2024 commercial real estate outlook: Finding terra firma

Realigning the global real estate industry to help meet new foundational realities

Article

•

38-min read

•

21 September 2023

•

Deloitte Center for Financial Services

Jeffrey J. Smith

United States

Kathy Feucht

United States

Renea Burns

United States

Tim Coy

United States

Key takeaways

- Expense mitigation is a top priority for most respondents; revenue expectations dropped to their lowest level since we began our survey in 2018. Top areas for expense mitigation are in talent and office space.

- Respondents point to cost of capital and capital availability as the weakest among real estate fundamentals. About half of respondents expect cost of capital (50%) and capital availability (49%) to worsen through 2024, up from 38% and 40%, respectively, last year.

- Many real estate firms aren’t ready to meet environmental, social, and governance (ESG) regulations. Nearly 60% surveyed say their firms lack the data, processes, and internal controls necessary to meet compliance standards.

- Most respondents say they plan to use outsourcing to drive efficiency. Their primary goals are gaining technological capabilities to streamline processes and adding agility and resilience to their operations.

- Real estate firms should address years of amassed technical debt by ramping up technology capabilities. Most respondents (61%) admit their firms’ core technology infrastructures still rely on legacy systems, but nearly half are making efforts to modernize.

Learn more

Getting back on solid ground

Message from our sector leaders

Continuing to confront multiple challenges and shifting expectations, in 2024, the global real estate industry has an opportunity to start rebuilding on more solid ground. Multiple factors, from a pandemic-era recovery that shifted how and where people work to more recent geopolitical uncertainties and financial market instability, the coming year is expected to be pivotal in real estate firms’ ability to recover and build up. Marked by a myriad of mixed signals about the health and trajectory of our industry, real estate leaders may need to find their footing as they shape the next phase of real estate ownership and investment.

The coming 12 to 18 months are expected to be important as real estate firms reposition themselves, and it might take a combination of critical realizations and strategic realignments, some far different from the status quo, to get there.

This year’s commercial real estate outlook aims to help leaders find terra firma—solid ground—that the industry can build upon to meet new foundational realities.

In this year’s report, we advise leaders on how they may be able to establish more efficient, sustainable business through proactive property portfolio structuring and risk mitigation, value creation through green and decarbonization initiatives and tax incentives, and by transforming operations and technology.

The backbone of our report is our annual Global Real Estate Outlook Survey, which reveals what is top of mind for real estate owners and investors across North America, Europe, and Asia/Pacific. Our survey findings are supported by firsthand experience and insights by leaders at select Deloitte real estate clients and by many of Deloitte’s own subject matter specialists and research leaders at the Center for Financial Services.

We hope you find our insights and guidance useful and thought-provoking as you begin your strategic planning for the remainder of 2023 and into 2024. We welcome any opportunity to discuss our findings with you and your organization.

Table of contents

- Getting back on solid ground

- Concerns about a slowdown impact revenues & spending

- Structural expectations shifts across property markets

- Transitioning to a low-carbon future

- Leveraging tax to help strengthen the bottom line

- Evolving hybrid work and transforming operations

- Enhancing real estate technology capabilities

- Building on a stronger foundation for the future

Concerns about a slowdown further weigh on industry revenues and spending

Around the globe, economies remain afloat despite months of warning signs, with lingering uncertainties buoyed by pockets of clarity. Global economies continue to face multiple headwinds heading into 2024: the continued conflict in Ukraine, extreme weather catastrophes, population migration trends, a weaker-than-expected economic recovery in Mainland China, and ongoing risks of financial stress from tightening monetary policies.1 But proactive policy response to the banking turmoil in early 2023, resilient consumer demand, and a stabilization of energy and food prices seem to have settled some nerves.

Regardless of what economic forecasts might come to fruition, Deloitte’s 2024 Real Estate Outlook survey reveals that concerns about the state of the economy will likely continue to be a primary factor in global real estate leaders’ decision-making through 2024 and beyond. The survey includes strategic insights from 750 chief financial officers (CFOs) and their direct reports at major real estate owner and investor firms in 11 countries (see sidebar “Methodology”).

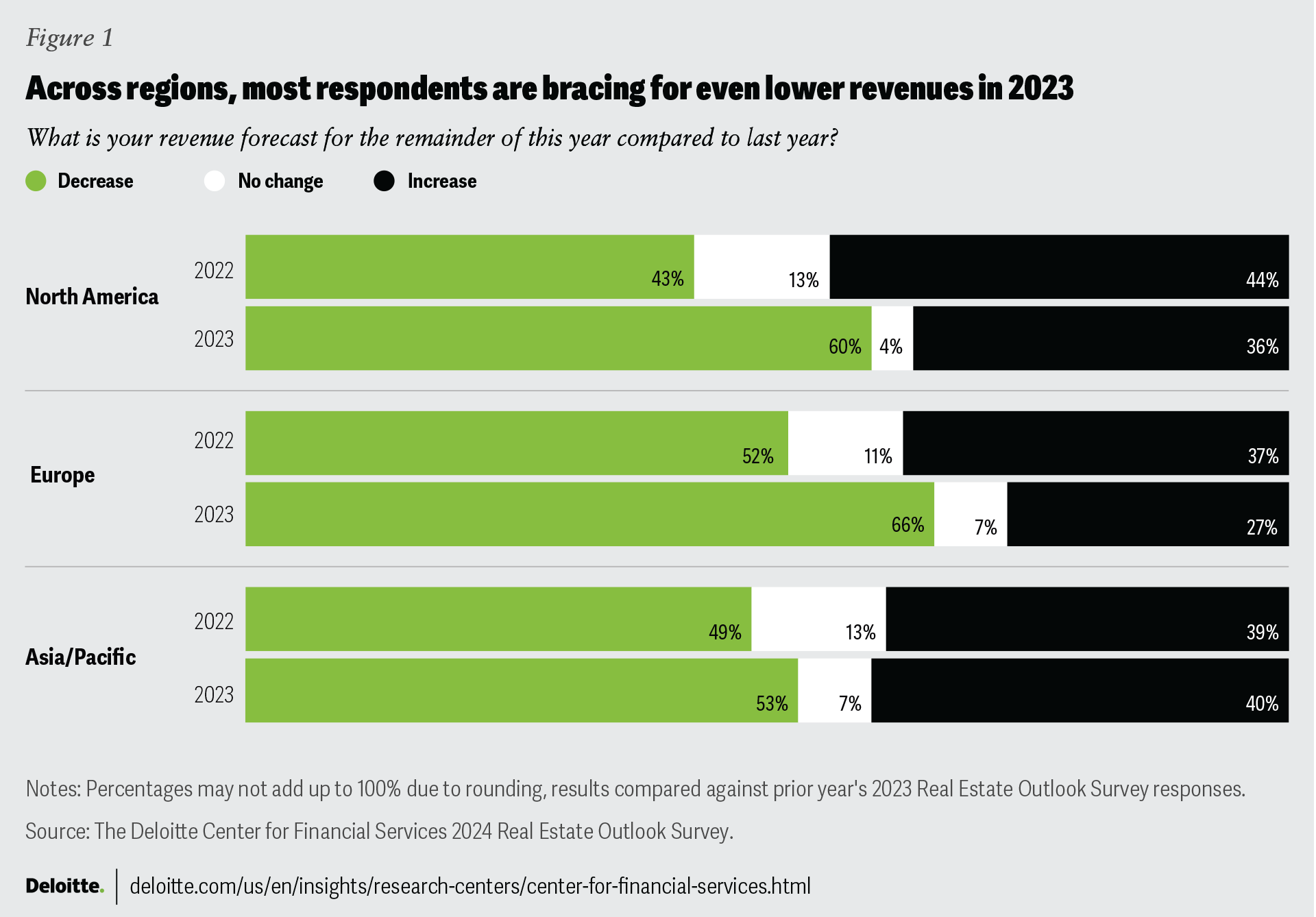

In this year’s survey, revenue expectations fell for the second straight year: Sixty percent of respondents expect declining revenues for the remainder of 2023, compared to 48% last year. Respondents from Europe (66%), North America (60%), and Asia/Pacific (53%) were the most likely to expect falling revenues (figure 1).

With revenue expectations muted for the second straight year, real estate CFOs who participated in our survey plan to continue reducing expenses. Two years ago, only 6% planned to make expense cuts; in 2023, 6% said they’d be cutting; now, 40% say they plan to further reduce spending into 2024. The primary functional areas targeted by respondents for expense reduction will likely be talent (49%) and office space (46%).

Methodology

The Deloitte Center for Financial Services conducted a survey of 750 CFOs and their direct reports at major commercial real estate owners and investment companies around the world.

Respondents were asked to share their opinions on their organizations’ growth prospects and workforce, operations, and technology plans through 2024. We also asked about their investment priorities and anticipated structural changes for the coming 12 to 18 months.

Respondents were distributed among three regions: North America (the United States and Canada); Europe (the United Kingdom, France, Germany, the Netherlands, and Spain); and Asia/Pacific (Australia, Japan, Mainland China, and Singapore).

The survey included real estate companies with assets under management of at least US$50 million and was fielded in June 2023.

Show more

Globally, respondents’ concerns around rising interest rates and the inflated cost of capital are top of mind, placing them near the top of all macroeconomic trends that could most impact financial performance for the next 12 to 18 months. Rising interest rates marked the largest year-over-year increase of all responses, jumping 10 spots from last year’s survey to third this year (figure 2). Of the new options added to this year’s responses, cost of debt emerged as fifth globally and was ranked among the top third in two of the three regions. In Asia/Pacific, the new option of redemption queues/short-term liquidity concerns ranked first in this year’s survey.

Respondents globally grew most concerned about cyber risk, identifying it as the most likely trend to impact their financial performance, especially in Europe, where nearly half of the respondents chose this option (figure 2). This was anticipated as the real estate industry increasingly incorporates smart technologies into their buildings and thus, now faces asset-level vulnerabilities.2

Shifting structural expectations across the property markets

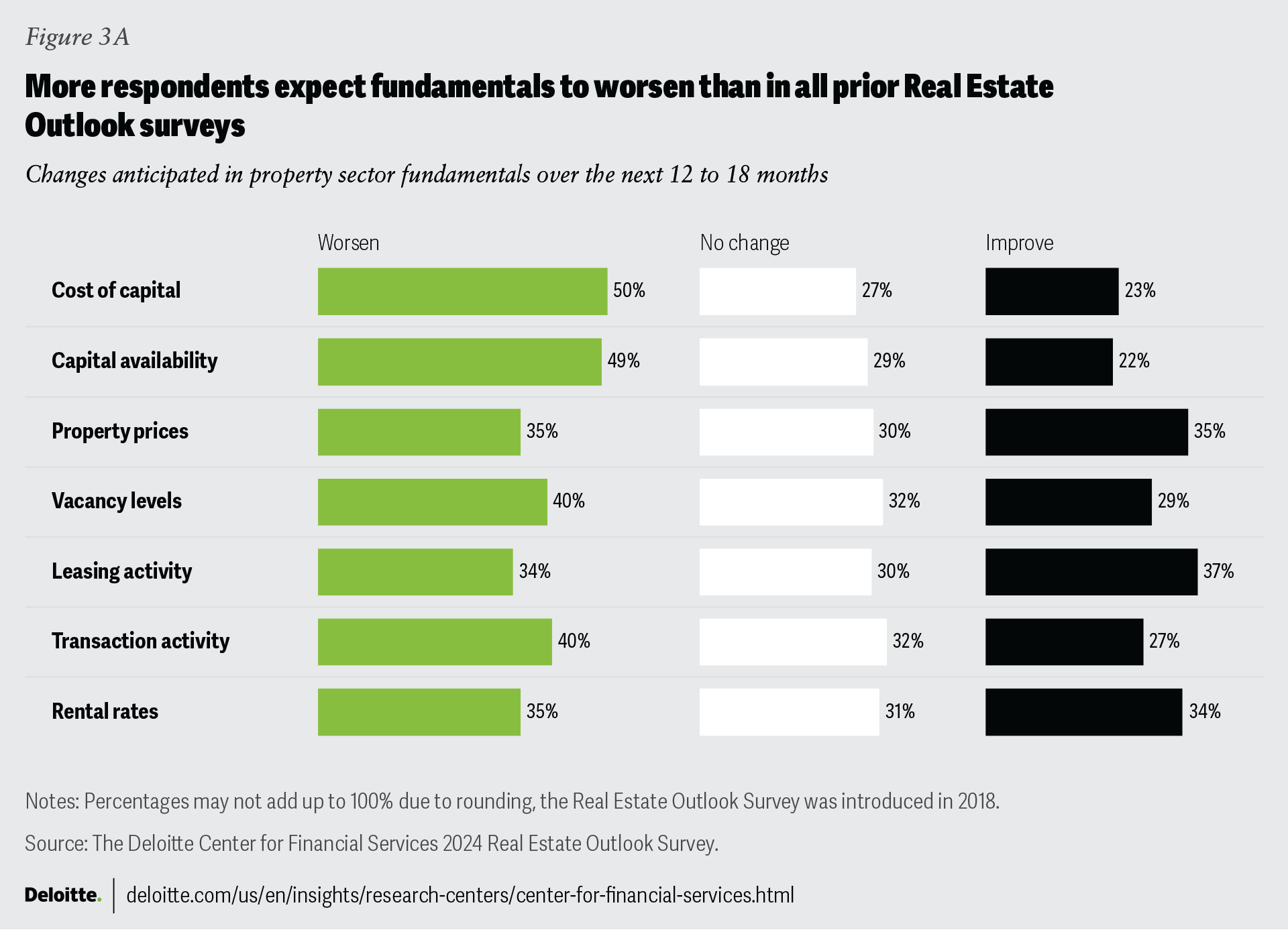

This year’s survey results show the largest share of respondents expecting real estate property sector’s fundamental conditions to worsen since we began the survey in 2018. Following the second straight year of expected revenue declines, additional expense reduction measures, and tightening business operations, respondents overwhelmingly say they expect worsening leasing fundamentals such as vacancies, leasing activities, and rental growth over the next 12 to 18 months (figure 3A). Some respondents believe real estate capital markets may be nearing a market bottom. The same percentage of respondents, compared to last year, expect property pricing and transaction activity to worsen.

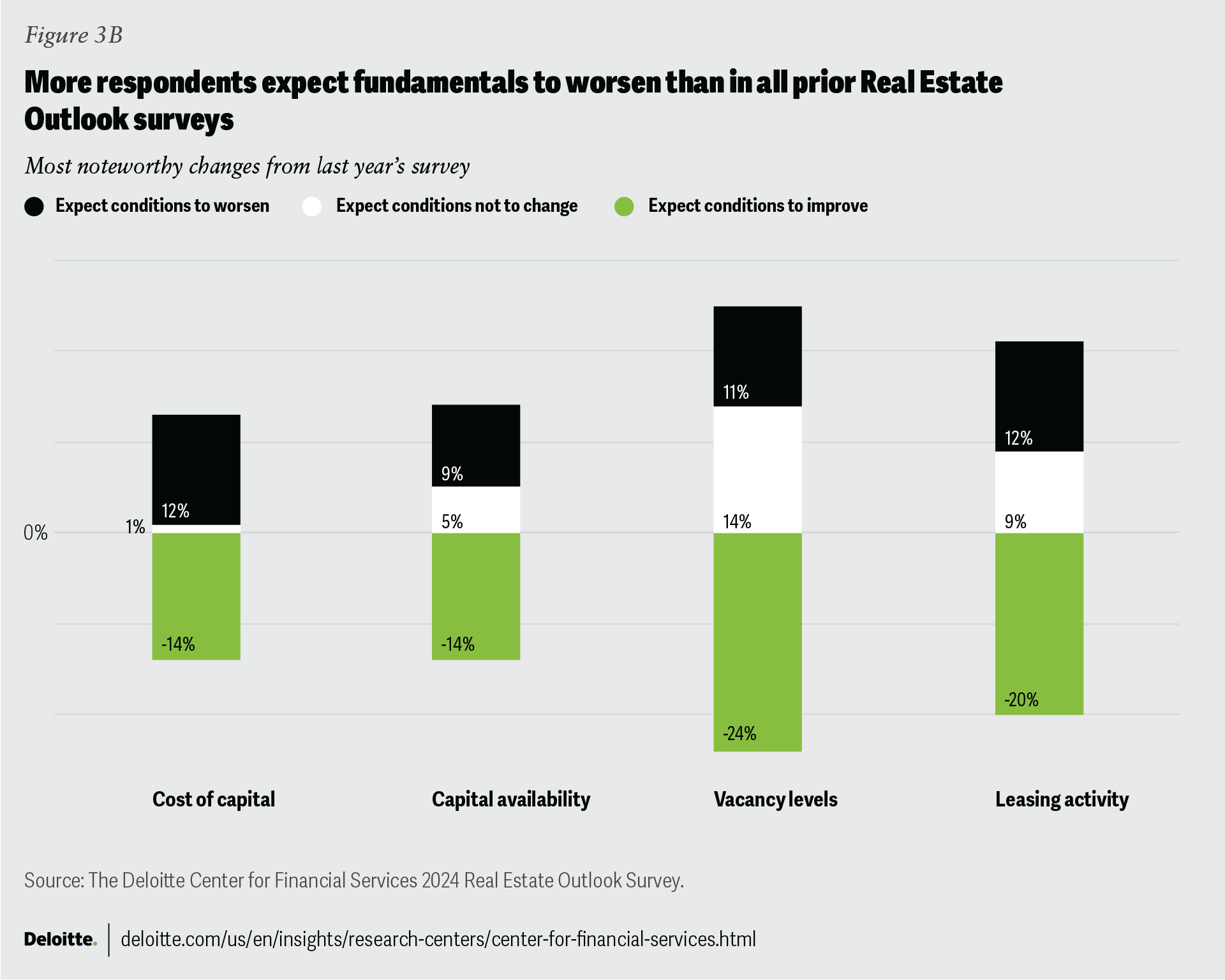

Some of the largest annual changes in fundamental expectations were capital availability and cost of capital (figure 3B). Respondents who were expecting worsening cost of capital increased from 38% last year to 50% this year, and those expecting worsening capital availability increased from 40% to 49%. These expectations likely reflect central banks’ efforts to reduce inflation by hiking interest rates, combined with lenders tightening their underwriting standards. Increases in global interest rates have increased the costs of financing: Average US commercial mortgage rates topped 6.6% as of the second quarter, nearly double the 3.8% rate at the beginning of 2022.3 Lenders also seem more cautious amid slowing economic growth expectations. A net of 67% of bank lenders surveyed by the Federal Reserve in April 2023 are tightening lending standards for commercial mortgages, up from a net of 9% that were actually planning on loosening standards at the end of 2021.4 Some lenders have retreated altogether, with unique lender counts dropping across most major property sectors so far into 2023.5

Facing tightening loan standards, fewer lenders, and higher borrowing costs, commercial real estate buyers could have more difficulty deploying capital for purchases in 2024. Property sales volumes dropped by 59% globally, 63% in the United States, 62% in Europe, and 50% in Asia/Pacific so far through 2023.6 Already in play was nearly US$900 billion in loans set to mature over the next two years in the United States.7 These mortgage maturities could also face difficulties in refinancing in the current lending environment of high borrowing costs and risk-averse lenders. Commercial mortgage-backed securities (CMBS) and collateralized loan obligation lenders are behind more than half of the total loan maturities coming due in 2023 alone.8 Delinquencies on CMBS loans saw a noticeable increase in June 2023, up 28 basis points (bps) to 3.9%.9

As real estate owners and investors weigh weakening economic growth sentiments and corresponding shifts in property fundamental expectations, their top property sector targets are changing. When respondents were asked which property types present the most attractive risk-adjusted opportunity over the next 12 to 18 months, digital economy properties (defined as data centers and cell towers) topped the list for all three global regions (figure 4). Both suburban and downtown office sectors dropped significantly since last year, which reflects how firms continue to grapple with hybrid work expectations. Downtown office dropped from first overall globally last year to 10th this year. Suburban office dropped five spots as well, to seventh.

Alternative sector opportunities, those not in the “core four”—office, retail, industrial, and multifamily—gained ground in this year’s survey; three are now in respondents’ top five targets. Single-family rentals (SFRs) and build-to-rents (BTRs) jumped five spots to second overall, closely followed by senior care (third) and life sciences (fifth). The greatest year-over-year increase came from self-storage properties, jumping six places from 14th to eighth overall, carried by respondents in North America.

Here’s a closer look at changes to individual property type expectations for the coming year:

Office

How we got here

Remote working has disrupted demand for office spaces across the industry. Despite the addition of over two million in-office jobs in the United States alone since 2020, the sector still shed nearly 200 million square feet of occupied space,10 and, on average, has experienced nearly 10% in asset value declines11 over the same period. Further gripped by greater economic uncertainty through early 2023, occupiers of commercial space have exhibited caution in new lease signings. This has driven vacancies upward across the globe, topping 15.6%, led by quarterly increases in North America (+53 bps) and Asia/Pacific (+42 bps) followed by Europe (+10 bps).12 As a result, office property valuations slipped down by 4.5% globally, topped by North America (5.9%) and followed by Asia/Pacific (3.4%) and Europe (2.0%).13

However, all things have not been equal across the real estate sector. Newer, high-quality assets continue to significantly outperform the rest as the flight to quality accelerates.14 Estimates suggest that new construction designed to accommodate hybrid work strategies has absorbed more than 100 million square feet of unused space. And while many regions still struggle with price discovery due to falling investment activity, the value gap between better-quality and lower-quality assets has clearly widened.15

A new foundation

Through early 2023, we may have gained more clarity on what realistic, stabilizing office space utilization rates across the globe might look like. On average, US office space utilization has steadied at just under 50% of prepandemic levels, compared to 70% to 90% in Europe and 80% to 110% in Asia/Pacific.16 Global variations can be attributed to varied housing formats, commute times, and labor markets.17

Real estate office owners and investors should acknowledge that hybrid work is here to stay. It is shifting how offices are used and valued, so valuation strategies should change as well. Now almost three years into assessing pandemic-era space requirements, office occupiers have more insight into how much office space they may need. According to CBRE’s most recent office occupier survey, 60% of US respondents believe their office utilization has stabilized, up from 43% who expected to reach a steady state in 2022.18 Those who still expect further utilization increases are primarily from firms with the lowest current utilization rates, and 71% of respondents expect their companies to reach steady state by the first half of 2024.

The office sector should be rebalanced, similar to what regional malls faced several years ago.19 Real estate services firm Cushman & Wakefield estimates that nearly 60% of existing US office inventory needs reinvestment or to be upgraded, with another 20% being completely undesirable without major work.20 At this stage, office owners and investors should be realistic about what to do with underperforming assets. They could consider adaptive reuse, conversion to meet higher-quality demand or sustainability regulations, or, if conversion wouldn’t be cost-effective, outright demolition. As we discussed in Deloitte’s 2023 FSI Predictions, should market fundamentals further deteriorate for the office sector, coupled with sustained stability in the multifamily sector, office-to-residential conversion opportunities could become a broadly viable option by 2027.21

Retail

How we got here

Following a near-historic retreat in consumer sentiment in early 2023, retail conditions are trending upward recently. In the United States, July marked the second consecutive month consumer sentiment rose, as efforts to tame inflation have so far been successful.22 Deloitte’s State of the Consumer Tracker shows consumers globally have consistently improved their finances; only 35% of respondents feel their financial position worsened over the past year through late June, down from 41% in February.23

Retail tenant demand has maintained momentum due to several years of industry transformation and larger retailer consolidations in higher-quality locations, despite varying degrees of health from economic indicators. According to Coresight Research, US store openings outpaced store closings by over 1,500 stores in 2022, and just under 1,000 stores so far through 2023.24 Leasing activity has generally remained positive across North America, Europe, and Asia/Pacific.25

A new foundation

Despite several prominent retailers filing for bankruptcy over the past year, there is still healthy demand, and landlords remain optimistic they can still quickly fill vacancies and push rents higher.26 This resiliency speaks not only to the retailers themselves—those who survived a pandemic and have generally built more robust operations with stronger financials—but also to the state of retail development and the favorable balance of supply and demand.27 While other sectors have gone through supply-side booms over the past few years, new retail development is still structurally restrained due to limited new constructions and demolitions from widespread store closures during the late 2010s.

E-commerce should be a tailwind for growth. Six in 10 retail executives foresee strengthening digital commerce offerings as a top opportunity,28 but the pace of growth has normalized from highs during the heights of the pandemic. Upgrading physical locations with better digital capabilities can help retailers achieve greater success. Retailers that can continue to build more robust efficiencies across last-mile distribution capabilities, omnichannel logistics, and e-commerce presence could define the next era of tenants. Landlords should be keen to lure these retailers into their locations.29

Industrial

How we got here

Boosted by growing e-commerce and third-party logistics providers, along with investments in reshoring initiatives to bolster stretched supply chains and domestic manufacturing, sustained demand for industrial locations has still led to high competition for existing space. Spending on consumer goods during the pandemic pushed demand for warehousing and manufacturing space to new heights. Absorption doubled in 2021 compared to the 2015–2019 average and exceeded that prior average by over 60% in 2022.30 To help meet this demand, a record amount of new construction is scheduled to begin by the end of 2023. But some markets are still supply-constrained and have near sub-1% vacancies. As a result, rent growth continues: 18.6% in North America, 10.8% in Europe, and 6.4% in Asia/Pacific year-over-year in mid-2023.31

A new foundation

A record industrial construction pipeline aims to address the vast supply/demand imbalance. Regulatory incentives are helping, too. Notable incentives are energy credits and tax deductions from the Inflation Reduction Act and the Creating Helpful Incentives to Produce Semiconductors Act (CHIPS Act). Other actions to better balance supply with demand include transitioning to new transportation and energy technologies and nearshoring global supply chains for more responsive operations.32 But this construction boom could face two potential threats: first, a lack of available land to build, particularly “megasites,” 1,000+ acre plots of land that have transit access near a skilled labor pool; and second, a robust-enough energy infrastructure to support these facilities.33

Megasites are custom-designed to meet the needs of a single occupier. These often have expedited development timelines, especially where time-sensitive tax incentives are in play. Megasite users have come to expect shovel-ready sites, but in the United States, fewer than two dozen sites like these are left.34 Land options become even more scarce for factories needing access to substantial sources of electricity, such as chip manufacturers and electric vehicle battery plants. Finding the right mix of conditions in breaking ground for new megasites could become more difficult. As a result, developers have faced costly extensions to project timelines for much-needed inventory. This, too, has contributed to higher rents.35

Residential

How we got here

On the heels of interest rate hikes, home sales reversed from the pandemic-era boom and pockets of home pricing corrections have emerged. Yet, despite these price drops, inflated mortgage costs and accessibility to capital have kept buyer activity muted.36 As a result, the outsized demand for multifamily rental properties that started during the pandemic continues. Most US markets have seen rent growth top 20% since 2019.37

Accounting for regional variances in common mortgage structures, household incomes, and central bank policies, a recent report categorized the progress of developed housing markets across the globe into three segments: early adjusters, bullet dodgers, and slow movers.38 Canada and Australia fell into the early adjuster camp; in these countries, buyers leveraged more accessible variable-rate mortgage terms during the pandemic, when credit was cheaper. Since then, they have experienced some of the steepest pricing corrections to date. The United States and France have seemingly dodged a few bullets: Most US homeowners hold long-term fixed-rate mortgages following the housing crisis in 2008. And among homeowners in France, there is very little household debt.39 These two markets have not seen significant, widespread price deflation so far through 2023 compared to other global regions. The United Kingdom and Germany are still in much earlier stages of housing volatility. Pricing is only starting to turn, but developers are beginning to worry as housing purchase demand wanes.40

A new foundation

Affordability will likely continue to be a fundamental issue that impacts global housing markets, especially among renters and first-time homebuyers. How municipal and federal governments respond could be pivotal in addressing housing supply and demand. Enacting policies that allow for more favorable zoning, such as allowing for more units to be constructed on a single lot, as well as financial incentives like low interest loans or tax abatements, could help.41 But so far, inflexibility at local levels has prevented measures like this from being adopted more broadly.42

The supply of new, affordable inventories will likely still be limited across many parts of the world due to inflated construction costs and difficulties obtaining development financing. US housing construction is expected to bounce back, but not until 2025, when forecasts suggest it could reach around 1.5 million units delivered per year.43 With the mismatch in global supply and demand for home purchases, multifamily rentals could still serve an accessible outlet for housing for those priced out of the market.44 As consumers continue to live in rental units waiting for their chance to buy, demand for multifamily rental properties could continue to be strong.

Hotel

How we got here

Vaccine rollouts and easing travel restrictions have helped the hotel industry steadily rebound. Benefiting from pent-up lack of leisure travel, the average revenue per available room exceeded prepandemic levels in the Americas (+14%) and Europe (+13%) but is still behind in Asia/Pacific (-7%).45

Hotel operators are increasingly concerned about “the quality equation”: balancing top-of-the-line service offerings while they face continued staffing shortages and supply chain limitations.46 At the end of 2022, the hospitality labor force was only 84% of prepandemic levels, and rising materials costs and limited financing options have delayed needed renovations and limited owners’ and operators’ abilities to invest in upgrades.47 This, combined with the increased cost of service, could have travelers questioning the value they received for their money.

A new foundation

The demand for hotel space is on the brink of a full global recovery, but with the reemergence of leisure travel comes a greater expectation per dollar spent. The days where travelers gave operators a pass on the price-versus-experience equation due to the pandemic, inflation, or labor shortages are likely over.48 As travelers become increasingly price-sensitive amid financial instability, hotel operators should meet their customer’s experience expectations head-on or they could risk losing them.

Corporate travel still lags behind as part of the recovery. While leisure travelers outnumbered business travelers, the latter historically contributes much more to bottom lines.49 If, by the end of 2024, companies recover to 2019 business travel spending levels, when adjusting for inflation, corporate travel could likely settle about 10% to 20% lower than it was prior to the pandemic.50 The United States and Europe are on similar recovery trajectories: In both markets, corporate travel spending is expected to reach only two-thirds of prepandemic levels by the end of 2023. A full recovery to 2019 corporate travel spending is not expected in the United States and Europe until late 2024 or early 2025.51

Alternatives: Digital economy, specialty housing, and life sciences

Digital economy

Hyperscale tenants, those that manage large-scale computing resources, dominated digital economy property demand again in 2022. Since then, they’ve started to expand into secondary and emerging markets. But in more developed regions, they may face limited land availability and power cost increases, limiting expansion opportunities. The sector has been at the mercy of utility price volatility, brought on by geopolitical instability in Europe, with median electricity costs increasing 16% last year.52 As the network of data center properties expands further to meet the growing needs of the digital landscape, fiber density and quality, as well as cloud availability, could be key drivers in locating new facilities.53

Single-family rentals/build-to-rent

Rent growth for existing single-family rentals has slowed. Eroding affordability is leaving fewer funds available for renters to meet more cost increases. Though rent growth has flattened out of late, rather than declined, it could be more likely that the 26% rent growth since the onset of the pandemic has likely become the new baseline.54 BTR home construction, on the other hand, is still thriving. Developers targeting this space are taking advantage of demand for those looking for private homes but want to wait for the dust to settle before committing to buying.55 In Europe, investors seeking further housing diversification outside of traditional multifamily have turned to these niche rental housing sectors. The United Kingdom has been the primary target; capital topped US$3.5 billion by June 2023, placing it second globally behind the United States.56

Senior housing

The perpetual demand due to an aging populace should sustain the senior living sector. Older populations around the globe are growing in number and proportion at a faster pace than historically. Between 2015 and 2050, the share of global populations 60 years and older is expected to nearly double, from 12% to 22%. By 2030, one in six people will be aged 60 or older.57 Revenue opportunities for the sector are expected to grow more than 6.5% over the next five years, but could end up lower because of increased operating costs and staffing shortages.58 In the long run, senior housing margins could benefit from adding more inventory and more diverse product offerings, such as active adult communities or ultra-luxury retirement facilities.

Life sciences

The exponential growth trajectory for the life sciences sector realized during the height of the pandemic has leveled off so far into 2023, though demand for space is still outpacing prepandemic levels.59 More recent economic headwinds, particularly in the banking sector, have paused some venture capital funding of life science companies, although levels still remain well above prepandemic funding by about 15%.60 Vacancies are expected to increase as record new construction comes online to meet demand, but should still remain well under long-term average vacancies, further propping up rental growth. The continued confidence in the underlying demand for medicines should drive optimism for life science users over the next several months,61 even though capital inflows from public and private sources could be tested again if volatility hits financial markets.

Actionable guidance to consider

Property market trajectories have been uneven; some sectors may now face new foundational expectations and realities. Going forward, real estate leaders should focus on mitigating risks and enhancing operational and regulatory resiliencies. Depending on capital structure, investor expectations, and risk tolerance, investment leaders at real estate firms can take a conservative or proactive approach:

Conservative

- Alternative capital sources: Firms can use mezzanine and preferred debt to fill short-term voids in available capital from the potential retreat of bank lenders who choose not to lend in a riskier capital markets environment.

- Tenant priority/mix: Pacing rent growth with inflation can help sustain cash flow but should be balanced with tenant relationship management. Owners/investors should work with tenants to ensure their needs are being met. Also, this could be a good time to sign on credit tenants to ensure a stable tenant mix.

Industry leader perspectives: Howard Hughes’s John Saxon on the importance of location and the mixed-use environment

“Location is certainly a key defining factor. We see a bifurcation of occupancy between central business districts and suburban assets. Typically, vacancies are rising in areas around today’s CBDs, whereas buildings that are located in highly amenitized areas in more open, natural settings are seeing an increase in leasing activity and showing higher occupancy rates. Our communities, which offer vibrant mixed-use environments outside of denser downtown metro areas, are seeing incredible leasing activity and a diversified tenant mix because of their ideal location.”62

—John Saxon, chief of staff, Howard Hughes Corporation

Show more

- Risk management: Ramifications of loan defaults by owners and developers could impact employee retention and shareholder value. They could leave businesses as vulnerable as the buildings themselves.

- Patience and thorough due diligence: Higher interest rates have already had some impact on asset pricing. Real estate leaders may need to be even more careful about site selection and asset quality to protect near-term stability and long-term performance.

Proactive

- Negotiating power: Conventional lending is tight right now. Debt investments could be used to access real estate investment opportunities and offer more term flexibility than traditional sources.

- Diversification through alternatives: For those looking to deploy capital, nontraditional property types may offer stability through diversification. From our survey, four of the top five target property sectors for owners and investors over the coming 12 to 18 months are outside the core asset classes (office, retail, industrial, and multifamily).

- Risk management: Being transparent with shareholders and investors may engender or reinforce trust. This should include being realistic about mark-to-market adjustments.

- Buy opportunities: What purchase opportunities could come from potential further asset devaluations? Low leveraged, highly liquid owners/investors who have been in recession planning over the past three to four years may already be looking for an entry point. In a decelerating treasury yield environment, savvy investors may look to fill the buyer void. This could present opportunities for investors seeking yield through real estate.

Constructing a sustainability strategy to transition to a low-carbon future

Sustainability as a tool for value preservation

The real estate sector is witnessing increased bifurcation. In the United States, sustainability credentials within real estate assets are now synonymous with premier Grade A office space commanding 31% higher annual rents. When adjusted for building age and location, the rent premium is 3% to 4%.63 Investors are becoming increasingly cognizant of property sustainability, and how comprehensive and verifiable reported metrics are for these assets can be the reason why many choose to invest or not.

Managing capital expenses to better mitigate physical and transition risk should be considered over the life cycle of investment into a building, from acquisition to sale. Owners and investors should consider how capital expenditures are being utilized to mitigate climate risk and build resiliency. Building owners who rely on outdated mechanical building systems may find it increasingly expensive and difficult to operate, especially in a more stringent regulatory environment where owners could face penalties for noncompliance.

According to estimates, close to 76% of the office supply in Europe could face obsolescence by the end of the decade if it is not upgraded.64 Nearly half of survey respondents believe the greatest material risk to investing in sustainable real estate is maintaining real estate asset valuations that do not appropriately consider climate-related risk.

Sustainability in building operations

Almost 80% of the predicted building stock for 2050 in some of the world’s largest business districts has already been constructed. This contributes to the thought that monitoring and reducing carbon emissions from existing structures should be the most impactful area in meeting decarbonization targets.65 An evolving regulatory environment may be the impetus real estate leaders need to act on, with focus on energy performance and emissions increasing in scope and stringency. The City Council of Sydney has imposed a minimum National Australian Built Environment Rating System energy requirement of 5.5 (0 being least sustainable and 6 being most sustainable) on new commercial buildings starting in January 2023 with net-zero carbon emissions targets by 2026.66

Over the past several years, leaders at major real estate firms have taken small steps to reduce their carbon footprint, ranging from installing clean, energy-efficient equipment such as heat pumps, and emerging digital solutions such as Internet of Things (IoT) devices and AI-based applications.

Industry leader perspectives: BXP’s Mike LaBelle on seamlessly incorporating sustainability into portfolio strategy

“We have been investing in our buildings and ESG has been a core principle of our strategy. We have an annual capex budget for our buildings that includes upgrading on a consistent basis, and we will continue to do that to meet standards. I think that green energy is going to be part of the future in a bigger way. For some communities where it’s hard to get access to green energy directly, we’ve purchased green energy offsite, and we’ve been doing that for a while. Our goal is to get our portfolio fully green. We have a net-zero goal set for 2025 for scope 1 and 2 and we’ve got a strategy to get there.”67

—Mike LaBelle, chief financial officer, BXP

Show more

Tracking and reporting data on tenant-owned space is also becoming important. Scope 3 emissions account for indirect emissions not owned or controlled by the firm, including tenant-owned areas. To be successful, a sustainability strategy should include green lease clauses, including submetering of the leased area, client energy disclosures, and cost sharing for capital expenditures made to improve energy efficiency. Green leases should be looked at as an opportunity, not a challenge.

Whole-life carbon assessments should become the standard

Whole-life carbon emissions (WLC) are the total amount of carbon a building produces over its entire life cycle. With the goal of net-zero, WLC assessments should be integrated at the design and planning stage to be leveraged throughout the life of the building. Building material databases like Embodied Carbon in Construction Calculator68 or The Structural Carbon Tool69 can benchmark embodied carbon and optimize material usage to reduce the carbon footprint. Pivoting to innovative building materials such as smart glass, low-carbon alternatives like engineered timber or cross-laminated timber, and low emissions cement can aid in reducing carbon emissions. Procurement policies for embodied carbon have been introduced across several states in the United States. In 2022, Vancouver, Canada also passed a plan to reduce embodied carbon in large new buildings by 40% by 2030.70 The European Union (EU)71 and the United Kingdom72 are also turning their attention to WLC levels.

Estimates suggest that around 2.6 trillion square feet will need to be constructed by 2060 to meet the housing needs of growing global populations.73 And waste from new construction is expected to cross 2.2 billion tons every year by 2025,74 with more than 75% of all construction waste deposited into landfills.75 When rebuilding, cities across the globe are favoring deconstruction rather than demolition76 in part because it tries to salvage and reuse original building components instead of destroying them. For example, in the United States, some leading institutions have set a variety of WLC targets to build more sustainable business for the future. BXP has set a target of minimum construction and demolition debris diversion rate of 75% for all new construction and renovation projects,77 while Kilroy Realty has set an embodied carbon reduction target of 30% by 2030 at new construction projects.78

Many real estate firms lack internal controls they need for compliance

Sustainability-related regulations across the globe are evolving and will likely require firms to include detailed ESG metrics in corporate disclosures with similar levels of transparency as financial reporting.79 According to our survey results, 59% of respondents say they do not have the data, processes, and internal controls necessary to comply with these regulations and expect it will take significant effort to reach compliance (figure 5). European firms appear to be slightly more prepared: Fifty-four percent of respondents in Europe expect compliance to be a challenge compared with 65% in North America and 58% in Asia/Pacific. As real estate firms integrate sustainability performance and resilience metrics into their corporate disclosures, it will be important to ensure data integrity and accountability of internal controls.

Actionable guidance to consider

To build, operate, and dispose of buildings more sustainably, real estate leaders should consider:

- Conducting materiality assessments and identifying business priorities that may impact operating performance to reach sustainability targets. Real estate firms operating in the EU will need to start reporting on nonfinancial themes based on their materiality under the Corporate Sustainability Reporting Directive in 2024.80 More than 46% of survey respondents say they have already conducted materiality assessments, while another 40% say they plan to undertake materiality assessments over the next year.

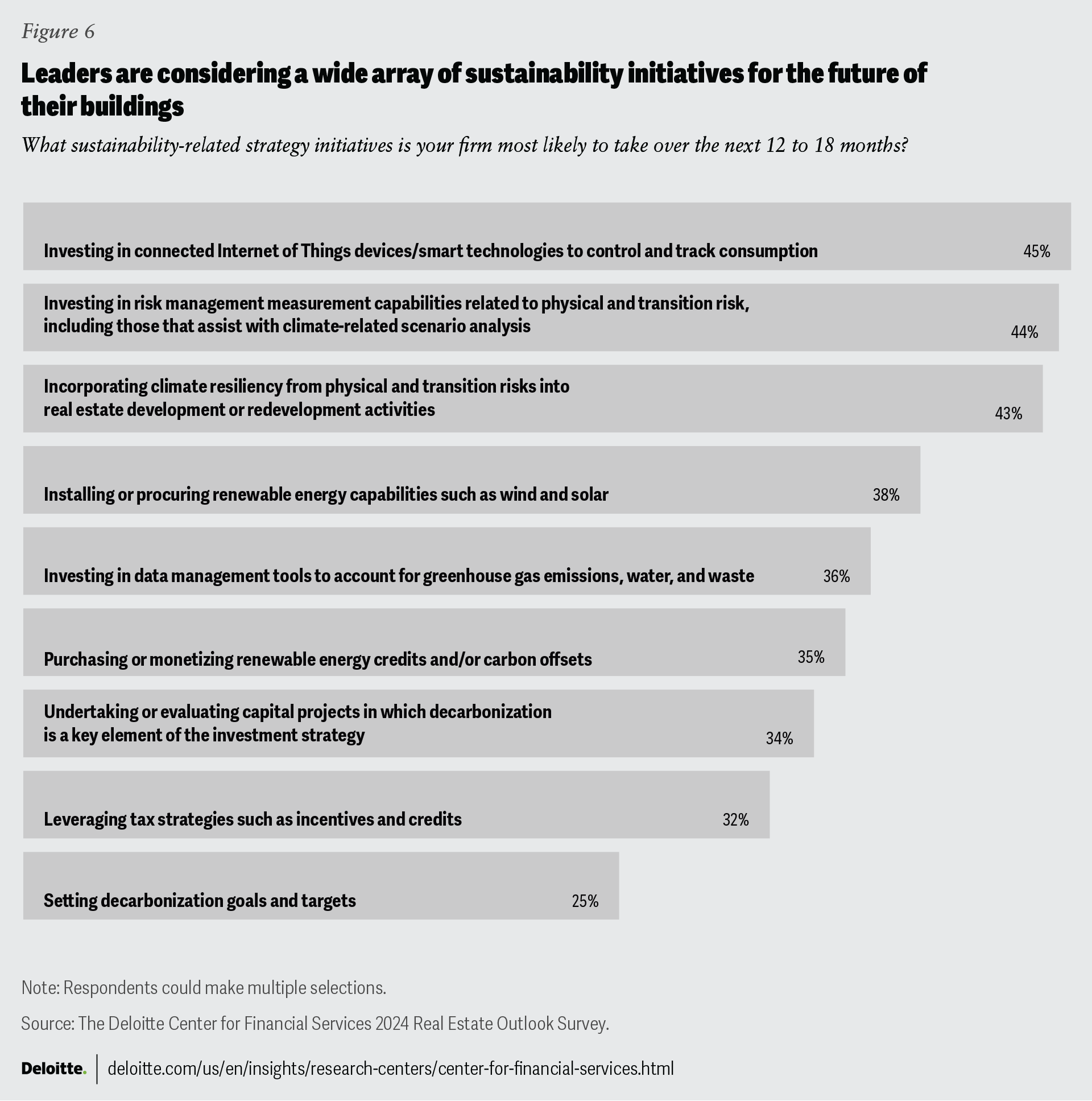

- Ensuring sustainability metrics are comprehensive and verifiable. Measuring and benchmarking greenhouse gas emissions and overall building performance and integrating climate innovation—transformative models incorporating new technologies and innovative business solutions aimed at reducing carbon emissions—should be a strategic priority to retain property values. Investing in connected IoT devices/smart technologies to control and track consumption was the top sustainability-related strategy identified by our survey (45% of respondents).

- Investing in sustainability risk management measurement capabilities. Firms should turn to comprehensive scenario analyses and test asset-level preparedness and long-term resiliency. For instance, they can factor in associated cost implications of increased cooling or heating requirements anticipated due to heatwaves, wildfires, drought conditions, snowstorms, or flooding. Transition risk may involve significant expenses in carbon pricing; this may become relevant in the future for firms with high energy consumption and reliance on fossil fuels. In our survey, 44% of respondents say they are most likely to invest in risk management measurement capabilities related to physical and transition risk over the next 12 to 18 months (figure 6).

- Accelerating the shift to clean energy solutions. Mapping out a successful decarbonization strategy involves transitioning to clean energy sources, both onsite and offsite. Buildings account for almost 30% to 34% of global energy consumption.81 In 2021, the real estate sector accounted for 26% of global energy-related emissions, of which 8% were related to the use of fossil fuels in buildings (direct emissions) and 19% related to generation of electricity and heat used in buildings (indirect emissions).82 Carbon emissions from the real estate sector should aim to decrease by more than 50% by 2030 (9% per year on average) to hit a fully net-zero target by 2050.83 More than one-third (38%) of survey respondents say their firms will likely install or procure renewable energy capabilities over the next year.

Deepening tax comprehension to help strengthen the bottom line

Leveraging credits and incentives to drive ROI

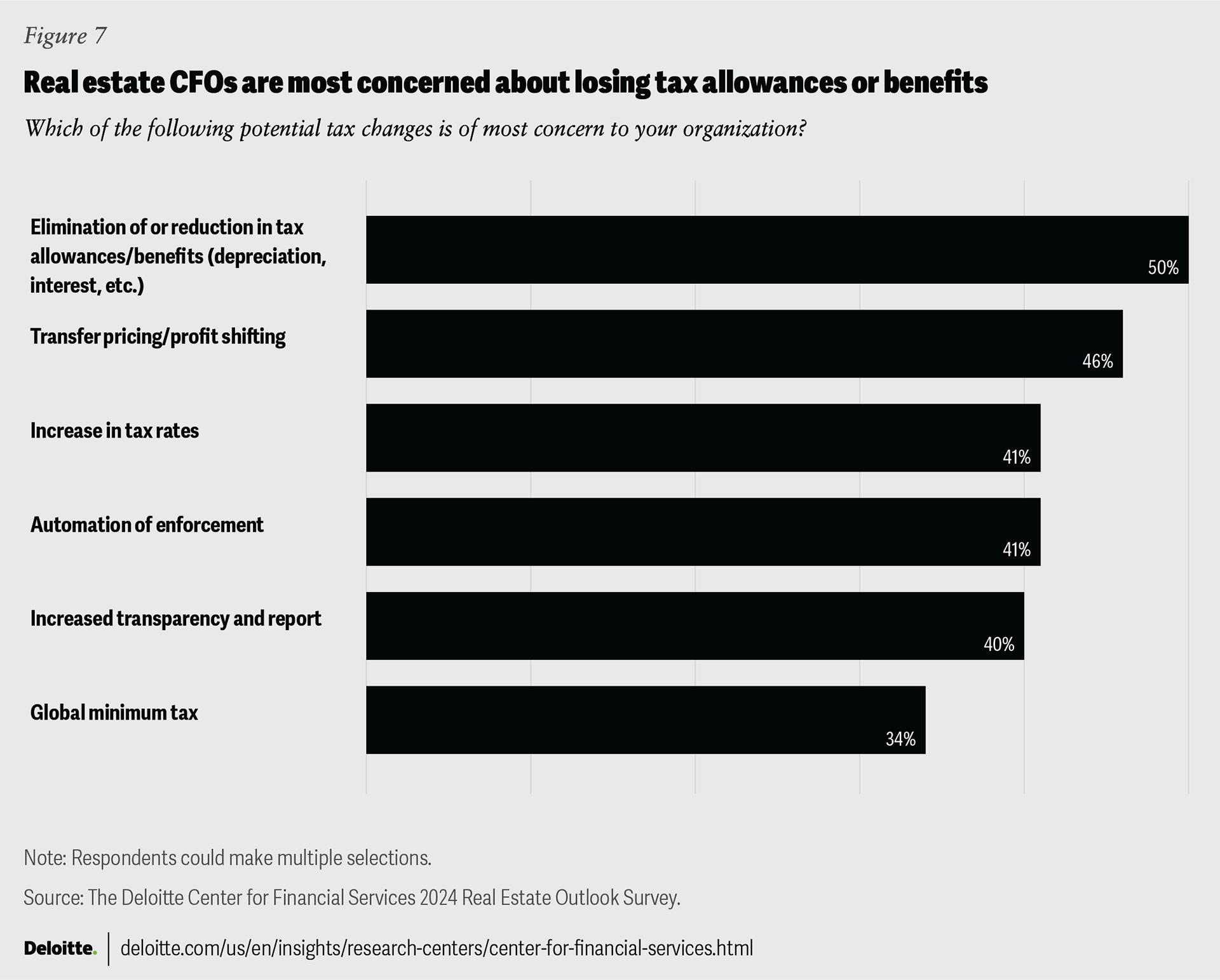

As the focus on expense mitigation continues into 2024, real estate tax leaders are increasingly exploring ways to reduce their tax obligations to support stronger bottom lines. Survey respondents are growing more concerned about the possible elimination of, or reduction in, tax allowances and benefits, with half of the real estate owner and investors selecting it as the most concerning potential change to tax structures (figure 7). This concern was the top response among respondents in Europe (56%) and North America (47%), and second in Asia/Pacific (47%). On average, it was identified as a top concern, 10% more this year than last. In Asia/Pacific, half of respondents say changes to transfer pricing/profit sharing is their top tax change concern.

These results highlight the importance that tax incentives play in supporting stronger financials, especially among those prioritizing the use of credits and incentives. Here are a few of the initiatives that are expected to impact real estate companies in the coming months:

- The Inflation Reduction Act (IRA) clean energy tax credits and incentives. As part of the IRA of 2022, enhanced tax credits and deductions are available for taxpayers that ensure the payment of prevailing wages for laborers and mechanics and the use of qualified apprentices in the construction of facilities or installation of energy-efficient commercial building properties. Compliance with these wage and apprenticeship provisions became effective on January 29, 2023, for facilities or installations on which construction began on or after that date. The IRA expanded, enhanced, and introduced several credits for investments in or production of clean energy, some of which may be transferrable and, thus, more accessible to real estate companies, such as real estate investment trusts (REITs). It also extended certain energy credits and increased the types of eligible technologies. The IRA provides incentives for energy efficiency upgrades to commercial real estate buildings, which may reduce the costs associated with and increase demand for improved energy efficiency in new building construction and retrofits.

- The Green Deal Industrial Plan. In early 2023, the European Commission proposed the Green Deal Industrial Plan, which would loosen state aid rules through 2025 to allow EU governments to subsidize investments in renewable energy or decarbonization initiatives.84 The plan would offer faster permits to manufacturers of key climate technologies and establish a European Sovereignty Fund to invest in emerging climate technologies. Funding will be provided among others by what remains of the EU’s US$872 billion postpandemic recovery fund.

Kicking off the global minimum tax

What’s in store

In late 2021, more than 135 countries agreed to the Organisation for Economic Co-operation and Development's (OECD's) proposed 15% global minimum tax, or “Pillar Two,” for large multinational enterprises.85 Each global member jurisdiction can decide whether to enact this framework into its domestic legislation. However, the rules are designed to impact the operations of large multinational enterprises even in those countries that do not incorporate the rules in domestic legislation. Early in 2023 86 and again in July, the OECD released technical guidance to assist governments and taxpayers with the implementation, with some countries slated to apply these rules beginning in 2024.87 South Korea, Japan, and the United Kingdom have enacted Pillar Two model laws, and other jurisdictions have proposed laws that are effective January 1, 2024. An EU directive requires implementation as of January 1, 2024 for EU member states.88

The US tax on global intangible low-taxed income, or “GILTI,” was not changed to conform to Pillar Two in the most recent tax reconciliation bill, the IRA. With a split-party US Congress, it is unlikely there will be bipartisan support for international tax reform or notable changes to the existing framework until at least the 2024 election cycle.

Multinational enterprises (MNEs) are the entities considered by Pillar Two. The framework’s Global Anti-Base Erosion Rules are in place to ensure MNEs pay at least a 15% tax rate in the jurisdictions in which they have operations. To be considered an entity within the scope of Pillar Two obligations, the MNEs must operate in at least two global jurisdictions and have a consolidated group revenue of at least US$818 million in at least two of four fiscal years immediately preceding the entry into force of the Pillar Two rules.89

The OECD has issued safe harbor guidance that may reduce the burden of Pillar Two in the initial years. In addition, there are certain exclusions to these rules, particularly as they relate to real estate investment vehicles (REIVs) and investment funds (IF), such as REITs and other funds that focus on investment in real estate. Subsidiaries of these entities may also be excluded if the REIV or IF owns at least 95% of the investment subsidiary.90 There are additional ownership thresholds and primary business activity designations that will differ from company to company and can impact qualification for these exclusions. Further guidance will likely be needed to help clarify the definitions and determine the applicability of these provisions.

Actionable guidance to consider

- Real estate tax leaders should assess eligibility and available opportunities for credits and incentives. These can help either offset existing tax obligations or open doors into capital sources. New laws coming into play over the next 12 to 18 months can change how companies approach their planning for tax credits and incentives.

- Know where you stand with global minimum tax requirements. Cross-border corporations should confirm their status as an exempt entity under Pillar Two, analyze potential safe harbors that may be available to defer immediate impacts, and prepare for any impending 15% minimum tax obligation that may be due. Uncertainty specifically around how real estate investment vehicles are treated could lead to unexpected tax savings or burdens.

Evolving hybrid work and transforming operations

Hybrid work may not be one-size-fits-all

The past few years have contributed to the idea that hybrid work opportunities are likely here to stay. But the meaning of “hybrid work” continues to evolve. Companies should provide direction to employees on where to complete their work and build the right infrastructure to support a hybrid environment as employees are trying to balance working at two different locations with different schedules and demands. This delicate balance can be taxing, and 64% of workers globally say they have considered, or would consider, looking for a new job if their employer wanted them back in the office full time.91 This age of hybrid work should be defined by flexibility and transparency. Decisions on days in and rule-setting from the top should evolve. This includes involving employee opinions on how many or which days are needed to connect in office or allocated to deep work at home. Coming into the office for a day filled with conference calls that could be done remotely could foster undesirable frustration among employees.

Industry leader perspectives: Heitman’s Mary Ludgin on leading an organization in today’s workplace

“We try to hire the smartest, most intellectually curious people possible and then give them room to run. Long before working from home, that included recognizing that some members of my team were really better if they were allowed to wander in at 9:30, and they would still be there at 8:30 at night. I just needed to give them the room in which they could be—what’s the cliché?—their best selves. I’ve always tried to create a space in which people can do their best work. We have the pleasure of each other’s company in trying to think through complicated circumstances.”92

—Mary Ludgin, director of global investment research, Heitman

From Deloitte’s Within Reach podcast series

Show more

Employees may be more receptive to hybrid decision-making if they have an open line of communication and measurable data to support hybrid effectiveness. A recent study by Deloitte outlined several metrics organizations can consider while developing their hybrid strategies, equally balancing work productivity and talent development. These measures include office space utilization, meeting quality, use of technology for communication, peer learning, team participation in decision-making and long-term planning, and interconnectivity between departments or functional areas, among others.93

While there is no blueprint for where work gets done, a good chance at a solution could require a mix clearly outlining hybrid worker contributions and sense of belonging within an organization’s long-term performance, and when indicated, physically evolving the workplace to better reflect the tasks that are best handled together, in-person. Studies show that the primary purpose for a physical office is collaboration, so workplace design should foster connectivity.94 The physical, virtual, or hybrid workplace has become a mere input to executing the work, and organizations that prioritize what employees need to get the work done will likely be better equipped to achieve the desired results.

Industry leader perspectives: Seaforth Land’s Tyler Goodwin on “earning the commute”

“As employers continue to vie for talent amidst this hybrid future, they need to establish a workplace environment that ‘earns the commute’ of their employees into the office. A cubicle farm in a glass box won’t do it… It needs to incorporate more breakout space and meeting rooms, and desks need to be comfortable and available. Hot desking can actually have a negative impact on earning that commute. Peak days often result in lack of seating, which can massively undermine the greater objective firms are trying to achieve [in getting people back in the office]. Given office accommodation is typically between 5% and 10% of talent costs, cutting back on space at the expense of experience and dedicated workspace feels a lot like stepping over a dollar for the sake of a dime.”95

—Tyler Goodwin, chief executive officer, Seaforth Land

Show more

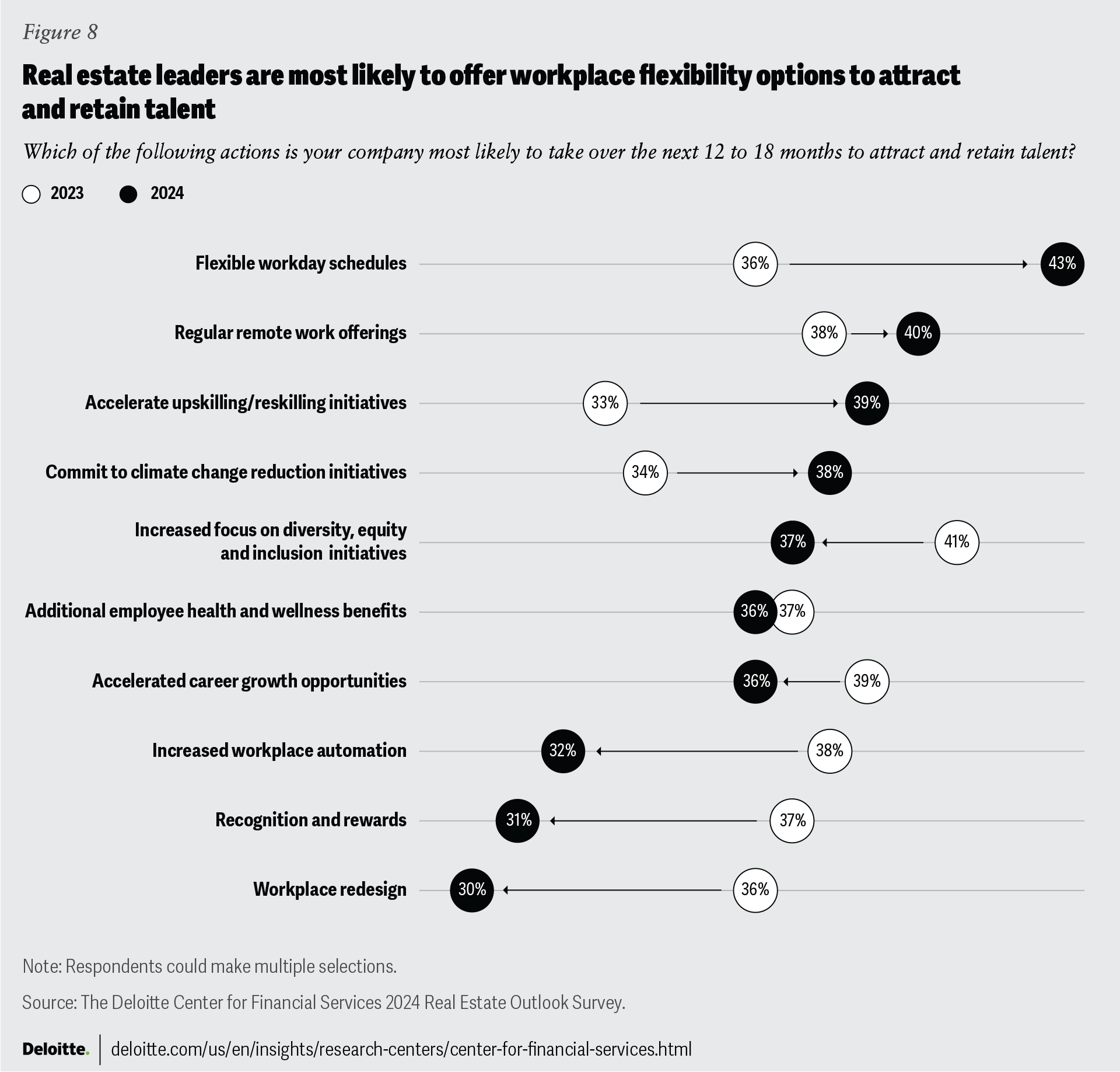

In our survey, real estate executives identified flexible workday schedules (43%) and regular opportunities to work remotely (40%) as their top actions for talent acquisition and retention (figure 8). These priorities have shifted from the prior year, where respondents’ top three actions to attract and retain talent were increased focus on diversity, equity, and inclusion (41%); accelerated career growth opportunities (39%); and remote work offerings and increased workplace automation (38%). Regular opportunities to work remotely retained a top spot year over year. But interestingly, flexible work schedules, accelerated upskilling, and a commitment to climate change initiatives garnered the largest increase in responses compared to the prior year. This shift in priorities reflects organizations’ responsiveness to employees’ feedback on the need for flexibility and transparency, as well as a desire to train existing employees in new areas as firms look to modernize technology and outsource certain functions. Conversely, workplace redesign, recognition and rewards, and workplace automation dropped in popularity as compared to the prior year. These initiatives likely require more capital outlay, reflecting organizations’ desire to mitigate spending with a particular focus on reductions in talent-related expenses and costs for office space.

Leveraging outsource capabilities for enhanced efficiency

Drivers of change

Organizations seeking to evolve the talent experience and physical workplace are also motivated to transform operations. Talent shortages and lack of agile infrastructure have been identified as some of the biggest barriers to success.96 Though from our survey, those priorities may differ across the size and scale of the organization. A majority of respondents from large real estate organizations (57%) still expect to increase headcount in 2024. This is a marked change from the prior year, where only 29% of large organizations expected to increase headcount in 2023. However, the inverse is true for smaller organizations: Only 45% of respondents expect to increase headcount in 2024, down from 53% in 2023. Given the lukewarm revenue projections as noted earlier and respondent expectations for worsening real estate fundamentals overall, organizations should consider many options for transformation and avoid defaulting to standard cost-cutting measures like procurement or reducing headcount.97

To that end, most of our respondents (61%) are considering outsourcing certain operational capabilities over the next 12 to 18 months. Their primary goals are gaining technological capabilities and streamlining processes (42%), adding agility and resilience to their operations (39%), and accessing integrated offerings across business lines (38%). While some could perceive outsourcing as a means to subtract headcount and replace it with third-party labor, real estate leaders seem to be pursuing an alternative route. According to our survey, those who plan to outsource operations are most likely to still add headcount, while those not outsourcing are most likely to reduce headcount. The former group appears to be doubling down on transformation, adding capabilities and resilience through outsourcing, as well as investing in new hires across differentiated skill sets.

Labor supply shortages and elevated cost of operation have impacted property management functions. A few real estate companies have turned to leading-edge technologies with more proactive capabilities, such as automating rent collections, leasing, and tenant management.98 These initiatives help reduce the need for onsite resources and improve customer satisfaction by offering real-time responsiveness. Firms may be leaning toward incorporating enterprise-level controls by centralizing operations in-house or partnering with third-party service providers. Many are shifting away from disjointed technologies deployed across different functional areas.

This is a part of a growing centralization and outsourcing pattern some residential firms have recently adopted:

- In 2021, Equity Residential was able to generate US$15 million in additional net operating income by integrating an AI-enabled property leasing and maintenance platform, which could handle 84% of inbound electronic leads and reduce approximately 7,500 labor hours per month. The REIT also anticipates adding US$25 million to US$30 million of additional net operating income over the next couple of years by leveraging technology and outsourcing repetitive tasks.99

- Gables Residential entered into a third-party servicing agreement with AvalonBay Communities to help support back-office and administrative functions within the Gables operation. AvalonBay’s customer care center will service the entire Gables portfolio and allow Gables to better meet growing customer service demands. The mutually beneficial partnership also helps AvalonBay make continued investments into technologies, processes, and people that help service their own portfolio.100

Apartment, BTR, and SFR owners are also leveraging recruitment outsourcing to address hiring needs. This can be especially helpful when they’re expanding in new markets or for new development projects, when hiring the right talent within time constraints can be a critical differentiating factor for success.101

What real estate firms can achieve

Real estate owners and operators are increasingly looking to deploy outsourcing or cosourcing models so that internal teams can focus on core service offerings, where they can gain a competitive advantage. Speed of delivery and intricacy can be a strategic differentiator across real estate functions such as lease audits, valuations, and tax, as investors demand greater transparency and thorough preinvestment due diligence.102 As data volume and demand for granular information on asset performance increase, investors are coming to terms with the limitations of traditional spreadsheet-based models for fund accounting or valuation of investment.

Industry leader perspectives: CBRE’s Vikram Kohli on accelerating operations transformation

“We want to take advantage of technology, automation, and machine learning and what's happening with AI as a way to potentially skip a generation of offshoring and outsourcing. We recently set up a centralized transformation office, comprised of several strategic efficiency-focused functions, to accelerate how quickly we achieve greater operational efficiencies and drive innovation through technology integration.”103

—Vikram Kohli, chief operating officer, CBRE Group

Show more

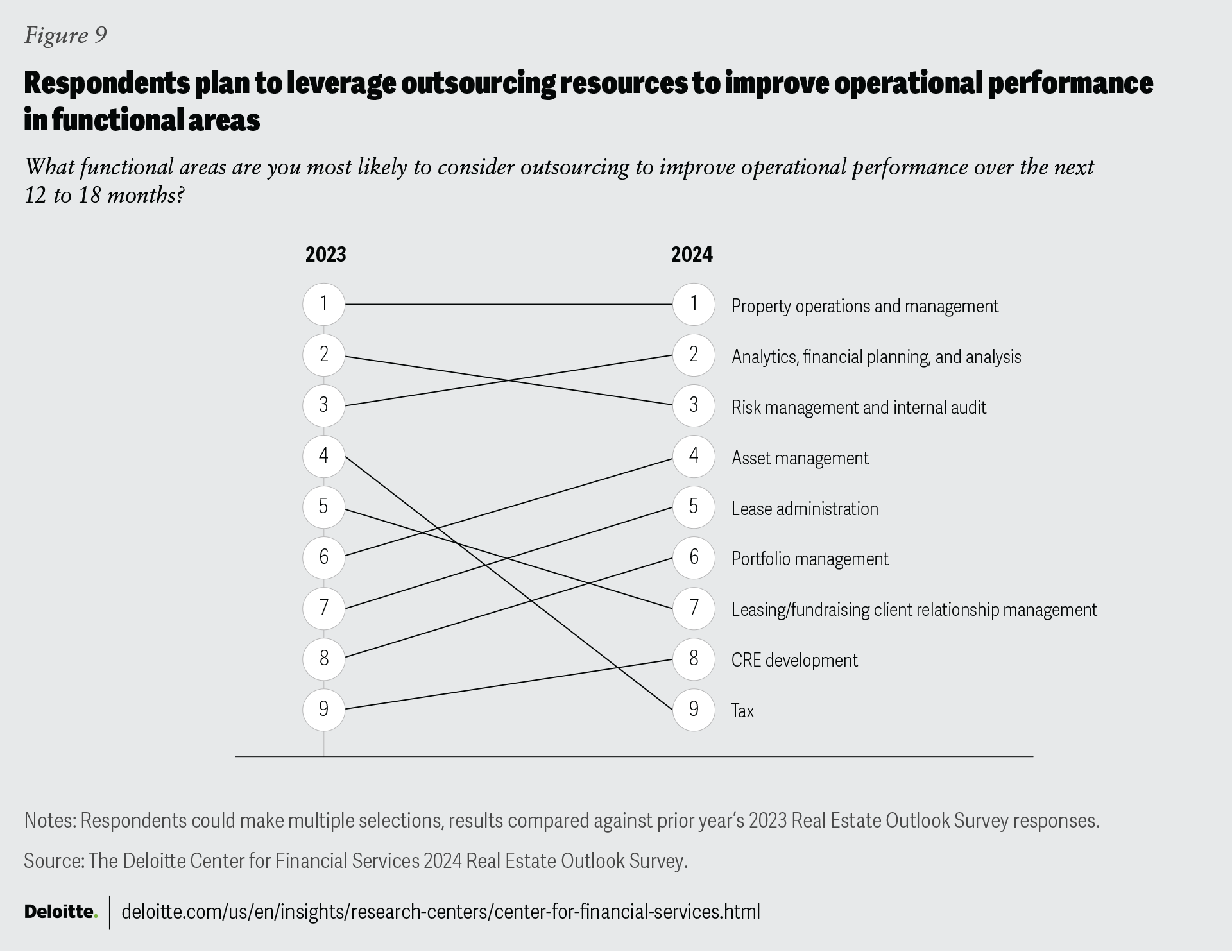

The top three functional areas most identified by survey respondents for outsourcing over the next 12 to 18 months are property operations and management; analytics, financial planning, and analysis; and risk management and internal audit (figure 9). Analytics, financial planning, and analysis notched the largest annual percentage increase, while tax outsourcing declined eight percentage points, dropping in ranking from fourth overall last year to ninth this year. Outsourcing these functions could allow real estate leaders to keep focused on creating, maintaining, and growing their competitive advantage in core functional areas such as customer relations, development, acquisitions, or leasing.

Actionable guidance to consider

- Prioritize clarity, collaboration, and equity as part of a hybrid work strategy. Hybrid work is likely here to stay, and employees have grown to expect clear communication on when and where. Regardless of what balance of at-home or in-person work organizations take, leadership styles and employee support structures should be aligned with in-person, remote, or hybrid arrangements. Leaders should consider concepts like team-by-team back-to-office schedules for added flexibility or broader meeting space and desk availability to help ensure that opportunities for connection are being provided to team members.

- Think about how the workplace could physically evolve to foster connection and collaboration among employees coming onsite. Build workspaces that spark casual conversation for those who are in-person; provide seamless videoconferencing capabilities for employees working virtually.

- Evaluate how outsourcing capabilities could accelerate agility and scalability. Consider enterprise service offerings that allow for integration across business lines and build resilience. Leveraging a third-party alone may not be enough. Those parties should be coordinated with in-house capabilities to create a seamless flow of data and operations inside and outside the organization.

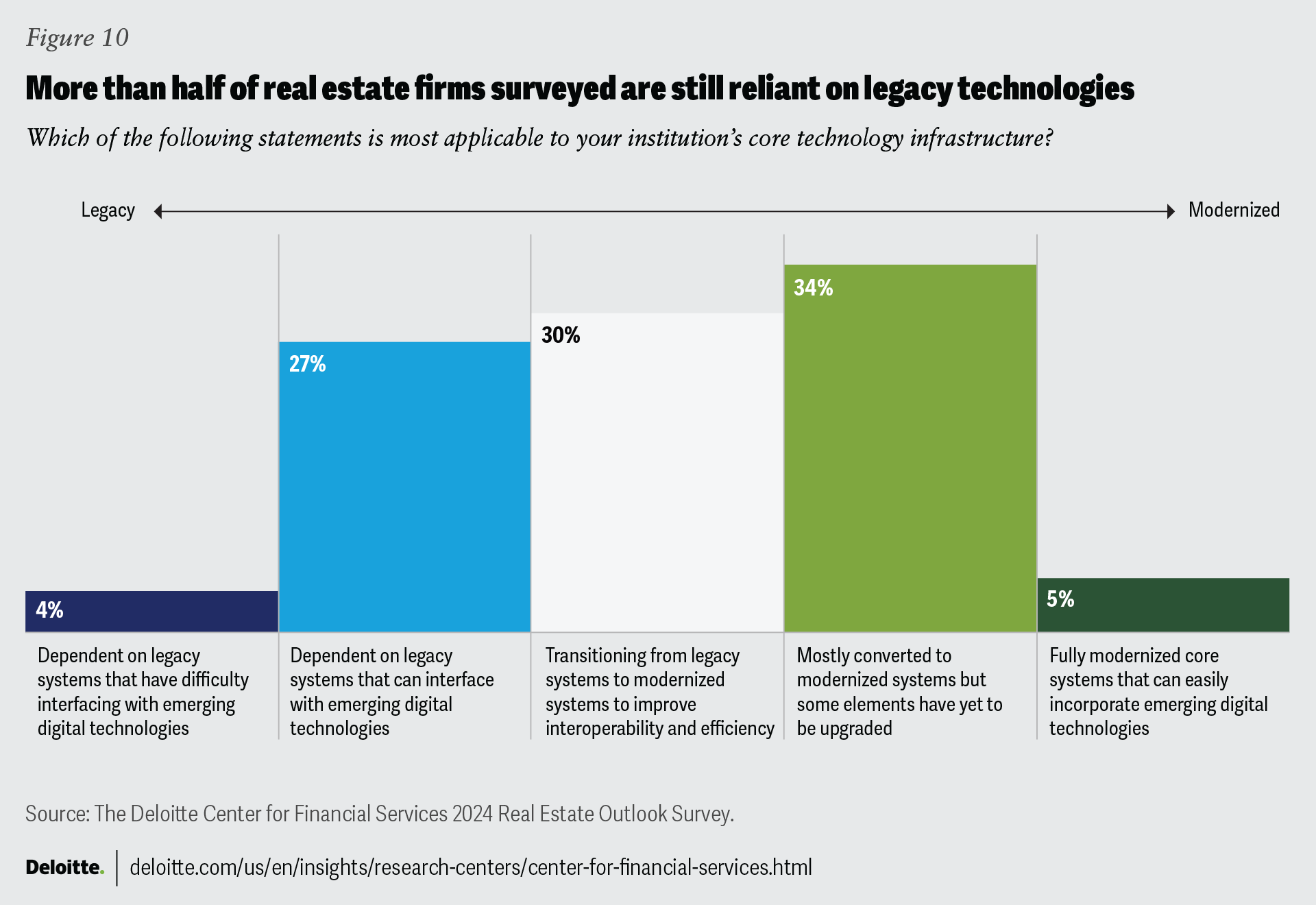

Enhancing real estate technology capabilities through speed and interconnectivity

The value of real estate has expanded; it now accounts for nearly two-thirds of real assets around the globe. But the technology supporting the industry has more or less remained the same.104 From our survey, 61% of global real estate owners and investors are still dependent on legacy technology infrastructures (figure 10). And while nearly half of these lega cy users plan to make the jump toward modernization, successful implementation is often more complicated than clicking “update.” Estimates suggest that up to 73% of enterprise data across industries goes unused, so there are opportunities for leaders in the real estate industry to put that valuable information to better use.105

Acknowledging real estate industry technical debt

Most real estate firms still depend on established, albeit aging, legacy technologies that often serve a singular purpose for a particular task. On average, firms still use spreadsheets 60% of the time for reporting, 51% for property valuation and cash flow analysis, and 45% for budgeting and forecasting.106 These independent data processes can limit business units’ ability to communicate with each other, leading to redundancies and inefficiencies that further slow the flow of data across an organization.

The costs associated with simply running and maintaining legacy technology, which were originally designed to save time or money, is known as technical debt. Estimates suggest that 10% to 20% of new product technologies are spent resolving existing technical debt. Some suggest the cost of technical debt can be as high as 60% of every dollar spent on information technology.107 However, the reality is that only 13% of real estate companies have access to real-time business intelligence and analytics, according to real estate services firm Jones Lang LaSalle.108

Challenges to more systematic digital adoption have likely come from the industry’s approach to generational diversity, outdated job roles, talent processes, and culture. From a Deloitte Center for Financial Services study, 45% of real estate employees are age 55 or older, compared to only 4% age 19–24. This lags behind the all-industry average of 24% and is double the banking and insurance average of 22% of employees who are 55 or older.109 Additionally, three out of every 10 new hires in real estate are baby boomers, and for every Generation Z hire, at least three baby boomers were recruited.110 Many of these new real estate jobs have targeted traditional skills like finance, sales, or property management rather than advanced technical skills like data analytics, software development, or cloud computing—contributing to a widening skills demand gap.111

Challenging the status quo

Addressing data silos and the corresponding degraded speed of data flow across the organization should be mission critical in 2024. Especially now, as firms shore up balance sheets to protect against more financial instability, any additional lag created by core data inefficiencies could cause setbacks that could be avoided. Firms should be as agile and informed as ever, and being able to deploy real-time, data-driven decision-making can be a powerful tool to set leaders in the space apart from the rest of the pack.

Industry leader perspectives: Simon Property Group’s Brian McDade on investing in technology to gain a competitive edge

“There’s an evolution of our business model that’s occurring. We, like other leaders in their respective industries, are going to become a data company. We are going to figure out how to monetize the plethora of data we have access to, whether it’s through AI integration or anything else. We are investing in technology at well above our historic rate to repay the tech debt that has built up. There is a competitive advantage that we’re going to have, given our size and scale.”112

—Brian McDade, chief financial officer, Simon Property Group

Show more

Even more impactful might be when data sources can speak to one another. Combining information technology, operations, and customer data can help support decision-making at the highest levels.

Too much data also isn’t helpful, and it’s important to select the right data tools to improve efficiency. It’s also important to find data sources that challenge the status quo rather than those that just validate existing thinking. Here is where emerging technologies can play a role.

When we asked our respondents about their interest and investment in emerging technologies, AI, a new choice this year, far and away outpaced other technologies in hard dollar commitments. Seventy-two percent of respondents say their organizations are either in piloting, early-stage implementing, or in full production with solutions enabled by AI (figure 11). With the emergence of generative AI capabilities in early 2023, global real estate leaders appear to be interested in exploring its use cases for the industry. Common applications could include automation of property acquisition or disposition recommendations, leasing and tenant management, property management, due diligence, and market analytics, among others.

Digital twin technologies, virtual replicas of buildings that use real-time data from smart sensors to better track utilities usage, came in second among respondents with 67% in hard dollar commitments, followed by smart contracts, self-executing transaction protocols stored on the blockchain, at 63%. Last year’s hot button concept, the metaverse, saw some waning momentum; it still represents the largest share of respondents who simply have no interest in the capabilities at 21%. However, there was a 5% increase in respondents whose firms put a metaverse-targeted solution into production from last year.

Actionable guidance to consider

- Do it now to compete for talent. New employees are seeking organizations with increasingly complex technology capabilities and integration so that they can hone their skill sets.113 Lagging technology capabilities could be a growing deterrent to attracting candidates into the real estate industry.

- Reevaluate what is possible; data is changing faster than you think. See what other leaders or industry early adopters have done and follow their leads, even in other sectors or disciplines. Keeping up with the latest and greatest is often like hitting a moving target. Innovative ideas that you may have had a few years ago, but not acted on, may already be getting stale.

- Establish a checks-and-balances technology decision-making process and expect more from the technology you choose. Do not settle for generic solutions for singular functions; that is what built up the monumental technical debt in the first place. Use committees or buying teams across departments to help guide technology acquisition decisions.

- Don’t be afraid of what’s out there. Consider emerging technologies as a legitimate means to an end rather than simply a passing fad. Explore the viability of use cases for your specific needs across solutions powered by concepts such as AI, digital twins, or smart contracts.

Building on a stronger foundation for the future of commercial real estate

Developments across the commercial real estate industry will likely be under the microscope for the remainder of 2023 and into 2024. How industry leaders choose to navigate the coming 12 to 18 months could be crucial in establishing a sturdy base of operations for the long term.

Recent changes to the real estate landscape could forever shape the trajectory of the industry. Some property sectors are poised to exhibit drastically different fundamentals than ever before. Sustainability considerations should be paramount through the entire life cycle of buildings, not only for environmental preservation but also for property value preservation. New and impending tax rules need to be navigated. Hybrid work is likely here to stay, and employers should adapt their workplaces to “earn” their employees’ commute. Efficiencies gained through operations and technology transformation can transform the industry. Leaders that treat these industry shifts as new foundational realities could position their firms with the stable footing needed to build for the future.

Jeffrey J. Smith

United States

Kathy Feucht

United States

Renea Burns

United States

Tim Coy

United States

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}