{kind=link}

{kind=link}

Japan has been saved

Cover image by: Jaime Austin

Japan’s economic recovery in 2020 was relatively strong. By Q4, real GDP was down just 1.2% from a year earlier, thanks to a rebound in consumer spending and ample foreign demand.1 By comparison, real GDP in the United States and European Union was down 2.4% and 4.8%, respectively.2 However, the strong start to the recovery was upended this year as the pandemic worsened. Despite a mild COVID-19 outbreak relative to the Americas and Europe, infections in Japan were on the rise at the beginning of 2021,3 which prompted the government to issue another state of emergency for 11 prefectures, including Tokyo.4 As a result, economic activity in Q1 likely contracted. As Japan waits for more vaccines to be distributed, domestic demand will likely remain sluggish into the summer, though accelerating growth in the rest of the world will provide support for Japanese exporters. In the second half of the year, however, growth will accelerate, thanks to sizable fiscal stimulus at home and abroad.

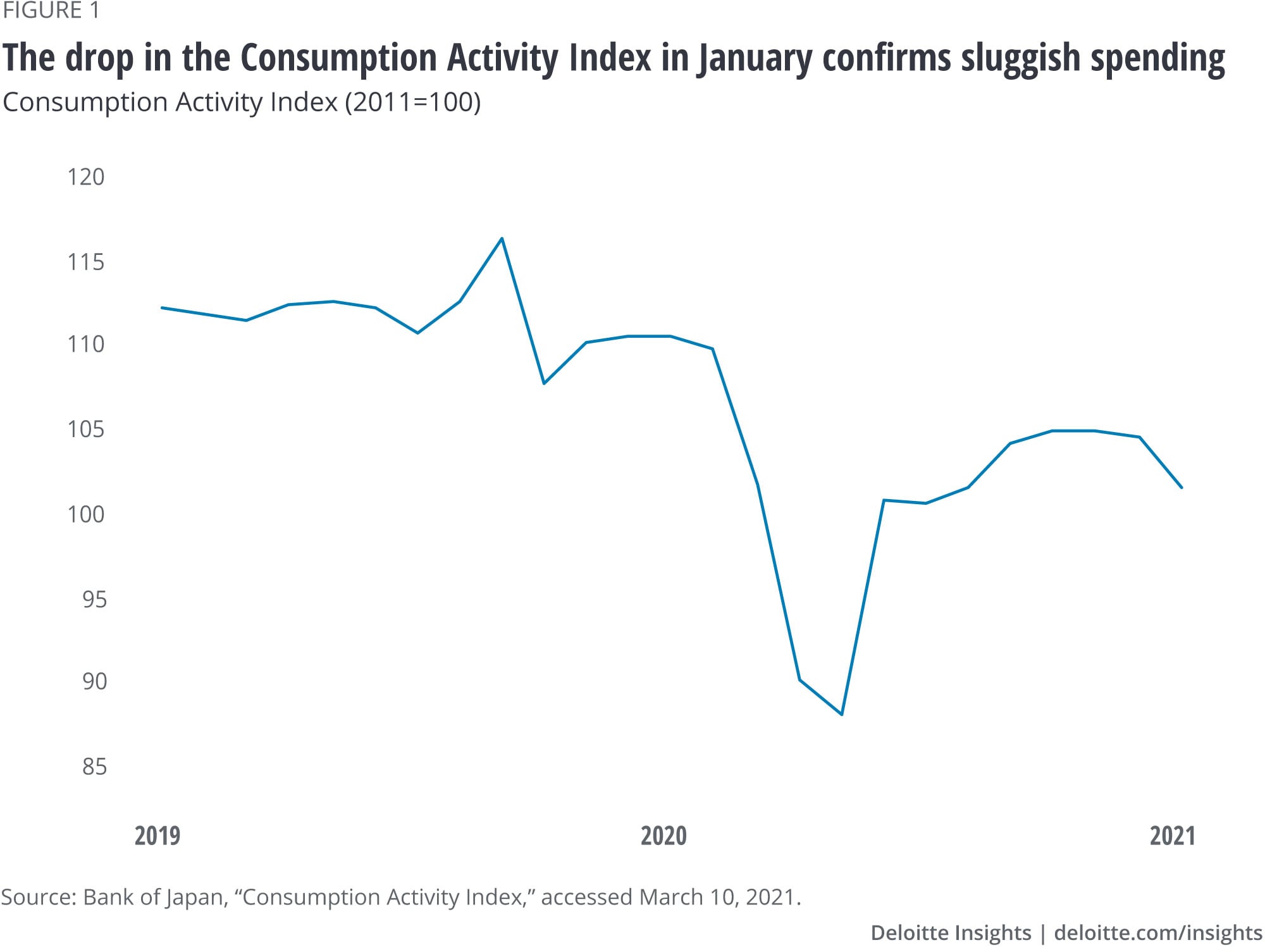

Japan’s faltering growth was evident in January when the Consumption Activity Index fell 2.8% from December (figure 1).5 Similarly, the decline in year-over-year (YoY) retail sales worsened in January.6 In an effort to curb the spread of the virus, the government suspended its travel subsidy that had encouraged more domestic tourism and related spending toward the end of 2020. The subsidy suspension, rising infection rates, and a new state of emergency together caused mobility near retail and recreation establishments to plummet in January. By February, infection rates had slowed down again, and mobility had picked up, though it remained firmly below where it had been in the fall.7

Although consumer spending will likely rebound in Q2, the pace of growth is expected to remain sluggish. The biggest constraint to growth is the lack of available vaccines. Japan’s vaccine approval process, which requires more clinical trials than many other countries, delayed the start date for vaccination.8 The tentative timeline for vaccination suggests that the general population will not even have access to vaccines until July.9 Meanwhile, the state of emergency for the Tokyo area was extended to March 21 to allow hospital bed occupancy to come down further.10 Moreover, the incidence of infections caused by new and more contagious variants of the virus is on the rise in Japan,11 which adds to the risks of in-person economic activity while the population waits on a vaccine. The mobility numbers in February were strikingly similar across Japan’s prefectures regardless of whether they were under a state of emergency,12 suggesting that Japanese residents may remain cautious even as lockdown restrictions are eased. Risk of another wave of infections caused the government to exclude foreign spectators from the Summer Olympics in Tokyo,13 which will deprive the country of a boost to consumer spending it had previously anticipated.

Several other factors are likely to restrain consumer spending in the near term. Despite a low unemployment rate of 2.9%, average cash earnings in December were down 3.2% from a year earlier, the worst contraction in 12 years.14 In addition, this year’s shunto, the annual wage negotiation, is unlikely to yield much in terms of pay increases. One poll shows that roughly two-thirds of companies plan to keep wages flat or make cuts amid low profitability and an uncertain future.15 Moreover, the travel subsidy will not be immediately renewed when the state of emergency ends for Tokyo, removing a key support to growth that was available at the end of last year. Although consumer confidence rebounded from January, it was still 11.8% lower in February relative to a year earlier, which bodes ill for additional spending.16

One of the largest tailwinds to Japan’s economy has come from abroad. Prior to December, Japan posted 25 consecutive months of YoY declines in goods exports (figure 2). In January this year, though, goods exports were up 6.4% from a year earlier, accelerating from a 2.0% gain in December.17 Exports to China and the rest of Asia were particularly strong. Some of that strength is due to the timing of the Lunar New Year, which limits economic activity in China.18 In 2020, the holiday was in January, but this year, it was in February, distorting the YoY comparisons. Export growth would still have been strong without this quirk in the calendar. For one, Japan posted double-digit year-ago export growth than Asian countries, such as India, Malaysia, and Thailand, where the Lunar New Year is not a highly celebrated event. Second, goods exports to China were still up 10.4% YoY in December when the timing of the Lunar New Year should have understated export growth. Rising export sales have in turn supported the manufacturing industry, with the Purchasing Managers’ Index jumping to 51.4 in February, its highest reading since December 2018.19

In the United States, a large stimulus package and a relatively rapid vaccine rollout have improved the economic outlook, which is expected to support exports from Japan to the world’s largest economy. Although Japanese exports to the United States weakened in January, the United States likely supported Japan’s strong export growth indirectly. The US current account deficit fell to its lowest point in more than a decade in Q3 2020,20 the most recent data point available, and the trade deficit continued to widen through January 2021, suggesting that the widening of the current account deficit continued into this year. At the same time, China,21 the European Union,22 Japan,23 Australia,24 and India25 all posted surpluses. The implication here is that the United States is absorbing global surpluses and acting as the ultimate buyer of Japanese exports.

One challenge for Japan’s exports is the global shortage of semiconductors. Automakers around the world, including those in Japan, have cut production as they are unable to obtain the semiconductors they need to keep up with demand.26 As a result of these struggles in the auto industry, Japan’s motor vehicle and parts exports dropped 4.6% in January from a year earlier. The semiconductor shortage could continue for the rest of the year, which will further restrain Japan’s motor vehicle production and exports.27 However, there is a silver lining for Japan. Semiconductors and their machinery make up a substantial portion of Japan’s exports, amounting to a little more than half the value of motor vehicle and parts exports. Surging exports of semiconductors and their machinery, which were up 24.7% from a year ago in January, more than offset the decline in motor vehicle and parts exports. The decline in auto exports may ultimately outweigh the rise in semiconductor exports, but the chip shortage will not be all bad for Japan’s trade balance.

Economic growth should accelerate as the country moves into the second half of the year. More vaccines are part of the story, but the government has also provided an impressive amount of fiscal stimulus—amounting to roughly two-thirds of annual GDP—since the pandemic hit.28 Part of the most recent package will go toward directly stimulating the economy, such as extending the travel subsidy once it is deemed safe to do so. Plus, previous stimulus measures raised last year’s household savings to their highest point since 2017, which should offset at least some of the decline in wage growth. Policymakers are still considering another stimulus package, which would boost growth further.29

The largest portion of the most recent stimulus package will go toward structural changes aimed at boosting the postpandemic economy.30 Digitalization and carbon neutrality by 2050 are two of the key policy initiatives. Digitalization, which would include moving more government services online and expanding access to 5G technology, has the potential to raise much-needed productivity growth and attract private investment. Carbon neutrality, on the other hand, has the potential to raise Japan’s trade balance as it is currently a net importer of energy commodities. Nonetheless, both initiatives will likely take years to yield notable results.

Monetary policy could become looser as well. The Consumer Price Index fell 0.6% from a year earlier in January.31 The Bank of Japan (BoJ) underwent a policy review in mid-March to assess its policies aimed at avoiding a deflationary spiral where prices and wages move lower in tandem. That may prove difficult given that the BoJ’s policy rate currently stands at –0.1%. Although some central banks, such as the Swiss National Bank, have lower policy rates, a lack of bank profitability in Japan has prevented the BoJ from lowering rates further. The policy review provided the BoJ with a scheme to limit the downsides of a negative interest rate policy, but the changes were relatively small.32 One former BoJ official believes the central bank may be using the policy review to find ways to lower rates without eroding bank profitability. However, Japan’s deflation may ultimately reverse course on its own. Indeed, the BoJ’s governor, Haruhiko Kuroda, stated that deflation was due to temporary factors. Although Japan is likely to escape deflation, the BoJ does not expect to reach its 2% inflation target until 2024.33

The BoJ’s expectation around inflation highlights the challenges that Japan’s economy faces. The pandemic will hold down output as most consumers remain understandably cautious while the risk of infection remains relatively high. However, unprecedented stimulus measures at home and abroad are expected to boost GDP growth in the second half of the year. Structural reforms may do little for growth this year but have the potential to raise productivity and the trade balance in the longer run.