Giving green a chance has been saved

Cover artwork by: Jaime Austin

Countries are increasingly committed to tackling climate change. This year, the United States rejoined the Paris Agreement1 and China doubled down on its objective to be carbon neutral by 2060.2 Under the Paris Agreement, 196 countries have committed to reducing greenhouse gas emissions.3 For many countries, the top priorities are to reduce emissions in energy-intensive industries, electrify transportation, and reduce coal consumption.4 As a result, energy-intensive industries, such as steel and aluminum production, will face considerable pressure to reduce emissions. Demand for coal and oil may slow down, which will reduce global exports of these high-emitting goods. In the long run, nearly every industry may face higher costs owing to emissions. As countries move toward their Paris Agreement goals, the flow of goods around the world could change dramatically. There are countless ways goods trade could change in response to climate change, but for the purposes of this article, we will focus on the effects of the proposed carbon border-adjustment tax in the European Union (EU) and the nearest-term policy responses to that tax.

The Paris Agreement allows each country to make its own nationally determined contribution to reducing greenhouse gas emissions. As a result, countries are at different stages in the process. Among the largest economies, the European Union (EU) has made the most progress—it has an emissions-trading system that operates on the cap-and-trade principle.5 Given the uneven development of such systems around the world, the risk of carbon leakage—where carbon reduction in one region is offset by higher carbon production in another region—has risen. Such a scenario disadvantages producers in regions with more stringent climate policies than those with softer standards. This is why the EU is moving forward with a carbon border-adjustment that allows the EU to set the same carbon price for imported goods as it does for its own domestic production.

Before we examine how a carbon border-adjustment in the EU will affect international trade, we need to establish how the adjustment will likely work. A carbon border-adjustment tax should be set to equalize the price of carbon produced in the EU with the price of carbon implicit in its imports. There are large operational hurdles for this to happen. First, the EU needs to know the price of carbon for that good in the exporting country. Second, the EU will need to know how much carbon was emitted in the production of that good. The latter issue is particularly tricky as it would require monitoring production outside of EU borders. Exporters with lower carbon prices and higher-emitting production processes will face the highest tax rates. Conversely, exporters with higher carbon prices and lower carbon-emitting processes should receive at least some discount on the tax.6

Setting a border-adjustment on energy-intensive goods would reduce the EU’s demand for such imports as their after-tax price would increase for EU buyers. In the short run, this should increase the balance of trade—EU imports fall—and the value of the euro relative to these energy-intensive exporters. Because the EU is a large economy, this will initially lead to an oversupply of energy-intensive goods in the rest of the world, pushing exporters to lower prices. The fall in prices is expected to raise the demand of these goods from non-EU countries that do not have a carbon border-adjustment tax or similar policy, thereby offsetting at least some of the export decline to the EU.7 What happens from there is highly dependent on the reaction to the border-adjustment policy in the rest of the world.

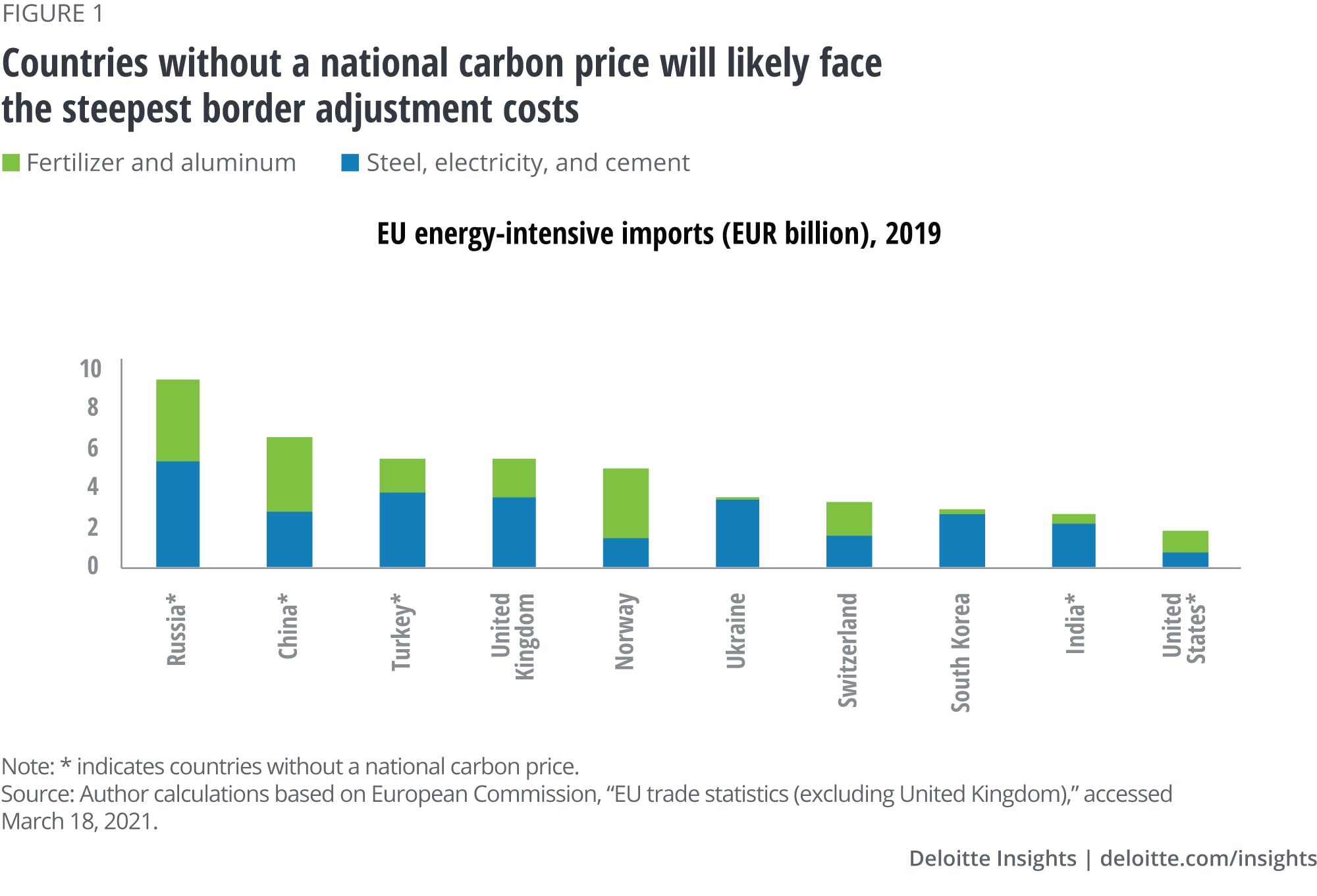

Although details remain scant, the first industries to be subject to a carbon border-adjustment tax are to be steel, cement, and electricity. Aluminum and fertilizers will likely follow.8 Russia has the most exposure to the EU when it comes to these energy-intensive goods (figure 1). China and Turkey each exported more than 5 billion euros of these goods to the EU in 2019.9 None of these countries has fully established a national carbon price yet, suggesting that they would be subjected to a high tax rate. Ukraine and India are highly exposed to the EU, and only Ukraine has established a national carbon price but it is just 1.2% of the EU’s level.10 To make matters worse, production of steel in China, Russia, and Ukraine is carbon-intensive relative to the EU’s own steel production,11 suggesting these exporters would face additional costs once a border-adjustment is implemented.

The United Kingdom, Norway, and Switzerland also have relatively high exposures.12 However, Norway is part of the EU emissions trading system; Switzerland has a higher carbon price than the EU; and the United Kingdom’s carbon price floor was only slightly below the EU carbon price in November 2020.13 This suggests that a border-adjustment may be nonexistent for Norway and Switzerland and relatively low for the United Kingdom.

Other countries are also highly exposed to an EU carbon tax relative to the size of their economies. Although not among the top 10 exporters of energy-intensive goods, Brazil, South Africa, and Egypt each exported more than 1 billion euros of them to the EU. Energy-intensive exports from Mozambique, Serbia, and Belarus were each just shy of 1 billion euros.14 For some of these countries, those exports to the EU represent large shares of national income.

Some non-EU countries have expressed concerns about a carbon border-adjustment tax. Developing countries may be particularly vulnerable because they will struggle to keep up with the sizable investments that are required to reduce emissions and remain competitive in these industries. The EU may exempt the world’s least developed countries,15 and some experts have even advocated for sending border-adjustment revenues back to developing countries to be invested in emission-saving technology.16 Russia is particularly opposed to the carbon border-adjustment tax as it stands to lose a substantial amount of exports. The country has already intimated that it will challenge the policy at the World Trade Organization (WTO).17 Many experts have said that a carbon border-adjustment tax can comply with WTO rules, but it must be designed carefully. Otherwise, the EU will have to back down or face retaliation.18 The EU could face retaliation outside of the WTO’s dispute settlement system, which would further undermine an already-fragile rules-based trading system. Moving ahead with the border-adjustment is likely to create rifts in the geopolitics in Europe and beyond, as the EU’s relations with Turkey, Russia, and other eastern European countries could deteriorate significantly.

It should be noted that a carbon border-adjustment tax is not the only climate policy that may affect trade flows. EU policies to electrify its transportation systems and reduce its reliance on coal will also have sizable effects on international trade and geopolitics. Electrification will necessarily lower EU demand for oil and coal. Yet again, Russia was the EU’s largest source for both in 2019. Russia’s exports of natural gas may help to cushion some of the decline, but its natural gas exports to the EU are less than a third of its petroleum exports. Australia and the United States are the two other major coal sources, while Norway, Nigeria, the United States, and Iraq are the main sources for petroleum.19

While the EU’s climate policies are multilateral in principle, they are unilateral in practice. How the rest of the world reacts will largely determine how trade flows develop once the carbon border-adjustment tax is in place. Assuming it takes some time for other countries to catch up to the EU’s climate policies and carbon prices, EU exports may face downward pressure. In 2019 alone, the EU exported more than 32 billion euros of iron and steel and more than 16 billion euros of aluminum. The United States, Turkey, and China are some of the largest recipients of these goods.20 Until these countries implement their own national carbon-pricing initiatives, they may switch to cheaper and higher-polluting alternatives outside of the EU. It is also possible that they could implement countervailing duties on EU exports in an effort to pressure the EU to lower or remove the tax.

What happens in the United States is critically important as it is the world’s largest economy and consumer. Although the country has wavered in its support for tackling climate change, the current US president campaigned on more environmentally friendly policies, one of which included a carbon border-adjustment.21 Should such a policy come to pass, the EU could have an opportunity to raise its exports to the United States. The EU already exports more than US$7 billion of steel, cement, fertilizer, and aluminum to the United States. Aside from Canada, the other large exporters of such goods to the United States are Brazil, Mexico, and Russia. If these three countries continue to lag in their climate initiatives, the EU and Canada will have an even greater opportunity to capture additional market share in the United States. However, more recently, the US climate envoy has urged the EU to hold off on a carbon border adjustment, and expressed concern that such a policy could be damaging to international relations and the global economy. Instead, he indicated such a policy should be used as a last resort should other countries not take the necessary steps to reduce emissions.22

As the United States and other countries work to reduce emissions, global oil and coal consumption will begin to fall further, with fewer opportunities for carbon leakage. Canada accounts for the largest share of US oil imports, followed by Mexico and Saudi Arabia.23 The other major oil exporters globally include Russia, Iraq, and the United Arab Emirates.24 However, widespread carbon pricing is expected to make oil export declines uneven. For example, oil production in Canada and Venezuela is highly carbon intensive, suggesting that these could be the first places oil importers will shy away from while they reduce greenhouse gas emissions. At the same time, Saudi Arabia’s oil production has a relatively low carbon intensity,25 raising the possibility that demand will shift in its favor. Lowering global coal consumption will disproportionately affect Australia, Indonesia, and Russia, which together account for more than 75% of global coal exports.26 Most of these economies are highly dependent on these resources, and unless they are able to diversify away from those resource exports, they’ll face serious economic challenges.

Although global oil and coal exports will face downward pressure, other exports are likely to rise. As countries work toward their emission commitments, global demand for lower carbon-emitting goods will likely increase. The same is true for green technologies that limit emissions in energy-intensive industries, lower the cost of renewable energy, and raise the energy storage capacity. The EU stands to benefit from the rise in demand of these goods. The EU’s higher environmental standards have put pressure on domestic producers to develop these green technologies, giving the region first-mover advantage.

The EU’s proposed carbon border-adjustment tax demonstrates how climate-related policies can quickly become trade policies. As Europe and the rest of the world reduce emissions, exporters of energy-intensive goods will likely have to grapple with lower prices in the short term and potentially significantly soft demand in the long term. New export markets will be made available to countries that can effectively lower the emissions of their industries and develop cutting-edge green technologies. However, this assumes more countries follow the EU’s lead on climate change mitigation and continue to pursue their commitments under the Paris Agreement. The United States’ withdrawal from the agreement and subsequent rejoining reveal that such an assumption is not guaranteed, and that progress to a greener future may not be linear.

{kind=link}