Capital markets: Modules and Microservices Seizing the opportunity

7 minute read

29 February 2020

Oleg Tyschenko United Kingdom

Oleg Tyschenko United Kingdom Lucinda Clements United Kingdom

Lucinda Clements United Kingdom Magda Kosowska United Kingdom

Magda Kosowska United Kingdom-

Vikram Tuli United Kingdom

Vikram Tuli United Kingdom Vishal Aravind Krishnasamy United Kingdom

Vishal Aravind Krishnasamy United Kingdom Pranav Lakhotia United Kingdom

Pranav Lakhotia United Kingdom

The financial services industry faces high pressure on revenue and margins, combined with regulatory demands and increased market competition. Technology remains a pivotal game-changer in meeting these challenges.

The financial services industry continues to face new challenges.1, 2 Greater pressure on revenue and margins, combined with regulatory changes and increased market competition are pushing banks to reshape their business models into leaner organisations, responsive to both changing market conditions and growing customer demands.3, 4 Technology remains a pivotal game-changer in meeting these challenges. Examples include cloud computing and prototyping on cloud, which are helping banks to accelerate innovation cycles, improving flexibility and speed-to-market at a lower cost.

Learn more

Explore the Financial services collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

Digital is now a daily reality for decision-makers. Its broad inflow and impact across business requires constant observance and evaluation of the opportunities (increased speed, agility, cost reduction) and threats (increased competition and soaring market share to FinTech companies).

Despite its potential to alter the entire value chain, technology still relies heavily on close collaboration with business. Global firms such as AWS, Netflix and PayPal have shown the benefits of combining technical expertise with customer and business knowledge. Successfully migrating from a monolithic architecture to a microservices architecture (MSA) has given them unique agility and scalability at lower cost, whilst staying renowned as customer centric. They have also moved from simple automation to the advanced technologies of machine learning and AI, delivering tailored customer offerings, operational efficiency and business agility on a global scale. Such change is not made by simply shifting to a new infrastructure but by studying what underpins the operating models and organisational culture, creating a ‘vehicle’ that can support the transformation.

Past approaches to IT projects are inadequate, and agile innovations must become the norm in project delivery. We need to define how the organisation will operate to achieve business goals and respond to the strategic drivers. As we address it through the move of technology architecture towards MSA, the question is not ‘should we’ but ‘how do we’ take this opportunity and stay in the game.

Where to start?

Evolving technology will drive business transformation for at least the next three years, liberating banks from legacy IT systems. Banks must respond to change as it happens, but how will they do so?

1. Create a blueprint

Banks must define their vision and direction as a blueprint (a ‘target-state architecture’) for the type of business they aim to be in the future. An MSA-based blueprint is helpful to banks aiming to build a dynamic platform, but choices must be realistic and pragmatic, since the underlying functions may not be mature enough for the transformation journey. Aligning technology with cross-business functions, especially operations, will be key in overcoming this.

A holistic view of the organisation must also evaluate the level of maturity and identify where people, processes, technology and data are unprepared. Any gaps in preparedness may be considered as opportunities to utilise and deliver MSA. In many instances, this entails a significant change to ways of working, operating and service delivery. Still, ‘MSA first’ must be the design principle for new products and services.

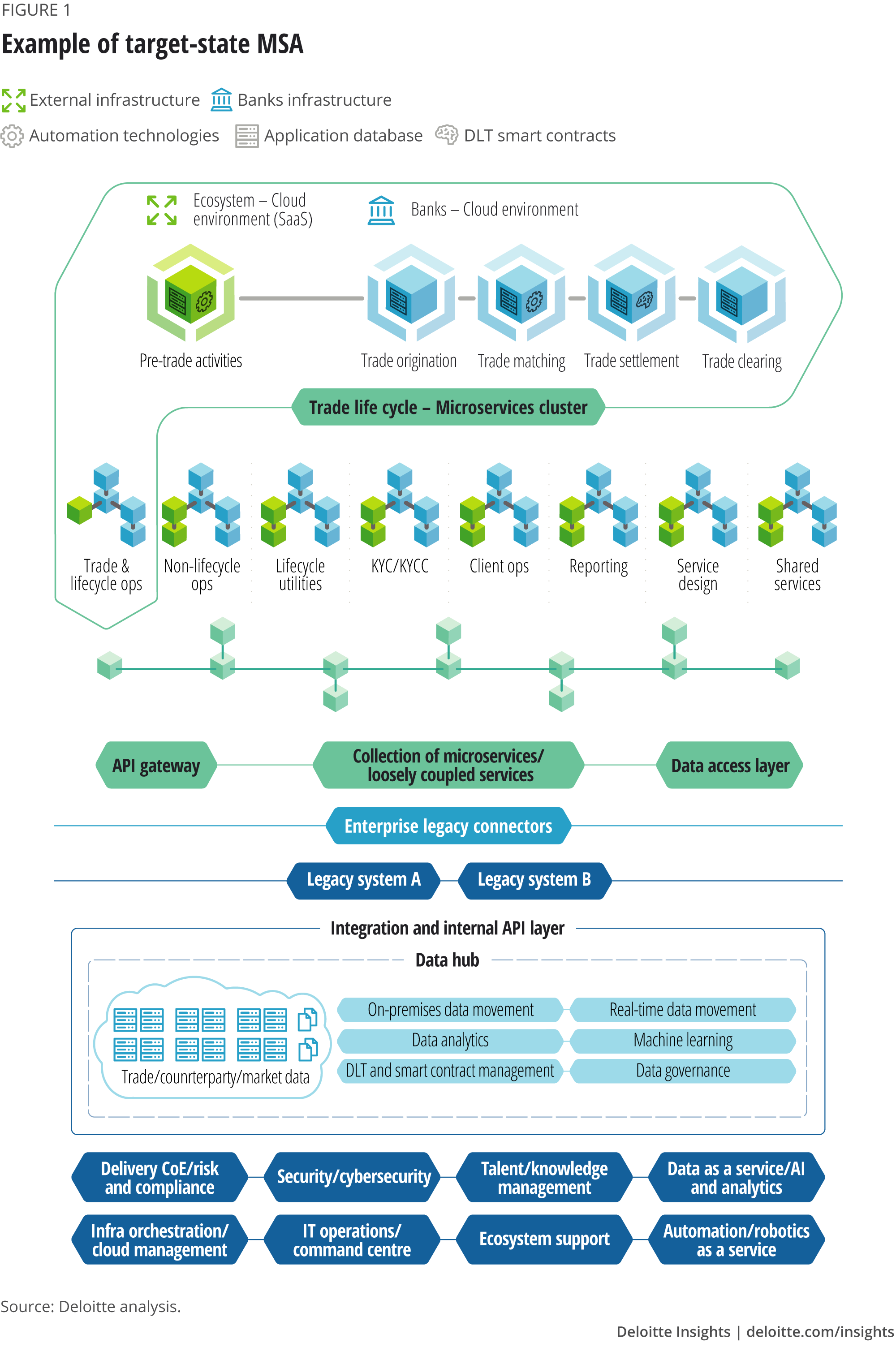

In the example shown in figure 1, a microservices architecture breaks down business activities (and capabilities) into small modules. These can be built and developed independently and scaled up across the organisation, at pace and as required, by collaborating with external and internal stakeholders. This can enable the bank to stand out in the market, embrace innovation and capitalise on efficiency opportunities for its core operational functions.

2. Prepare to partner with FinTechs and BigTechs

A bank’s control of key processes within its value chain was traditionally done in-house. Changes both technological (MSA, cloud, machine learning) and regulatory (open banking) have made this business model obsolete, whilst enabling FinTechs and other tech companies to advance rapidly in the market. Such disruption drives new and specialised products, whilst raising customer expectations. Banks must consider opportunities for ecosystem partnerships in their new business model blueprints. A fraud check or a credit check service is a good example of MSA in action. Such functions can be performed in isolation, possibly by outsourcing the operation as a microservice or a group of microservices to an ecosystem partner. Market dynamism requires banks to be at the forefront of change, always monitoring market trends and changing technology to ensure their competitiveness and the relevance of their blueprint. MSA’s modular structure will support banks in this: It can simplify both the making of new partnerships and the introduction of new products, since fresh components can be easily added, removed or replaced without affecting the rest of the system.

3. Get used to cloud, and lots of it

A cloud-based platform for MSA requires no physical infrastructure and the chance for a software-as-a-service model, rather than developing and maintaining software and systems in-house. Cloud is not just about infrastructure, but also value-added services. It deploys the MSA securely and connects with ecosystem partners, enabling deployment without adding to compliance requirements. In planning a move to a new technology architecture, banks must judge if they are ready to move to cloud-based operations. It may help them to budget incrementally for a step-by-step transition to a cloud-first architecture model. Regardless of the chosen approach, cloud benefits will be quickly apparent, including accelerated implementation, reduced time to market for new products or services and a lower cost of applying and maintaining the technology.

Another feature of cloud MSA is ‘plug and play’. This means that whenever a change is needed in the architecture, the relevant MSA module is simply taken away and a new one put in its place, without disrupting the rest of the system.

A blueprint must utilise services, rather than deploying technology components. The design principle of business architecture must be ‘rent before buy, buy before build’, meaning that technology services can be rented or subscribed to from various suppliers, rather than be built from scratch.

4. Use intelligent automation to unlock more value

Automation continues to transform business, driving both cost reduction and product innovation. Banks have lately focused on digital workforce, due to its applicability, easy implementation and attractive ROI (benefits delivered in a shorter time frame compared to complex technology delivery programmes). Many banks have deployed automation and basic cognitive technologies to streamline what is routine and rule-based in their operational processes. This achieves significant cost reduction with improved quality and processing speed, allowing the workforce to focus on more important activities.

Process automation can help banks address cost and efficiency pressures directly, but genuine long-term value is gained through automating non-routine, cognitive tasks that involve judgement and problem solving. Operating on the cloud and adapting MSA can offer the chance to tap into advanced cognitive technologies (AI, blockchain, IoT) to improve efficiency and business agility and drive innovation. Banks may then take automation further to create intelligent processes, combining RPA and analytics with cognitive technologies, to help humans successfully deliver complex processes and tasks more efficiently. For example, AI is already being used by wealth management firms to analyse and review portfolio data and to auto-generate meaningful reports. Global banks are increasingly using AI to enhance regulatory compliance and monitoring and to bolster fraud detection systems that protect customers.

As a result, business operations are changing how they work and deliver services, creating a need for technology-driven operating models that might need to be revisited and redesigned.

5. Prepare for a technology-driven operating model

Business models change with technology, as the boundary between technology and operations grows increasingly blurred. MSA brings a range of strategic and operational benefits, but also needs investment and careful consideration of the operating model aspects.

The role of internal IT function changes as organisations move their technology onto cloud. Responsibilities such as patching, life cycle management and capacity management will no longer be required in-house. The introduction of augmented workforce (through AI and robotics) and the shift towards BizDevOps (business, development and operations)/BusProdDevOps (business, product, development and operations) developments mean that banks will need more highly skilled professionals to drive the design, development and support of new products and services. Banks must be ready to rethink the future of their workforces and support their people during a transition to tech-fluent roles.

New technology requires review of the existing governance model and controls to ensure they are fit for purpose. Banks will require robust governance processes to evaluate data protection and cyber-security while operating on cloud. Governance framework needs continuous review at modular and enterprise level to ensure that customers and the business are protected from any associated risks.

For example, machine learning can provide real-time predictions of client behaviours across asset classes. This helps banks assess future liquidity requirements and manage risk proactively. However, the reliability of these predictions must be considered. Relevant regulations covering use of personal data for behavioural analytics must also follow compliance guidelines.

The impact of tech-fluent business roles on operating models is covered in detail in Deloitte’s latest edition of Nine big shifts5 where there is an in-depth analysis of the changes necessary to align operating models to support new technologies and ways of working.

6. Be customer centric with data

Capital markets generates large volumes of market and trade-related data, which is an asset in terms of gaining valuable customer, business and market knowledge. However, ownership of data is spread across different organisations and must be made interoperable to extract maximum value.

MSA opens a range of opportunities to utilise cognitive and analytics technologies that analyse and enrich existing data sets, creating insight into customers and operations. Using cloud-native machine learning algorithms can drive the adoption of AI, which can enhance operational insights, project outcome and customer experience. MSA enables the delivery of innovative machine learning products and services on a cloud platform.

Data power will help banks to reimagine their method of identifying, trialling, evaluating and scaling new technologies, making them business and customer relevant.

What’s next?

Should MSA’s modular structure be the target-state architecture for banks within capital markets? Strategies will differ between institutions, but it is highly probable that capital markets business operations will become simpler, leaner, more agile and more automated over the next few years.

- Business processes across the value chain will be simplified, with layers of complexity that do not directly support core objectives removed.

- Organisations will be leaner, using the cloud and external partners to reduce the need for in-house infrastructure, escaping from legacy IT systems.

- Business agility will be achieved by modularity, managing business operations as a number of autonomous technology components and services.

Banks within capital markets will clearly not succeed in the future if they cling to the current business blueprint and fail to embrace change.

Deloitte Technology Strategy and Transformation

Deloitte Technology Strategy and Transformation?s specialists help capital markets organisations drive increased value from the day-to-day technology operations. Our offerings provide the vision, strategy, and roadmap for wide-scale transformations to business and IT operations, aligning the technological changes with business goals. We work with senior leadership to set the technology direction, help to define the target state and prepare the plans for the transformation. Contact the authors for more information or read more about our technology strategy services on Deloitte.com.

Learn more

Get in touch

- Lucinda Clements

- Partner Consulting

- Deloitte UK

- lclements@deloitte.co.uk

- +44 20 7007 9948

© 2021. See Terms of Use for more information.

Related

More on Banking & Capital markets

-

2025 banking and capital markets outlook Article4 months ago

2025 banking and capital markets outlook Article4 months ago -

Executing the open banking strategy in the United States Article5 years ago

Executing the open banking strategy in the United States Article5 years ago -

The digital banking global consumer survey Article6 years ago

The digital banking global consumer survey Article6 years ago -

The API imperative Article7 years ago

The API imperative Article7 years ago -

Infusing data analytics and AI Article5 years ago

Infusing data analytics and AI Article5 years ago