Decarbonizing the passenger vehicle fleet: A framework to achieve net-zero targets

To curb climate change, most vehicles on the road will have to be replaced. A Deloitte Center for Sustainable Progress analysis offers a path that benefits customers, the planet, and business alike.

Road transportation is a significant source of global carbon emissions, accounting for 15% of the world’s carbon emissions, according to the International Energy Agency (IEA).1 Though automakers in the three key auto markets—the United States, Germany, and China—are now rolling out electric vehicles, the IEA estimates that 91% of the world’s existing passenger vehicle fleet still runs on fossil fuels,2 a mix that the industry—and the world—rapidly needs to change.3

But, according to Benedikt Middendorf, director of Deloitte Germany’s Automotive practice, who contributed to the Deloitte Center for Sustainable Progress’ analysis of the German auto market, the world cannot achieve net zero by simply accelerating the production of EVs. “What we found is that, while ramping up of electric vehicles is frequently addressed in the public debate, the problem of the remaining internal combustion engine vehicles on the roads has largely been neglected,” he says. “An organic replacement of the existing cars with cleaner alternatives alone will be insufficient to meet the net-zero targets.”

Deloitte Insights spoke to Middendorf to learn more about the research findings and what they could mean for other countries.

Q: Thanks for giving us a closer look at this aspect of the net-zero challenge. For context, can you share more background on the problem you are trying to solve? How much do passenger vehicles contribute to climate change? How big of a challenge will it be to curb those emissions?

A: The objective is to be carbon neutral by 2050 to support the temperature goals outlined in the Paris Agreement. Around 28 jurisdictions, ranging from Paris and Madrid to Amsterdam and Copenhagen, are preparing for a total ban on internal combustion vehicles beginning in 2025.4

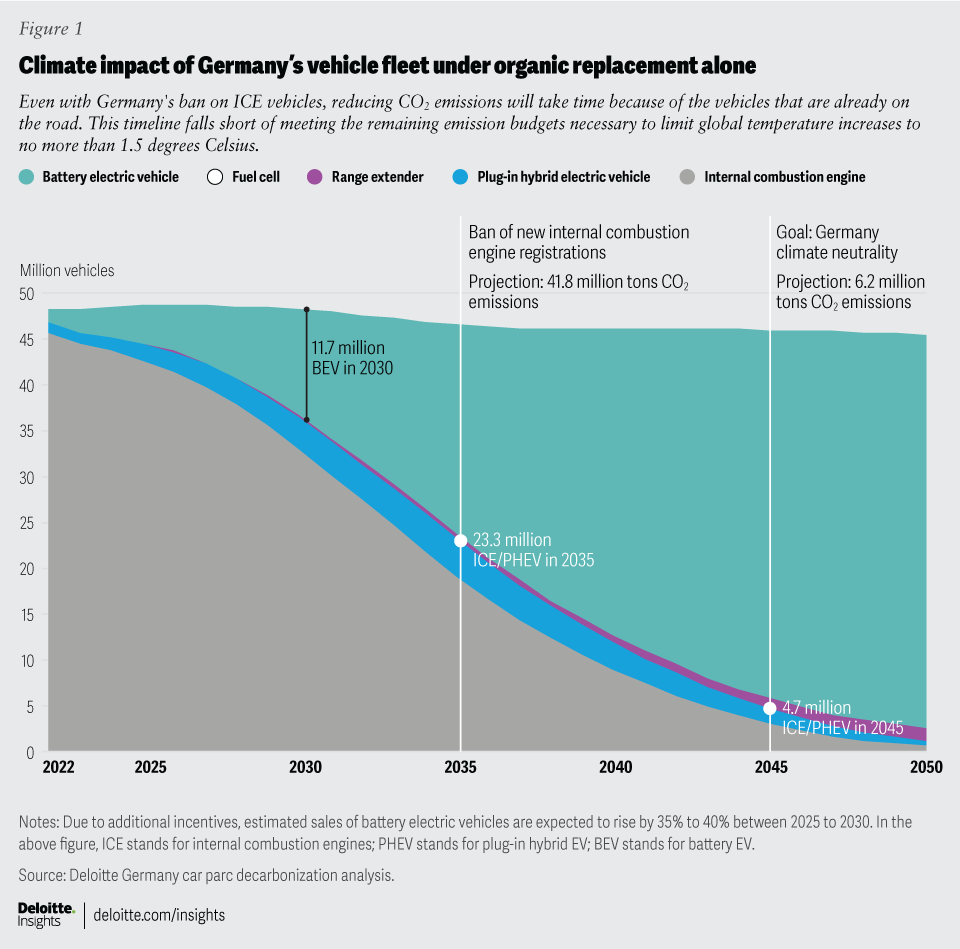

In European cities, local administrations and mayors have already introduced restrictions on driving cars with internal combustion engines. And starting in 2035, the European Union will not allow registration of vehicles that are not zero-emission.5 It’s an important first step in decarbonizing transportation, but we know it won’t be enough because of the gas-powered cars that are already on the road. When the transition takes place in Germany, for example, about half of the passenger vehicle fleet—around 23.3 million vehicles based on our analysis—will still use ICE technology.

Customers tend to drive their vehicles for about 15 years, so even with the expected increase in battery EV sales, our research suggests that the sector’s emissions will not fall. The sectoral targets established in the “Fit for 55 package,” which is a set of proposals by the European Commission aimed at reducing the EU’s greenhouse gas emissions by 55% by 2030, passed in June 2022, will be exceeded.6 A paradigm shift across the automotive sector is essential to help drive down the carbon footprint of the existing fleet of ICE cars currently on the road, ensuring a sustainable and cleaner future for transportation.

Q: What are some of the important aspects we collectively need to think about to solve this challenge?

A: This is a global challenge, and it requires an approach that can tap into the needs of the different stakeholders that have an influence on the transition, namely customers, car manufacturers, regulators, and policymakers. They each have unique perspectives that cannot be neglected.

The person who owns an internal combustion engine car, for example, may be aware of their carbon footprint, but they may not want to scrap it if it’s still running because it might be paid off, or they may not be able to afford to replace it. Is it worth the extra expense to cut their personal carbon emissions?

Regulators, on the other hand, are looking holistically at the carbon footprint of the passenger vehicle fleet, with an eye toward making manufacturers accountable for the full life cycle emissions of their products.

This, in turn, poses a new challenge for car manufacturers, who have been otherwise focused on expanding participation in the EV market (rather than addressing the damage done by the ICE vehicles that are still in circulation).

To help make this transformation accessible, practical, and relevant to the people, policymakers may need to introduce cleaner alternatives. Once the EU stops producing gas-powered vehicles, it should increase the demand for ones with zero emissions, both new and used. If the policies are too restrictive, though, there is a risk of economic and social impacts that could be unevenly distributed among the society. Instead, regulators should strive for a balanced resolution that distributes these impacts in an equitable manner, so they’re not shouldered by those most vulnerable. Planning for a just transition in the automotive space can also create new opportunities.

In our study, we looked at data from the German auto market7 to develop a framework that includes several different policy actions. We considered approaches like incentives for replacing old vehicles, penalties and perks for the industry, and subsidies that span across different sectors. We then looked at how these types of policies could impact different types of vehicles and customer groups.

Q: It’s interesting to think about each of the factors underlying the transition. It sounds like we need different strategies to influence change in different ways based on the stage of decarbonization. How does your model work through those questions?

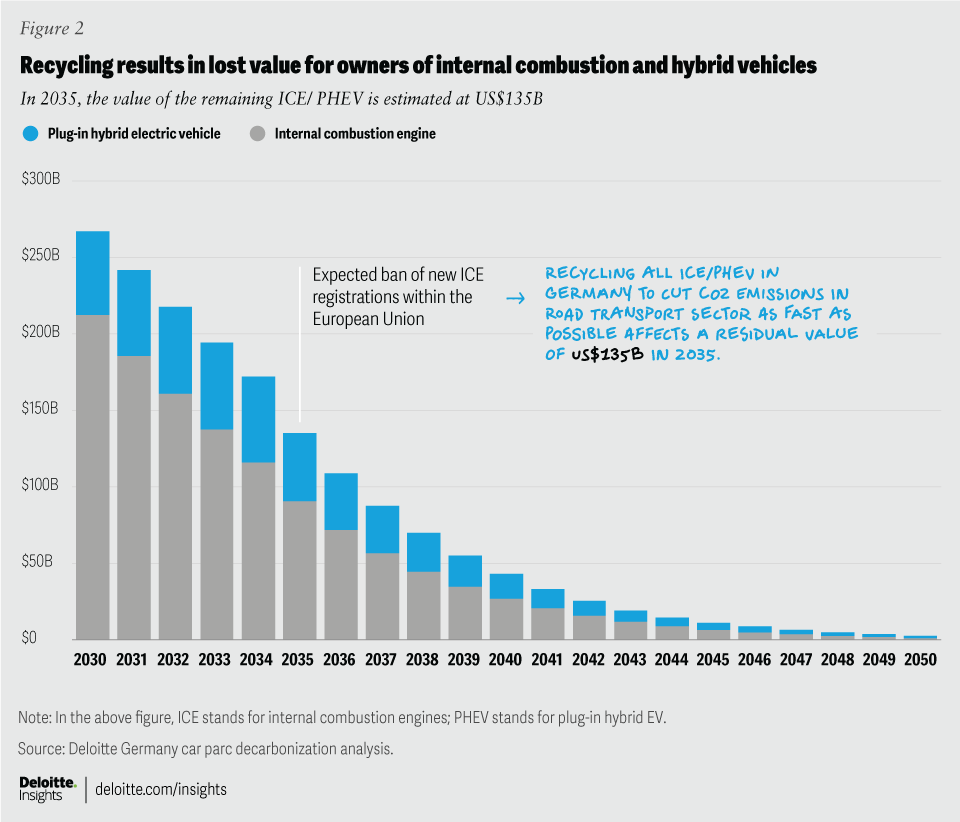

A: In our study of the German market, we created a tool that calculates the carbon dioxide emissions of the remaining internal combustion engine fleet until 2050. We also put a price tag on the remaining ICE fleet, estimating the number of vehicles per type and age, as well as their residual value (what the car is worth to consumers at a given time). For Germany, the residual value of the ICE vehicle fleet in the year 2035 came to about US$135 billion.

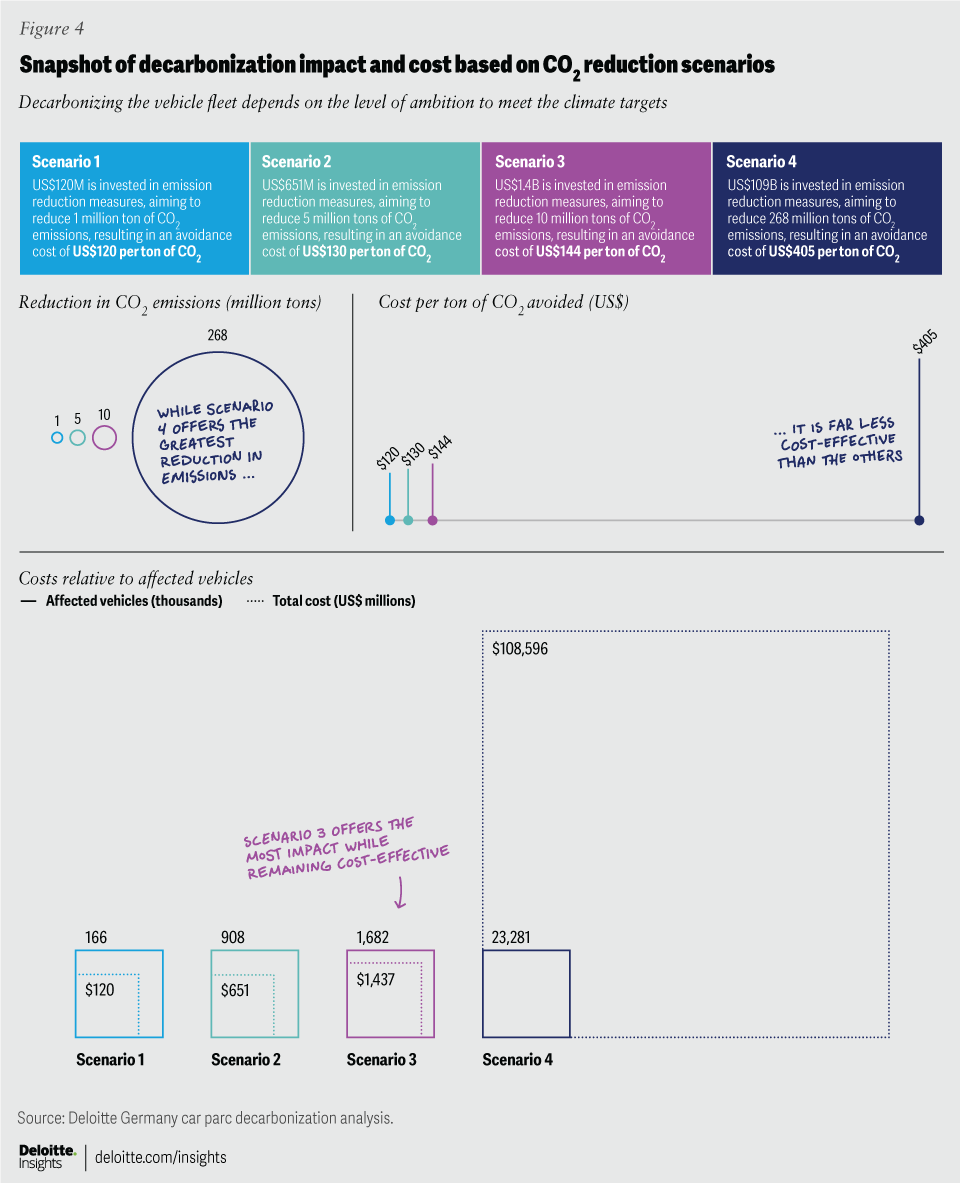

By calculating a vehicle’s value relative to its expected CO2 emissions over the remainder of its useful life, the tool can help policymakers, operators, and business leaders identify which cars should be removed from circulation first. This calculation involves comparing the vehicle’s residual value to its recycling value (what the car’s materials could be sold for if it were recycled). We then considered the expected remaining CO2 emissions for each vehicle. The difference between the two is the emissions avoidance cost.

Using the information from those steps, we can identify which vehicles, if removed from the market, could offer the most significant reduction in emissions for the lowest cost.

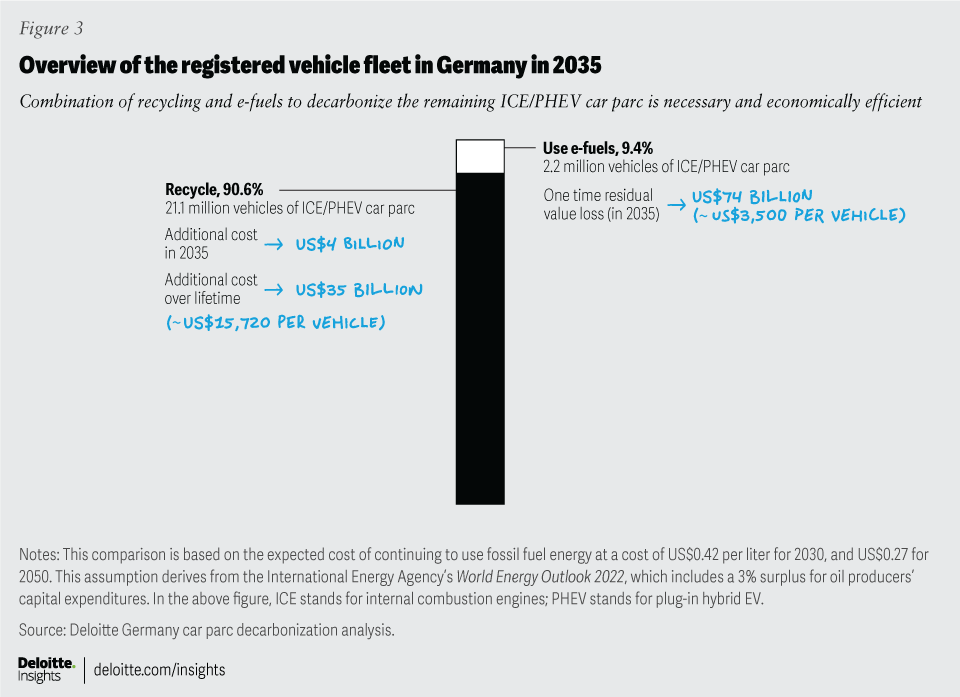

Finally, we explored other viable solutions available to help address decarbonization, which come down to two main solutions: either recycling the ICE cars or converting them to use synthetic e-fuels.

If we limit our focus to recycling alone, individuals could lose up to 90% of the residual value of their cars, which for Germany totaled about US$125 billion. Depending on the vehicle type, the emission avoidance cost from recycling ranges between US$120 and US$2,700 per CO2 ton. In this scenario, a huge amount of emissions from ICE vehicles get wiped instantly from the market, but there is uncertainty about future payments to the lenders who have been financing these vehicles.

Decarbonizing the fleet by running ICE vehicles on e-fuel is another option, which our analysis shows offers emission avoidance costs in the range of US$637 to US$777 per ton of CO2 equivalent (CO2e). Currently, though, it is constrained by the cost of producing e-fuels, which is higher than that of producing fossil fuels. This might change in the future; the cost of e-fuel prices is expected to fall from US$3.72 today to US$1.50 by 2050,8 according to Deloitte Germany’s economic model developed in collaboration with Agora Verkehrswende. However, investing heavily in e-fuel production infrastructure may not be a cost-effective strategy in the long run, as demand for such fuels is expected to diminish as the number of ICE vehicles out there dwindles.

Q: Does your research suggest a best-case scenario strategy? What are some of the risks and benefits associated with it?

A: Our solution suggests reframing the problem as a new business model. Automakers have a distinct opportunity to boost their profits by transforming themselves from product manufacturers into transportation service providers that actively support decarbonization. This could take the form of not only selling more zero-emission vehicles but also fostering alternative business models and diversifying revenue streams. Automakers could gain control over the existing internal combustion vehicle fleet through a “buy and lease” program, where the company effectively buys back the cars they sold to customers, and then offers a lease as a monthly subscription. Companies can then use their asset management capabilities to replace the fleet more efficiently with new zero-emission vehicles.

Q: How does the simulation you ran on Germany compare with what you might expect from other markets such as China and the United States? Do you feel like there is a strong appetite for this type of change or is it going to be a hard sell?

A: The transition will likely take place at varying speeds worldwide, so the proposed changes have similar implications for other auto markets like China and the US, but the magnitude could be much larger. In China, there are many new and lesser-known electric car manufacturers leading the transformation, particularly in the bigger cities. The EU has been in this transition for quite some time, so they have a very robust and evolved biofuel directive and legislative framework that differs from the United States, considering the existing fuel standards. When it comes to the commitments countries have made as part of the Paris Agreement, for example, Germany’s nationally determined contribution is also different than that of the United States; Germany has attached great importance to investments in alternative fuel production and infrastructure to reduce emissions.9

Q: You have talked about transitioning people from ownership to usership, but how do you address the emotional attachment that many people feel to their car? How do you help them overcome what they’re used to?

A: The transformation is possible and sustainable if there is adequate charging infrastructure available. Beyond other factors, people will potentially switch to an electric car if the city offers them easy, frequent, and accessible charging infrastructure.

The way people use vehicles is likely to change in the future. The old notion of car ownership may go away as people move toward a car-sharing or leasing model. More and more companies actively support this transition by offering “mobility budgets” to their employees for various transportation options. The emotional attachment aspect may transform into a new set of customer aspirations around being able to get around in a better, newer, and environmentally friendly vehicle. In this transformation, it is important that the relevant solutions generate added value for customers, car manufacturers, regulators, and policymakers alike. Only if we succeed in seeing the transformation as an opportunity and as a business model will it be successful. We will not succeed with pure bans and pure regulation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}