Australia Economy up, house prices down

3 minute read

09 February 2019

The Australian economy has gone 27 years without a recession. While there are growing risks on the horizon, economic growth should remain solid in 2019, with business investment likely offsetting the slack created by a devastating drought, a contracting housing sector and subdued consumer spending.

Australia’s economy remains on track. Strong global growth—particularly in Australia’s neighbourhood—is adding to national income, while a combination of rising commodity exports and government spending is ensuring that economic growth continues at around trend pace.

Yet, what the latest set of national accounts figures laid bare is that there is likely to be a number of challenges to economic growth in 2019.1 Both housing activity and house prices are going backwards—the housing correction we had to have, given the frenzied price growth in recent years. In addition, the current drought afflicting large parts of the country’s interior is also weighing on activity and creating significant difficulty in some regional communities. While these remain ongoing concerns, Australia’s broader economic fundamentals remain favourable.

That broader strong performance is seen in employment growth. Australia’s labour market is consistently adding more jobs than is needed to accommodate the growth of the working age population. This has resulted in steady declines in the unemployment rate while the participation rate has also increased to its highest level on record. Job gains have been broad based across most sectors, but strongest in business and household services.

Australia’s resource sector has also been a strong contributor. Increased resource production capacity from recently completed LNG plants will add to economic growth over the next 12–18 months. Additionally, Chinese stimulus in response to the negative effect of the ongoing trade conflict with the United States is keeping key commodity prices (iron ore and coal) higher than they would otherwise be.2 However, given that the current strength in commodity prices is a response to economic weakness, it is not expected to be permanent.

On the positive side, leading indicators for business investment suggest that it will pick up some of the slack left by weakness elsewhere. Strong growth in profits, increased capacity utilisation, low borrowing costs for big business and the need to spend money to maintain Australia’s significantly expanded mining capital stock all point to growth in investment over 2019 and 2020.

However, other recent supports for the economy may now begin to fade. Dwelling investment is likely to detract from growth over the short term, while the boost from public demand will weaken as the rollout of a new social insurance scheme for Australians with disabilities finishes. Public infrastructure spending has lifted strongly in recent years, but is also expected to peak this year.

That presents a number of risks. Large house price falls (coupled with the already significant fall in equity prices) may reduce households’ willingness to spend as their wealth declines. Consumer spending may then weaken as a result. Consumers will be relying on wage growth to boost spending, substituting the reduction in wealth. Wages have been moving up, but the rate of improvement has been slow.

Housing sector faces gravity

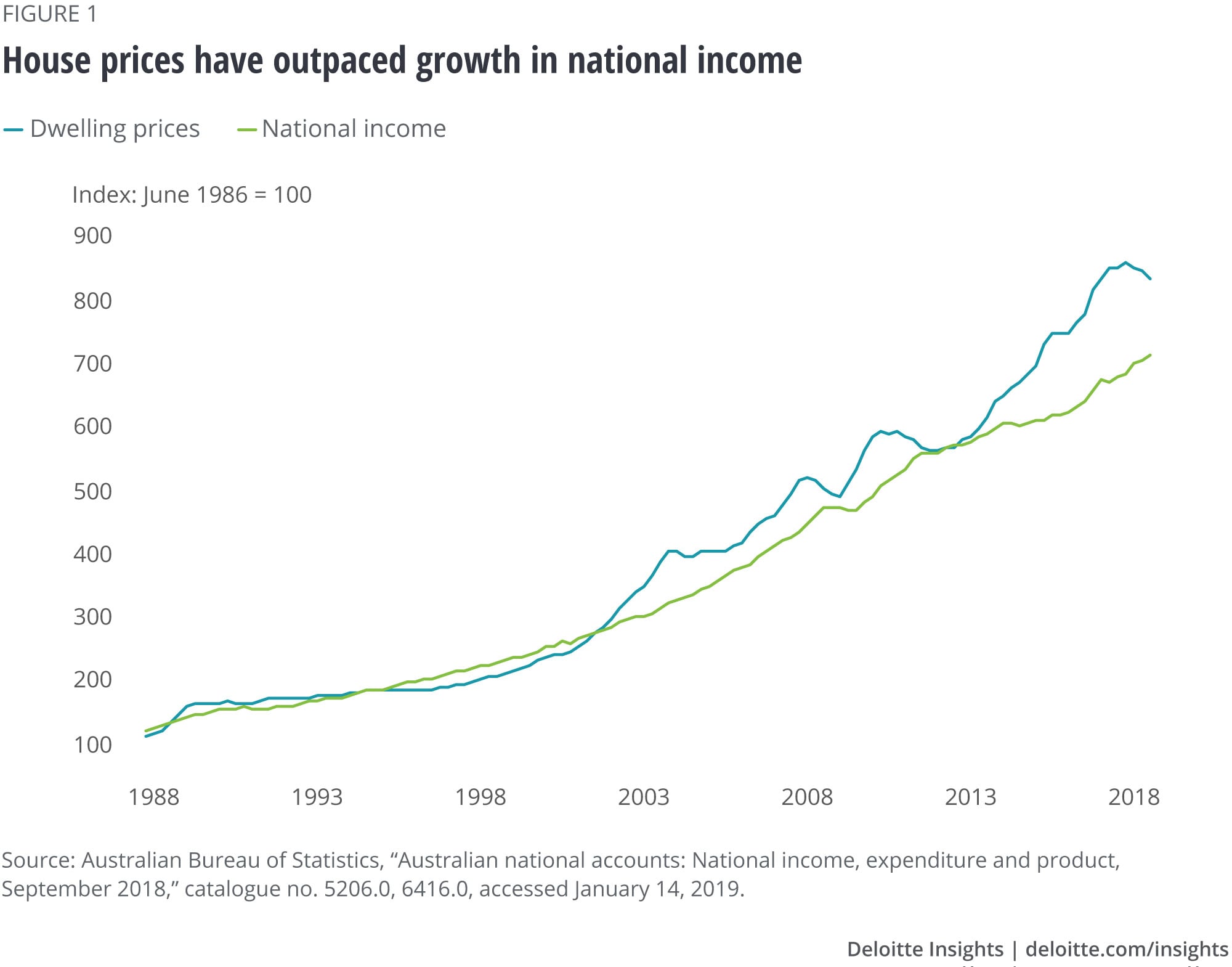

The former Australian Prime Minister Paul Keating once said of Australia’s last significant recession in 1991 that it was “the recession that we had to have.” Whether or not that was true, it is arguable that the former PM’s sentiment could be applied to the current downturn in Australian house prices. As figure 1 shows, house price gains since the start of the millennium have far outstripped national income growth. This has been particularly true over the last five years, in which a trifecta of record low borrowing costs, strong demand from overseas investors and red-hot population growth sent demand sky high.

More recently, the effect of some of these positive factors has faded, while others have become outright nasty for the market. A combination of tighter regulation and more cautious lending due to the Banking Royal Commission at home, coupled with increased global funding costs and reduced investor interest (including from overseas), has resulted in a reversal in fortunes. Prices are down 6.1 per cent and 4.5 per cent from their peak in Sydney and Melbourne respectively, Australia’s two largest markets.3 While these falls are significant (and getting worse), some perspective is important, as prices are still respectively 74 per cent and 59 per cent above their previous cyclical trough.

Additionally, the current price correction is occurring during a time of strong employment growth, which is helping households to absorb the impact of falling wealth. This is particularly important as Australian households are among some of the most indebted in the world. The strong economy also provides other employment opportunities for those who work in industries that are exposed to the housing cycle, such as real estate agents and builders.

Overall, the broader effect of the current decline in house prices across most Australian cities seems manageable, even as prices are expected to continue falling into 2019. On balance, we see a continuation of Australia’s impressive run of more than 27 years without a recession, with growth at or above trend over the short term.

Deloitte Global Economists Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- David Rumbens

- Partner, Financial Advisory

- Australia

- drumbens@deloitte.com.au

- +61 3 9671 7992