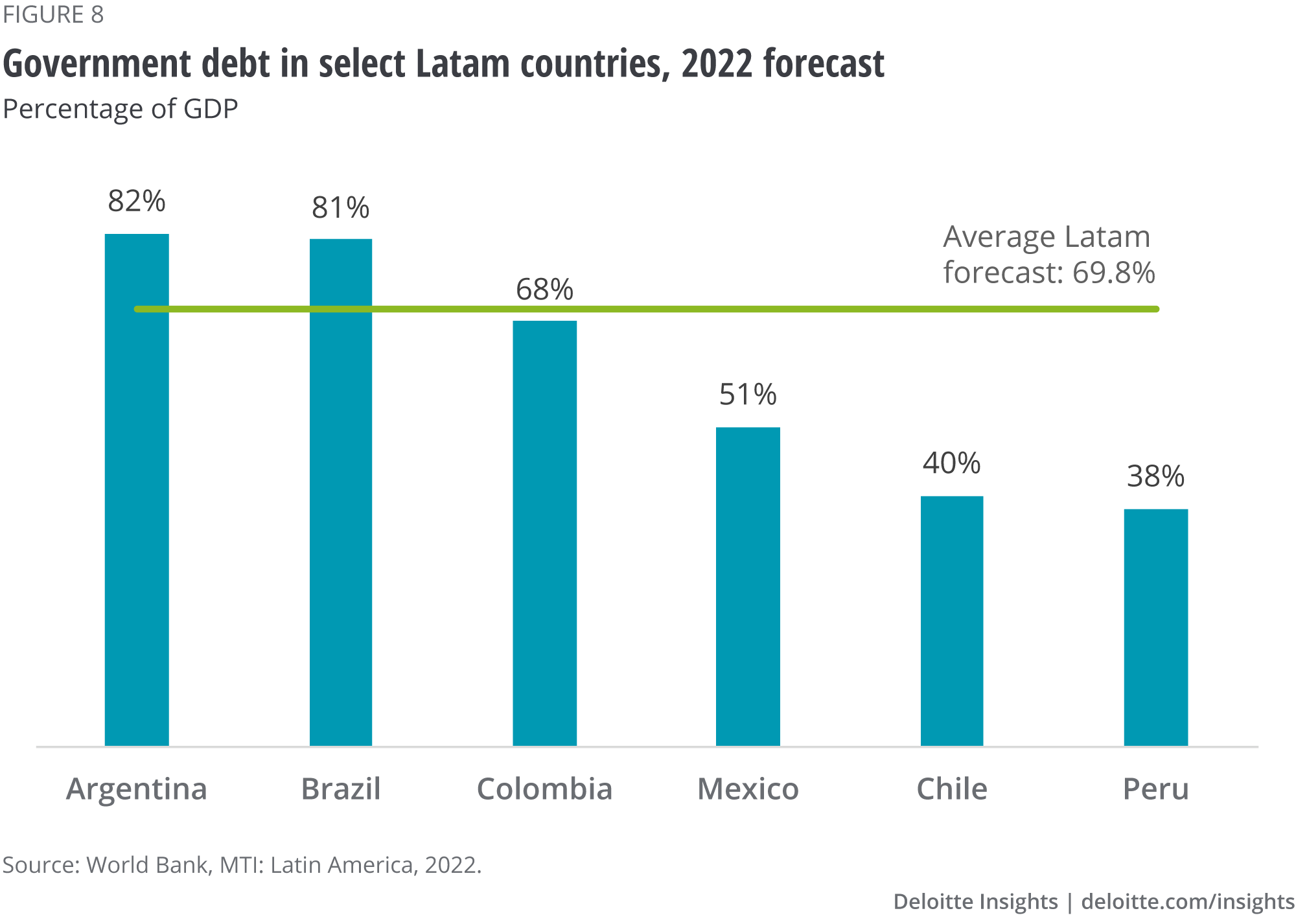

As far as public finances go, the higher spending during COVID-19, mainly through economic and health transfers to families and firms, had led to high deficits and increased government debt. Consequently, public debt in the Latam region, as a ratio of GDP, reached 71.6% in 2021, its largest ratio since early 1990s (approximately 80%).22 The World Bank estimates the ratio to be 69.8% by the end of 202223 (figure 8).

According to the World Bank’s development indicators, the region’s unemployment rate was 9.9% in 2021, down only 0.1 percentage points from 2020 and up 2 percentage points from 2019. In fact, in most countries, the unemployment rate is still above prepandemic levels. Higher unemployment together with inflation pressures risk to curb consumption.

Latam had just begun to leave behind the disruptions caused by the pandemic when Russia invaded Ukraine in February of this year, which brought with it a set of new pressing challenges. Now, the region has to deal with stronger inflationary pressures, weakening global economic growth, and higher interest rates.

This juncture prompts the need to make good use of the windfall from high commodity prices, in the countries where it has a net positive effect (the majority of Latam countries). This external shock generates the accumulation of additional inflows of foreign currencies that would be directed towards: i) investment in capacity creation and in the development of higher added value products in innovation-intensive industries that generate productivity gains; and ii) the creation of countercyclical funds, so as to finance public policies in periods of economic stress and keep debt within manageable levels.

To do so, healthier public finances are needed. Expanding the tax base and tackling tax evasion are pending tasks in several countries. Success on these fronts may reduce the dependence of public revenue on primary products. And despite the fiscal challenges, public investment needs to persist so that the economic recovery does not lose momentum. One critical area is infrastructure, such as ports and roads, and a continued investment on this side could mitigate potential disruptions in supply chains or trade logistics.

Finally, central banks in many Latam countries have been increasing interest rates to fight inflation. It is paramount to keep restricting monetary policy during this period of high worldwide inflation; however, an excessive interest rate correction might hurt economic recovery.