India economic outlook, July 2022 has been saved

Cover image by: Jaime Austin

As 2021 was coming to a close, there was optimism in the air. India was gearing up for a strong economic recovery—several forecasters such as the International Monetary Fund expected growth to exceed 9% this fiscal. This optimism received a jolt early this year as a wave of omicron infections swept through the country (which, thankfully, did not last long), and then in February, Russia invaded Ukraine. These events aggravated the preexisting challenges such as surging inflation, supply shortages, and shifting geopolitical realities across the world with no definite end in sight. And the subsequent confluence of headwinds such as surging commodity prices and disruption in trade and financial transactions quickly deteriorated economic fundamentals that were trending up a few months back. Consequently, this has compelled us to temper our growth expectations.

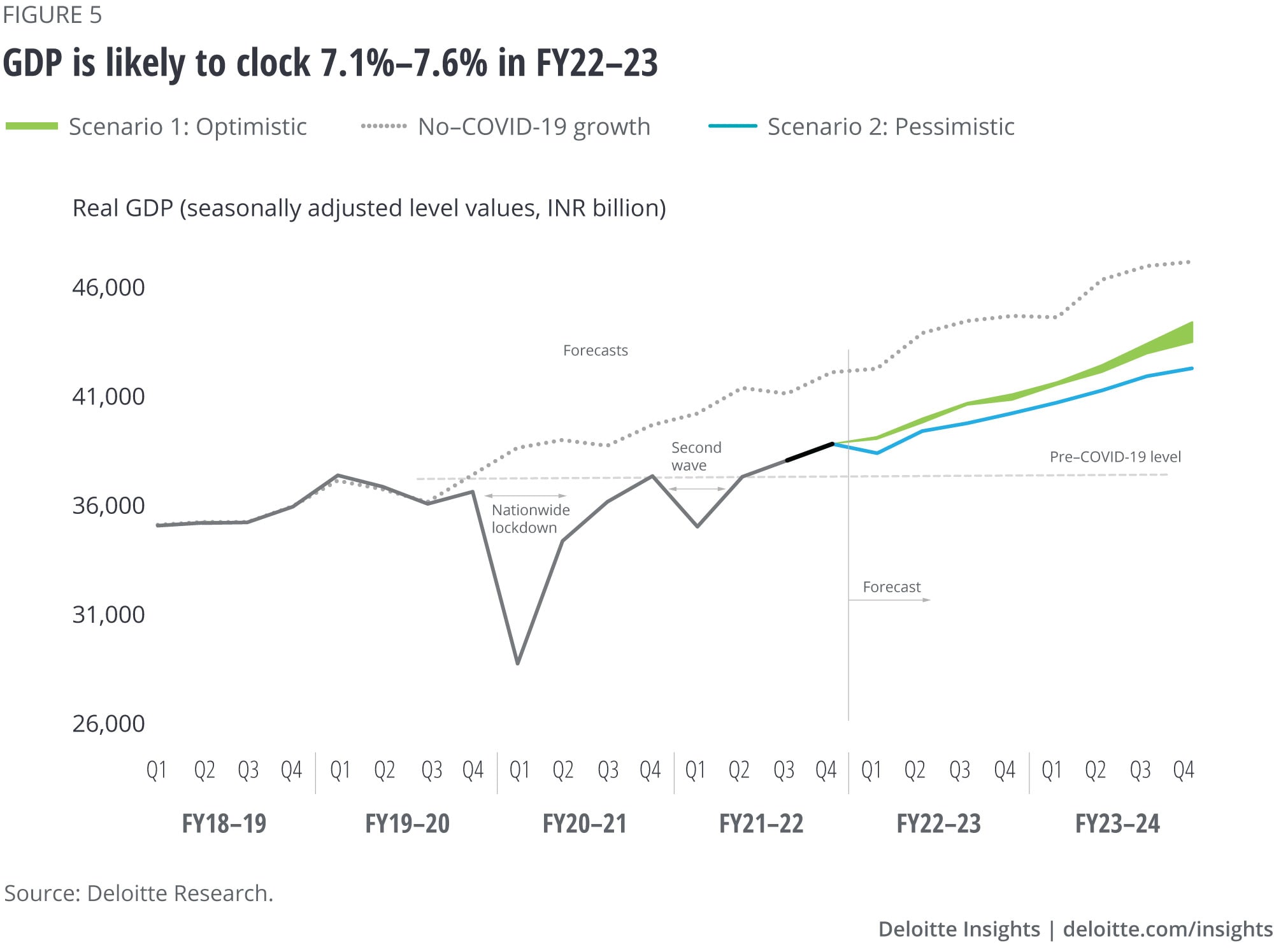

However, we believe the risks are not strong enough to deny India an economic rebound given the domestic demand potential. We expect India to grow by 7.1%–7.6% in FY22–23 and 6%–6.7% in FY23–24. This will ensure that India reigns as the world’s fastest-growing economy over the next few years, driving world growth even as several major economies brace themselves for a slowdown or possibly a recession.

India is primarily a domestic demand–driven economy with consumption and investments contributing to 70% of the economic activity. According to the Reserve Bank of India (RBI) analysis of 10,000 listed companies, businesses have seen a steady net profit-to-sales growth over the past year and are sitting on piles of cash (as evident from the cash coverage ratio).1 Although investments are growing sporadically partly because of supply chain disruptions and global uncertainties, industry and service activities remain robust, as indicated by the recent Purchasing Managers’ Index (PMI) numbers for India (figure 1).

Inflation, like in many other countries, has been hard on Indian consumers, with low-income households getting disproportionately impacted. That said, consumer confidence is improving with the easing of mobility restrictions.2 There is an appetite for spending among the top 10 income percentile of the population that has not spent for more than a year and thus is onto revenge buying and traveling. The number of flights taking off and hotel reservations have enthused travel industrialists. Revival in business travels and in-person client interactions have also helped the hospitality sector.3 Furthermore, the number of foreign tourists visiting India almost doubled between January and April this year.4 While demand for services is skyrocketing as is evident from the PMI numbers that were at an 11-year high in May 2022, the industry sector is also holding up well (figure 1).5 Demand for electricity in the first six months of the year has been higher than in the past three years. The number of vehicles registered, meanwhile, has reached prepandemic levels.6

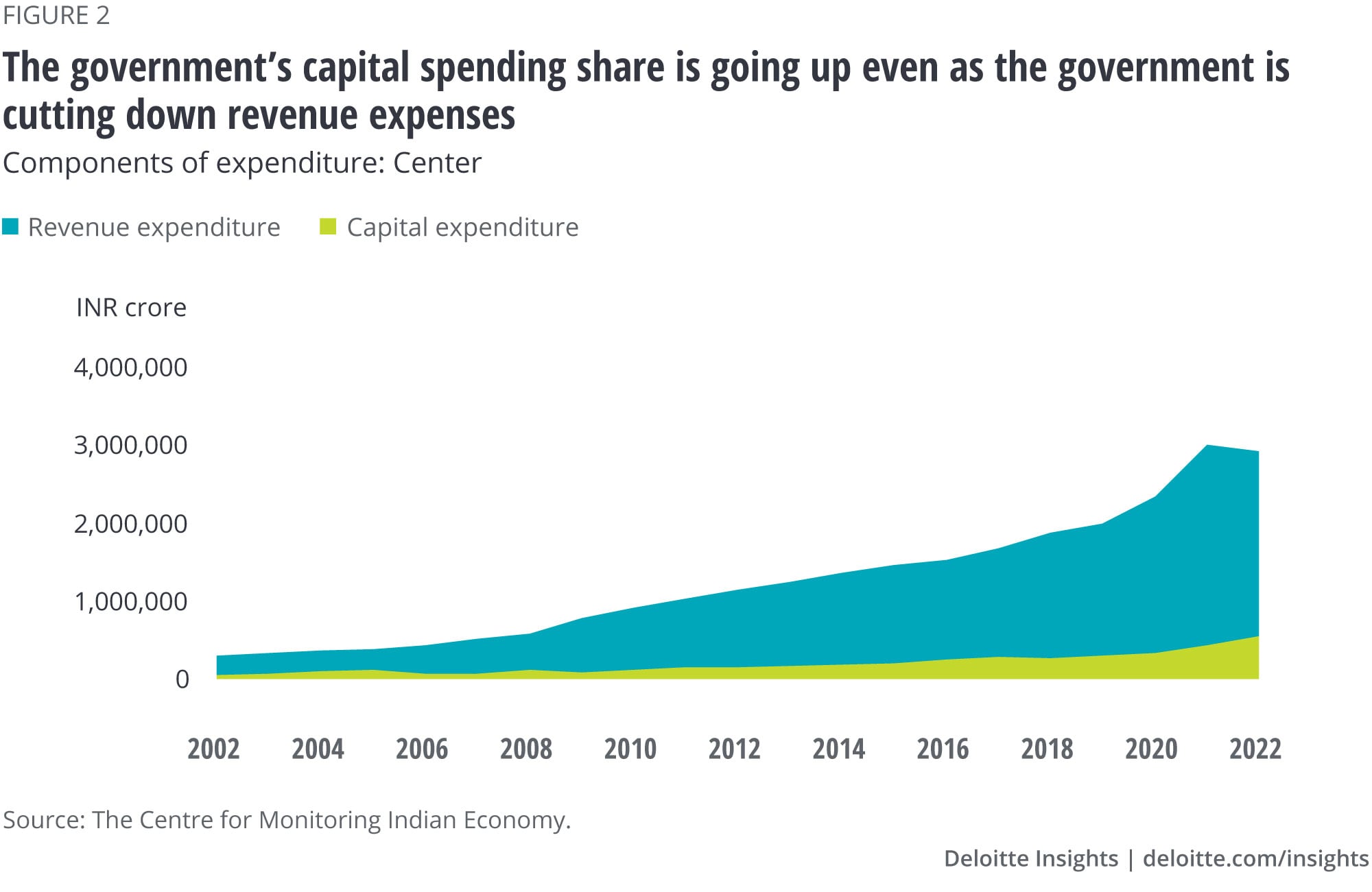

The other good news is that the government’s capital spending share is going up even as it is cutting down revenue expenses (figure 2). India’s gross tax collection has beaten all expectations. The total tax collection reached INR 27.07 lakh crore (US$356.82 billion) in FY21–22, surpassing the government’s revised target by a substantial margin.7 Improved economic activity and better compliance efforts in taxation have aided in better revenues. The tax buoyancy (which is a measure of growth in tax revenues compared to GDP growth), the simplified tax regime with low rates, comprehensive review and rationalization of the tariff structure, and digitization of tax filing are likely to support further capital spending in the future. Higher capital spending on infrastructure and asset-building projects is likely to boost growth multipliers in the medium term.

Last, but not least, exports, in terms of their contribution to GDP, performed exceptionally well during the pandemic and bolstered recovery when all other growth engines were losing steam. Going forward, the contribution of merchandise exports may waver as several of India’s trade partners witness economic slowdown. That said, the opportunity to boost services exports on the back of the global digitization wave is promising. Similarly, India’s manufacturing sector growth looks encouraging as several multinational companies will look for resilience and cost-effectiveness in light of the China Plus One strategy (for more on this strategy, watch out for our upcoming report on India’s readiness for Trade 4.08).

Moreover, if an expectation of a global economic slowdown results in a fall in commodity prices, which is what commodity indices currently indicate, Indian import bills will also come down.9 That may improve India’s current as well as fiscal accounts.

Inflation—which began after the pandemic led to supply chain disruptions, and then exacerbated due to the war in Ukraine and the subsequent sanctions on Russia—has emerged as the toughest challenge for economies around the world.

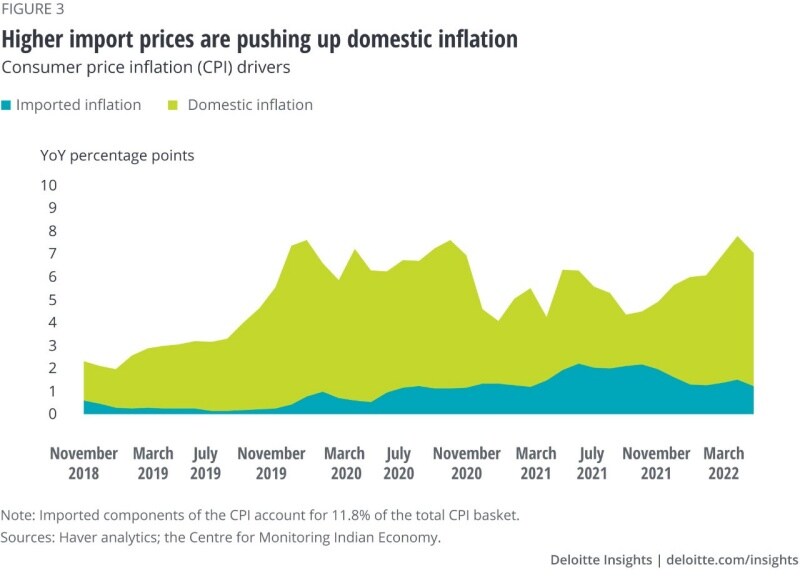

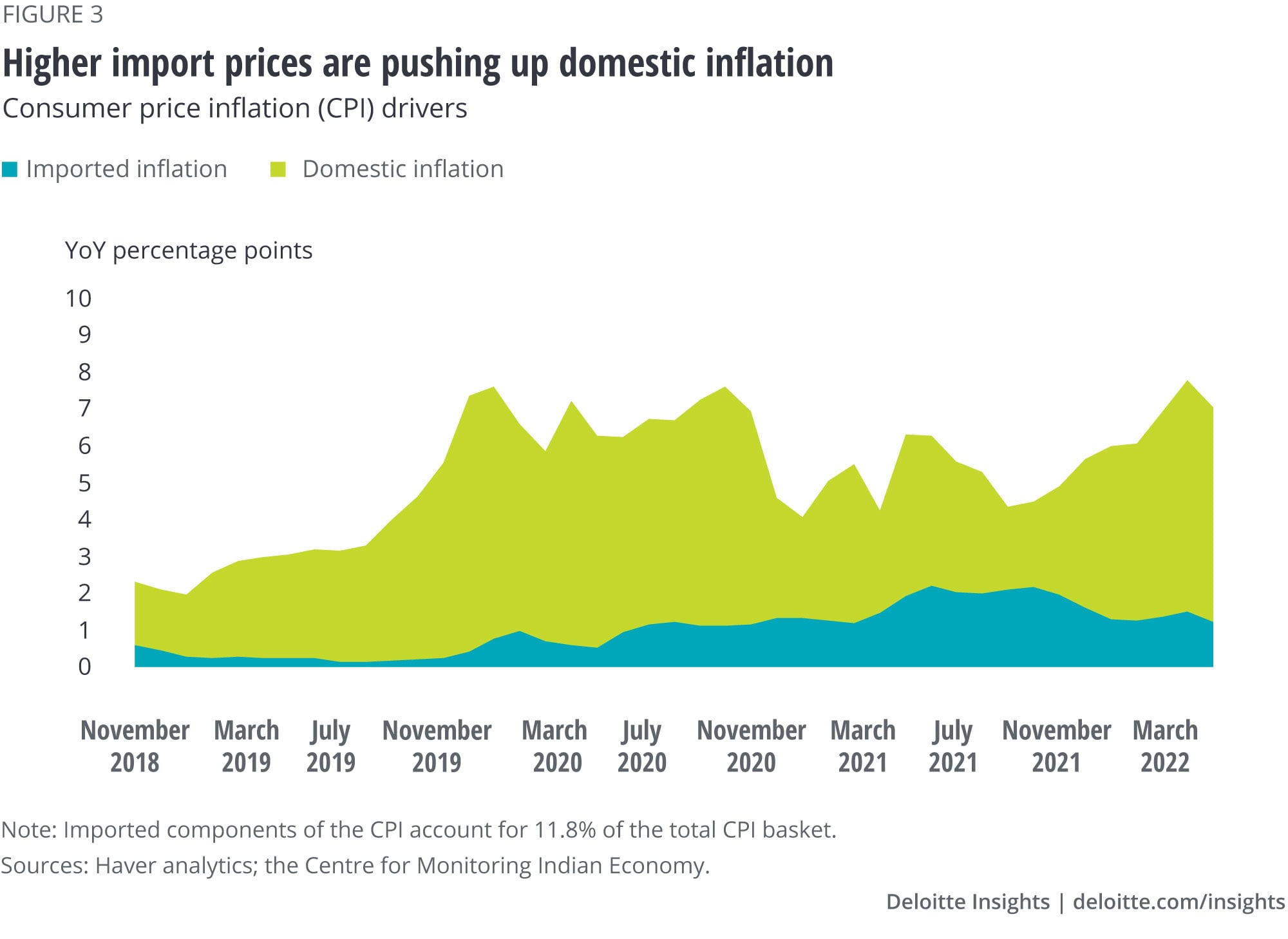

Inflation remained a persistent problem in India throughout the pandemic. A large part of it was earlier driven by high food prices, followed by fuel prices that started rising in 2021. Lately, a surge in demand for services has contributed to inflationary pressures. Most importantly, rising prices of commodities and raw materials globally have also seeped into the economy through imports. According to our estimates, the contribution of high import prices to domestic inflation remained significant throughout the pandemic (figure 3).

The danger of persistent and prolonged inflation is that it reinforces inflation expectations. It then pushes up core prices (those excluding food and fuel prices, which are highly volatile) that often tend to be sticky-down. For instance, once a restaurant increases the menu prices, it rarely revises the prices down even if food inflation has eased off. In short, what started as food and fuel inflation has become more broad-based.

Till late 2021, a majority of the central banks believed inflation to be transitory. Cognizant of the fact that a tighter monetary policy cannot address supply-side issues but impact demand instead, banks globally hesitated in raising policy rates to anchor rapidly accelerating inflation. Finally, after reassessing the risks, several advanced nations decided to take the plunge; over the past six months, the central banks of the United States and the United Kingdom have been aggressively hiking policy rates, while the European Central Bank has recently hinted at similar actions.10 Moreover, many central banks are correcting their balance sheets. The possible consequences of such actions on global liquidity have unnerved investors, leading to capital flight, especially from emerging nations. These nations have seen their currency, external accounts, and borrowing cost conditions deteriorate, and to soften the blow, they have been forced to incur a higher fiscal deficit.11

With banks globally tightening their monetary policy stance and domestic inflation remaining above the comfort zone (of 4%+2%) for several months, the RBI was left with very few policy choices. It sprang into action and raised the policy rates by 90 basis points within a month. It also has started reducing liquidity in the market, although it has kept the monetary-policy stance accommodative so far.

The challenge is that the aggressive rate hikes may not result in taming inflation immediately. The rate hikes and liquidity squeeze are expected to raise borrowing costs and reduce demand, which, in turn, will ease price pressures. Therefore, the likely consequence of a tighter monetary policy everywhere will be a slowing down of economic activity. Concerns about a recession in the United States and the EU are imminent, and the questions being asked are “Not if, but when.”12 China’s outlook for the rest of the year, meanwhile, remains uncertain as it continues to rely on lockdowns and other restrictions to contain the spread of the virus. Activities in the property and auto sectors have also seen moderations in the region. In short, the combination of geopolitical developments and global exigencies (such as the pandemic) are stressing supply chains, creating logistics bottlenecks, influencing trade relationships, and constantly changing the trade basket and competitive advantages.

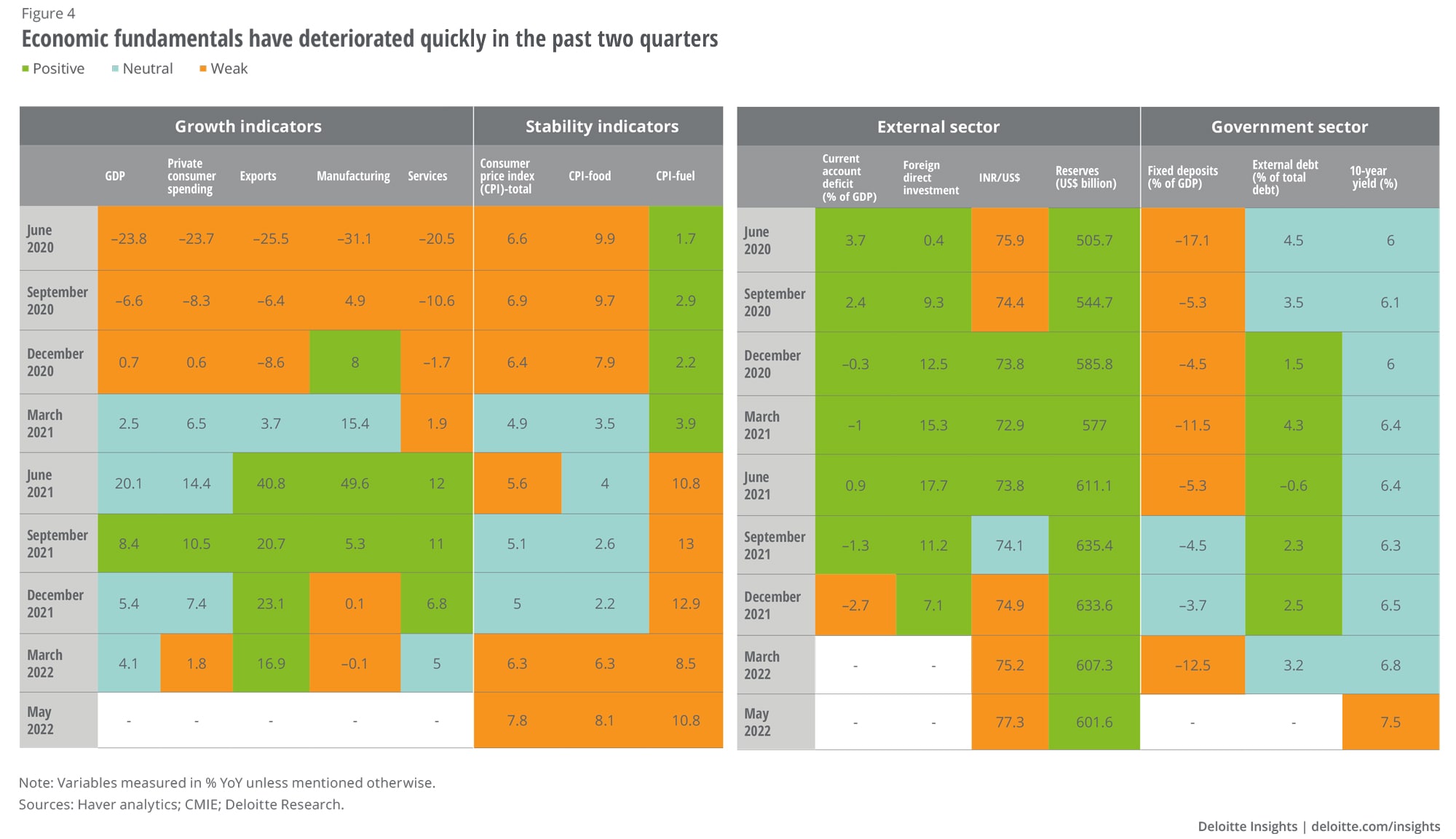

Economic fundamentals have deteriorated fast in the past two quarters, thanks to the uncertainties in and risks to the global business environment (figure 4). As a result, we have revised down our baseline projections compared to our outlook in March by over a percentage point. We expect two possibilities, with assumptions around the longevity and severity of the Russia-Ukraine conflict and the pandemic. Global economic growth and disruptions to the supply chain will be other critical determinants.

Scenario 1 is where the Russia-Ukraine crisis does not escalate but prolongs with a possibility of abating by the end of the year. Growth in the United States and the EU slows down but remains steady. The pandemic, meanwhile, has a marginal impact on the economy.

Scenario 2, a pessimistic one, is where the Russia–Ukraine crisis continues for a much longer duration, possibly spilling over into 2023. Advanced nations impose further sanctions on Russia, which provokes the latter to react (by reducing deliveries of natural gas to Europe during the winter months). Tensions escalate with several nations getting directly involved in the war. The United States and Europe enter a recession. The pandemic forces lockdowns and economic slowdown in several economies, including China. We do not associate much likelihood to this scenario.

According to our baseline (Scenario 1), FY22–23 will likely witness the strongest rebound (figure 5). Despite global risks, consumer and investment demand picks up. The buoyancy impact of the government spending (the infrastructure spending and production-linked incentive schemes) coincides with the economic recovery. Global economic slowdown, geopolitical conflicts, and rising global wages possibly enhance India’s status as a preferred alternate investment and outsourcing destination. We also expect several of the stressed economic indicators to likely improve as soon as global risks recede and recovery gains momentum.

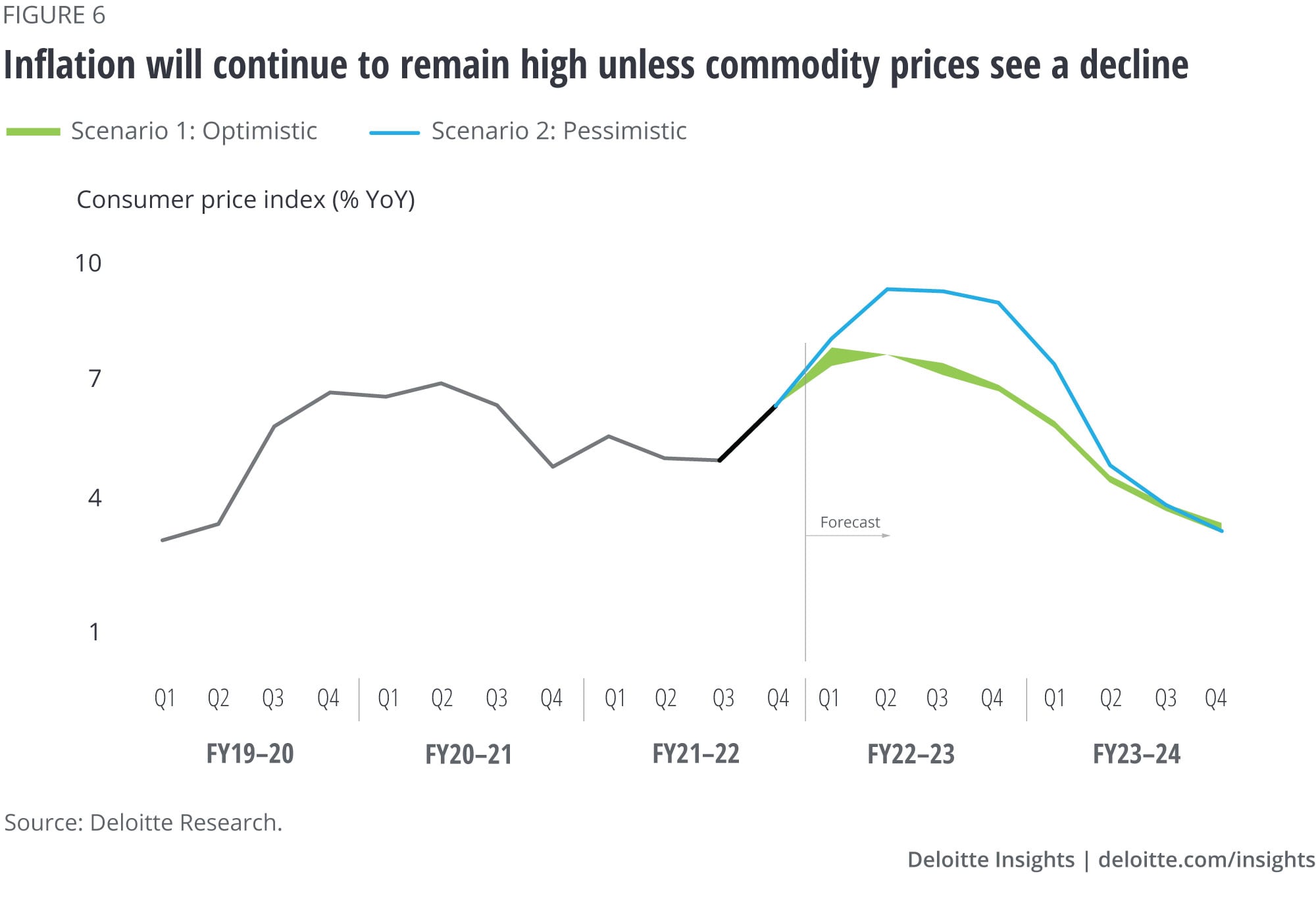

That said, we expect inflation to remain stubbornly high despite rate hikes in FY22–23 unless the global slowdown causes oil and commodity prices to fall (figure 6).

The domestic currency recovers some lost ground against the US dollar, but not before early next year. India’s relatively strong recovery and global slowdown improve INR’s strength. The fiscal deficit deteriorates marginally because of higher subsidies (for fertilizers) and reduced excise duty revenues from oil. However, there are no long-term implications on the government’s consolidation targets as higher tax collections and returns from capital investments partially offset the expenses.

Under the highly pessimistic assumptions, we expect the economy to experience a remarkable slowdown throughout our forecast period. Stagflation is a strong possibility under this scenario.

To conclude, it is true that uncertainties in the global business ecosystem will send crippling headwinds toward India. Inflation and supply chain disruptions will remain entrenched for some time. However, domestic demand and the desire of global businesses to look for more resilient and cost-effective investment and export destinations, among other factors, will help India ride this tide of headwinds. The optimism about India’s economic recovery, although slightly bruised, remains intact.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}