Japan economic outlook, January 2023 has been saved

Cover image by: Jaime Austin

Japan’s economy contracted slightly in Q3 2022, raising concern that the recovery that had just begun was coming to an end. However, the contraction was due mostly to a drop in net exports,1 which is hardly an indicator for the country’s domestic economy. Indeed, the strength of import growth is a sign that domestic demand remains reasonably strong.

Looking ahead, real GDP growth should return to positive territory. A full unwinding of pandemic-related restrictions has unleashed pent-up demand for consumer spending. Unfortunately, high inflation2 is quickly eroding household purchasing power. As pent-up demand fades and the reality of weaker inflation-adjusted wages sets in, the economy will grow only modestly in 2023.

On the policy front, economic conditions are becoming slightly tighter. The Bank of Japan (BoJ) has allowed some government bonds to trade at higher yields.3 However, the central bank is likely to keep its policy highly accommodative. Above-target inflation is mostly due to strong food and energy prices, which buys the central bank more time to keep rates low. Plus, as a global slowdown takes hold, the yen will likely appreciate, which will create disinflationary pressures. Fiscal policy, meanwhile, will likely tighten as policymakers look to fund their defense policies with tax hikes.

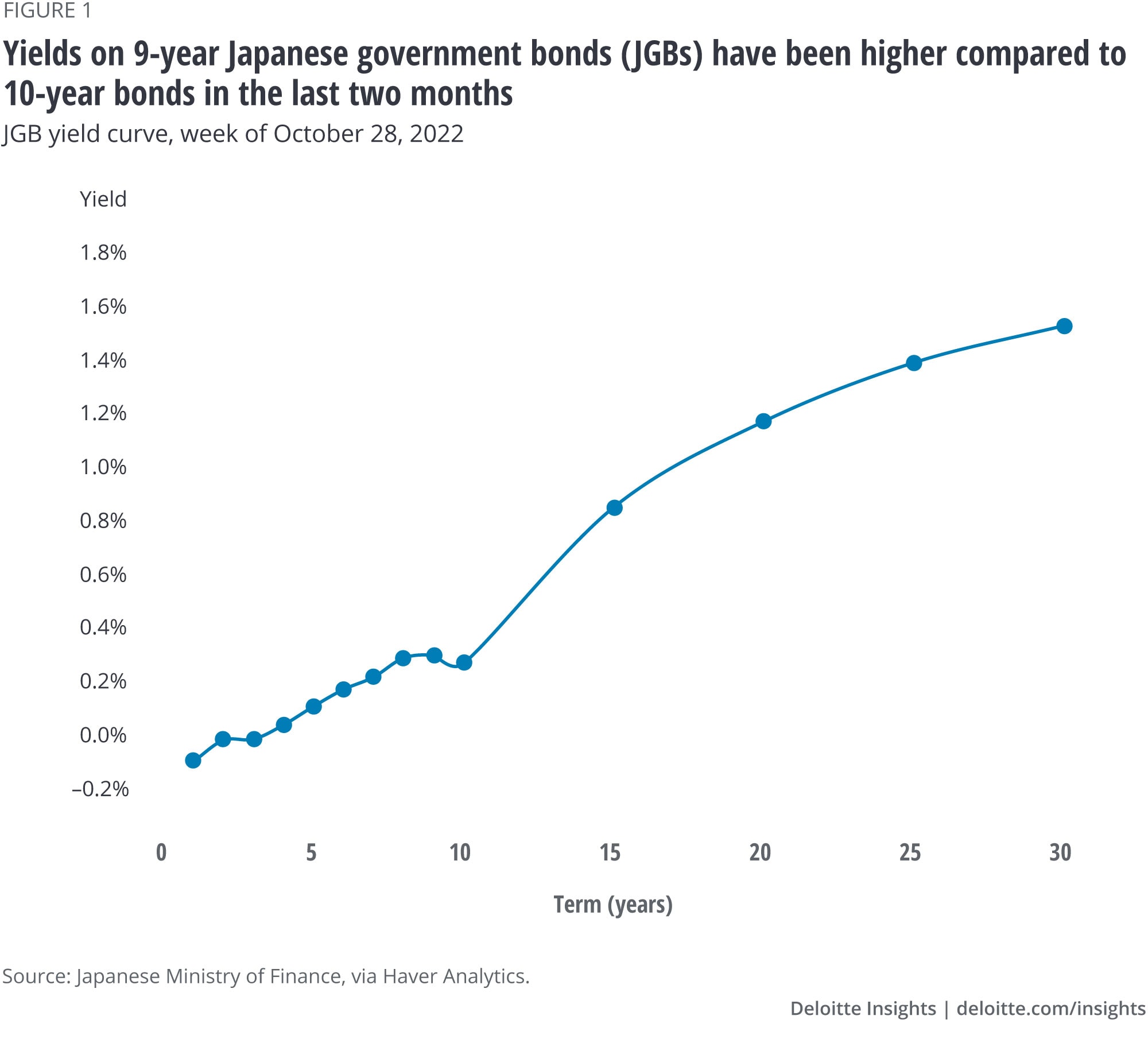

The BoJ had been the only central bank to maintain its loose monetary policy stance in the face of higher inflation across the globe. However, in December, the central bank widened the band of its yield curve control (YCC) policy. Previously, the BoJ had targeted the 10-year Japanese government bond (JGB) yield to be between –0.25% and +0.25%, but now the yield will be allowed to float 25 basis points higher or lower.4 Although Governor Kuroda insisted that this is neither a rate hike nor does it spell an end to the YCC policy, it does represent a modest tightening in monetary policy.5 The 10-year bond yield was clearly facing upward pressure prior to the central bank’s announcement. For example, yields on 9-year JGBs, which are not targeted by the BoJ, have been repeatedly higher than the 10-year yield over the past two months (figure 1).6 This inversion of the yield curve indicates that market interest rates are higher than what the central bank is targeting at the longer end of the yield curve.

The macroeconomic effects of the policy change have mostly been felt through the exchange-rate channel. The Japanese yen had already appreciated a little against the US dollar in the weeks leading to the BoJ decision. After the surprise change in policy, the yen appreciated further, from approximately 132.2 to 131.1—a more than 4% appreciation in a single day (figure 2).7 Where the yen goes from here will depend on how US central bank policy and Japanese inflation evolve. As of December 20, 2022, financial markets expected the Fed to pivot, or reduce rates, before the end of 2023 despite Federal Open Market Committee members’ insistence to the contrary.8 Should a Fed pivot become more likely, then the yen will appreciate further.

With headline inflation running at 3.8% year over year in October,9 it may seem that the BoJ ought to raise interest rates. Other major central banks delayed tightening policy as they mistook inflation to be more transitory than it really was. Some goods prices are showing clear signs of acceleration. Furniture and household utensils prices, for example, were up 6.9% from a year earlier, a marked jump from the 3.9% rate a year ago in July. Apparel prices are also accelerating and running 2.5% higher than a year earlier.10

However, the BoJ is unlikely to hike rates this year. Western core inflation, which excludes food and energy, was up just 1.4% from a year earlier in October.11 Plus, the level of western core prices is merely back to where it was before the pandemic. Inflation in some expenditure categories will be short-lived.12 Communication inflation was strong in October, but prices are coming off a very low base and remain roughly 30% below where they were when the pandemic hit, thanks to a policy change to mobile phone charges. For most major expenditure categories, inflation remains benign. Price growth for rent, medical care, education, and culture and recreation is firmly below 2%.13

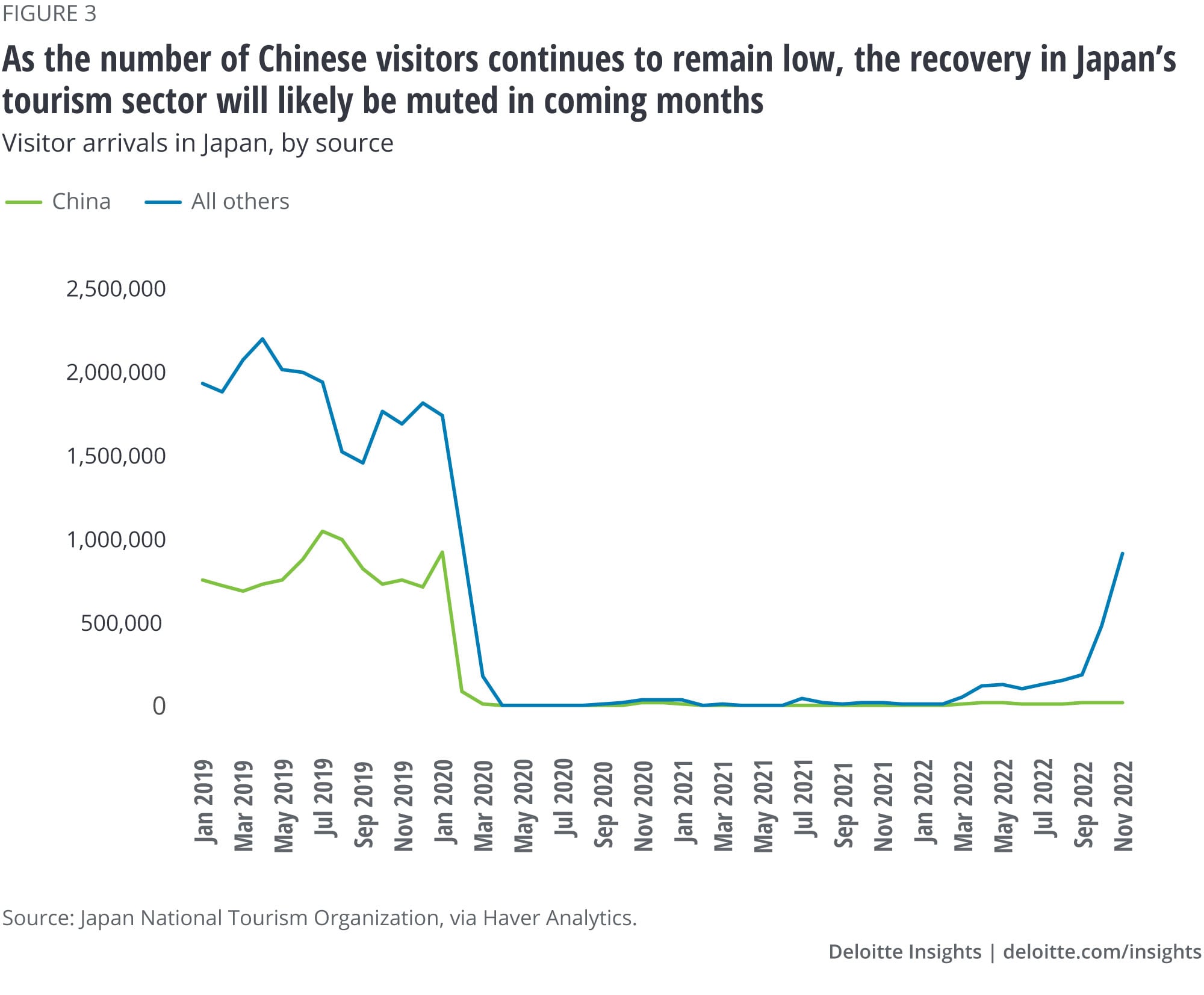

The few services that are posting strong inflation are mainly related to restaurants and travel,14 which are now seeing a rebound in demand after pandemic-related restrictions were more fully loosened. Although this could ultimately drive headline and core inflation higher, the gains may prove to be short-lived. Domestic tourism has certainly rebounded, and more foreign visitors are entering the country than at any time since the pandemic hit. However, there is still a long way to go before the tourism sector achieves a full recovery.

Domestic consumers are seeing the prices of basic goods rise quickly, which is eroding the value of their wages and limiting how much they can spend on tourism or other discretionary items. Indeed, after adjusting for inflation, wages at establishments with five or more workers were down 2.6% from a year earlier in October. At establishments with 30 or more workers, inflation-adjusted wages were still 1.5% lower than a year ago.15 Larger companies are likely able to boost wage growth, but smaller companies have slimmer profit margins, which have only gotten smaller in the last two quarters. Given that about 60% of Japan’s workforce is employed by small- or medium-sized businesses,16 most workers are unlikely to receive substantial pay increases in the near term. This bodes ill for discretionary consumption.

As domestic demand growth remains muted, the recovery in foreign tourism will likely remain incomplete. Japan relies heavily on Chinese foreign visitors (figure 3). Although China has abandoned its zero-tolerance COVID-19 policy recently, including quarantine requirements for those entering the country from abroad, outbound tourism is likely to remain muted. A surge in COVID-19 infections will prevent some would-be Chinese tourists to stay home. High infection rates will also limit the capacity of Chinese airports as workers become sick and are forced to stay home. Plus, not everyone will be willing to travel internationally immediately. For example, in November 2022, Japan received 84,300 visitors from the United States, which is well above the 1432 visitors in November 2021 but still a long way off from more than 148,993 visitors in November 2019.17

Policymakers have grown increasingly concerned about the rising geopolitical tensions in the region. As a result, Japan’s defense budget for FY2023 is expected to reach 6.8 trillion yen, which would be significantly higher than the previous fiscal year.18 Moving forward, the government plans to spend more than 8 trillion yen per year to ramp up its military capabilities, bringing defense spending to 2% of GDP by 2027.19 Such spending levels would be in line with NATO member commitments.

Funding such a sizable rise in defense spending has proved controversial. Almost 65% of the Japanese public disapprove of raising taxes to fund additional military spending.20 Without higher revenue or lower spending, Japan will face higher debt levels. Already, Japan’s general government-debt-to-GDP ratio is nearly 250%, well above that of other major economies (figure 4).21 Should interest rates shift materially higher, deficit spending could make Japan’s debt situation much worse.

Despite the public disapproval of the tax raise, revenue will likely need to come from somewhere. A rise in corporate taxes will likely be a popular choice for policymakers. Nonfinancial corporations are sitting on a relatively large pile of cash. Cash or cash equivalents amounted to 180% of GDP in Q3, the highest in at least 40 years.22 Plus, profit margins for some of the largest Japanese companies are firmly above prepandemic levels, thanks in part to a weak yen creating a windfall for those selling in foreign currency.23 At the same time, those earnings have not translated into much stronger wage growth. Corporations posting strong profits and holding large sums of cash are likely to make them an easy target for policymakers looking to raise revenue.

A fully funded rise in defense spending will prove to be modestly contractionary. Although higher taxes will be met with higher expenditures, some of those funds will be used to purchase foreign weapons.

In the nearer term, Japan’s economy will continue to grow, albeit modestly. Pent-up demand and a rise in travel should allow consumer spending to eke out gains. However, slow wage growth amid relatively high headline inflation will keep spending restrained. Monetary policy should also remain accommodative, which will add another layer of support to growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}