Is the writing on the wall for buildings? Business investment since COVID-19 has been saved

Cover image by: Jaime Austin

Some of the longer-term business implications of the COVID-19 shock are beginning to become clear. Business investment suffered a very short-term decline in the first half of 2020, but then bounced back. Or rather, some categories of business investment bounced back; others not so much. And, unfortunately for businesses and workers involved in those types of investments, the prospects for those sectors appear poor. COVID-19’s impact is likely to put a permanent stamp on the US capital stock.

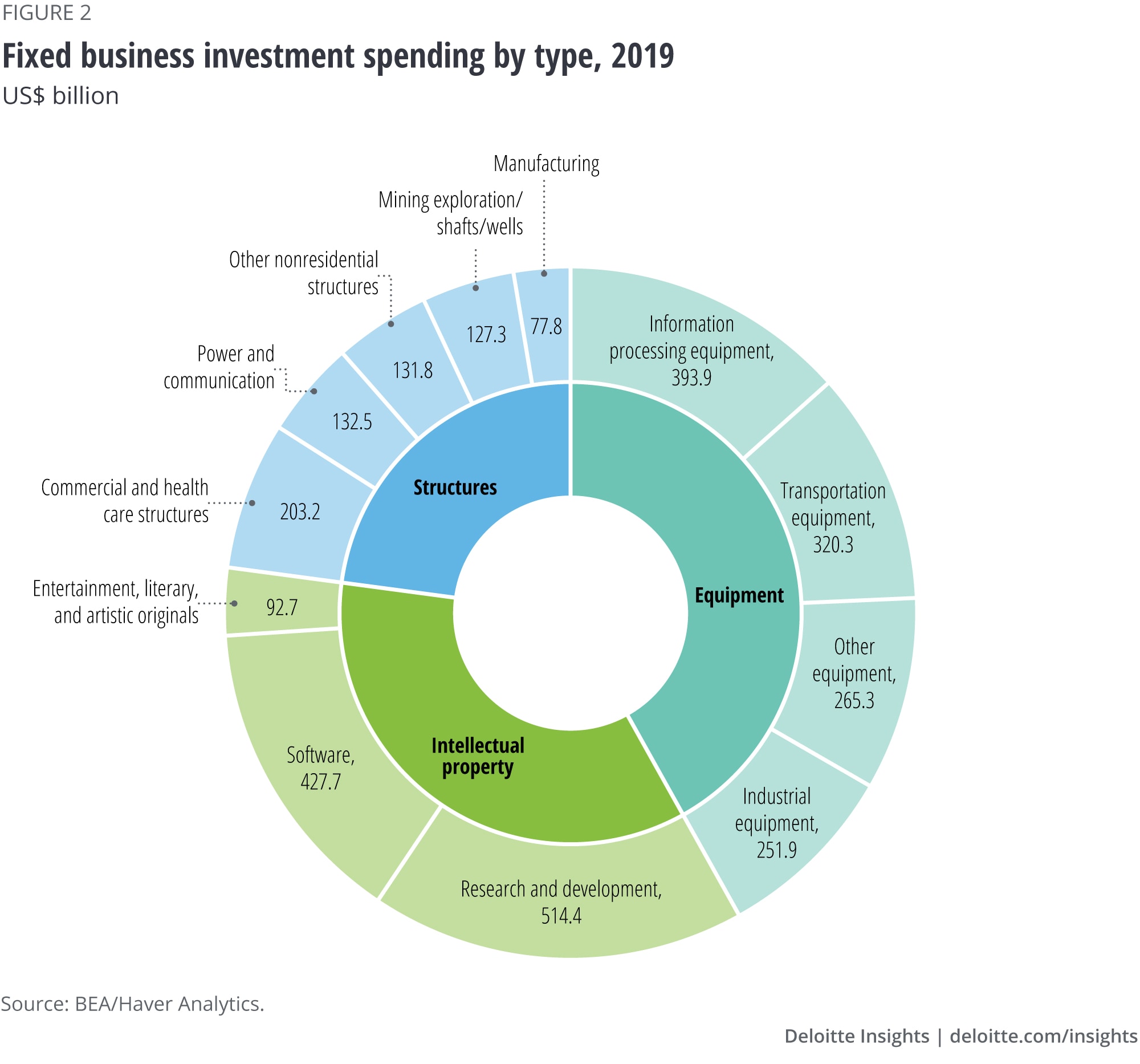

Figure 1 shows the change in the three major categories of business investment—structures, equipment, and intellectual property—since the beginning of the pandemic.

The differences among the broad categories of investment are striking. Investment in structures is down 21% from the prepandemic level. Investment in structures fell when the pandemic started—and it continued falling. In fact, it has dropped in every quarter (except one) since the pandemic started. In contrast, equipment investment is up a reasonable 5% since the start of the pandemic, and intellectual property investment jumped 12%.

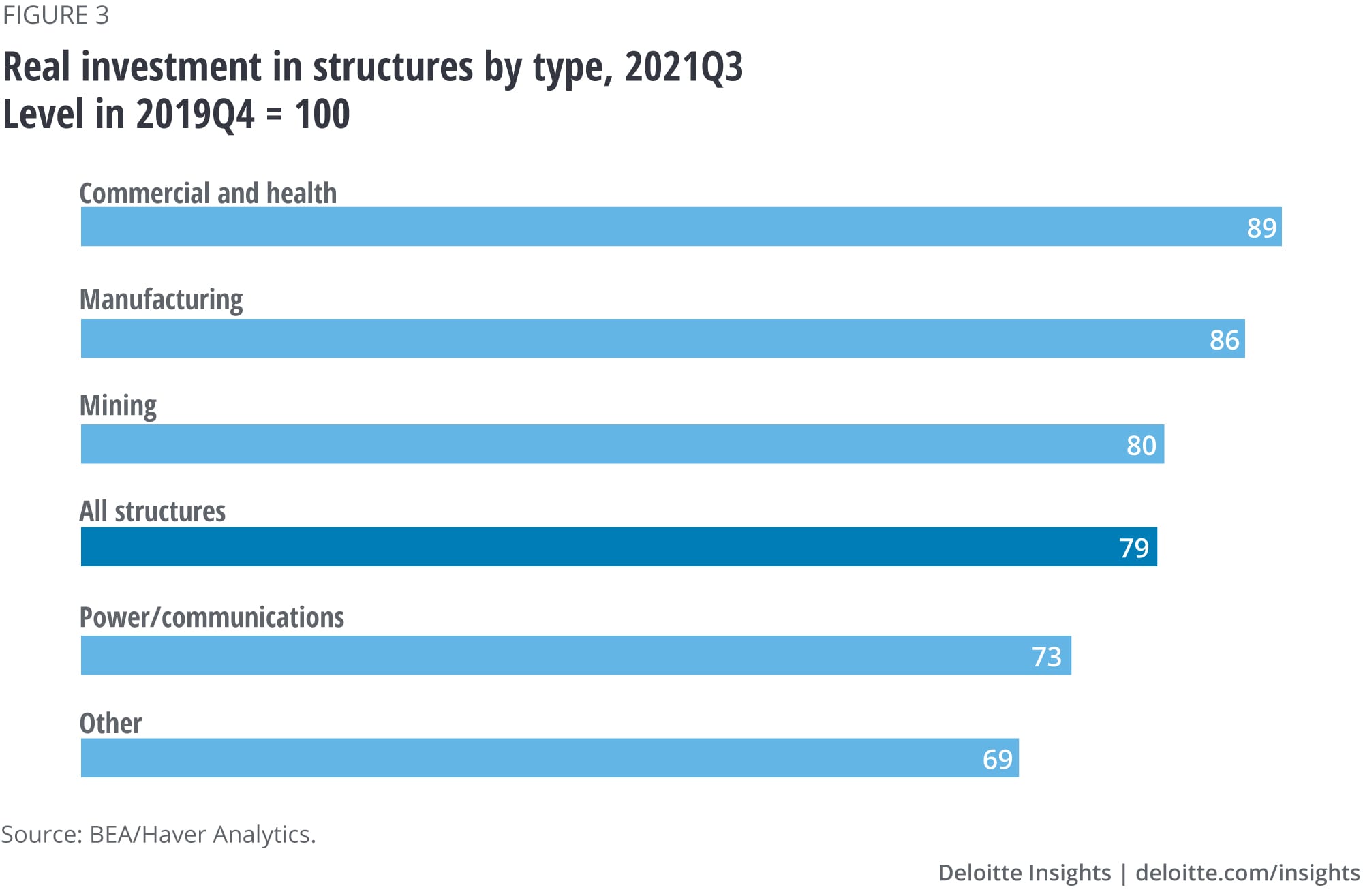

Investment in all types of structures declined during the pandemic and has continued to remain low (figure 3). Commercial and health structures appear to have experienced the smallest decline among the major categories. However, this masks significant weakness in office structures (down 20%), multi-merchandise shopping (down 31%), and food and beverage establishments (down 33%). Fast growth in the construction of warehouses offset the decline in other categories. Truth is, there is little prospect of an increase in demand for office or retail space in the near future, and construction is responding.

In contrast, the decline in manufacturing buildings looks a little odd. Manufacturing capacity utilization is now above the prepandemic level. If this continues, stretched factory production will eventually create the need for more manufacturing space—unless the surge in demand for goods that is stretching manufacturing capacity is temporary. In that case, manufacturers might be making a wise decision in not increasing building capacity now.

Mining mainly consists of energy (oil and gas) structures such as exploration rigs and follows energy prices closely. The pandemic collapsed oil prices, and although prices have rebounded, it will take some time for energy investment to respond.

Other structures include a number of categories—such as religious and educational—where construction is down for a variety of reasons (especially because of a falloff in fundraising for these mainly nonprofit institutions). This category also includes lodging, which is down 43% from the prepandemic level. Given many experts believe that business travel will fall permanently as businesses substitute increasingly effective virtual meetings and communication for face-to-face meetings, this is only prudent on the part of the hospitality industry.

The lesson is clear for many types of structures. The pandemic and the changes associated with it have reduced the need for buildings. With expectations for more virtual work and online retail in the future, and probability of less business travel, investment in structures is very likely to remain weak.

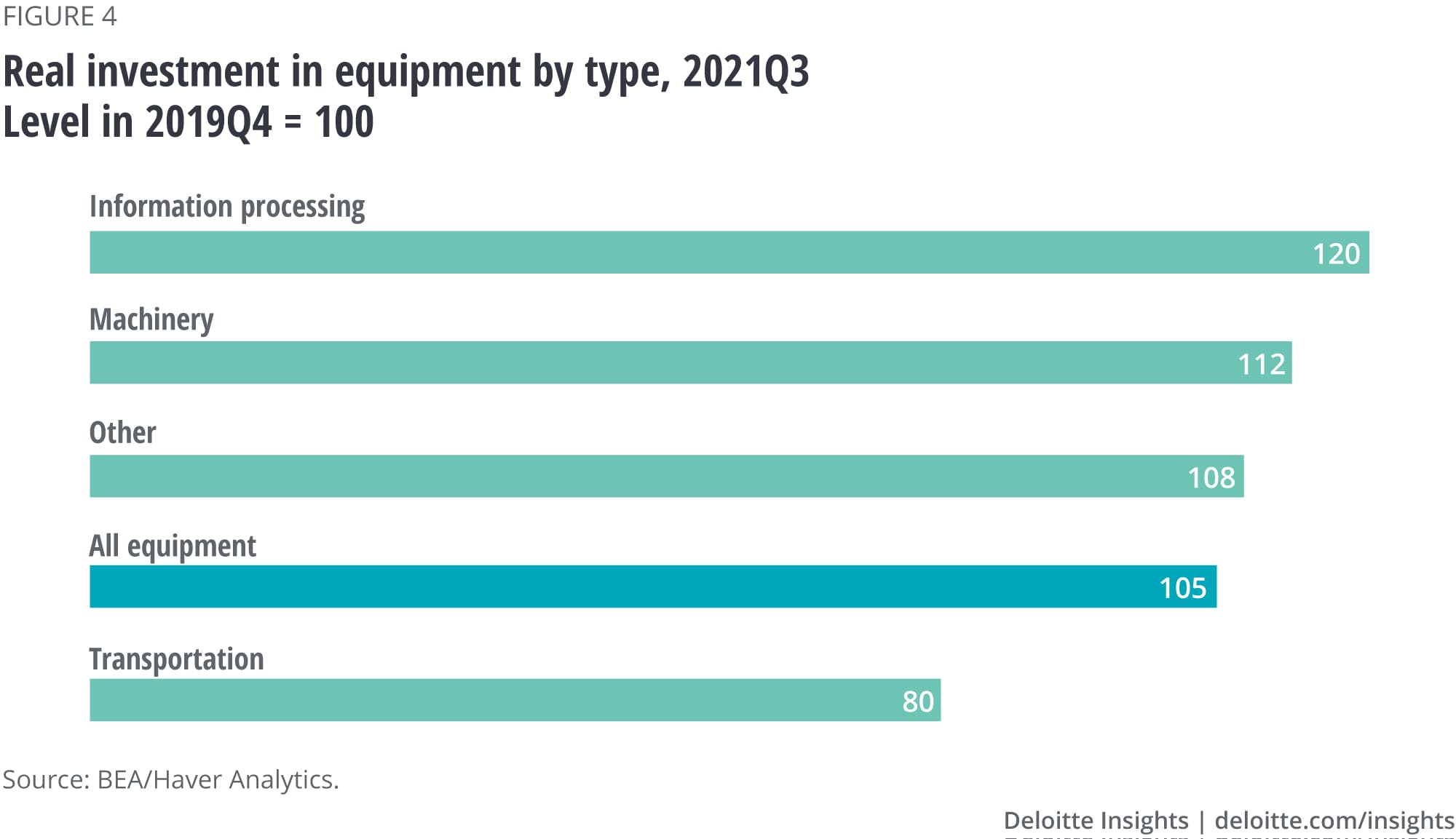

Equipment investment dropped 14% in the first half of 2021, but more than recovered over the next year. However, not all types of investment shared in the initial decline in the first half of 2020. Information-processing equipment purchases, for example, grew even in Q2 2020, when just about every other economic sector experienced a decline. This likely reflects the immediate need for such equipment as companies pivoted toward building the infrastructure necessary for remote work.

By Q3 2021, investment in information processing equipment was up 20% from the prepandemic level. This is despite a decline in the most recent quarter (Q3 2021), mainly driven by a drop in computer purchases.

Industrial equipment investment only moved above the prepandemic level in the middle of 2021. It has grown at a satisfactory—but not particularly strong—rate since then.

Transportation equipment fell by over half in the first half of 2020. It then grew for several quarters, until Q3 2021, when it fell again. As a result, it remains 20% below the prepandemic level. This is mainly due to a decline in the purchases of light and heavy trucks (down 24%), although purchases of aircrafts are (not surprisingly) still below the prepandemic level as well. The recent decline in truck purchases may well reflect the auto industry’s continuing supply chain problems. Eventually, the wider adoption of shopping and working at home is likely to strengthen demand for shipping and delivery vehicles.

Intellectual property investment took a hit in the Q2 2020, and then bounced back (figure 5). By Q3 2021, investment in intellectual property was up 8% over the prepandemic level. This was largely the result of very fast investment in software, the largest category of intellectual property investment.

After declining for one quarter (Q2 2020), software investment grew at an average annual rate of 14%, compared to 9% in the four years before the pandemic. Of course, any computer engineer knows that software investment is an important counterpart to investment in equipment; all those new computers and servers are only as valuable as the software running on them. Software investment was already growing fast, but the need to jump to remote work has pushed businesses to invest even more in software.

Investment in research and development (R&D) also showed an acceleration after the initial pandemic-caused decline, from an average rate of 5.3% before the pandemic hit in the first half of 2020 to 9.8% after. R&D (like software) may be less affected by the need to work remotely. Plus, the need for R&D may have grown—R&D is necessary to find new ways for businesses to operate and new products and services that solve problems in the changed economy.

Investment in artistic originals, a relatively small portion of intellectual property (about 9%), has failed to return to the prepandemic level. Much of that category relates to movies and television shows, which have found production challenging in the postpandemic environment. This weakness—while disappointing for consumers of entertainment, not to mention the artists involved—will not have a large impact on future economic production.

The rush to purchase goods rather than services, the move to remote work, and the increasing popularity of online shopping are upending past business models. The economy is changing. So, it’s not surprising that patterns of business investment are changing to reflect those fundamental shifts.

Changing patterns of investment will make past benchmarks for business and the economy less useful. For example, the increased share of investment in equipment and intellectual property at the expense of buildings will raise the depreciation rate of capital. Equipment (especially information-processing equipment) and intellectual property (especially software) lose market value much more quickly than longer-lived structures. Businesses with a larger share of capital invested in equipment and software will likely post faster depreciation rates for their plant and equipment (depending on the relationship between “economic” or actual capital depreciation, and accounting and tax concepts).2 It may also be necessary to write off current capital, which is no longer as valuable as it was in the past.

The changed investment patterns will also mean the substitution of people for things. The capital input for intellectual property investment tends to be lower than that for machinery or buildings, so the demand for capital may remain lower than expected for a given level of total investment. That could help put a lid on interest rates, which, ultimately, reflects the supply and demand for capital.

The “new economy” is a phrase that comes up every so often in economic history. It’s time to dust it off again: A “new economy” is a good description of the business adjustment to the postpandemic world.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}