India economic outlook, January 2023 has been saved

The author would like to thank Rupesh Bhat for his contributions to the article.

Cover image by: Jaime Austin

Apart from the customary change in dates, very little in the new year feels different from the one gone by for the global economy. Geopolitical uncertainties continue unabated, a legacy of the last year, and there’s wide consensus among economists now that the global economy is on the verge of entering a phase of severe slowdown.

It is unlikely that India will remain insulated from these developments. But here is a bit of good news as far as India’s economy goes—there are enough reasons to be optimistic about India’s economic outlook in 2023. In particular, healthy domestic drivers will likely help the country post reasonably strong growth this year.

The private sector balance sheet has improved over the past couple of years, implying that the private sector is poised to increase spending, which can boost capex as and when the investment cycle picks up. Besides, corporate deleveraging has improved banks’ balance sheets, aiding the banking system to come out of the asset quality cycle. Furthermore, high goods and services tax (GST) and direct tax collections have provided the government ammunition to spend and cushion the impact of the impending global slowdown and keep the economy buoyant. Consumer demand among the affluent class remains strong as is evident from the robust growth in the retail industry and the better profit performance of consumer staples and discretionary companies in recent quarters. Also, recent labor market data suggests a strong rise in labor force participation and job creation in certain sectors. However, job growth has to sustainably improve to translate into durable demand growth.

The path to sustained recovery, however, will be distorted, given three major challenges India is likely to face. First, inflation will likely remain high this year even though it may have already peaked or may peak soon. Second, aggressive tightening of monetary policies across the central banks of advanced economies is likely to cause a global slowdown this year, impacting domestic investment and consumer demand as the proclivity to save increases. Tighter liquidity conditions may also result in capital outflows and a rising imbalance in the balance of payment account. Third, the labor market is yet to improve, and the pandemic’s seemingly imminent return remains a wild card that could derail the strong recovery in the services sector as well as consumer demand, both of which are critical to GDP growth.

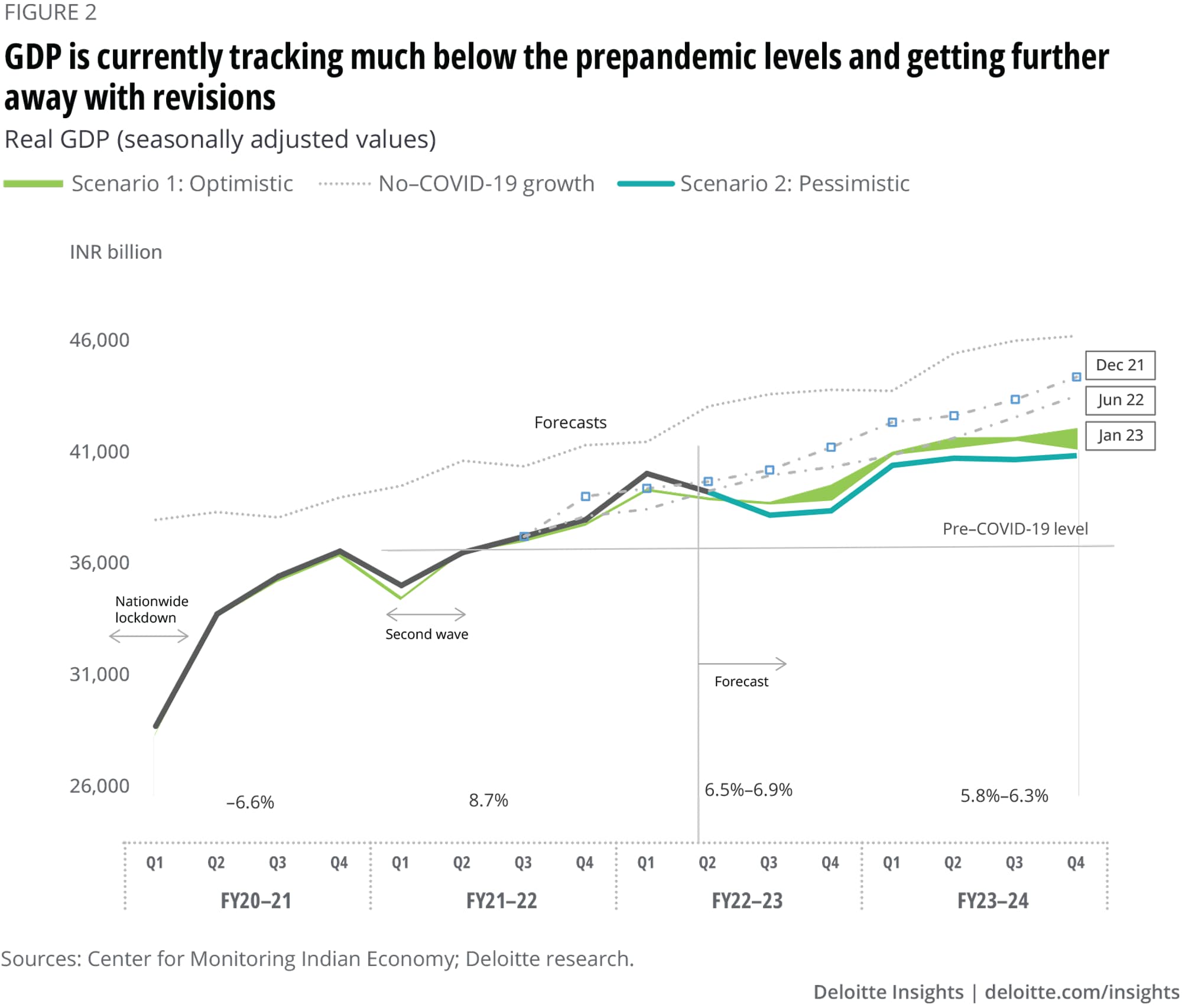

Given that the economy turned out to be weaker in H1 FY 2022–23 than we had anticipated, we have revised our outlook. We expect India to grow in the range of 6.5%–6.9% in FY 2022–23 and 5.8%–6.3% in FY 2023–24. Considering the extent of volatility associated with the global and domestic economy, we are restricting the duration of our projection to just a year ahead. Hopefully, we will be better positioned to predict beyond a year by the next outlook release.

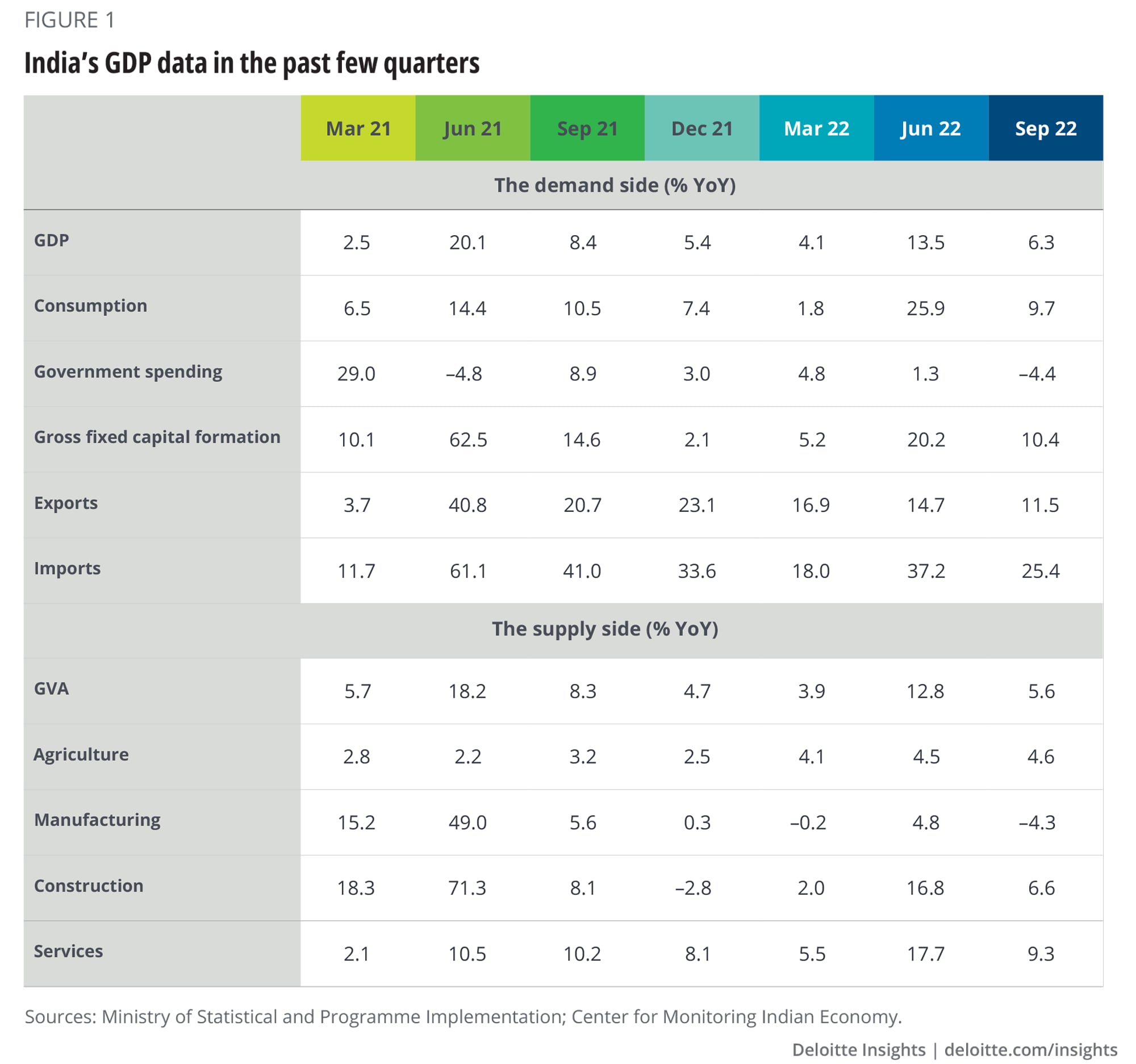

India’s GDP grew by 6.3% year over year (YoY) in the July–September quarter of FY23. While this growth appears substantially lower compared to the April–June quarter (13.5%), strong growth in the latter was because of the low base effect. In 2021 this quarter, the economy was severely impacted by the second wave of the infection and consequent mobility restrictions, which dragged economic activity down.

It is heartening to see that, from the expenditure side of accounting, gross fixed capital investment and private consumption remained robust and grew by 10% YoY. Participation of the state governments and the private sector in investment spending was low. Strong growth in private consumption, especially in the discretionary segment, is a good sign and may cue the private sector to boost investment, which has remained muted despite higher capacity utilization. All other drivers weighed on growth. Negative inventories suggest that businesses preferred to exhaust their stocks, which means that they will have to ramp up production if consumer spending holds up.1

Surprisingly, government spending contracted by 4.4%, taking away a chunk of the GDP growth in Q2. This was despite strong revenue growth in the quarter. Both exports and imports increased, but the latter accelerated faster thereby widening the current account deficit.

On the production side, gross value added (GVA) grew by 5.6%. Contraction in manufacturing and mining sectors (–4.3% and –2.8% YoY, respectively) weighed on the overall sectoral contributions to economic activity. In our previous outlook, we highlighted the issue around the possible low contribution of manufacturing, despite the sustained push by the government. The revival of the services sector by 9.3% helped boost growth, with “trade, hotels, transport, communication, and services related to broadcasting” sectors witnessing very strong growth of 14.7%. That said, these sectors remained below the prepandemic trend levels (and are the only services sectors that have not yet caught up). Agriculture grew at a healthy rate of 4.6% despite the unseasonal and uneven pattern of rains.

October–December has been a busy quarter for consumers, and those who have been travelling outside or recently visited shopping malls may have witnessed a spurt in consumer spending. The latest economic data, however, provides mixed signals.2

On the positive side, the manufacturing purchasing managers’ index (PMI) in December rose to the highest levels in over two years. This comes after two months of low industrial production numbers. The falling inventory levels and strong demand during the festive quarter were bound to push production up.

Capacity utilization in the manufacturing sector is now above its long-run average (although it varies quite a lot across sectors), which bodes well for fresh investment activity in creating additional capacity. According to the Center for Monitoring Indian Economy (CMIE), the total value of new private sector investment proposals in 2022 saw an uptick—in fact, this value reached the highest level since 1996, with proposals worth INR 19.7 trillion made so far. That said, the number of proposals has been relatively small. This could mean that businesses have resources to invest but are focused and prudent about investments. They are spending on select but high-valued projects. Credit growth, meanwhile, remains healthy as banks with better balance sheets and margins are willing to lend.

On the other hand, exports visibly slowed down in October and November 2022 and are likely to moderate even further this year. The INR is still struggling to anchor itself against the US dollar. Lately, the USD index has declined, but INR has not seen a reversal in valuation against the dollar. The consumer price index (CPI) may have peaked but it is too early to say if it has stabilized. For the Indian economy to post a strong recovery, it is imperative that inflation remains on a sustained downward path.

Foreign investment, which fell to its lowest after June 2020, is gathering pace moderately. November was a strong month on this front, but flows tapered in December. Last, but not the least, although job creation has improved, incomes haven’t seen the rise needed to beat inflation. Moreover, job opportunities and wage growth among the low- and middle-income populations grew modestly.

Not all headwinds are meant to be challenges. For instance, globally, nations and multinationals are emphasizing resilience in, diversification of, and securing their supply chains in light of geopolitical developments and global exigencies. India presents huge potential and opportunities as an export hub and investment destination in the manufacturing and services space. India’s recent trade agreements are aimed at integrating the manufacturing sector with the global supply chain. Consequently, there has been a healthy rise in foreign direct investment (FDI) equity flows from Japan, Singapore, the United Kingdom, and the United Arab Emirates in H1 FY2022–23, even as FDI from the United States fell. This points to a rising confidence among global investors to invest in India and India’s inflows are becoming more diversified.

More so, low asset values have led healthy companies to consolidate positions and enter new segments.3

Defying trends, India registered record mergers and acquisition deals in 2022, with the biggest transactions seen in banking, cement, and aviation. Many conglomerates entered new businesses, while brick-and-mortar companies partnered with technology firms.

India’s trade with Russia has shot up post the Russia-Ukraine war. According to Reuters, imports of the top five principal commodities have increased since the war as India imported these commodities at discounts.4 India also benefits from the fact that its refineries are best suited to process Russian oil.

We believe the path to recovery for the Indian economy will be lengthier with consumer spending moderating owing to pressures from inflation and higher borrowing rates. Investments will likely be the biggest growth drivers, primarily driven by the government sector capital spending, while the private sector may take some time to join the investment bandwagon. The private sector will, however, likely continue with focused spending on select projects in the meantime, as was observed last year.

Our key assumptions for the forecast remain in line with what they were in the previous outlook (See the sidebar, “Key assumptions” for more information on our optimistic and pessimistic scenarios). Given that the economy turned out to be weaker in H1 FY 2022–23 than we had anticipated, we have revised down our outlook by 0.2 percentage points this financial year. The downside risks for the currency and the current account balance have also increased. Unfortunately, with each revision, the actual GDP gets further away from the no–COVID-19 GDP trend, indicating the extent of the damage that may be difficult to reverse (figure 2).

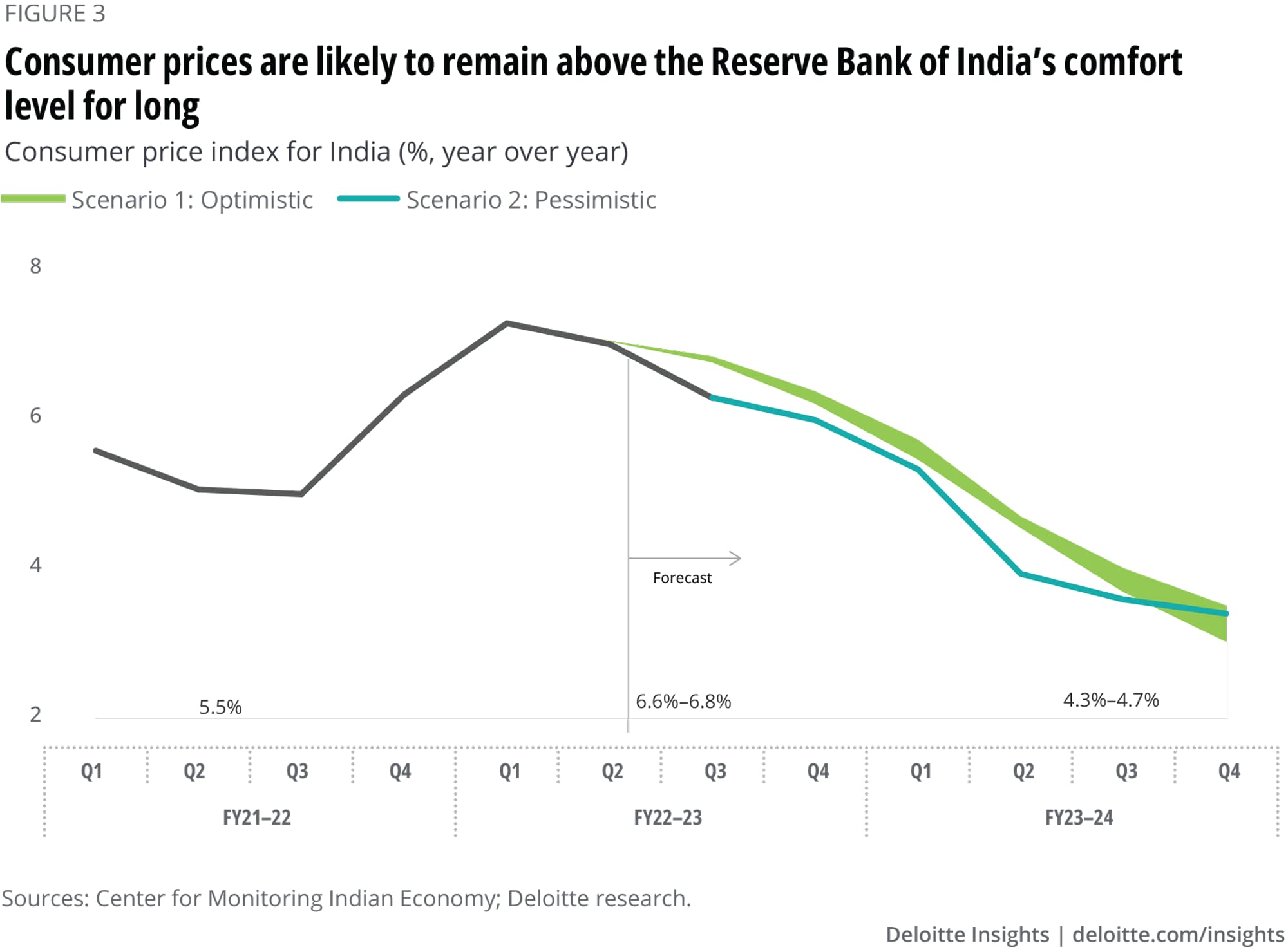

The rise in prices may peak soon but sustained demand growth will keep pressure on supply, leading to overheating of the economy. A high base effect may aid in easing inflation, but it will remain on or above the Reserve Bank of India’ (RBI’s) comfort levels (4% + or –2% YoY) this year and even the next, before easing in the second half of 2024 (figure 3).

The budget is around the corner and while we have a long wish list, here are our four key expectations.

Improve supply chain to control inflation: While there will be a continued fight against inflation, India needs sector-specific targeted efforts to manage supply, and therefore, inflation. For instance, a large part of inflation is due to food prices, and the government must make efforts toward building infrastructure to optimize the food and agribusiness supply chain. Developing market linkages by identifying and connecting farmers with buyers and facilitating contract negotiations between the two could be critical.

Incentivize the services sector for job creation: The government’s focus has rightly been on sectors such as infrastructure, construction, and manufacturing that create jobs for workers across all skills. However, the services sector has huge potential—be it in retail, trade, or information technology. So, while India continues its focus on various schemes such as Product Liked Incentive to promote manufacturing and sunrise sectors, it will have to also focus on the services sector where India is competitive and has a comparative advantage. An effort toward building global in-house centers of the world and adopting agility in doing business could revive the services sector and create employment opportunities.

Find new sources of revenue: The government will have to support growth by boosting spending to cushion the impact of global exigencies as well as the global economic slowdown. Besides, the government will have to continue the momentum in infrastructure spending to ensure jobs and asset creation. The challenge would be to raise resources for the expenses it incurs. While tax revenues have been strong, thanks to the economic revival and inflation, the government will have to monetize assets so that it can front-load its expenses this year. While the government exceeded its asset monetization target in FY22, it is likely to miss the target for the ongoing fiscal. Going forward, it will have to focus on states with large monetization base, identify potential assets that can be monetized, and also bring in strategic partnerships with private players to allow private capital to flow into select sectors.

Prepare India to bounce back when the global economy recovers: The government needs to focus on completing ongoing infrastructure projects and boosting sectors with strong linkages and multiplier effects. While progress in several infrastructure projects has been good so far, highway networks are yet to gain momentum and progress in power and energy has been modest. The emphasis should be toward improving financial inclusion and technology connectivity beyond Tier-1 cities. Furthermore, focusing on supporting the micro, small, and medium enterprises sectors could help India achieve all-inclusive growth.

{kind=link}

{kind=link}

{kind=link}