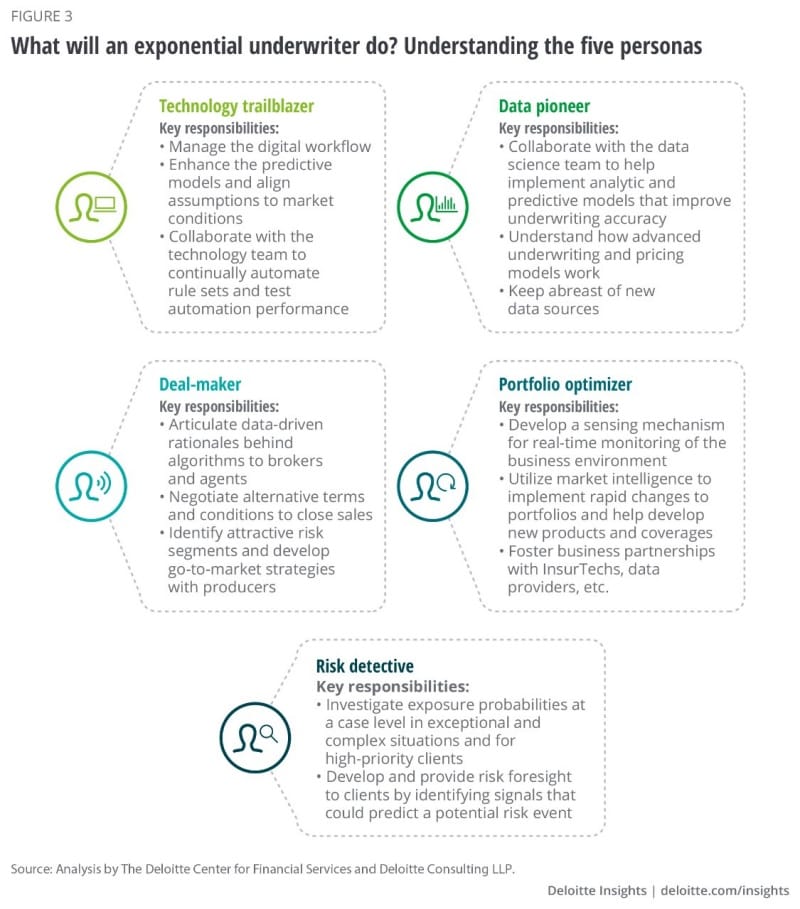

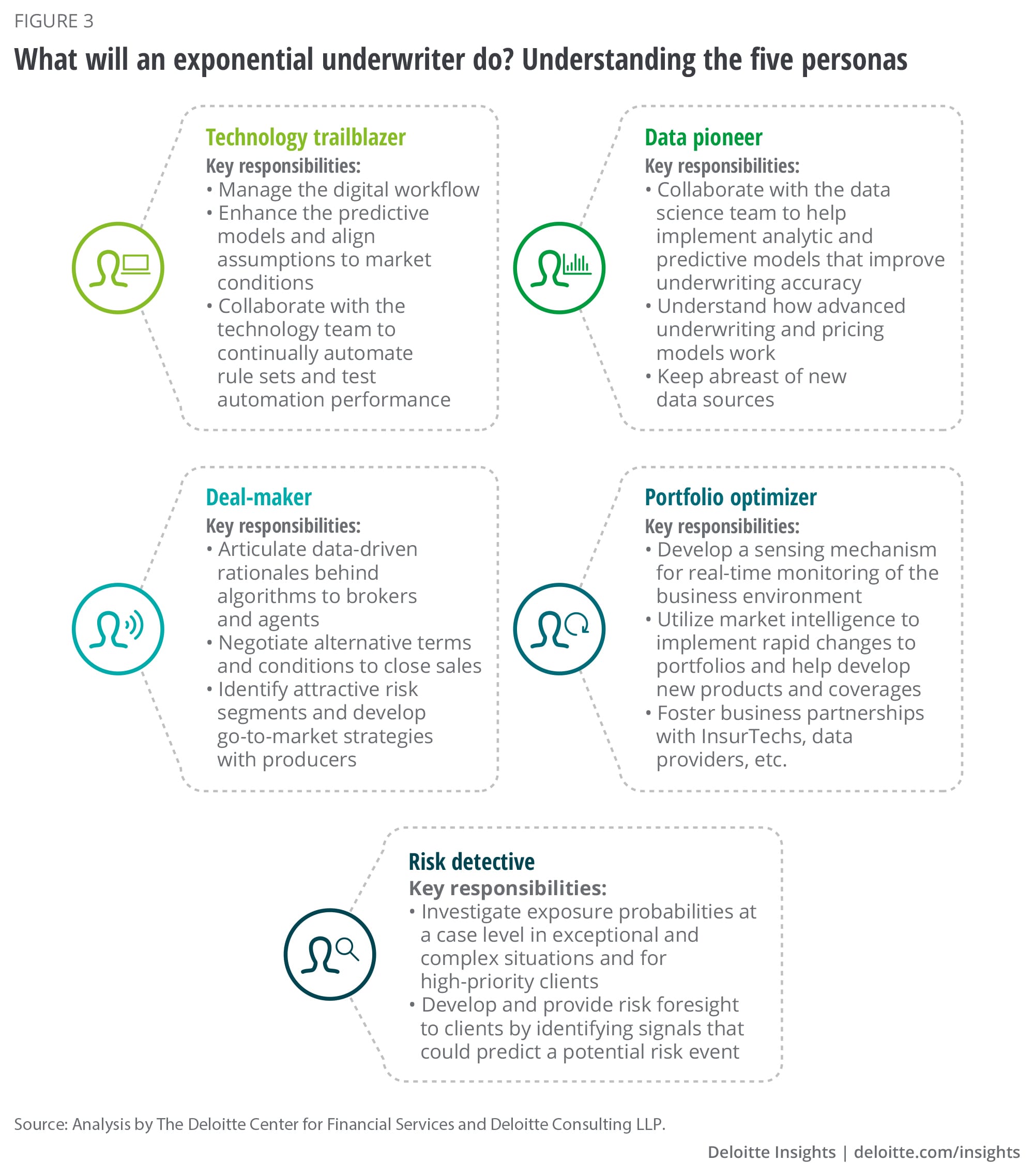

1. Technology trailblazer

Exponential underwriters would likely be in charge of managing the digital workflow. They would be owners and supervisors of automation programs, tweaking them regularly to optimize performance and improve operational efficiency. As Heather Milligan, senior vice president, life underwriting at Lincoln Financial Group, explains, “Underwriters are starting to own implementation of AI programs and are driving automation priorities by working on rule engines and their interfaces. This progression is likely to continue as real-time underwriting decisions become more important.”

Underwriters should collaborate closely with IT teams to refine underwriting platforms, automate rule sets, and test the automation’s performance. And with the emergence of no-code/low-code development platforms, such as Mendix and Unqork, exponential underwriters will likely become more involved in the software development process itself, further reducing time to market and cost.10

2. Data pioneer

With increased use of predictive datasets, such as electronic health records and pharmacy scans in life insurance and telematics and industrial sensor data in P&C, underwriters should closely collaborate with data scientists to design, develop, and implement analytic and predictive models to improve underwriting and pricing accuracy. Tim Ranfranz, head of risk selection strategy at Northwestern Mutual, said he sees “underwriters working with data scientists and data engineers and helping them understand the data, how it is coming in, and why we use data in the way we use it for our traditional underwriting. I think there’s a healthy partnership there.”

Data pioneer underwriters will likely need to master how models select or price risks to ensure decisions are defensible to challenges from distributors, clients, and regulators. This knowledge could also be used to train front-line underwriting peers on how to provide data-driven advice to clients. In addition, data pioneers could monitor model outputs and rule sets, identifying when to update rules to reflect realities of market conditions and stay ahead of the competition.

Data pioneers should also be at the forefront of developments in the InsurTech and data provider space within underwriting. Working with data scientists, they can scout for and experiment with new datasets that could help refine models in a cost-effective manner.

Finally, as the human face for an increasingly automated underwriting function, they could also engage with regulators early in the development of models and their underlying data sources. This could create more transparency and alleviate any regulatory concerns.

3. Deal-maker

As insurers increasingly use predictive models to assess risk and price policies, underwriters will likely be called upon more often to partner with sales teams to explain the rationales behind their decisions to agents and brokers as well as applicants. They will also likely be called upon to help negotiate alternative terms and conditions to close sales rather than present their determinations as “take it or leave it” deals.

As Heather Milligan at Lincoln Financial explains, “You’ve got to get on the phone and be personable with the producer and explain why you did what you did.”

Finally, they could also help account managers identify attractive risk segments and develop go-to-market strategies with producers. In their role as a deal-maker, exponential underwriters will also likely be tasked with cross- and up-selling activities.

4. Portfolio optimizer

Underwriters could also take a lead role in developing a robust market-sensing mechanism to provide real-time monitoring of the business environment. This market intelligence would help them make rapid changes in overall risk portfolios in response to market trends, which should ultimately boost profitability.

“The underwriter of the future is going to be a great portfolio manager and will have the tools and the analytics for that and will be able to spend more time in that capacity,” said Michael Harnett, CUO, North America at Everest Insurance. “The underwriters with a more granular understanding of margin analysis and how to optimize portfolios—that’s where we are heading. And I think that’s where the industry will probably be forced to head in order to maximize the efficiency around capital and capital allocation.”

At the same time, this market intelligence could be utilized to help develop modular products or enhance product sophistication, which could give companies a competitive advantage.

5. Risk detective

In this role, underwriters would likely dedicate a significant portion of their time to assessing exposure probabilities at a case level in exceptional and complex situations and for high-priority clients. Being a risk detective would require underwriters to develop a deep business understanding, risk assessment expertise, and exemplary communication skills. “The complexity of what [exponential underwriters] are going to do when it comes to risk assessment will be increased, because that easier stuff—maybe the lower face amount, the younger ages, the more healthy population—that will be running through our accelerated model or our straight-through processing,” said Erin Corrao, head of new business development at Northwestern Mutual. “That leaves the complex work for the human risk assessment.”

Risk detectives would also focus on developing and providing exposure foresight to clients, by identifying signals that could predict a potential event that could be avoided or at least mitigated.

Finally, exponential professionals could be called upon to shepherd new underwriters identified for this persona by sharing their tacit knowledge gained through experience. In fact, this knowledge exchange would have to be reimagined; as vanilla cases get automated, it could be harder for new underwriters to acquire investigative skills on the job. Risk detectives may have to develop their own expertise and that of their teams in different ways than they do today, such as getting involved with industry groups at a younger age and implementing innovative apprenticeship models.

What is the right mix of exponential underwriter personas?

Should insurers focus their resources more heavily on developing an underwriting workforce that thrives as portfolio optimizers but not as much on data pioneers? Or should they be more heavily skewed toward a workforce that thrives as deal-makers, or equally balanced across all personas?

There is no “right” combination as needs will vary company to company. Insurers should identify the unique mix of personas that their underwriting workforce will likely require based on factors that drive their underwriting strategy, such as their lines of business, the composition of their customers, the demands of their distribution channels, and overall market strategies.

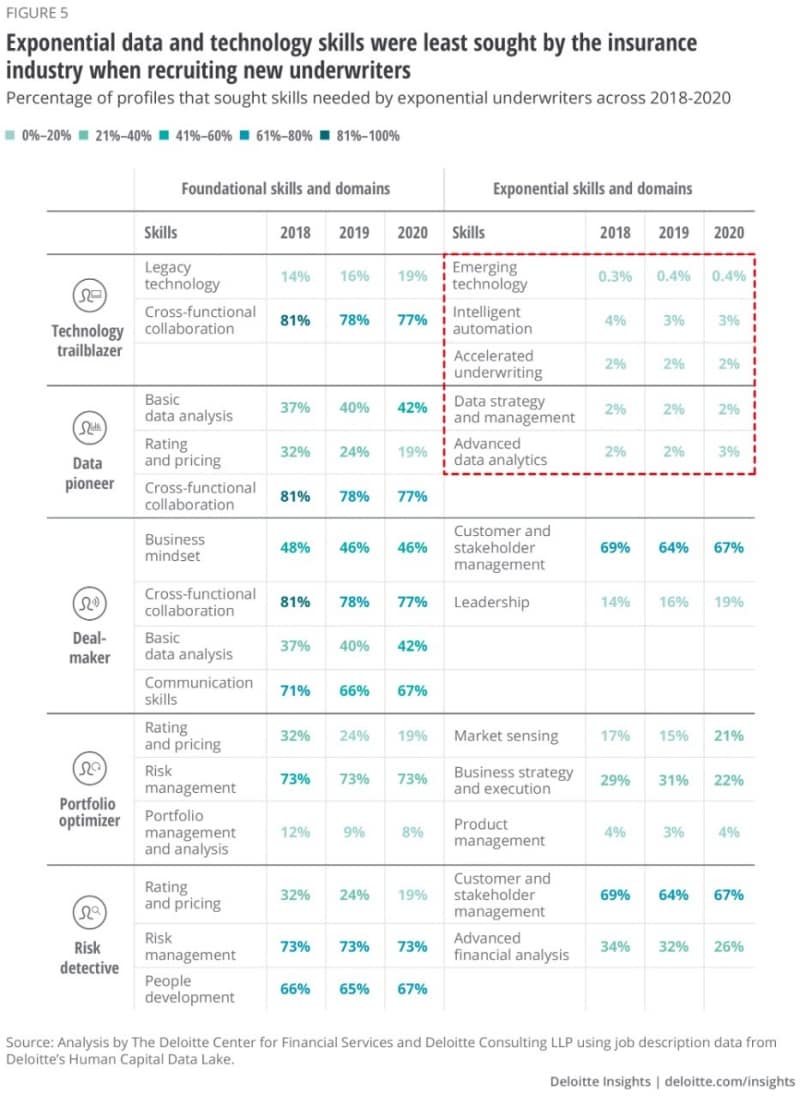

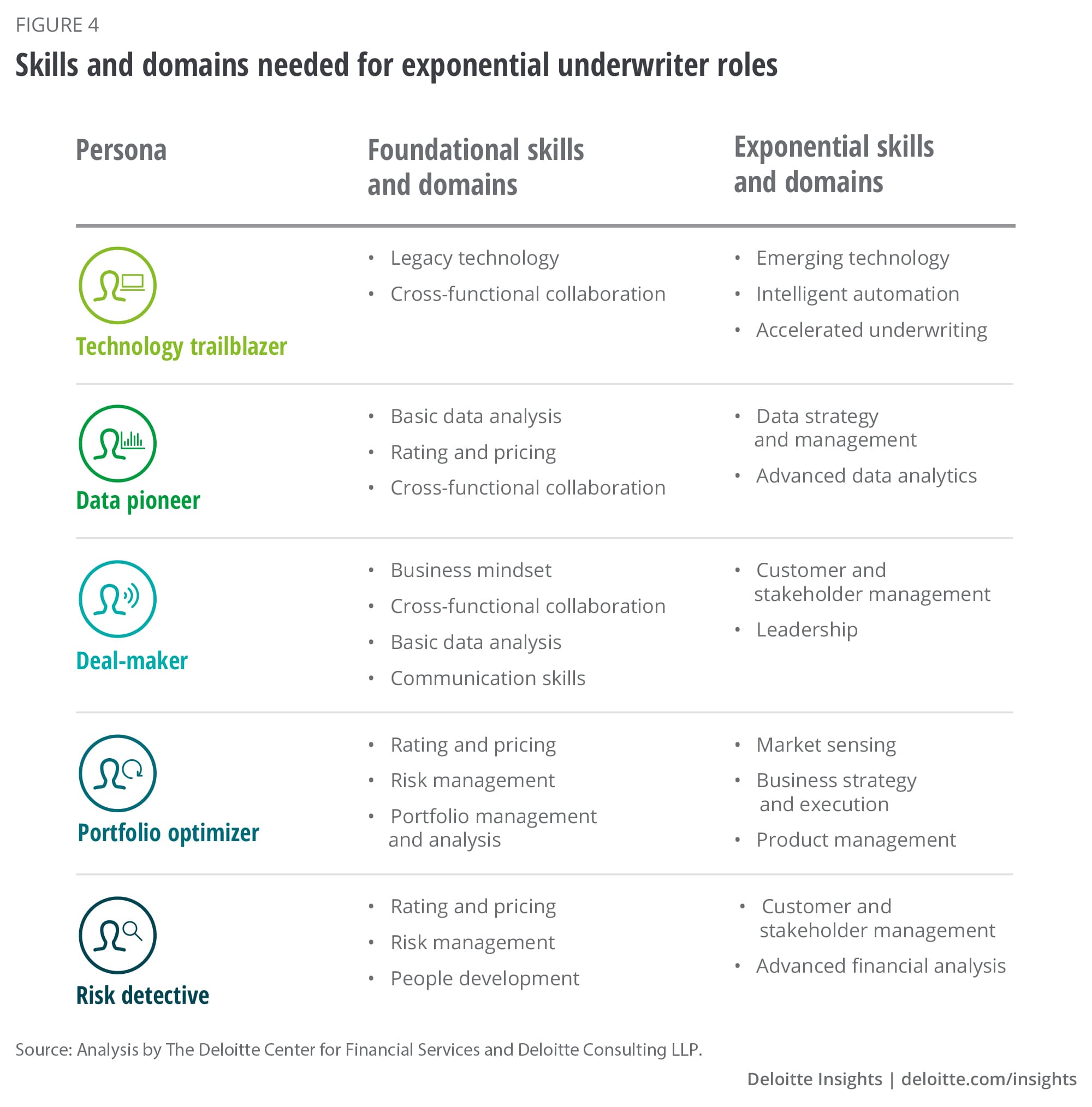

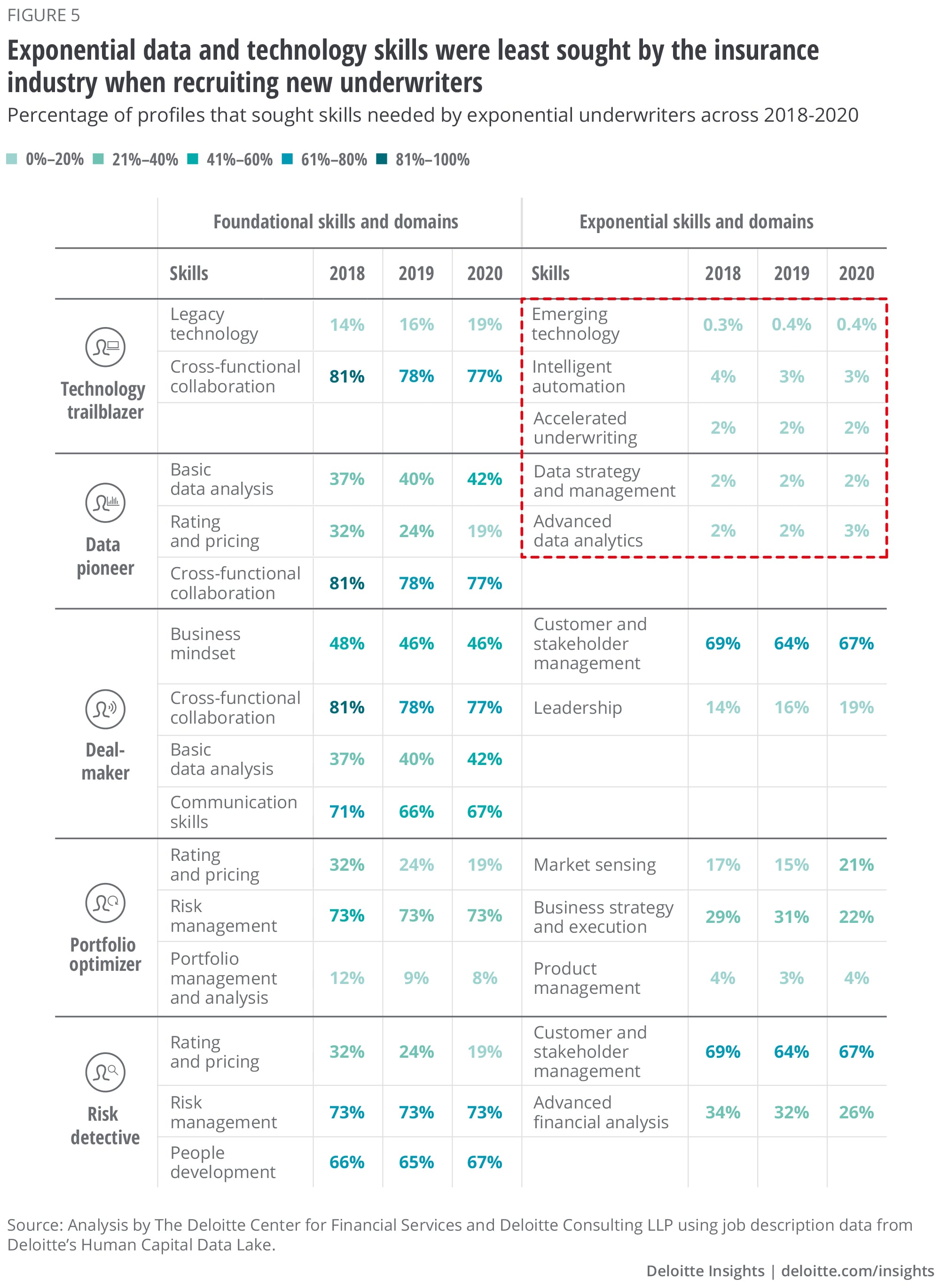

Are insurers recruiting people who have the skills needed to become exponential underwriters?

Our CUO conversations helped us uncover specific skills that future underwriters would likely need to cultivate to take on each of the exponential personas. Many of those skills can be developed by upgrading capabilities that underwriters likely already possess in their current roles. However, to upskill their workforce and develop multidimensional exponential professionals, insurers should also cultivate skills and expertise in domains that are typically not considered traditional to underwriting (figure 4).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}