Robinson Crusoe’s capital: Stranded by COVID-19 has been saved

Cover art: Tushar Barman

COVID-19 is likely to change the US economy in some profound ways. Workers who have become used to working remotely are likely to want to continue doing so (at least some of the time); businesses that saved money on travel and offices may want to lock in some of those savings. The impact on consumer spending is uncertain, but the possibility of future pandemics may dampen the long-term spending growth in areas that could be sensitive to new diseases, such as restaurants and recreation services.

That shift presents the US economy—as it is currently configured—with a problem. The country’s capital stock—buildings, machines, and even ideas that power worker productivity—was designed for the prepandemic world. (See sidebar, “What is capital?” for the definition of capital as used in this article.) Some of that old capital will become even more productive and valuable postpandemic—but some of it may become less productive, or even useless. It’s odd to think that capital equipment and buildings could suddenly lose their value. But picture what could happen if, for example, cruise holidaymakers prefer other vacations in the foreseeable future?

All capital depreciates over time as it is used.1 Depreciation can take the form of physical deterioration (e.g., a machine wearing out) or obsolescence (e.g., a computer program being replaced with a more effective version). As a capital asset depreciates, it becomes less valuable. It may become less productive, or it may require the user to spend more on upkeep, or its output may become uncompetitive.

What happens then? If the value falls enough, the capital is “stranded.” There is a machine, or a building, or perhaps even an idea, but with no productive value, the machine or building or idea is useless. Ideally, the owners will write off the asset, sell it for scrap (if it has any scrap value), and move on.

Stranding happens more often than we might expect: The dynamic US economy is constantly forcing firms to write off what appears to be useful capital because demand has shifted or because better and more productive capital has entered the market. Anybody who has had to replace a “perfectly good” computer or smartphone in the recent past because the underlying software is no longer supported it will have experienced this.

COVID-19 may accelerate this process and will likely reduce the value of some capital types. Right now, much restaurant equipment (and the building space for restaurants) stands idle, many office spaces are empty, and some city busses and airplanes are parked. We are assuming, of course, that we will return to using this capital once the pandemic is over. But the postpandemic economy is likely to look different from the prepandemic economy. For example, many analysts are speculating that business air travel could decline significantly, as businesses learn to use virtual meetings effectively. This means that not all airplanes will come out of the hangar. Some may be parked forever and effectively become valueless. In other words, those aircraft will be stranded.

Just how much capital could be stranded after the pandemic? We measured the possible size of the affected capital stock using the Commerce Department’s detailed measures for nonresidential capital. The department’s Bureau of Economic Analysis publishes annual estimates of the nation’s capital stock by type of asset. The bureau identifies about 20 types of assets, ranging from aircraft to warehouses. We classified these assets into three categories: assets that would be less productive in the postpandemic world, assets that would continue to be as productive as before, and assets that might become more productive. For example, we assumed that the increase in working at home would make office buildings less productive. That doesn’t mean that there won’t be substantial use of office buildings, but it does mean that the marginal product of an office building—the additional production an additional building could provide—might be substantially lower in the postpandemic world.

Figure 1 shows our classification of these assets.

To be very clear, we are not likely to stop using all capital in class 3, or become desperate for capital in class 1. And these are very broad classifications: Within each, there may be subcategories that go against the general trend of the class. For example, office furniture demand may fall as people work at home; but demand for furniture at hospitals may rise. In general, however, capital utilization of class 3 categories is likely to be affected, likely prompting businesses to reduce investments in those areas. Instead, businesses are likely to increase investments in class 1 capital, which will be in greater demand.

Figure 2 shows the approximate shares of each class of capital in the US capital stock. We estimate that about one-fourth of the US capital stock risks losing value after the pandemic. It’s a bit disconcerting to realize that the pandemic could reduce the long-term productivity of such a large share of the capital stock.

Much of the at-risk capital is in the form of structures. These include office buildings (28% of class 3 capital), mining structures (20% of class 3 capital), and shopping structures (13% of class 3 capital). This presents a problem and an opportunity for the economy.

The problem is with the sudden depreciation of structures. Structures usually have a long life with low depreciation rates. For example, the standard tax life of nonresidential real property (i.e., nonresidential structures such as office buildings and retail space) is 39 years.2 (The actual economic life may be greater). That means that a sudden depreciation of office buildings will have a larger impact on the capital stock than a sudden depreciation of computers (which many businesses fully depreciate—and replace—after two to three years). The computers were going to lose value anyway: the buildings were expected to provide many more years of service. The large share of structures that seem to be at risk suggests that the productivity shock of the pandemic could be surprisingly large.

The opportunity comes from the fact that buildings are more flexible than other types of capital. Some machines can be repurposed (business-owned automobiles and light trucks might be sold on the consumer market), but specialized machine tools and airplanes can’t be easily converted for other uses.3 Renovating buildings for different uses may be costly, but such renovations were a feature of the US real estate market even before COVID-19, indicating that the building shell can retain considerable value.4 Not all buildings may be in desirable locations or have the architecture to make such renovation practical. But the option of renovating these structures may limit the impact of stranding to some extent.

So far, the discussion has focused on “real” capital—the actual machines, buildings, and ideas that power the economy. Ownership of real capital, however, is traded in financial markets, yielding the question of what changes in the value of real capital will do to the value of financial assets. There is no easy answer, because the exact impact depends on how much and which capital is stranded, and where it shows up in the financial system.

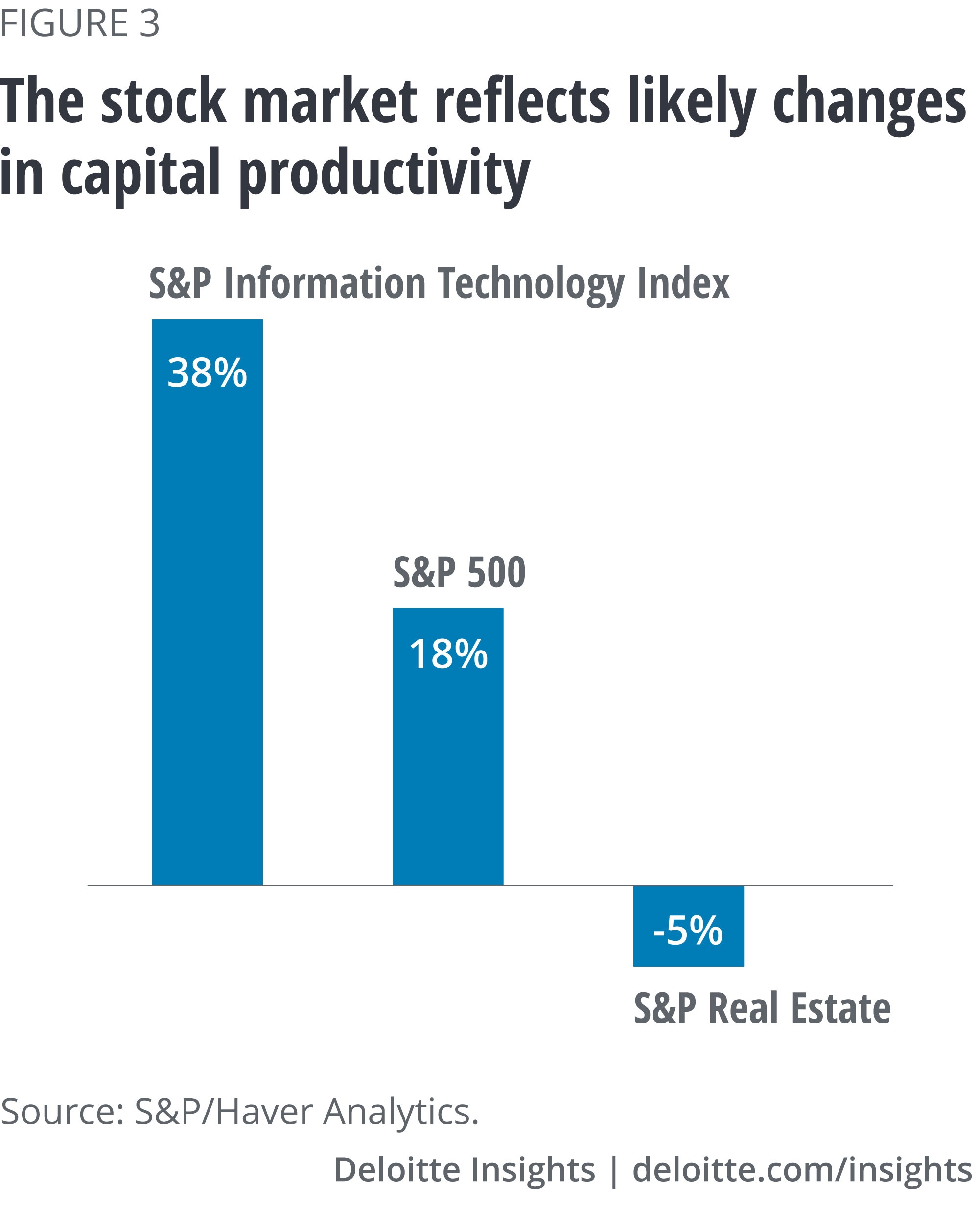

This means that stranded capital will have an impact on financial markets as well as on the economy’s ability to produce goods and services. In fact, that has already happened. Figure 3 shows S&P stock indexes for information technology (where existing capital is likely to become more productive) compared to real estate (where much of the existing capital is likely to become less productive). Overall stock prices held up surprisingly well during the year after the pandemic started, but information technology stocks soared. In contrast, real estate stocks (including real estate investment trusts) did substantially worse than the market. And that’s what we might expect as investors revalue existing assets in the wake of the pandemic.

Many people are hoping for, and expecting, a return to the prepandemic world. Businesses however will likely have to grapple with the fact that the value of the productive assets that they own will have changed. Accountants could write off stranded capital, reducing the value of companies that are overly invested in such capital. Markets will likely continue to place higher valuations on capital—such as information processing equipment—which has proven value in the postpandemic world. Changing patterns of valuation will lead to changing investment patterns. Business leaders will need to anticipate these changes and to orient their organizations toward the future—even if it means leaving behind capital that was once valuable.

{kind=link}

{kind=link}

{kind=link}