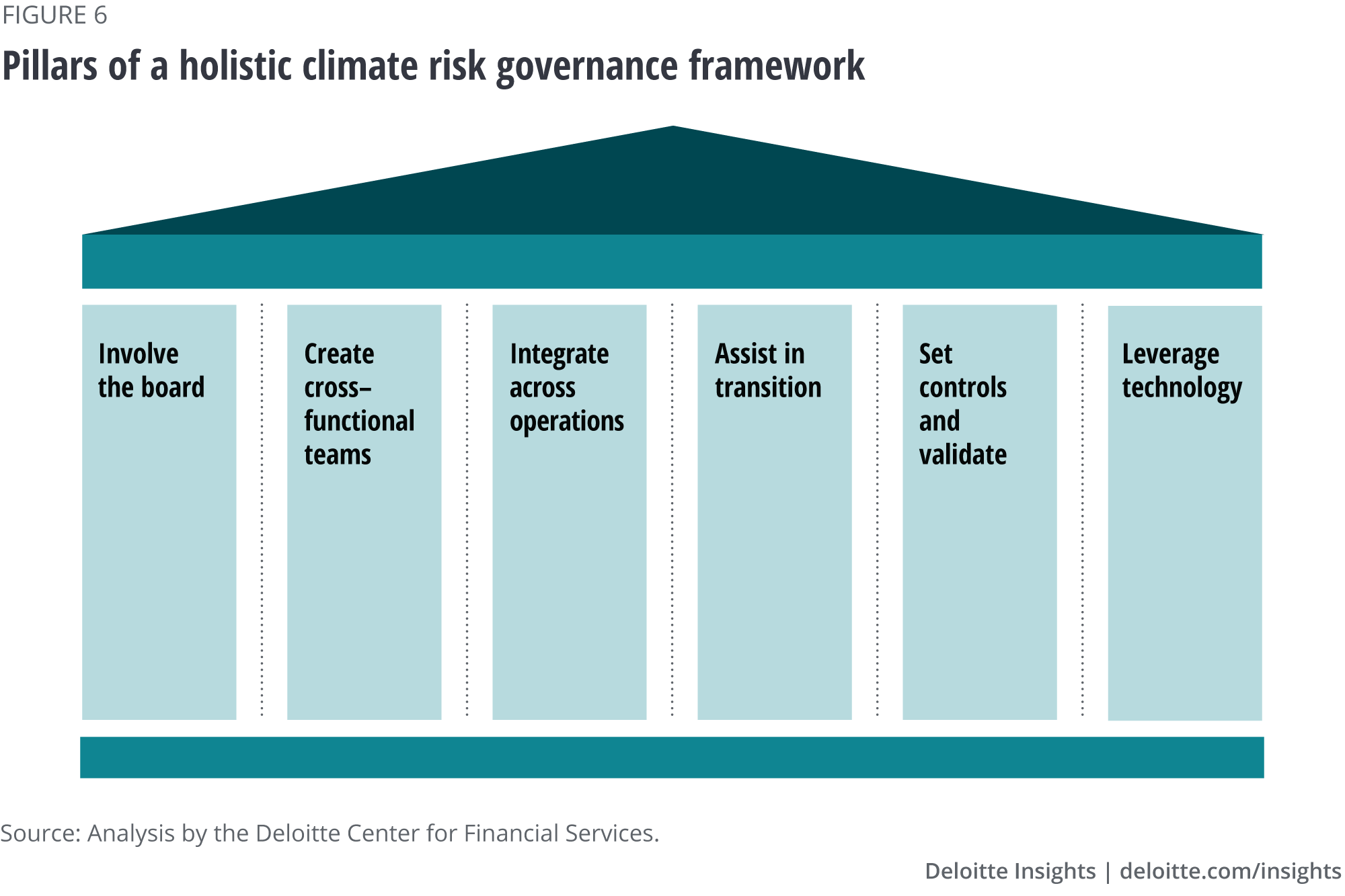

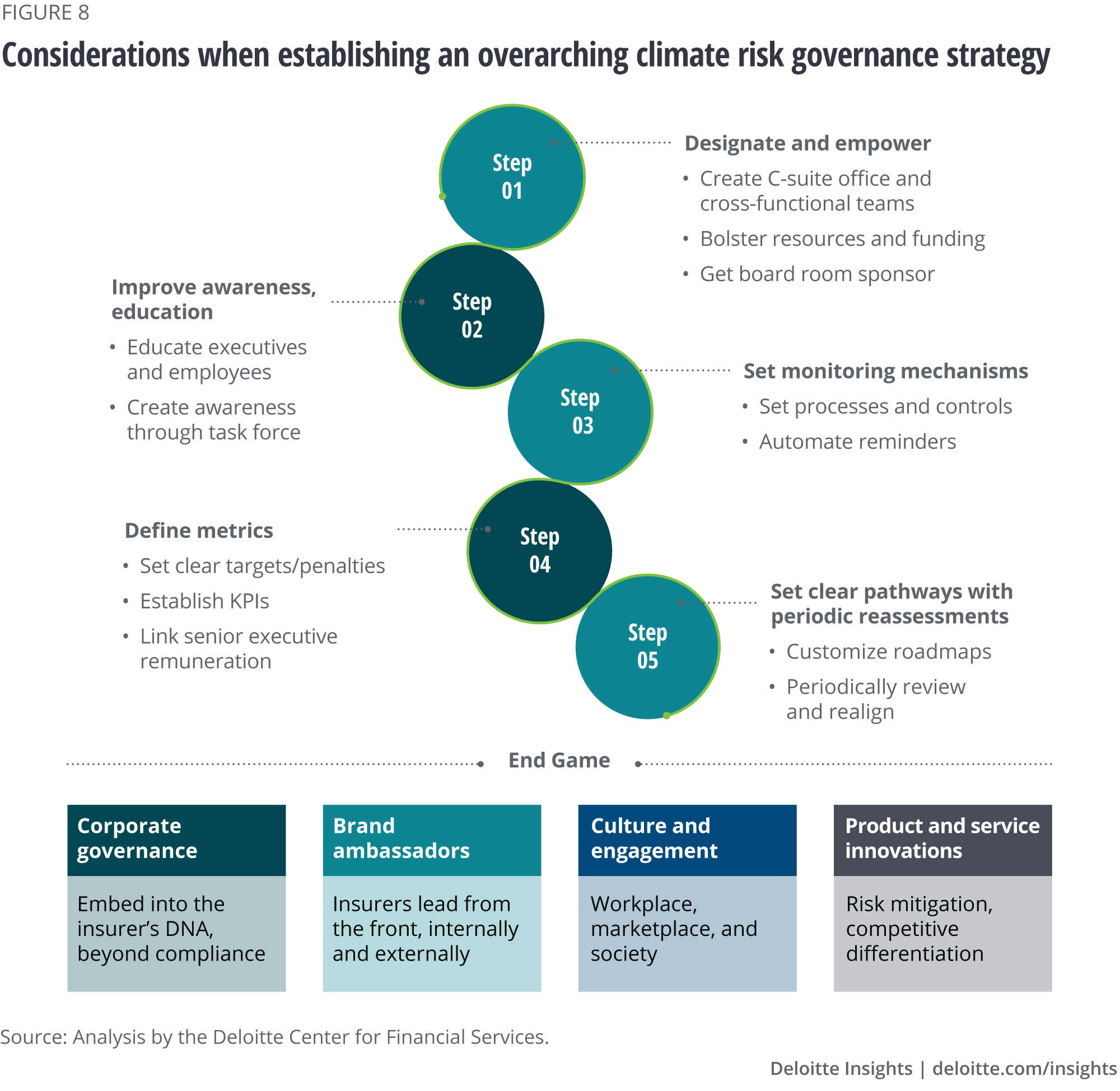

Assist in the transition: Establishing adequate measurement and reporting Scope 1 and 2 emissions (direct and indirect emissions from an insurer’s own operations) is important to maintaining compliance, but carriers can also play an important role in helping advance disclosure across their external insurance value chain—from distribution to third-party suppliers and alliance partners—as well as policyholders—all of which may feed into an insurer’s Scope 3 emissions. Insurers can help by educating and guiding value-chain partners to be compliant with climate risk disclosure requirements as well as by assisting stakeholders in managing transition risk.

One example is reducing premium costs for policyholders focused on clean-energy and decarbonization efforts. Chubb is tightening its requirements on insurance policies for oil and gas producers to reduce emissions of the greenhouse gas methane. As part of its underwriting process, Chubb looks to verify whether policyholders are taking required steps toward decarbonization.14 AXA has also developed sector-specific guidelines for direct investment and underwriting to ensure consistency with its climate risk strategy and sustainability goals. The company further plans to increase premiums from green insurance products15 to Euro 1.3 billion by 2023.16

Given the industry’s focus on risk management and loss control to protect lives and property, insurers invest heavily in risk analysis and loss control resources, and most already have the capabilities to prudently assess and price climate-related exposures,17 whether physical, transitional, or reputational. As a result, insurers may be uniquely positioned to serve as sustainability brand ambassadors, and many are even leading from the front. The Hartford, for one, embedded climate-sensitive principles in its underwriting and enterprise risk management practices, increased the share of personal lines products that reward energy-efficient behavior, designed commercial products specifically for the sustainable energy industry, and offered coverage for energy-efficient construction and development projects.18

The industry should also continue its external risk mitigation efforts by helping bolster building codes, seeking to enhance zoning restrictions in areas exposed to high climate risk, and initiating other proactive loss control efforts.

Set controls and validate metrics: Measuring climate risk may come naturally to the industry, which for decades has focused on understanding weather, climate, demographics, and other mitigating factors based on real-time and historical data, as well as increasingly advanced predictive modeling capabilities.

With climate risk and broader ESG data being treated more like financial data in terms of compliance, carriers should ensure adequate controls before the information makes its way into filings and public reports.

Insurers should therefore be periodically reassessing climate metrics to confirm their validity and keep up with changes in compliance requirements. They should also work with industry groups to convince stakeholders watching over them to establish more standardized monitoring and rating systems, which could help enable clearer comparisons and save valuable resources by eliminating unproductive, repetitive reporting.

Leverage technology: Insurers should consider deploying more enabling technology, including centralized digital platforms, that can act as a repository for managing climate risk-related data and tasks, automating basic data gathering, and providing consistent historical data to help monitor and streamline reporting. Technology can further serve as a catalyst to spark innovative problem-solving, such as by using advanced analytics, artificial intelligence, and machine learning to help identify, quantify, and limit climate risk in current portfolios, as well as to help prospectively avoid such exposures in future policy underwriting and investments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}