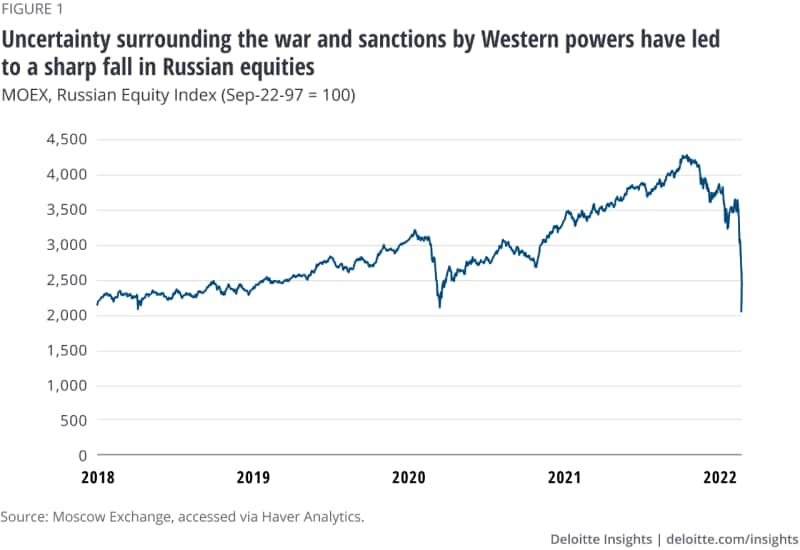

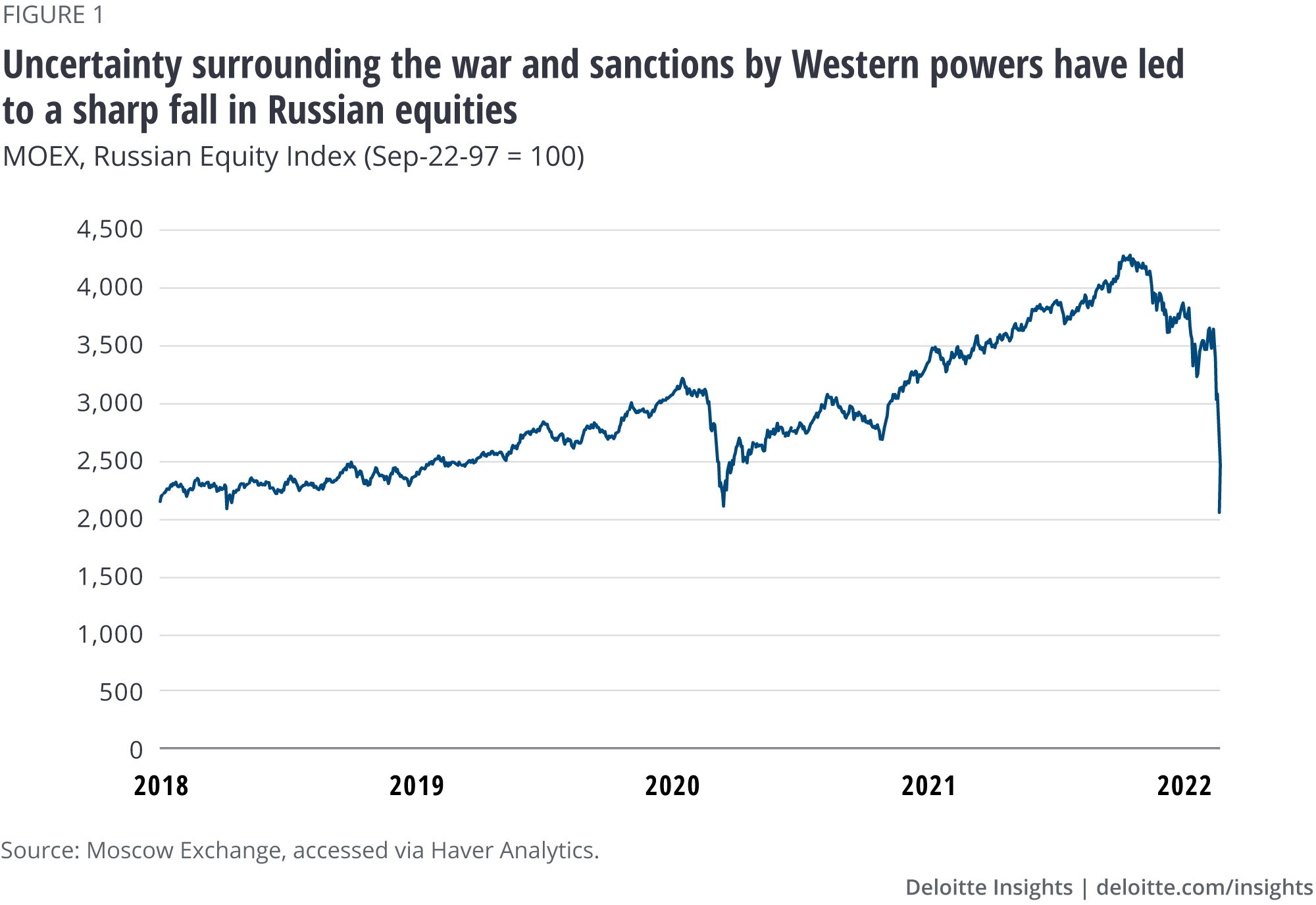

Impact on Europe

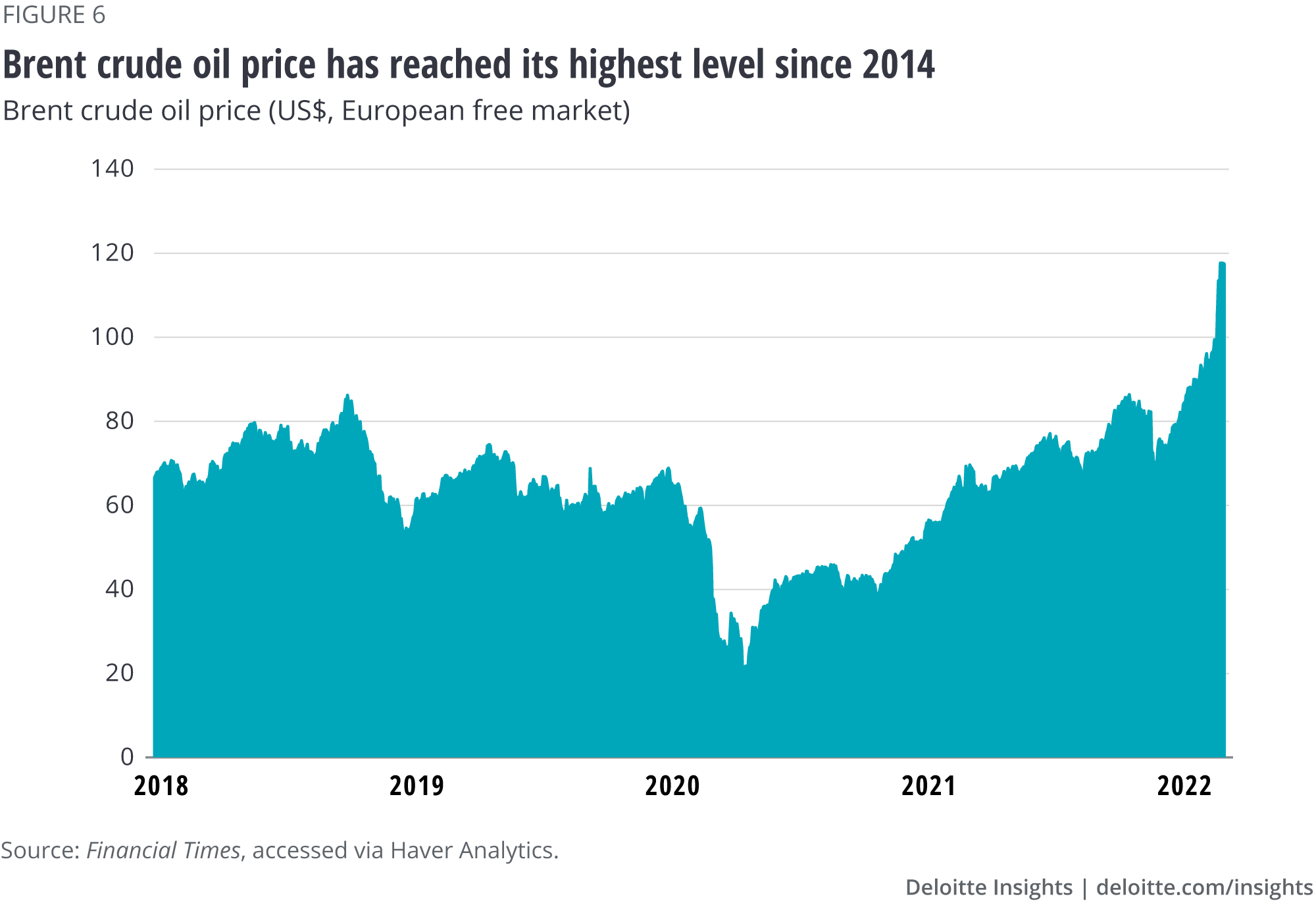

Russia only accounts for 4.8% of EU trade,23 which is down from 9.3% in 2012, and 2.3% of German trade. Ukraine only accounts for 1% of EU trade. Russia’s annexation of Crimea in 2014 accelerated a long-term reduction in Russia’s importance as a trading partner for Europe.24 However, EU trade with Russia is strongly concentrated in energy. Russia accounts for 40% of EU gas imports, 25% of oil imports, and 47% of imported solid fuels.25 If there were to be a complete shutdown of Russian gas, there would likely be bottlenecks in several European countries, including Germany, stemming from difficulties in distributing alternative sources of energy.

With the help of its well-developed gas infrastructure, Europe will initially be protected from supply shortfalls. How long it can avoid serious disruption depends on available LNG imports, storage levels, and the development of alternative sources. Any shortfall of supply would lead to higher prices and, consequently, higher inflation in Europe. Moreover, prolonged disruption of supply could have a negative impact on growth. Plus, uncertainty could weigh on consumer and business sentiment in Europe. Private households, meanwhile, have built up significant excess savings during the pandemic,26 thereby providing a buffer against declining economic activity.

Impact on the United States

Trade between the United States and Russia or Ukraine is relatively insignificant compared to the size of either economy. The principal channel through which this crisis might affect the United States is the impact on the price of oil and the prices of some key commodities. In addition, if the crisis has a significant negative impact on the European economy, that could spill over into the United States because of the extensive trade between the United States and Europe. Moreover, Russia and Ukraine are major producers of commodities that are important in the production of semiconductors and batteries. If Russian and/or Ukrainian exports of these commodities were to be curtailed, the global price would rise and shortages could ensue, thereby hurting some US industries, adding to inflation, and reducing potential output.

Impact on Asia/Pacific

Trade between Asia and Russia is modest, with Russia providing some oil and gas to China and Russia importing electronic and information technology products. This trade is not likely to be severely disrupted, but it could be affected by the need for trading companies to stay clear of sanctions. Plus, as a net importer of energy, Asia is vulnerable to sharp rises in the prices of energy and other commodities.

Concluding thoughts

Uncertainty about how the war will transpire, whether more sanctions will be imposed, and how Russia might respond to existing or potential sanctions will play a role in determining the economic impact of the war. Uncertainty elevates commodity prices and risk premia. It also increases the cost of doing business and likely delays important business investment decisions. In the days, weeks, and months to come, the direction of commodity prices and the prices of financial assets will evolve in ways that, hopefully, will enable businesses to make informed decision.

Beyond the economic impact of this war, it appears likely that the geopolitical framework of Western Europe is rapidly evolving. There could be a sizable increase in government spending on defense, raising questions about taxes and spending priorities. In addition, the fact that energy is at the root of the potential economic impact suggests that a larger debate about energy policy is likely to ensue. This could mean investments in diversifying sources of carbon-based fuels, as well as intensifying investments in clean energy. Finally, as of this writing, we are witnessing a disruption of supply chains for some commodities and increased stress in global financial markets. The war raises questions about the continuation of globalization and about the ability of any country to act against the wishes of the international community with impunity. These are issues that will be vigorously debated in the months and years to come.

Still, one cannot help but feel that we have entered a new era. Analysts have offered numerous historical analogies, many of which involve heightened tension and weakened global trade and cross-border investment patterns.27

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}