Deloitte's autumn edition of the European CFO Survey finds companies focusing on cost-cutting - and exploring how generative AI can help them

The mood of Europe's CFOs has become less positive since the spring as elevated inflation and tighter monetary policy weighs on their businesses. Cost-cutting is a major focus and generative AI appears on the horizon, but its adoption is not yet very advanced in Europe.

Richard Muschamp

Rolf Epstein

Dr. Pauliina Sandqvist

Ram Krishna Sahu

The Autumn 2023 edition of the Deloitte European CFO Survey reveals that the mood of Europe’s CFOs has deteriorated in the last six months. In the spring edition of the survey, Europe’s CFOs were cautiously optimistic, assuming business conditions would improve after a winter that had proven not as bad as expected. Over the course of the year, however, businesses in Europe have had to deal with persistently high inflation and rising interest rates. The momentum of the global economy has also weakened, with China’s economic recovery proving a disappointment so far. The manufacturing sector has been struggling globally and services have started to feel the pain too. Europe still faces the huge geopolitical challenge presented by Russia’s invasion of Ukraine. Altogether, the economic climate in Europe is subdued and the outlook fragile. Inflation is expected to decline further, but the pace at which it will fall is unclear. Tight monetary policy will probably restrain growth in coming months.

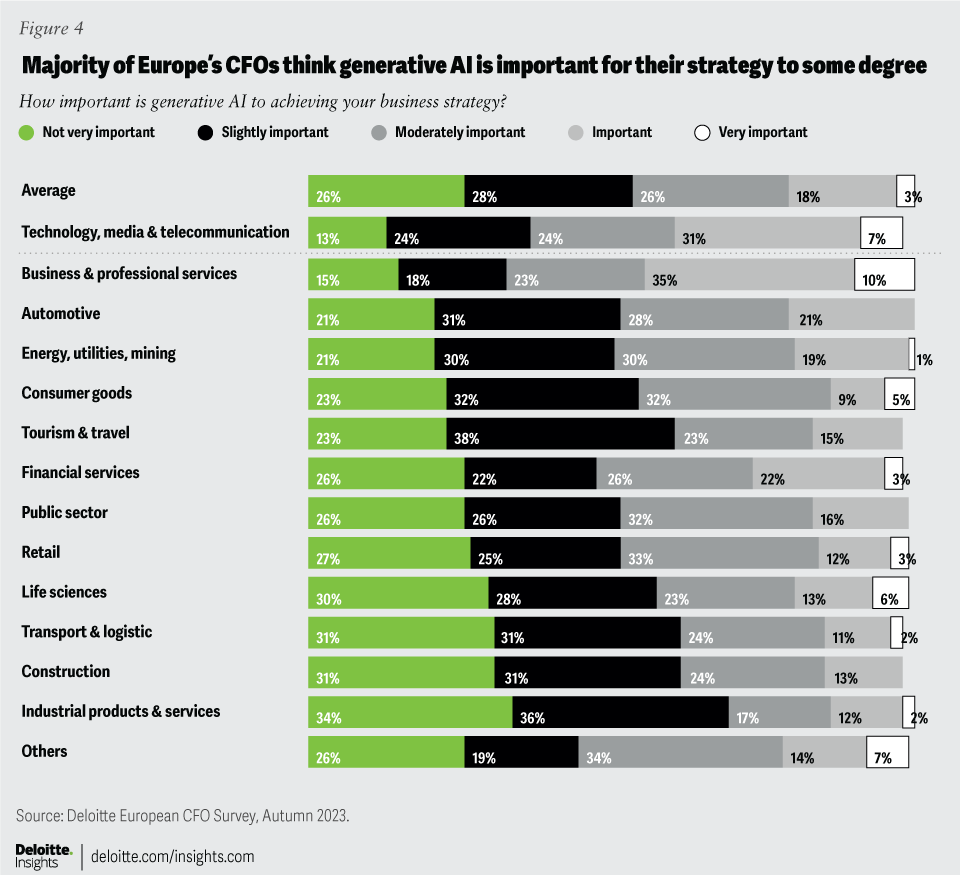

However, a difficult macroeconomic environment is not the only challenge Europe’s CFOs currently face. There is also the question of what to do about generative AI. For this edition of the European CFO Survey, we asked our panel their views on generative AI, what they are doing now, and what they think are the benefits and barriers. About a year after ChatGPT was launched, three out of four financial executives in Europe think that generative AI is to some degree important for their strategy. However, its adoption has not yet gone very far. Few European businesses have already implemented it, though many are experimenting with it. European CFOs see generative AI as having clear potential to reduce costs, boost efficiency and make better forecasts as well as improve customer experience. But they are having difficulty finding professionals with the skills to use generative AI to its fullest potential. In already tight labour markets, talent acquisition may prove to be a bottleneck holding back adoption of generative AI in Europe.

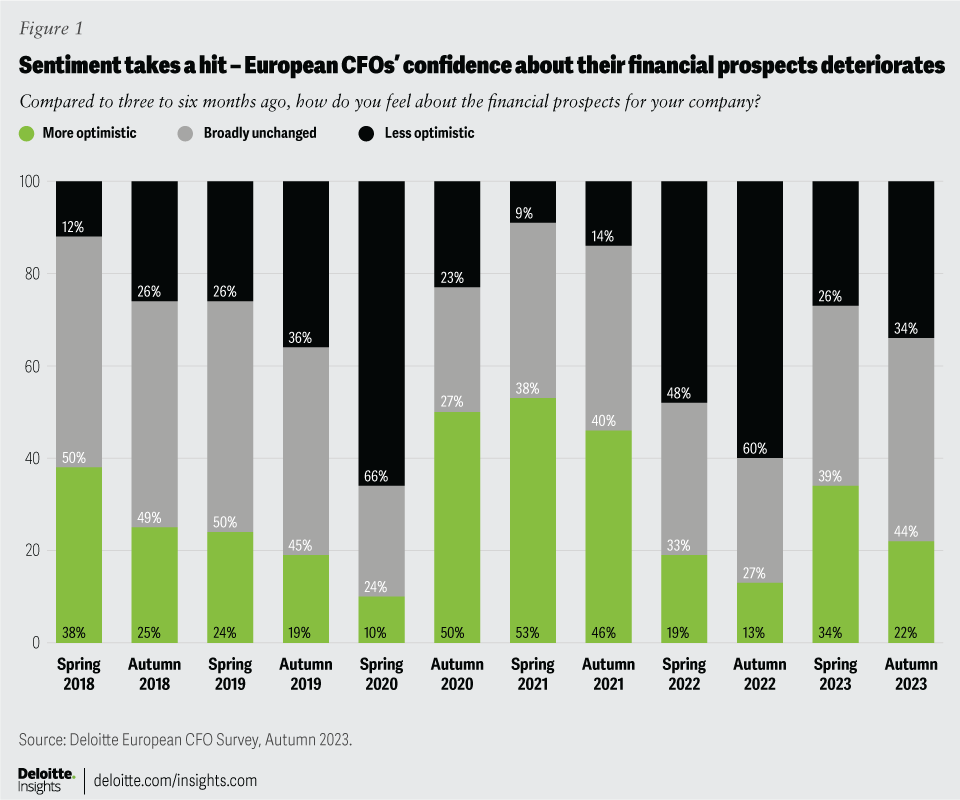

Sentiment takes a hit

Europe’s CFOs have become much less positive about their current financial situation. The net balance of business sentiment has declined since our spring survey from +8 per cent to –12 per cent, as 34 per cent of the CFOs surveyed are less optimistic than before and only 22 per cent are more optimistic (figure 1). The gloom is greater in larger companies: Financial executives from medium-sized (with revenue between 100 and 999 million euro) and large (more than 1 billion euro) companies are less optimistic than their peers in smaller enterprises (less than 100 million euro). The most notable fall in confidence was reported in Germany and Austria, with German growth hurt by struggling manufacturing industry, especially weak automotive and energy-intensive sectors, among other things.

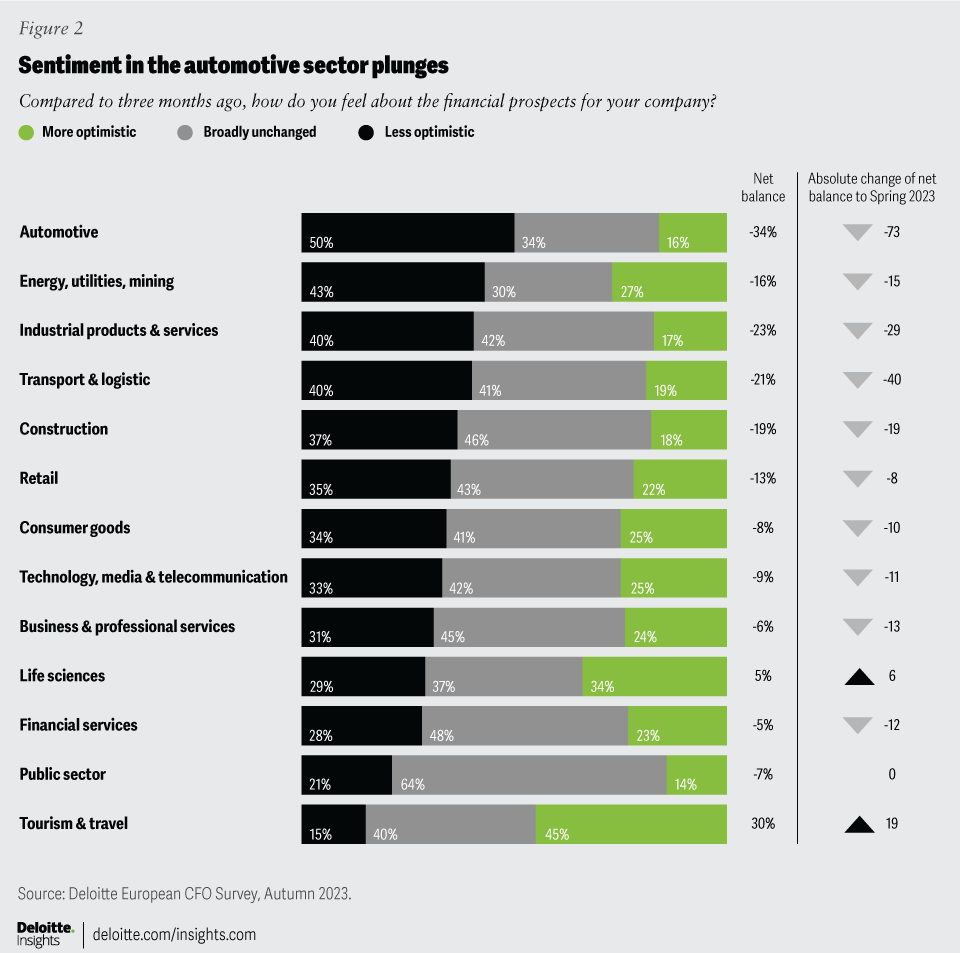

At the sector level the mood has changed most dramatically in the automotive industry (figure 2). Six months ago, automotive CFOs were more confident than their peers in other industries. Now they are the most pessimistic. Surging energy and labour costs are troubling European car companies and geopolitical tensions are affecting exports adversely. By contrast, the optimism of CFOs in tourism and travel has risen further. The postpandemic recovery in travel is continuing and does not seem to have been adversely affected by the cost-of-living crisis so far.

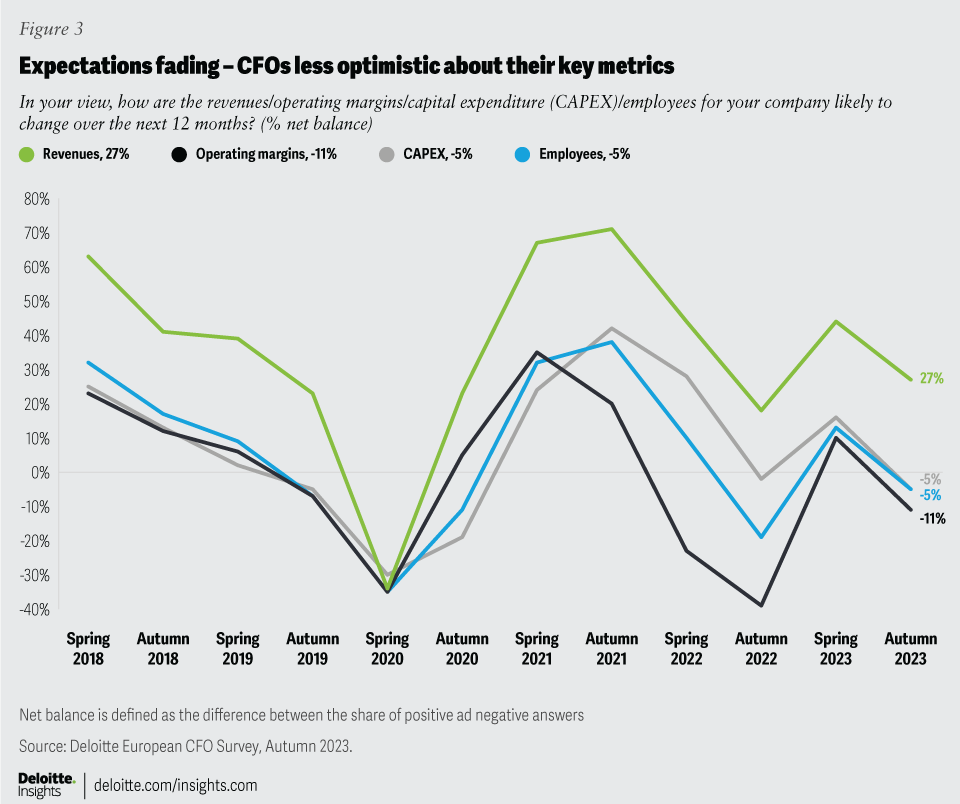

Expectations fading

CFOs’ hopes for the near future have also faded. While CFOs on balance remain optimistic about future revenues, the share of CFOs expecting revenues to increase in the next 12 months fell from 63 per cent to 53 per cent (figure 3). Executives in Germany, Italy and Portugal have revised down their revenue expectations radically.

Looking at sectors, automotive is alone in expecting decreasing revenues, suggesting that the hard times for the automotive industry will not be over soon. In the construction industry, high financing costs are taking their toll and CFOs expect only a small increase in revenues. On the other hand, financial executives in more service-oriented industries like business and professional services, and tourism and travel, as well as life sciences, expect their revenues to keep growing strongly over the next 12 months.

In the current high-cost environment the outlook for operating margins has worsened too. Over the coming 12 months, more CFOs expect operating margins to decrease rather than increase. The downward shift has mostly been driven by companies in the United Kingdom and Germany. CFOs in Denmark and Ireland are still relatively optimistic.

Not surprisingly, the lowest expectations are in the automotive and transport and logistics sectors, where high energy and labour costs are proving a major drag. But financial executives in life sciences remain quite optimistic about their operating margins.

Investment and employment to decrease as poor economic prospects weigh

CFOs across the continent agree that the economic outlook is the main risk for their business over the next 12 months. As a result, they have become more cautious about their capital expenditure and recruitment plans. For both key metrics the net balance has turned negative, pointing to small decreases in investment and employment over the next 12 months – reinforcing the poor outlook for Europe’s economic growth.

The gloomier mood is concentrated in the automotive sector, where CFOs have revised down their views for capital expenditure and employment drastically. Other industries remain more positive. In tourism and travel as well as the public sector, CFOs are planning to further expand their capital expenditure. The public sector too intends to take on more staff over the coming year. Firms in business and professional services are also still looking to recruit.

But the worsening in Europe’s current economic picture and its prospects is reflected in a reinforcement of the shift in CFOs’ strategic priorities that began to be evident a year ago—they are focusing on cost reduction. This shift to a defensive strategy is easy to understand: Europe’s CFOs, just like its consumers, are responding to the cost-of-living crisis by tightening their belts.

Generative AI enters Europe’s businesses

Generative AI is, in the view of Europe’s CFOs, one way in which they might achieve cost reductions – and they see this as one of the chief benefits of the new technology. A majority of corporates in Europe judge generative AI to be relevant for their strategy with almost half of CFOs stating that it is moderately to very important (figure 4). Only 26 per cent of survey respondents believe that generative AI will not be very important in achieving their business goals. Geographically, there is a divide. Financial executives in Austria, Spain and Ireland are convinced that generative AI represents an important advance. CFOs in Italy and Denmark think it not that important for their business strategy. From a sector point of view, too, there are great differences in the assessment of the relevance of generative AI. A majority of CFOs in technology, media and telecommunications as well as in business and professional services report that generative AI is at least moderately important to them, while their peers in industrial products and services and transport and logistics feel generative AI is currently not very relevant to their strategy.

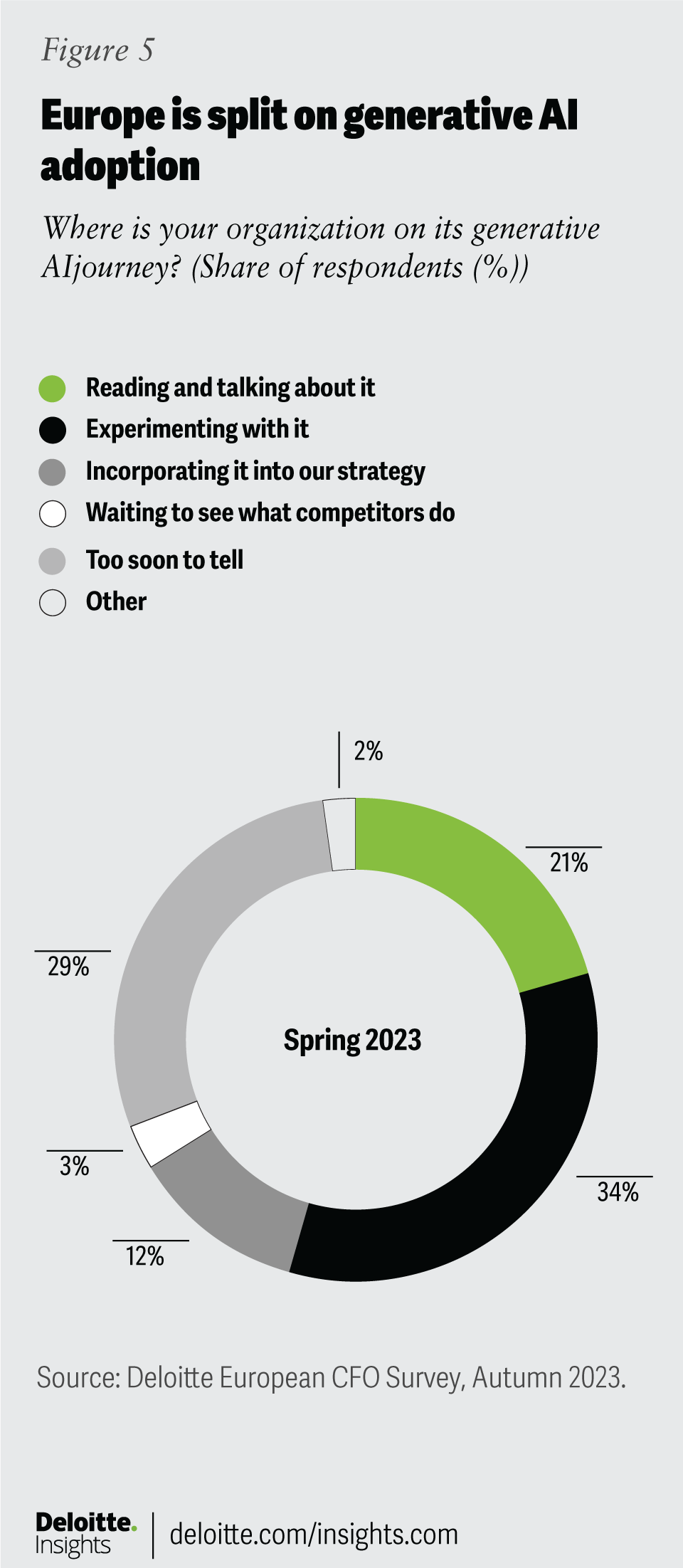

Many European corporates are pushing ahead with adoption in their businesses but so far most have not departed that far from the starting blocks (figure 5). The furthest advanced are the 12 per cent that are incorporating generative AI into their strategy. Meanwhile, more than a third report that they are experimenting with generative AI, one-fifth are currently reading about it and discussing it, while 29 per cent think it is still too soon to tell how they will adopt the technology. In general, one should keep in mind that generative AI is still quite a new technology, which is quickly developing further, and this makes assessment of it and preparation of an action plan challenging.

Businesses in Austria, Germany and Finland seem to be leading the way in adoption of generative AI in Europe while companies in Sweden, Poland, Italy and Denmark are less advanced. US companies, however, seem to be one step ahead of their European peers. The results of the Deloitte CFO Signals™ Q3 report indicate that 15 per cent of US corporates are incorporating generative AI in their strategy while 42 per cent are experimenting with it.

In Europe, businesses in the technology, media and telecommunications sector seem to be at the forefront of generative AI, with 30 per cent already incorporating it into their strategy, followed by business and professional services firms (25 per cent). At the next tier down, experimenting with generative AI, corporates in the retail industry (52 per cent) and in consumer goods industry (45 per cent) are leading the way.

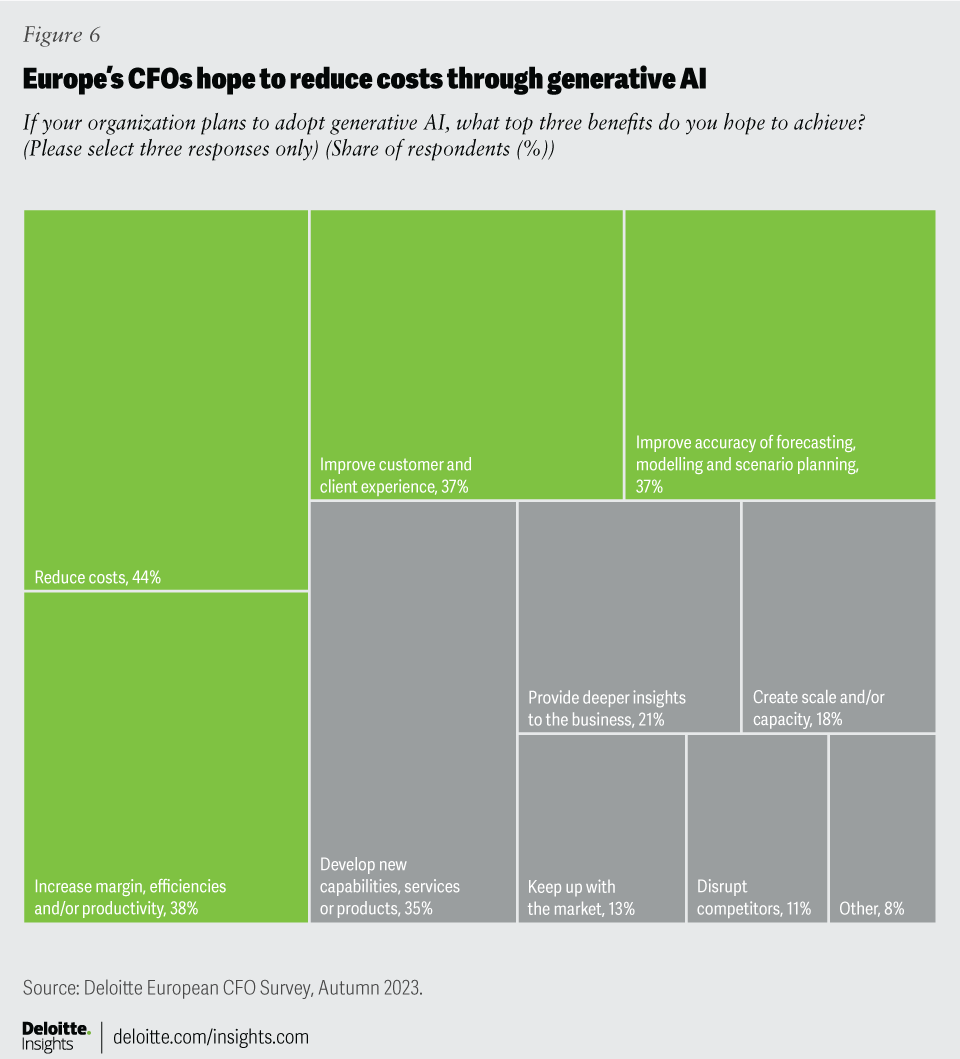

European CFOs who are already converts to generative AI are looking to it not just for cost reduction but also as a means to improve the accuracy of their forecasts, modelling and scenario planning, and to increase margins, efficiencies and productivity, and improve the customer experience (figure 6). In other words, many European businesses see generative AI as holding the promise of better all-round business performance in the future. Read more about key business-ready use cases for generative AI here.

One reason for the slow adoption of generative AI may be the lack of human and technological resources. Sixty-four per cent of CFOs report that talent, resources and capabilities are the main barriers to adopting and deploying generative AI. Businesses are having a hard time finding professionals with the right skills. Data and technological resources are also an issue for many respondents (42 per cent), next to privacy and security issues (35 per cent).

Overall, the investment in generative AI by European businesses is still relatively modest. The majority (67 per cent) expect to allocate less than 1 per cent of their organisation’s budget to generative AI over the next year. Almost one-third of companies are committing more and planning to spend up to 5 per cent of their budget already. Again, corporates in business and professional services as well as in technology, media and telecommunications are more ready to spend on generative AI.

Conclusion: A difficult winter foreseen, again

The autumn picture is both clear and gloomy. Europe’s CFOs see a challenging winter ahead. Inflation is still elevated and interest rates at levels that are, historically, normal rather than particularly high, but from the rock bottom, near-zero rates of the previous decade and a half. Consumers are struggling with spiralling costs, and CFOs face the same problem: they too are now focusing on major efforts to reduce costs – rather than planning to invest, hire staff and expand. As was the case last autumn, when the Ukraine conflict brought Europe the threat of energy shortages, CFOs are uneasy about the winter that lies ahead and about the risks to economic growth. Their mindset is therefore cautious.

With generative AI, many see the potential to help them reduce costs and improve their business performance in general. Yet, most are still in preparation mode. If competitors find benefits in using generative AI and steal a march on them, they will be swift to join the new trend – provided they can find staff with the knowledge required. If generative AI expands rapidly, competition for the respective skills will become intense.

Would this winter, like the last one, prove less difficult than feared? That might be possible if inflation falls, interest rate hikes cease and consumers spend more freely than expected. An end to the Ukraine conflict and an alleviation of geopolitical tensions generally would also help, but the latest developments in the Middle East are a discouraging setback. As was the case this year, the spring may see CFOs in a more positive mood. Much will depend on how consumers and the economy as a whole weather the impact of the inflationary shock of the past year.

About the Deloitte European CFO Survey

Deloitte has conducted the European CFO Survey since 2015, giving voice twice a year to senior financial executives from across Europe. The data for the autumn 2023 edition was collected in September 2023 and reflect responses from 1,213 CFOs in 14 countries and across a wide range of industries.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}