But Europe has now got through its feared winter without shortages, thanks mainly to unusually mild weather and energy-saving measures. Economic activity has therefore held up better than expected. Labour markets have remained robust, or even tight. And firms are in much better shape than their own CFO outlooks had foreseen. But this is not to say that all is now rosy.

The continuing war and geopolitical risks in general, fears about the economic outlook, labour shortages and high inflation, and labour costs are very much on the mind of Europe’s CFOs in the spring of 2023. As this latest edition of the Deloitte CFO Survey shows, a majority of them do nonetheless foresee growth in their revenues, and they intend to hire more staff, though not on a major scale. Their optimism is cautious, tempered by a sense that uncertainty remains elevated, with geopolitical and economic risks persisting.

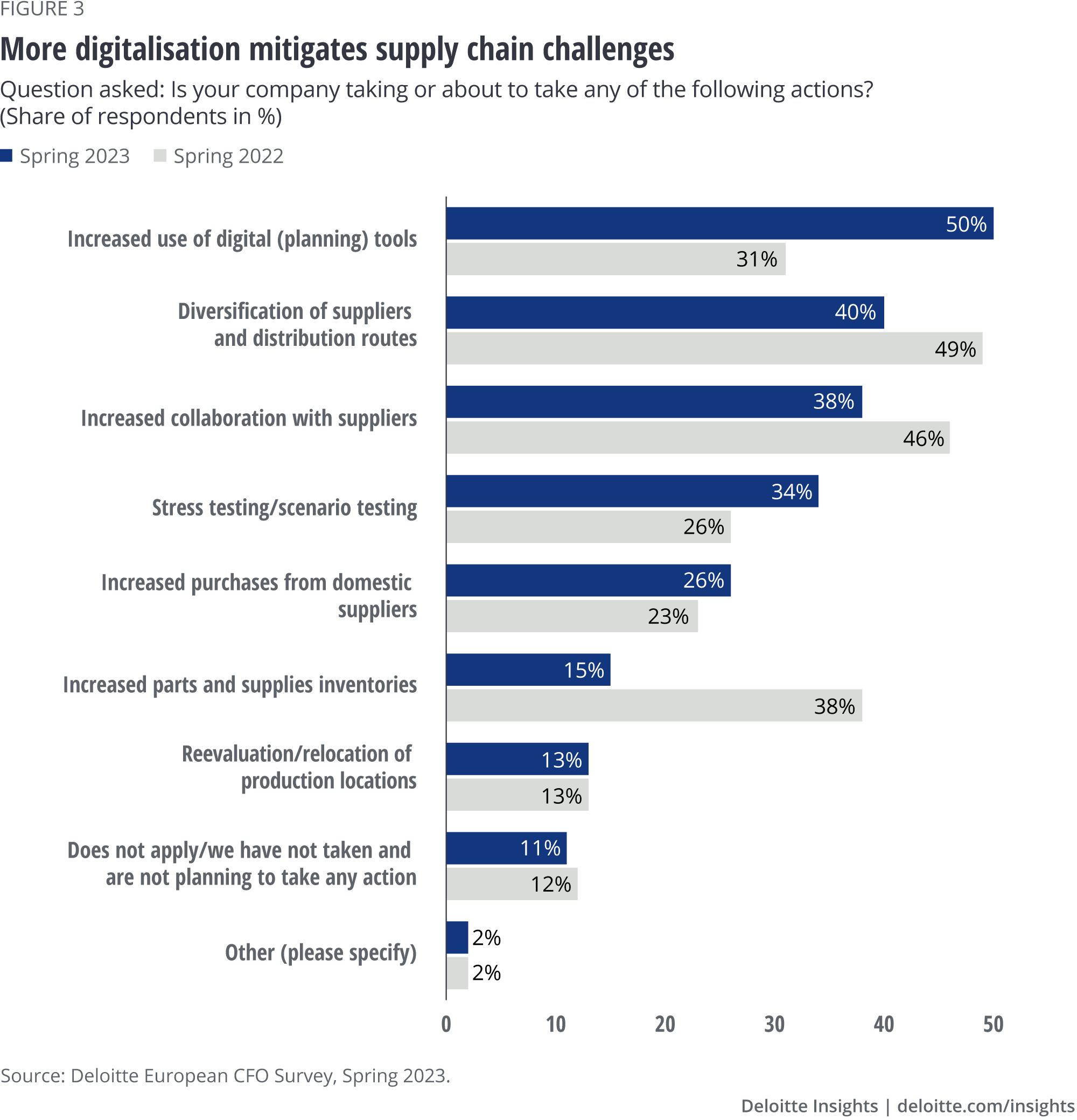

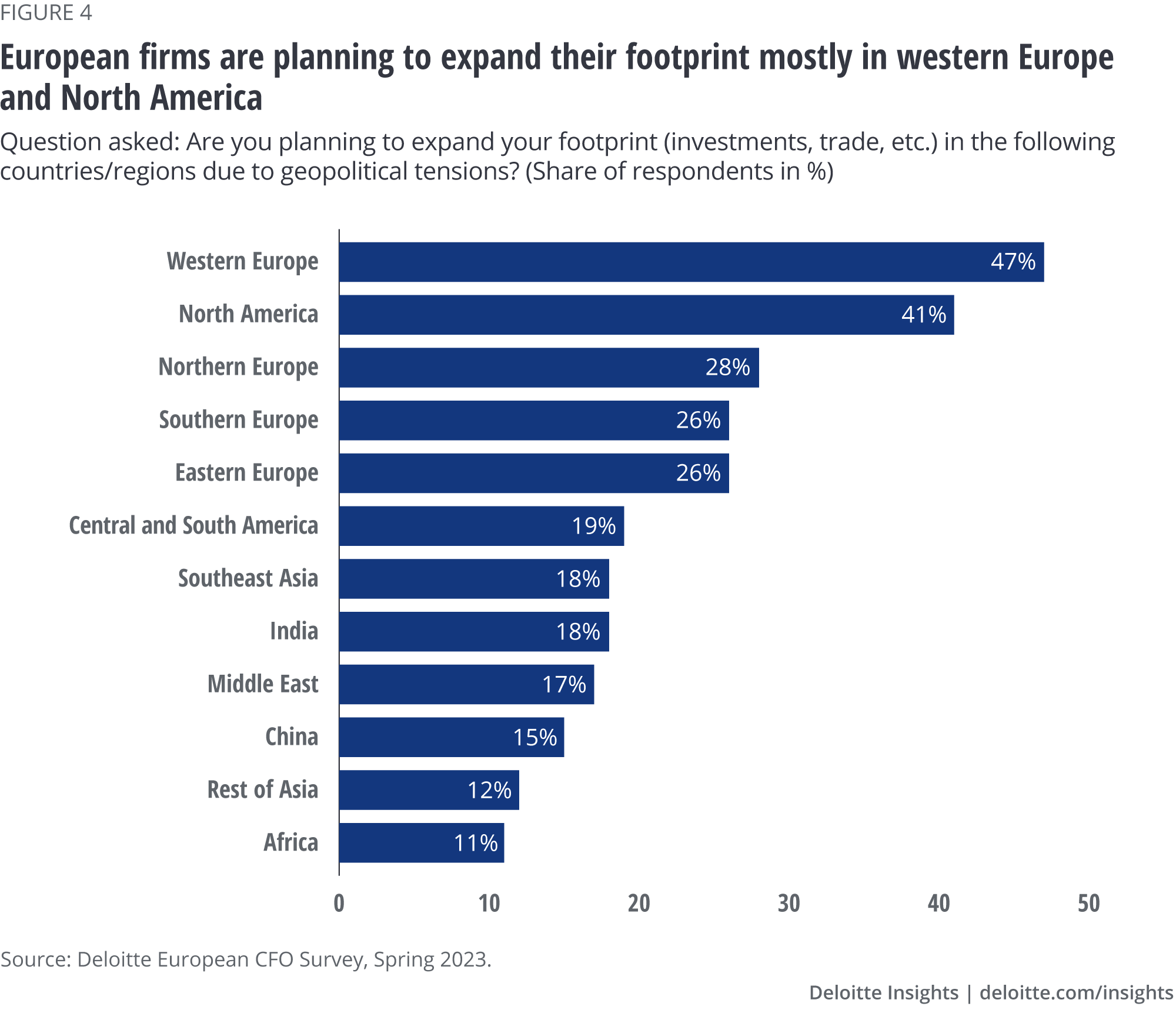

They also remain preoccupied by dealing with the serious difficulties that emerged in 2022. Europe’s CFOs are taking increasingly profound actions to make their supply chains more resilient, such as by using more digital tools rather than simply relying on increased inventories. As CFO priorities show, European firms are also planning to expand their footprint, mostly in western Europe and North America – not in regions in which they now tend to see greater risk.

From gloom to slight optimism

According to Deloitte’s European CFO Survey for Spring 2023, European firms have become far less anxious about their financial prospects than in the autumn and, on average, are mildly optimistic (figure 1). The net balance, the difference between the share of positive and negative responses, of CFOs feeling more confident about the financial prospects for their companies rebounded to +8% from the extremely gloomy –48% in autumn 2022. But the shift in mood is not all-encompassing: more than a quarter of firms remain pessimistic.

Business confidence in Europe has greatly improved because the winter disaster they expected did not happen. Russia’s invasion of Ukraine had provoked fears that heating for Europe’s homes and fuel for its factories might be limited during the winter. But the unusually mild weather conditions combined with more efficient use of energy and better energy supply than expected means that the much-feared rationing did not take place. Now Europe’s CFOs have turned to be more confident, but their optimism is tempered by a degree of caution.

Nor are all countries ready to embrace the somewhat better mood. Deep pessimism prevails in Norway (–32%), where consumers are reluctant to spend due to high inflation and interest rates, and CFOs worry about weaker growth. And in Sweden (–12%), Italy (–6%) and Turkey (–5%) too, CFOs’, on balance, continue to lack confidence in their companies’ financial prospects.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}