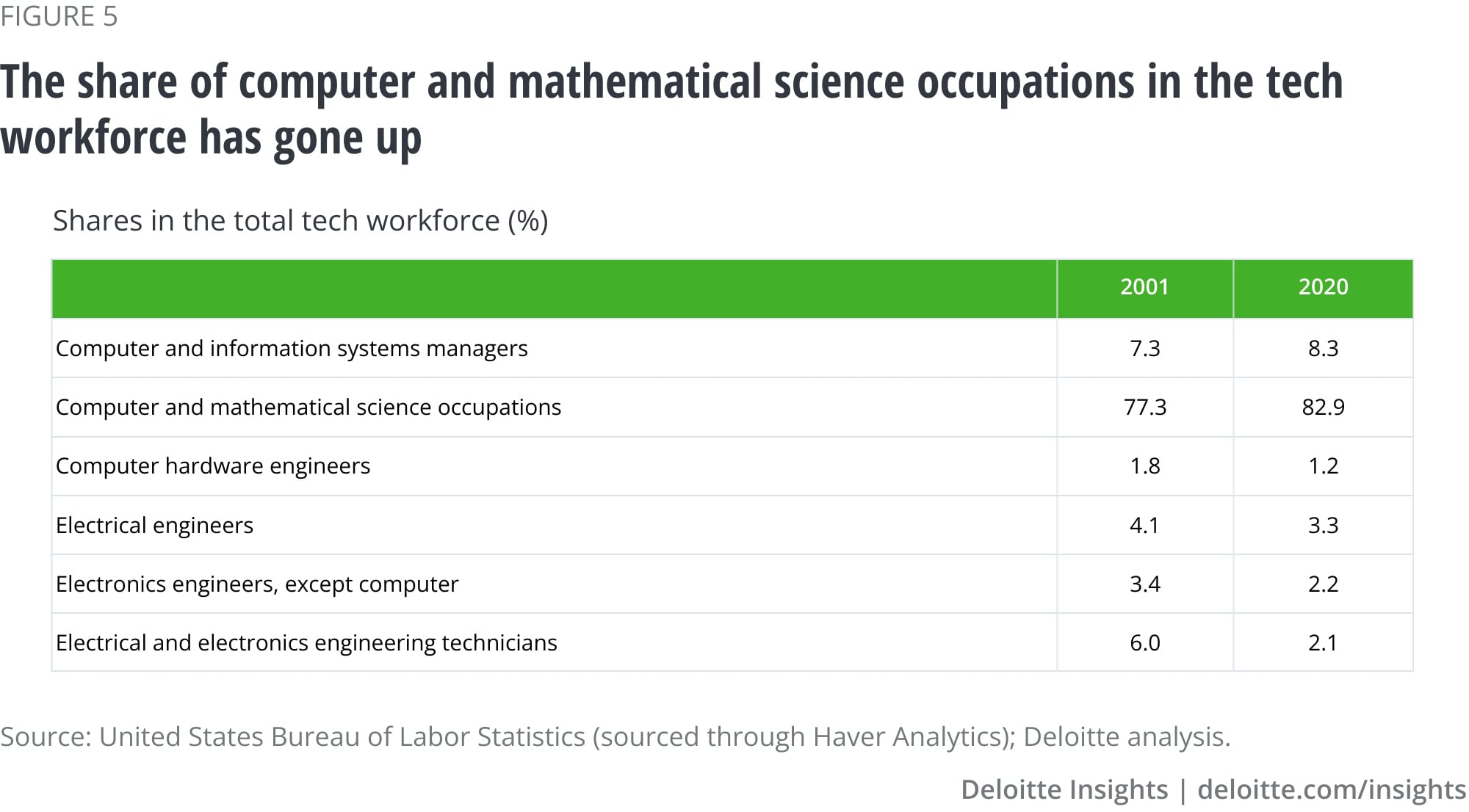

Analysis of trends7 within computer and mathematical science occupations reveals that mathematical science occupations (refer to the sidebar, “Six occupations make up the tech workforce in the economy” for more details) have grown at a faster pace than computer occupations in the last decade. For example, during 2012–2020, employment in mathematical occupations grew by 7.7% on average per year, buoyed likely by strong growth in jobs in statistical analysis and data sciences. Growth in computer occupations was lower (3%) during this period. No wonder then that the share of mathematical occupations within computer and mathematical science occupations went up to 5% in 2020 from 3% in 2012. Within computer occupations, information security analysts, which accounted for 3% of total computer and mathematical science occupations in 2020, grew by 8.3% on average per year during 2012–2020, while computer support specialists (share of 14% in 2020) went up 2.4%. The rise in employment for information security analysts isn’t surprising. As businesses go digital, they are increasingly worried about cybersecurity and data privacy and, hence, have been increasing investments in technology and talent to bolster their tech defenses.8

Who’s hiring more of the tech workforce? The usual suspects and many more

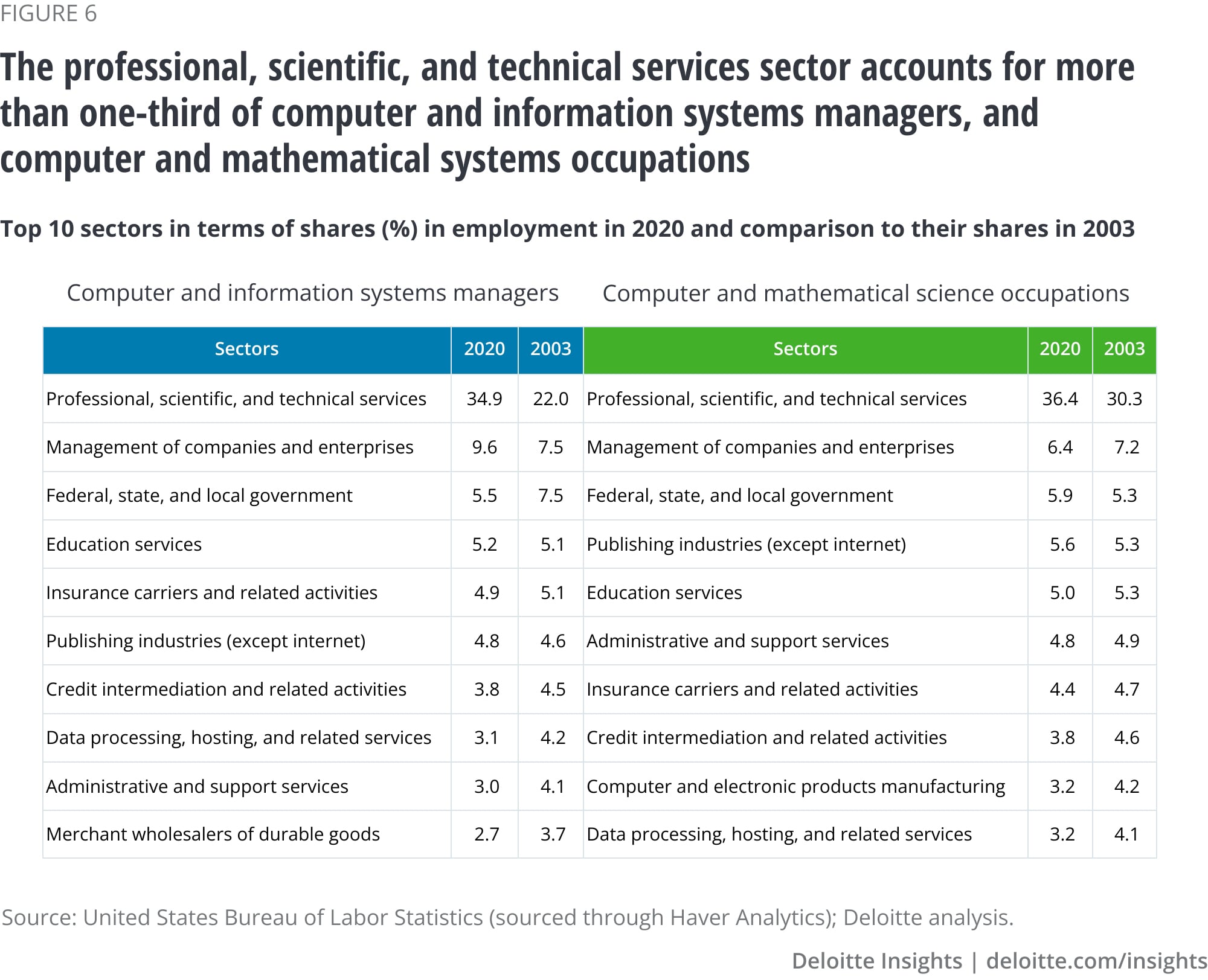

Which sectors account for a large share of the tech workforce? As technology spreads its presence in the economy, are we seeing any shifts? To answer these, the OEWS data again comes in handy. This database contains data on employment by sectors—88 of them. While there are gaps in the data for certain years, sectors, and occupations, there’s enough to draw some interesting conclusions on sector-level employment trends of the tech workforce.

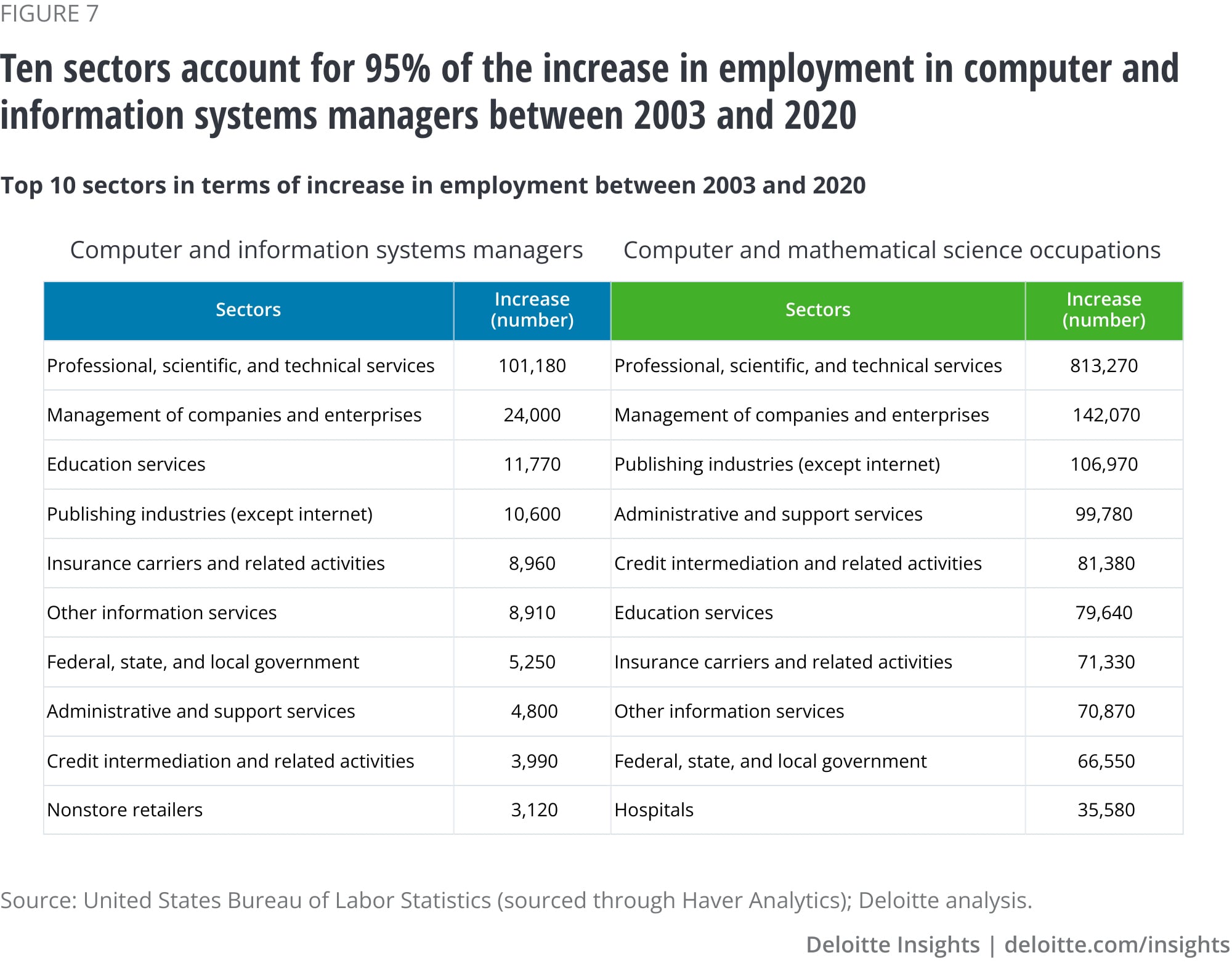

Analysis of employment data by sectors for computer and mathematical science occupations—which forms the bulk of the tech workforce—reveals that 10 key sectors employed nearly 78% of the workforce in 2020. Of these, professional, scientific, and technical services had the largest share (figure 6). The same is true for computer and information systems managers, where 34.9% of the workforce was engaged in the professional, scientific, and technical services sector. Interestingly, the sector—as figure 6 reveals—has strongly increased its presence in total employment for both the occupations over the years. That’s not surprising, given the strong growth in employment of both occupations in the sector. For example, the sector accounted for 46% of the nearly 1.8 million increase in personnel in the economy’s computer and mathematical science occupations between 2003 and 2020. Similarly, it accounted for 53% of the total increase in computer and information systems managers in the economy during this period. The trend of strong growth in the sector’s employment of these two key occupations within the tech workforce is most likely due to the rise of outsourcing, especially of professional and technical services—in light of increasing complexity, some sectors have chosen to purchase these services rather than keep this work in-house.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}