Recognizing the value of bank branches in a digital world Findings from the global digital banking survey

8 minute read

14 February 2019

Bank branches are still valuable to customers, even those who mostly use digital channels. Learn how banks can transform branches to enhance the customer experience and create more opportunities to connect with customers.

Banks around the world are in the midst of a sweeping digital transformation agenda, yet for many, realizing the true potential of these changes remain elusive. What role should bank branches play in this transformation, and why? In our third article in Deloitte’s global digital banking consumer survey series, we highlight the potential value of bank branches in an increasingly digital world.

Learn More

View the report PDF

Read the full results of the Global Digital Banking Survey

Explore the Financial services collection

Subscribe to receive related content

Bank branches are still relevant in a digital world

Based on a proprietary global survey (see sidebar, ”Methodology” for more details), we found that branches remain the dominant channel for account opening and customer satisfaction with branches is a stronger determinant of overall satisfaction than either the online or the mobile channels. In this article, we explore how these dynamics play out across different countries and customer types, and offer recommendations on what banks could be doing to rethink the branch experience in an increasingly digital world.

Methodology

The Deloitte Center for Financial Services surveyed 17,100 banking consumers across 17 countries to measure a range of banking attitudes, behaviors, and preferences. Among other questions, we asked respondents about their channel usage for various products and services.

Using this data, we built a linear regression model with overall satisfaction with the bank as the dependent variable and satisfaction with individual channels—branches, ATMs, contact centers, online, and mobile apps—as the independent variable. We included responses from only those consumers who had used all the above-mentioned channels (n=8,000).

The R-squared was low (0.18), which is not surprising given that the overall satisfaction with a bank typically depends on a number of factors beyond channel satisfaction. However, the model fit and the coefficients were significant (except for ATM satisfaction) to understand the relationships between channel satisfaction and overall satisfaction. The purpose of the model is not to predict overall satisfaction but to understand the relationships between channel satisfaction and overall satisfaction. Despite the low R-squared, we consider the model results to be quite revealing because of the significant coefficients.

Branches are the dominant channel for account opening

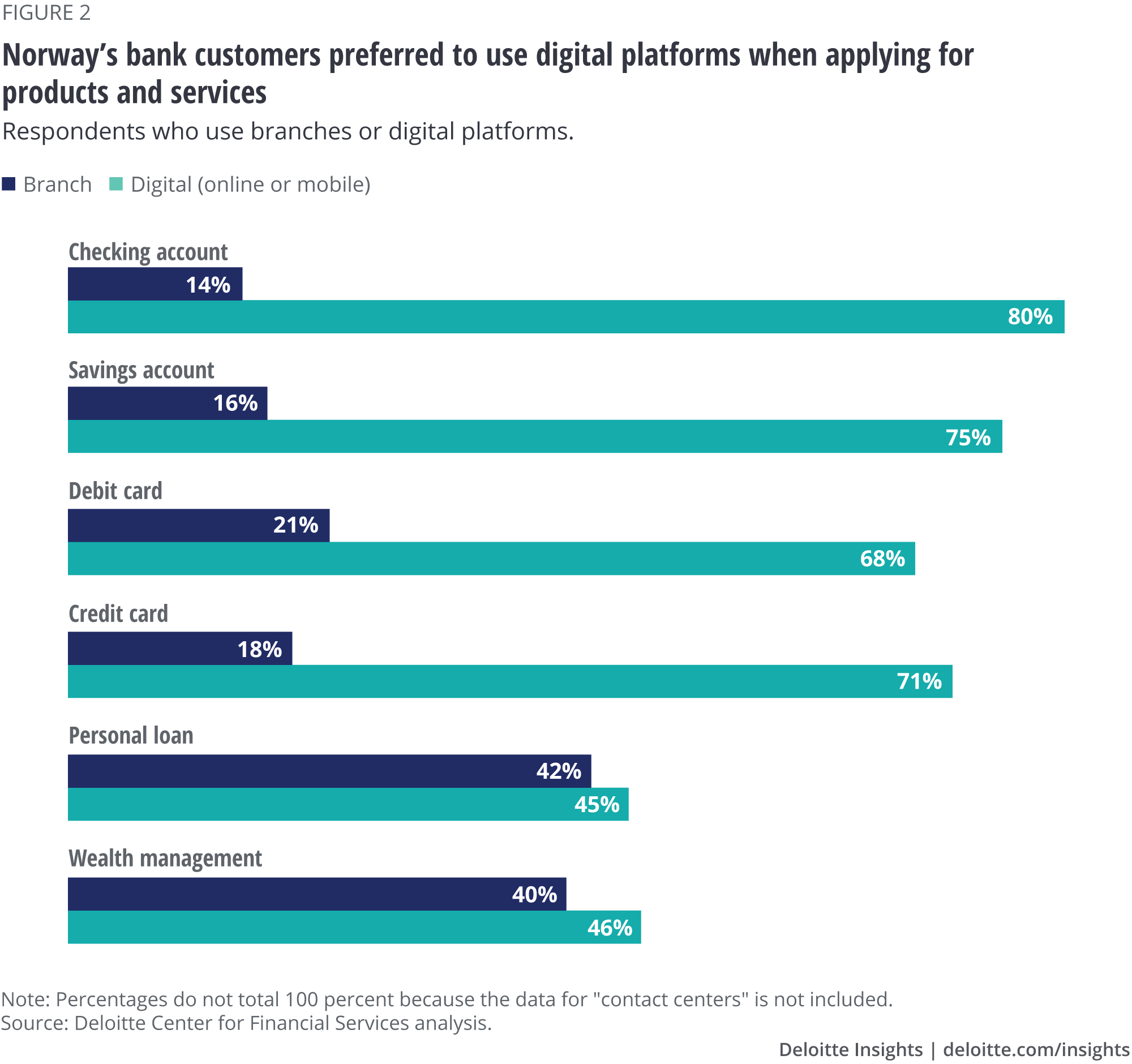

The survey revealed that most customers prefer branches over digital channels when opening new accounts for both simple (such as savings accounts and debit cards) and complex products (such as loans). This was true in developing countries, such as Mexico and Indonesia, as well as in developed countries, such as Spain, France, Germany, Japan, the United States, Canada, and Switzerland (figure 1). However, in Norway, one of the leading countries for digital channel usage, customers surveyed said they prefer digital channels over branches when applying for simple products, such as checking accounts, savings accounts, debit cards, and credit cards (see sidebar, “Digital product application in Norway”).

This preference for branches in opening new accounts is uniform across generations—baby boomers, Gen Xers, millennials, and even the youngest consumers, Generation Z. For instance, 64 percent of boomers, 54 percent of Gen Xers, 48 percent of millennials, and 56 percent of Gen Z consumers surveyed said they prefer to visit branches when opening a new checking account.

Digital product application in Norway

Norway is a mature market for digital banking services. It ranks in the world’s top 10 countries with the highest internet penetration (with 99 percent of its population using the internet in 2017).1 Norwegian customers in our survey are avid users of online and mobile banking services for both transactional and informational services, such as bill payments (97 percent of the Norwegian customers surveyed used digital channels) or updating account details (96 percent of the Norwegian customers surveyed used digital channels). They also clearly prefer to use digital channels when applying for new products (figure 2).

Norwegian banks appear to have capitalized on these developments. DNB Bank, for instance, digitized its mortgage application platform in 2017.2 Customers can now apply for mortgages on their mobile apps. The bank is now planning to streamline the loan process for its commercial clients.3

The branch experience influences customer satisfaction more than online or mobile channels

It is well-known that high customer satisfaction yields more loyalty, advocacy, and product ownership or share of wallet.4 Our survey also validated that highly satisfied customers are more likely to recommend their bank to others and are less likely to switch their primary bank (8 percent likelihood) than dissatisfied customers (18 percent likelihood).

Our regression model results show that the effects of satisfaction with branches and contact centers on overall satisfaction are at least twice as large as satisfaction with online or mobile channels (see figure 3 and sidebar, “Methodology”).

In our previous article, Accelerating digital transformation in banking, we identified three groups of customers: traditionalists, bank customers most reliant on traditional channels versus online or mobile; online embracers, customers who used digital channels frequently, online more than mobile; and digital adventurers, those most likely to use digital channels (both online and mobile apps). We found that branch satisfaction has a higher influence on overall satisfaction compared to satisfaction with digital channels for all the three customer segments.

Why are traditional channels a stronger determinant of overall satisfaction than digital channels?

We believe there may be a few reasons behind the higher influence of traditional channels on overall customer satisfaction. First, favorable or unfavorable experiences during moments that matter can have lasting impressions. Due to the typical complexity and/or urgency of these interactions, account opening and problem resolution are two critical interactions that customers are likely to make in channels involving the human touch—typically, branches and call centers. For instance, in our survey, more than four in 10 customers who disputed a transaction or filed a complaint did so through contact centers. Branches were the second-most used channel for these activities.

Customers must expend time and effort carrying out these types of transactions, which makes them important experiences. Imagine a customer having to wait 10 minutes before they connect with a call center representative to discuss a simple query or interacting with an unsympathetic bank representative at a branch. The negative impressions resulting from these interactions can stay in customers’ minds for a long time. On the other hand, customers may experience high satisfaction if a query at the call center was handled efficiently or if they had a successful meeting with the relationship manager in the branch, which would far exceed their satisfaction from paying bills online or on the mobile app without a hitch.

Second, branches tend to be a symbol of trust. And, given money matters are complex and personal, trust has played a foundational role in banks’ safekeeping and depository functions. Our survey confirmed that more respondents used branches to make deposits than other channels. Branches also foster brand image and help maintain relationships with customers.5

Third, branches also provide easy access to banking services: 68 percent of respondents to our survey believe proximity to branches and ATMs is an important or very important attribute in choosing their primary bank. Moreover, more than four in 10 respondents across generations visit a branch at least once a month. Respondents who were likely to switch to a new bank/institution in the next two years cited “closer proximity to branches and ATMs” as the third most important reason for making this change.

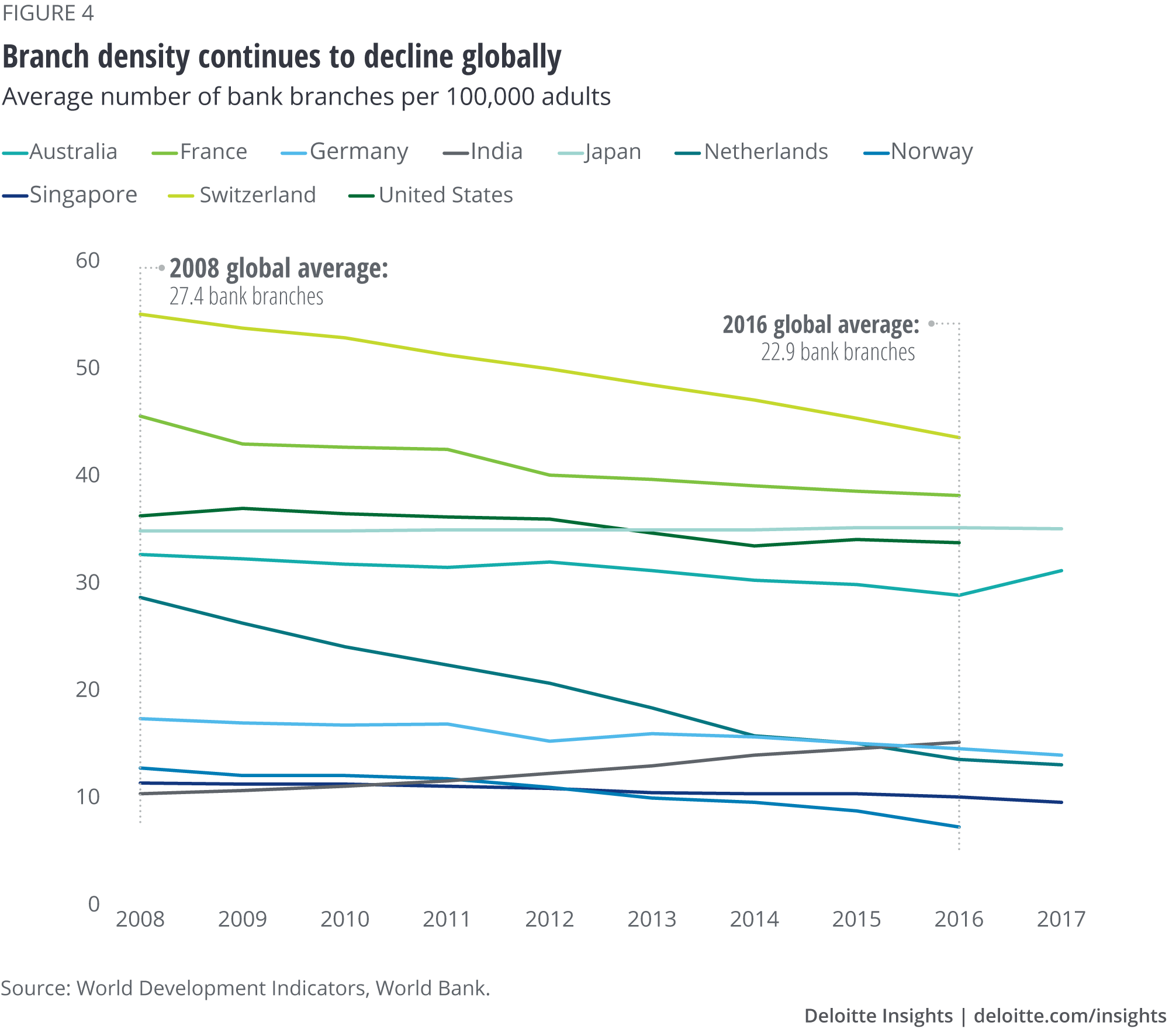

But branch density is declining

In many countries around the world, though, bank branches are closing.6 More than 3,000 branches have been shut down on a net basis in the United States since 2010,7 while in the United Kingdom, more than one-quarter were closed between 2012 and 2017.8 These actions have been in response to cost-cutting pressures and customers’ shift to digital channels for routine transactions, such as bill payments or person to person (P2P) transfers.9

As a result, branch density—the average number of bank branches per 100,000 adults—has declined in many countries. For instance, branch density reduced from 54 branches to 42.5 between 2008 and 2016 in Switzerland. In Norway, which is digitally more advanced than most countries,10 branch density dropped from 11.7 branches in 2008 to 6.2 in 2016 (figure 4).11

While closing some bank branches is a business decision that may make sense for a variety of reasons, it seems as though banks should not completely give up on branches yet. Our survey findings tell a compelling story about the unique value branches can provide to customers and the key role branches often play in building and sustaining strong retail banking franchises. For this reason, we would caution bank leaders against viewing branches merely as another stand-alone channel. Instead, leaders could adopt a strategy that fully and seamlessly integrates branches into the banks’ overall digital transformation strategy.

Reimagining branch transformation

How can bank leaders strike the right balance between physical and digital footprints? The following strategies should be considered:

Invest in branch talent. As digital simplifies the banking experience in branches, banks should continue to focus branch workforce training on ensuring high-quality interactions with customers and creating positive moments that matter. Our 2017 study on account opening underscored the need for “attentive and empathetic human interaction by frontline staff during the account opening process.”12 In this vein, to help answer clients’ complex questions about market trends, UBS trained 10 wealth management advisers in Switzerland to use the digital clone of its chief economist and chief investment officer.13 BBVA Compass is using certifications to help train its frontline staff on methods to help customers with their complex queries and decisions.14

Blend the human touch with technology. One-third of the customers in our survey said they would be open to using branches more if banks offered certain digital capabilities that would enhance convenience. These enhancements included extending service hours through virtual remote services with a representative (36 percent), offering digital self-service screens with a representative’s help if needed (34 percent), and being able to schedule a virtual video meeting with a bank representative (31 percent). Interestingly, all of these options focus on how digital can drive high-touch interactions with a bank representative, either remotely or in-person. While these approaches are not new, they are not yet widespread, although more banks are beginning to experiment with them.

HSBC, for instance, introduced a robot—Pepper—in its flagship Fifth Avenue branch in Manhattan. The idea behind having a robot in the branch was never about replacing bank tellers; rather, it was designed to make the banking experience more appealing.15 Pepper is programmed to answer customers’ basic questions and direct them to the right adviser/personnel in the branch.

Similarly, NatWest bank in the United Kingdom introduced its AI-powered bot, Cora, to answer customers’ basic queries in one of its branches in 2018.16 The bot can also be used with internet and mobile banking.

Accelerate the transition to a seamless omnichannel integration. In our survey, seven in 10 customers considered having a consistent omnichannel experience as important or very important when selecting a primary bank. Reimagining branches of the future is expected to entail breaking the channel silos between physical and digital channels and allowing customers to seamlessly move from one channel to another. ING Bank in the Netherlands, for example, allows customers to schedule appointments with the bank representatives at the branch via their online banking portal.17

Provide a sense of community. Branch visits can go beyond completing transactions and gathering information. They can become enjoyable experiences. Nearly 31 percent of customers in the survey globally said they would be likely or very likely to increase visits to a branch if it resembled a café, where they could plug in, hang out, and work. Some banks are experimenting with this trend: To lure millennials, Capital One opened new café branches with cafés that are a far cry from traditional branches.18 In the Capital One cafés, customers can connect with “café coaches,” onsite bank representatives who are available to chat over a cup of coffee about different banking products, or they can choose to just hangout with friends and enjoy the café’s food and free Wi-Fi.19

Embrace the human touch in digital channels. Digital does not, and should not, mean a lack of personal interactions. Banks should replicate the branch experience, especially the responsiveness and empathy, in digital channels—be it in online banking, on mobile apps, or at ATMs.

Final thoughts

In this article, we discussed why bank branches remain valuable to customers in this digital age of speed and convenience. Perhaps most important, branches should be considered the most powerful channel banks have to provide customers with high-touch, person-to-person experiences. Our survey showed in several circumstances, customers still prefer the human touch, which branches can amply provide—especially when applying for new products, such as opening a checking account.

We also made suggestions on how banks could make the most of their branch networks, integrating digital and technology advancements into the branch experience and, conversely, encouraging the human touch in digital experiences. As bank leaders execute on their digital transformation strategies, we urge them to fully recognize the value branches offer and keep customer preferences on top of mind when repositioning branches.

Deloitte Consulting

Innovation, transformation, and leadership occur in many ways. At Deloitte, our ability to help solve clients’ most complex issues is distinct. We deliver strategy and implementation, from a business and technology view, to help you lead in the markets where you compete.

Learn more

Contact

- Angus Ross

- Managing director

- Deloitte Consulting LLP

- angusross@deloitte.com

- +1 347 449 2664

© 2021. See Terms of Use for more information.

Explore more in Financial Services

-

A moving target: Refocusing risk and resiliency amidst continued uncertainty Article4 years ago

A moving target: Refocusing risk and resiliency amidst continued uncertainty Article4 years ago -

Pricing innovation for credit cards Infographic

Pricing innovation for credit cards Infographic -

Funding takes focus for nonbank online lenders Article6 years ago

Funding takes focus for nonbank online lenders Article6 years ago -

Managed services Article8 years ago

Managed services Article8 years ago