What can we learn from the last recession? Preparing for a new wave of M&A in the automotive sector

7 minute read

20 October 2020

An unprecedented health crisis is causing major financial disruptions for businesses across the automotive value chain. An increasing number of distressed assets may be leading to an upturn in M&A activity. Lessons learned from the last recession can provide valuable insights for companies looking to navigate turbulent market conditions.

The COVID-19 pandemic has had a significant impact on the automotive industry. Demand for new personal vehicles took a significant hit in the first half of the year as health and financial concerns interrupted traditional automotive shopping behaviors.1 Current industry forecasts suggest US light vehicle sales will drop roughly 3.1 million units or 18% from 17.1 million units in 2019 to 14 million units this year, representing a downward revision of 2.8 million units compared to expectations released in January.2 In an effort to restart business activity, some auto companies have resumed operations to varying degrees of success.3 However, a return to normal conditions is highly dependent on efforts to mitigate the spread and impact of the virus.4

Learn more

Explore the automotive collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

From a financial perspective, both automotive original equipment manufacturers (OEMs) and suppliers are experiencing significant cash flow disruptions and are looking to various mitigation strategies, including gaining access to government support programs, drawing down on lines of credit, finding alternative sources of financing, and living off existing working capital. OEMs and large, tier-one automotive suppliers have generally been better positioned in the short term to tap into existing debt facilities and alternative financing to address cash burn concerns. However, almost every company has considered cost-cutting measures, such as furloughs, reduction of work hours, and discretionary spending freezes, in an effort to preserve liquidity. Small- to mid-sized suppliers are also looking to OEMs for prepayments and other forms of financial support in order to help build the working capital necessary to ramp back up to full production. To be sure, some companies entered the pandemic in a much better financial position relative to their peers. Conversely, those companies that have been slower to react or unable to secure financial support are under intense financial pressure that may well lead to an increasing number of distressed assets across selected portions of the automotive value chain. This situation may eventually lead to a significant pickup in the number of mergers and acquisitions (M&A) across the sector.

Companies that have been slower to react or unable to secure financial support are under intense financial pressure that may well lead to an increasing number of distressed assets across the automotive value chain.

As the pandemic continues to unfold, both the government and individual businesses are trying to understand and predict what a return to normal market conditions may look like. Obviously, people are looking back to the 2008 financial recession for any learnings that could help guide a recovery effort. Although there are a number of significant differences between the two crises, there were some critical lessons learned that can provide valuable insight into what to expect from an M&A standpoint in the automotive sector going forward (figure 1). It’s also important to note that the current situation remains highly dynamic. As a result, many current market observations may not fully capture the potential distress that could result from the continuing impact of the pandemic.

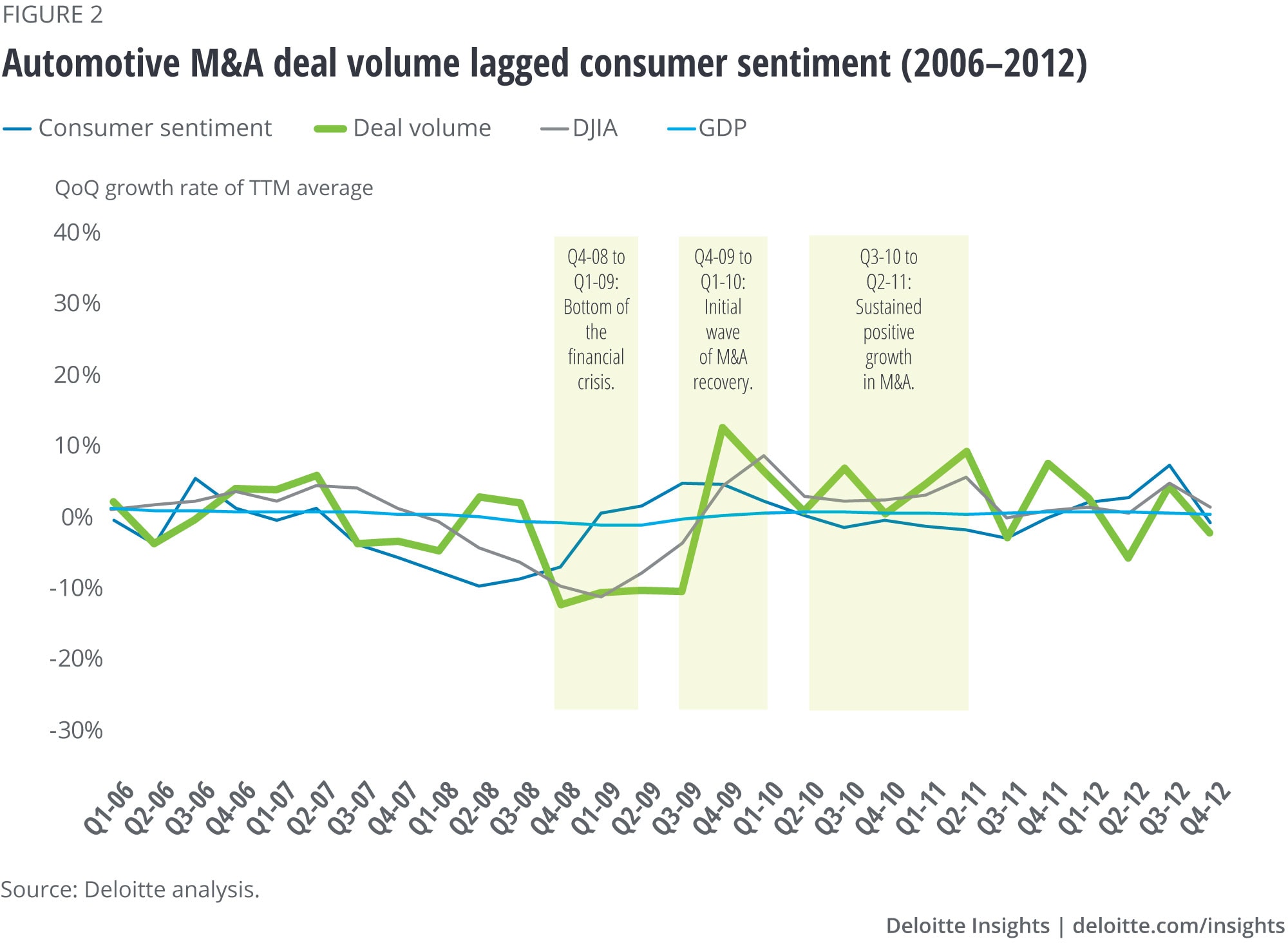

In order to anticipate what may occur as a result of the current pandemic, it can also be useful to take a deeper dive into the specific trends occurring in the automotive M&A space before, during, and after the 2008 financial crisis (figure 2).

The automotive M&A market did not immediately recover from the bottom of the 2008 financial crisis. In fact, it lagged the recovery of consumer sentiment, GDP, and the Dow Jones Industrial Average or DJIA by approximately nine months. That was followed by a 12-month period of relatively sustained growth in automotive deal volume starting Q2 2010.

During the initial wave of transaction activity between Q3 2009 and Q1 2010, approximately 70% of deals were driven by private equity and other investor group buyers.5 Analysis of the individual transactions during that period reveals that deal volume was primarily focused on commodity parts suppliers, but at transaction multiples that were well below predownturn levels. Corporate buyers were more prevalent during the secondary phase of transaction activity between Q2 2010 and Q2 2011, which focused on more value-add subsectors.

Overall, the recovery in automotive M&A transactions from the last recession was led by asset divestitures and surgical carve-outs that increased 56% from 2006 to 2009. During this period, transaction values were largely below US$250 million as OEMs and suppliers exited noncore or distressed portions of their portfolio.6

Following that period, the industry went through a 10-year cycle of economic expansion and transaction activity. In fact, the last six quarters of M&A activity immediately preceding the COVID-19 outbreak were characterized by trading at relatively high EBITDA multiples, 77% higher than the 2008 financial crisis recovery period, largely driven by activity in the high-tech supplier space. In addition, deals involving private equity players showcased multiples that exceeded those involving corporate acquirers. In the COVID-19 environment, overall automotive deal volume has declined 41% on a quarterly basis from Q4 2019 to Q2 2020, a trend that has continued into Q3 2020 and may persist depending on the lasting impact of COVID-19 containment measures.7

What to expect when you’re expecting M&A recovery

Going forward, the M&A environment will likely recover. Based on our analysis of the 2008 financial crisis data compared to what we have seen so far during the pandemic, we expect to see the following play out in the automotive industry:

- Private equity and other financial investors will likely lead an initial wave of recovery as they did in 2009 by deploying capital with a focus on distressed assets and surgical carve-outs at more compressed multiples than those heading into the pandemic. We also expect strong access to capital as the top 400-plus private equity investors (PEIs) that are active in the automotive industry have over US$1.2 trillion of unallocated “dry powder” as of September 8, 2020.8 In fact, PEIs have approximately double the available cash to invest now compared to the period immediately following the 2008 financial crisis.

- Companies with strong balance sheets heading into the pandemic and those who have access to financing will likely be active buyers in the recovery. They will likely focus on opportunities to advance their position on desired technologies by keenly targeting synergistic opportunities while taking advantage of depressed EBITDA multiples.

- Strategic decisions to exit noncore, distressed, and less-profitable global markets and vehicle segments may be accelerated due to liquidity issues. We also expect an uptick in divestitures and surgical carve-outs, similar to those observed in the 2008 ̶ 2009 timeframe.

- The parts supplier sector will likely lead the way in M&A activity. Such activity will be focused on smaller entities and transaction values. In fact, small- and medium-sized suppliers that lack the ability to secure financing will likely be an attractive target for several types of buyers, including:

- Private equity players looking for a high return on invested capital

- Entities looking for attractive bolt-on opportunities

- OEMs looking to mitigate risk and/or create efficiencies by strategically consolidating their supply chains through direct investment or prepackaged marriages

- Companies in lower-tech subsectors will likely be the initial target of deal activity. However, unlike 2008, we expect the number of technology-driven deals to recover quickly as a result of the significant focus on advanced vehicle features created over the last decade. In fact, we already see this playing out in the special purpose acquisition company (SPAC) market.

- The uncertainty of COVID-19’s impact on financial performance could drive an increase in earnouts in future deals. Since such earnouts will likely be based on adjusted EBITDA post-close, there will likely be increased scrutiny and negotiation of EBITDA adjustments between the parties.

- Finally, protracted deal timelines will likely result from additional considerations, such as cross-border trade.

Although the number of transactions is likely to rise with more distressed assets emerging in the sector, higher transaction multiples may not fully materialize, outside of the high-tech space, while the market and overall economy digest the impact of COVID-19. In the meantime, there are a variety of key considerations for companies on either side of a potential transaction.

Five things companies should consider in a post ̶ COVID-19 M&A world

- PEI buyers were able to act quickly during the last recession to take advantage of depressed EBITDA multiples. Corporate buyers looking to acquire advanced technology capabilities now can learn from that by streamlining a deal process to avoid losing out and having to pay more later on.

- Companies with distressed assets that can adequately invest in the time and resources required to prepare for a potential divestiture or sale process will likely realize a higher multiple than those that don’t focus on divestiture/sale.

- Resilient companies looking to take advantage of heightened interest in the sector by potential buyers should invest in the resources necessary to evaluate market conditions and properly position nondistressed assets for maximum value creation.

- Since the last recession, both the cost of regulatory compliance and efforts to globalize the automotive supply chain have increased significantly. At the same time, trade relations between some countries have become strained. As a result, buyers and sellers should consider the impact of these trends on potential transactions in a post ̶ COVID-19 environment.

- Buyers and sellers should properly evaluate the ongoing impact of COVID-19 to adjust EBITDA through the diligence process. The impact of the pandemic may also lead to working capital methods not commonly seen in the past to protect both buyers and sellers upon transaction close. These methods could include the use of net working capital collars, clawbacks, or use of forecasted versus historical working capital when setting a working capital peg.

To be sure, there is a tremendous amount of uncertainty in the automotive sector going forward. In many ways, the pandemic has acted as an accelerant for underlying financial pressures already threatening an industry heading into a period of declining demand. However, looking back at the last economic recession can provide some important clues in terms of what we are likely to see transpire on the automotive M&A front over the next several months.

Financial buyers have a significant opportunity to take advantage of a low transaction multiple to consolidate commodity-driven supply subsectors. That said, corporate buyers can use acquisition opportunities to strategically de-risk their supply chains and strengthen their position relative to advanced technologies. Going forward, the number of automotive M&A deals is likely to grow as governments’ support programs begin to dissipate, leaving weaker companies exposed to additional financial pressure. Overall, companies that use the learnings from the past recession will likely be best positioned to take full advantage of the M&A environment created by the pandemic.

M&A Transaction Services

In our M&A transaction services we make maximum use of experts in each area and of the Deloitte global network to support effective decision-making through apt information collection and analysis.

Learn more

Get in touch

- John Roop

- Risk and Financial Advisory leader

- Partner, Deloitte USA

- jroop@deloitte.com

- +1 312 613 2389

© 2021. See Terms of Use for more information.

Related content

More on the automotive industry

-

Software is transforming the automotive world Article4 years ago

Software is transforming the automotive world Article4 years ago -

Deloitte City Mobility Index 2020 Collection4 years ago

Deloitte City Mobility Index 2020 Collection4 years ago -

How the pandemic is changing the future of automotive Article4 years ago

How the pandemic is changing the future of automotive Article4 years ago -

The futures of mobility after COVID-19 Article4 years ago

The futures of mobility after COVID-19 Article4 years ago -

Transformation and disruption for automotive suppliers Article5 years ago

Transformation and disruption for automotive suppliers Article5 years ago