Is it time to rethink inflation?

Economists thought they had figured out how inflation started and what policies can stop it. But recent experience is making some economists rethink the entire problem.

History provides many instances of inflation—a general rise in the prices of everything—to learn from. The Roman empire famously took to currency debasement, leading to centuries of rising prices.1 Spanish imports of silver from South America sparked a century or more of inflation in Europe.2 Germany experienced the world’s most famous hyperinflation in the early 1920s. In all these cases, the basic cause of inflation is clear. It’s the creation of money beyond the needs of the economy—whether by “debasing” coins, importing silver, or by printing money.

But the 21st century has not been kind to this theory. Recently, in much of the developed world, the relationship between money and inflation seems to have broken down. And, yes, there are people who are ready with new answers, and with a new story to guide policymakers in limiting inflation. So far, however, the Fed and other central banks aren’t buying those ideas—but that could change.

Printing money and wage-price spirals

The standard story about inflation that economists believed (and what you may have learned in a college economics class) after the 1970s described how money creation spurred higher prices, and, if not contained, could create long-term inflation.

- The authorities (central banks in the modern world), faced with an economic downturn, ease credit conditions. To do so, they create or “print” money, putting that money into the hands of economic actors (banks, businesses, and households).

- Businesses, flush with cash from cheap borrowing, spend heavily on (possibly low-return) investments. That raises the prices of inputs, the most important of which is labor.

- Higher wages allow households to buy more.

- With demand high (and likely above capacity), businesses raise prices to cover their higher costs.

- Households thus face higher prices. Workers in those households want to prevent their real incomes from falling, so they demand higher wages.

- The need to raise wages forces companies to raise prices to cover the increased wage costs.

- Back to #3, workers see higher prices and want further increases in the wages to compensate.

- The pattern continues, with prices spiraling upward—especially if the central bank, fearing a downturn, is unwilling to turn off the credit tap.

A more refined version of this story brought in consumer and business expectations of inflation. Once workers and businesses set prices in anticipation of future inflation, the job of stopping inflation became a lot harder. Central banks (notably the US Federal Reserve) had to create recessions, essentially to convince businesses and households to lower their expectations of future inflation. This meant monetary restraint and high interest rates were the key tools to fight inflation.

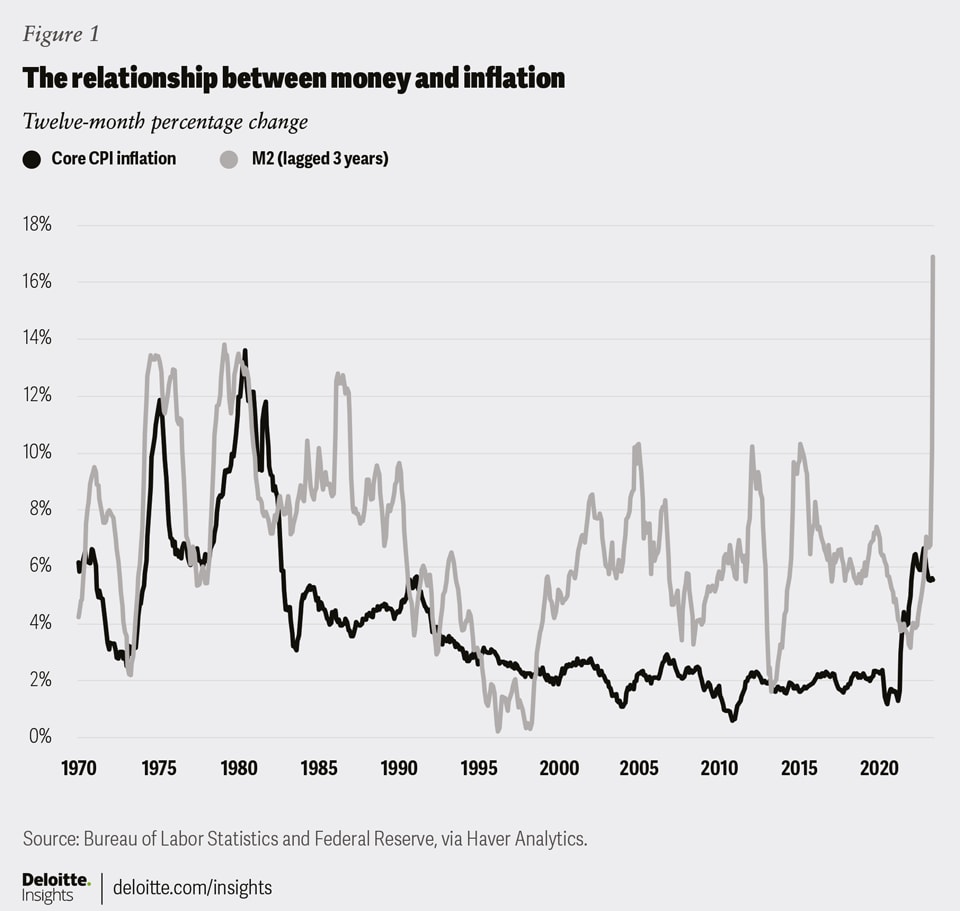

This story was a good description of the inflation that gripped much of the world from about 1965 to 1990. But even in the 1980s, many economists questioned whether the role of money in creating inflation was as clear as the textbook story made it to be. The first problem involved the money supply. Figure 1 shows that the growth in money supply detached from inflation in the 1980s. Inflation was much lower than what the money supply growth would have suggested, and the dip in money supply growth in the late 1990s and jump in growth during the 2000s didn’t result in much change in inflation.

What happened after 1980? Markets responded to financial deregulation by inventing new banking and savings products, so the measurement of money supply became less certain.

Economists responded at first by trying to refine the measurement of “money” (see, “Measuring money”).3 However, by around 1990, most experts on monetary policy understood that the theoretical concept of money was too difficult to measure effectively for policy purposes. The Fed’s experiment with targeting the money supply to control inflation ended in the early 1980s. Instead, the Fed’s preferred tool became short-term interest rates. But the basic idea remained; fighting inflation meant raising interest rates. And raising interest rates worked by limiting the creation of “money” and near-money assets. This, in turn, limited overall spending, and therefore the ability of workers to ask for raises and of businesses to raise prices.

Measuring money

The textbook definition of money is “a generally accepted medium of exchange.” That definition can be surprisingly hard to apply when it comes to measuring the amount of “money” available to economic actors.

Printed currency and coins are obviously money. By the mid-20th century, many transactions in modern economies were completed using checks, which are written “drafts” on a bank account. Economists therefore include balances at bank accounts—specifically, any bank account that, by contract, allowed the holder to receive currency “on demand,” or demand deposits. The basic measure of money therefore included currency (including coins) and demand deposits. As other, more expansive measures followed, economists designated this measure “M1.”

The US financial system has created other assets that are very “liquid” (easily turned into cash or demand deposits). Some economic actors hold these assets as a close substitute for cash or demand deposits. There is no practical difference between the ability to use a savings account or a checking account for payments (since switching funds from savings to checking requires trivial time and effort). That leads to a broader definition of money, including not only the assets in M1, but also savings deposits, some “time” deposits, and retail money market funds. This is a broader measure of money, “M2.”

At one time, some US analysts used an even broader measure of money, “M3.” The Federal Reserve stopped publishing M3 in 2006 and has stated that “M3 does not appear to convey any additional information about economic activity that is not already embodied in M2.”4

Some analysts use the “monetary base” to understand policy. The monetary base is the sum of currency outstanding and bank reserves, which are the limiting factors in banks’ creation of deposits. However, a recent change in the Fed operating procedure means that the relationship between the monetary base and the supply of money is no longer stable or useful.5

Economists have created other measures of the money supply, depending on the time period and the types of assets available to economic actors. Money definitions will differ among countries with different financial systems and assets available to use for transactions. But for the United States, today, most analysis is limited to M1 and M2.

Inflation in the 21st century

In the last two decades, that inflation story of money creation leading to a spiral of higher wages and prices didn’t seem to apply. There were, in fact, three strikes against the standard approach.

- The rise in unemployment after the global financial crisis was quite large. Many economic models predicted that such a steep rise in unemployment should have actually pushed wages6—and perhaps even prices—into decline. Figure 2 shows that, despite a rise in unemployment twice that of the previous two recessions, wages didn’t fall much more than in the much milder downturns in 1990 and 2001.

2. During the global financial crisis, the Fed created a lot of “money.” The M2 money stock grew over 6% in 2007 and 2008, and over 8% in 2009. The monetary base and M1 grew even faster. But fast money growth did not translate into higher inflation, despite the expectations of some distinguished economists.7

3. Record-low unemployment rates in the late 2010s did not lead to an acceleration of wages, as the standard story would expect. That was certainly good news, and made things easy for the Fed. But the disconnect between the labor market and wages was hard for economists to explain.8

The COVID-19 pandemic saw even faster money growth (13% in the second quarter of 2020). Although inflation did indeed pick up after a year or so, the evidence points to supply chain issues rather than tight labor markets as the initial cause of this inflation.9 Real wages (adjusted for the employment mix) have, in fact, fallen about 5% since the pandemic started. That suggests that labor markets are not yet tight enough to raise wages, despite record-low unemployment rates and a large gap between the number of job openings and the number of unemployed.

Other theories?

The apparent failure of the standard inflation story has created an opening for new ideas about inflation.

To be clear, persistent and high inflation rates, like those currently occurring in Zimbabwe and Argentina, can be traced back to extremely fast growth in the money supply. For these and other countries that experience very high inflation, the traditional story still provides a good description of what is going on. But for developed countries with complex financial systems and more moderate levels of inflation (below 10%, or so) the relationship between money and inflation, or the labor market and inflation, appears to be more complicated.

There are two new approaches to the question of inflation:

- Modern Monetary Theory (MMT) is a controversial alternative to standard Keynesian/Monetarist macroeconomic models. MMT suggests that broad demand, which is not necessarily related to the money stock, creates inflation. MMT theorists argue that fiscal policy is more effective than monetary policy at managing both inflation and keeping the economy at full employment. How to slow inflation? MMT calls for a combination of restrictive spending (and/or tax hikes) and government incomes policies, while maintaining full employment.10

- Recent research in antitrust and competition has led some economists to suggest that, in place of a wage/price spiral, we are experiencing a profit/price spiral. According to these analysts, decreasing competition in the US economy allows firms to raise prices and increase margins under cover, as it were, of the need to raise prices because of higher costs.11 How to slow inflation? Antitrust policy is an important element of calming today’s inflationary environment, according to this theory.

As these ideas are new (at least in the mainstream of economics), it’s too early to judge whether they are useful guides to fighting inflation. What is true is that they have become an important element in economists’ discussions about what causes inflation and how to cure it.

The Fed is going to stay the course

While the economics profession is considering new ways to think about inflation, Fed officials have stated clearly that the standard story is still guiding policy. In May, at the press conference after the Federal Open Market Committee (FOMC) meeting, Fed Chair Jerome Powell admitted that the inflation we currently observe may not be caused by labor market tightness.12 But he (and presumably the Fed staff and other FOMC members) still thinks that the path to lower inflation lies in taking pressure off the labor market by reducing demand. And the way to reduce demand is to raise interest rates and (effectively) reduce the supply of money and credit. Other developed-country central banks, like the European Central Bank and the Bank of England, also continue to follow the traditional paradigm.

Perhaps that’s not so surprising. Central bankers are not famous for being risk-takers (nor should they be). And the new theories about inflation are largely untested and still the subject of intensive debate. But if inflation continues to react to central bank policies in unpredictable ways, some economists are laying the basis for a shift in how monetary policy is conducted. If any change is really warranted, it may take years—maybe even a generation—to occur. Perhaps it’s not surprising that we can leave the last word to the most influential macroeconomist of the 20th century.

“There are not many who are influenced by new theories after they are twenty-five or thirty years of age, so that the ideas which civil servants and politicians and even agitators apply to current events are not likely to be the newest. But, soon or late, it is ideas, not vested interests, which are dangerous for good or evil.”13

—John Maynard Keynes

{kind=link}

{kind=link}