M&A emerges from quarantine M&A strategies to thrive in the post-pandemic environment

15 minute read

17 December 2020

Globally, companies announced a record $1.4 trillion worth of M&A deals in the post-lockdown months. A good proportion shows efforts to transform themselves and thrive after the pandemic with deals to secure supply value-chains or to acquire innovative and sustainable technologies.

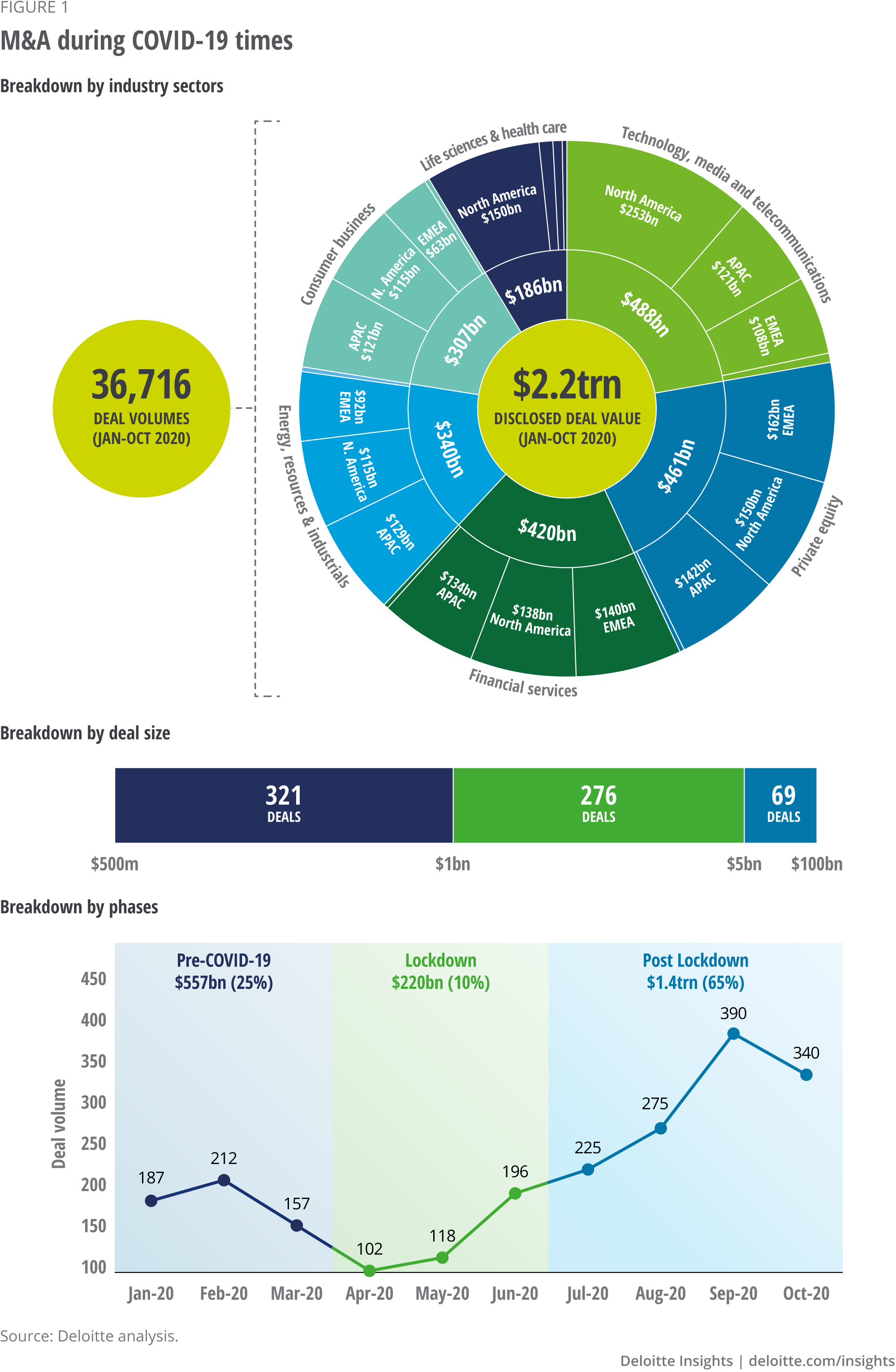

In a year besieged by pandemic uncertainties, M&A rode a roller coaster. In the first half of the year, lockdowns led to a sharp dive. But as soon as these began to ease, M&A soared back up. Globally, companies announced a record $1.4 trillion worth of deals in the post-lockdown months from June to October 2020, 84 per cent higher than in the first five months of the year, leading to a total value of $2.2 trillion worth of deals in the first 10 months of the year.1 The positive news on COVID-19 vaccines has also given a significant boost to corporate confidence – over $40 billion worth of deals were announced in the week the first news about the high efficacy of coronavirus vaccines was reported.2

All regions and sectors benefitted from this resurgence. In particular, there was a strong uptick in the mega-deal (>$5bn in value) category (figure 1). Many were all-stock deals, signalling that acquirers want to preserve cash, in a way acknowledging some of the integration risks brought on by economic uncertainties. 3

Learn More

Explore the Strategy collection

Explore the Leadership collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app.

These extraordinarily difficult times have created unique opportunities. While some of the M&A activity recorded was due to companies resuming deals put on hold during the economic freeze generated by the different national lockdowns, a good proportion also reflected company efforts to transform and thrive in the post-pandemic world. This is why in recent months we have seen not just traditional consolidation-driven M&A but also non-traditional deals, such as cross-sector alliances, co-investments with private equity, divestments of prized assets, deals to secure supply value-chains, and disruptive M&A deals to acquire innovative and sustainable technologies.4

The long road to post-pandemic recovery has just begun. Given the high stakes, in the Autumn 2020 edition of the Deloitte European CFO survey, we asked around 1,500 CFOs across 17 countries about their M&A objectives, strategic priorities, execution risks and post-deal value-creation challenges.5 In this report, we examine the findings of the survey and present implications for dealmakers.

CFO sentiments on drivers for M&A

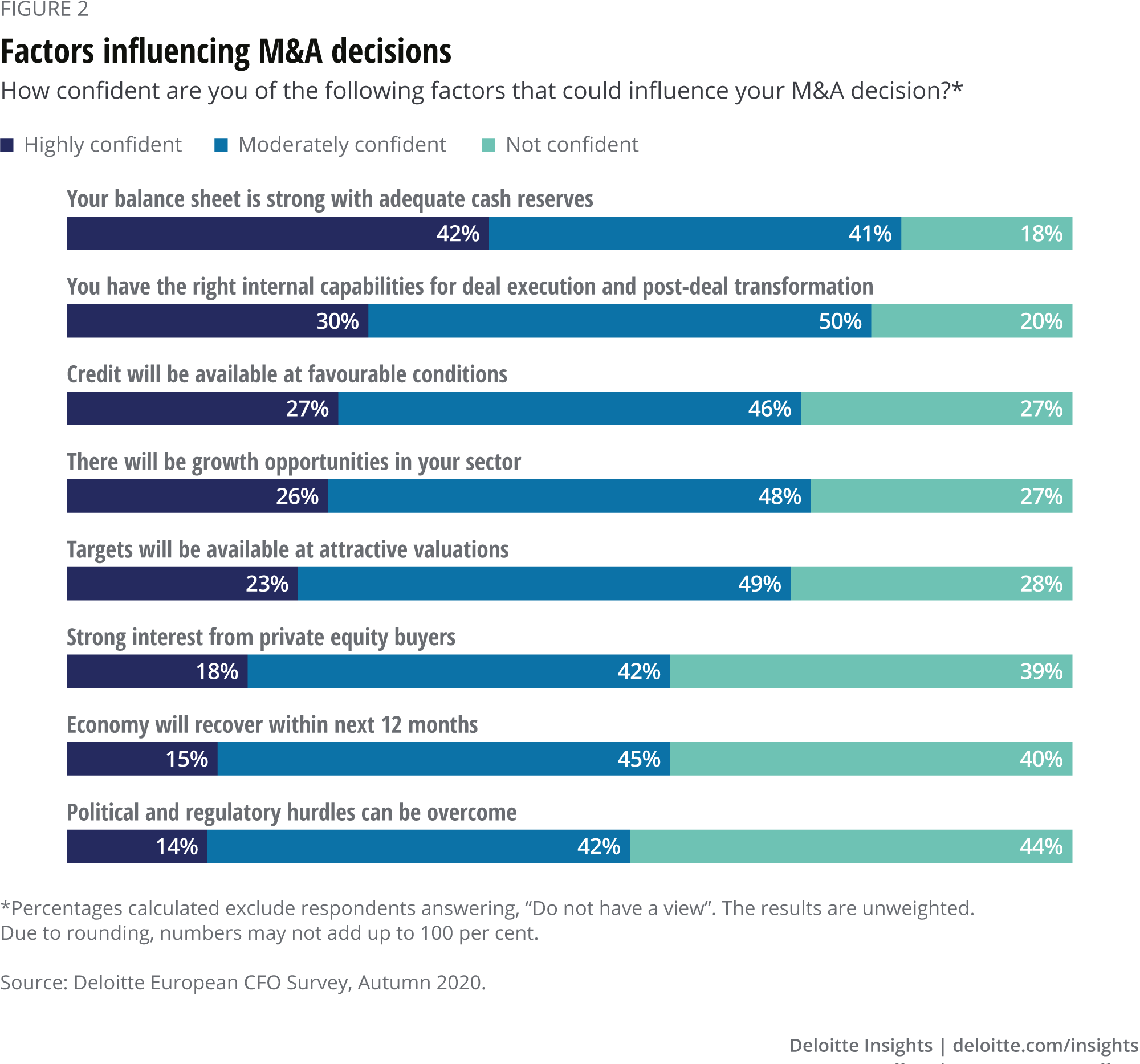

In order to ascertain the headwinds and tailwinds for M&A, we asked CFOs to rank the internal and external factors that will influence their M&A strategies and priorities within next 12 months (figure 2).

Tailwinds – confidence in financial strength

Around 83 per cent of the CFOs reported high levels of confidence in the strength of their balance sheets, and this was the case particularly with CFOs from the financial services, automotive and professional services sectors. The confidence can partly be explained by the long-term shift towards capital and cash preservation that followed the 2008 financial crisis. Since then, the corporate sector has been steadily increasing their cash reserves, and in Europe, at the end of the second quarter of 2020, EURO-STOXX 600 non-financial companies had a record $1.07 trillion in cash and short-term investments.6 On the other hand, CFOs within companies that are not confident about their financial strength indicated they are planning to pursue divestments of non-core assets to shore up their balance sheets.

In addition, with no signs of an imminent reversal of the current highly accommodative monetary policy, around 73 per cent of CFOs report that they are confident about the availability of credit. Many listed companies in Europe took advantage of the favourable credit markets to raise around $1.04 trillion in investment-grade bonds this year.7 Others took advantage of specific government interventions to strengthen their finances, such as emergency measures providing extended credit lines, liquidity guarantees, or deferrals of taxes and social security contributions.8

Tailwinds – confidence in growth opportunities

Around 73 per cent of the CFOs are also confident about growth opportunities in their sector, especially in financial services, life sciences and technology, media and telecommunications (TMT). Price is also not seen as a problem: around 74 per cent of CFOs are confident acquisition targets will be available at favourable valuations. However, as their company’s business model may be changing, finance leaders need to evaluate prospective deals on their strategic fit, not just attractive valuations. In addition, around 80 per cent of CFOs have reported confidence in their internal deal execution and integration capabilities. Companies face the formidable task of realising synergies under extremely challenging conditions. This means they need to revise their standard integration playbooks and incorporate virtual, digital and analytical tools extensively in the post-deal value-creation process.

Headwinds – the economy and regulatory hurdles

When it comes to headwinds for M&A, it comes as little surprise that the majority of CFOs are concerned about the external environment. Around 40 per cent of CFOs are not confident that there will be an economic recovery within the next 12 months, and almost half the respondents (44 per cent) are wary about their ability to overcome political and regulatory hurdles to complete M&A transactions. Earlier this year the EU Commission announced a broadening of member state referral systems concerning mergers, while in the UK the government has also announced new proposals to safeguard sensitive UK assets from being acquired by overseas companies.9 Despite the tailwinds, we should expect a degree of caution and prudence as companies evaluate deal opportunities.

Rethinking the strategic role of M&A from respond to recover and thrive

The post-pandemic world is expected to unleash structural and systemic changes, and it is widely expected that recovery will be highly asymmetric across regions and sectors. Companies will need to decide the direction of their strategy, identify the new capabilities required and prioritise the markets where they need to operate in order to drive growth and profitability.

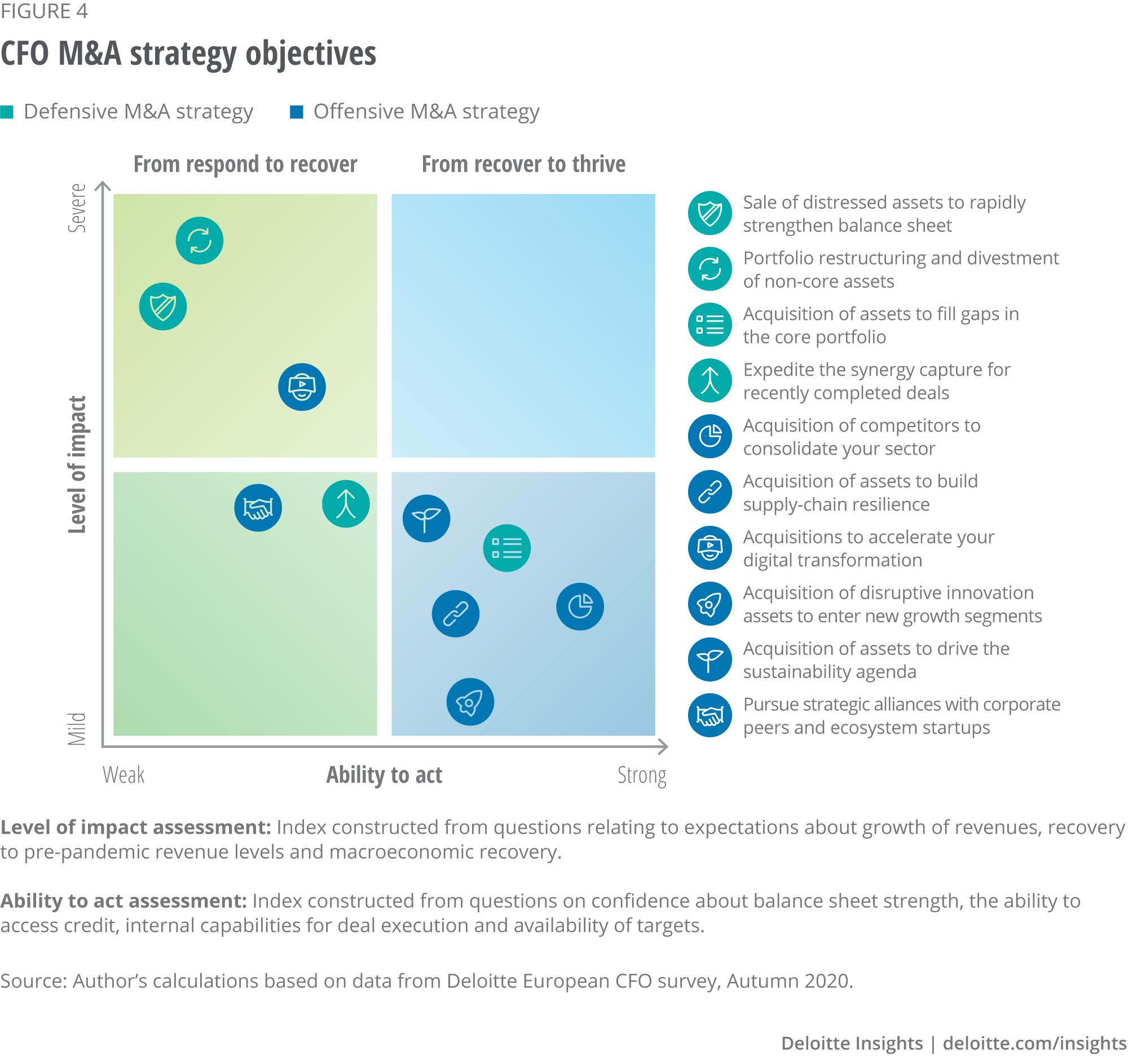

In a recent Deloitte report called “Charting new horizons”, an M&A strategy framework was presented to help companies prioritise their strategic choices and develop a pathway through the three phases of a crisis: from responding to the shock, to recovering and finally thriving in the new business environment.10 Redefining M&A plans in terms of these scenarios and choices will bring much needed clarity of purpose while confronting uncertainties (figure 3).

In order to understand the role of M&A in companies’ journeys, we used the survey results to reconstruct the framework, creating two indices that measure how companies score on the two critical dimensions: ‘level of impact’ and the ‘ability to act’.11 We asked CFOs to prioritise M&A objectives for the short (< 6 months) and medium (6-12 months) term and then evaluated their responses against the indices. This allows for a determination of how the strategies are playing out based on the pathways different companies are choosing as they move from respond to recover and thrive.

The analysis shows CFOs are using a combination of defensive and offensive strategies to safeguard their position in the market, accelerate recovery and position themselves to achieve market leadership (figure 4).

We found that CFOs of companies more severely impacted by the crisis were focused on survival and prioritised defensive measures to salvage value through the rapid sale of assets, divestment of non-core assets and portfolio restructuring. Many companies whose business models have been adversely impacted but have the ability to respond have indicated they want to expedite synergy capture from recent acquisitions to bolster their balance sheet, acquire technology assets to accelerate digital transformation, and pursue strategic alliances with a wide range of players to set them on the path to recovery.

On the other hand, companies that were relatively less affected and also feel confident about their ability to respond prioritised M&A objectives in line with transformation and growth aspirations. These included acquiring assets to close gaps in their portfolio, driving their sustainability agenda, building supply-chain resilience and acquiring disruptive innovation assets to enter into new growth segments.

On balance, 59 per cent of the respondents selected strategies related to offensive M&A, while 41 per cent selected defensive ones. Companies are increasingly pursuing non-traditional M&A activities, such as joint ventures, alliances, disruptive M&A and venture investments in sustainable assets (32 per cent), in addition to portfolio restructuring activities leading to divestments (21 per cent) and more traditional M&A deals, such as consolidation plays (47 per cent).

We take a detailed look into all these M&A strategies in the breakout box below.

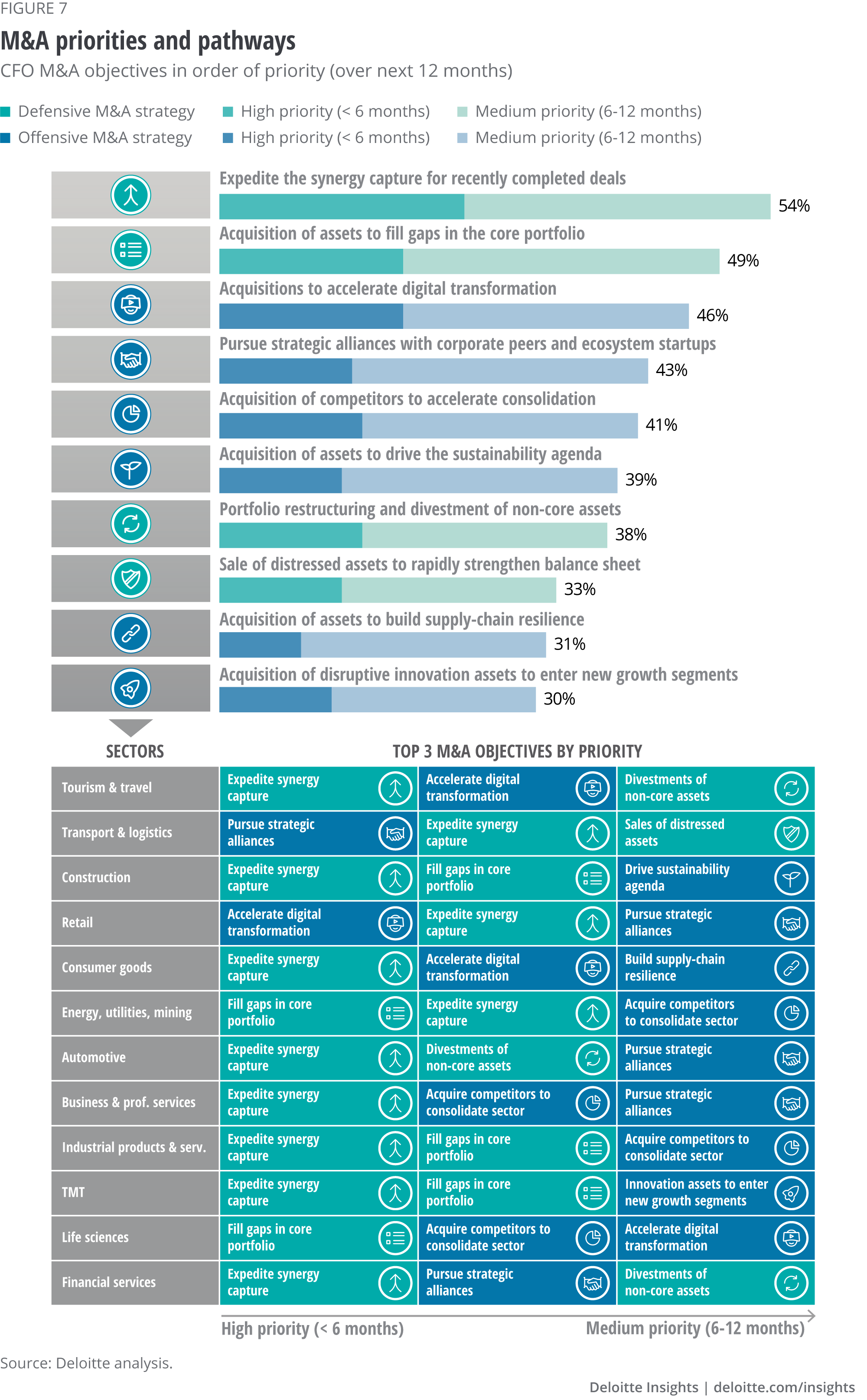

M&A priorities and pathways

Below we outline a range of strategies, highlighting their role in different phases of the journey from respond to recover and thrive.

From respond to recover

Companies that have been severely impacted by the crisis and are in a financially vulnerable position are taking decisive measures to secure their survival. Meanwhile, companies where the impact has been less severe have indicated they plan to use M&A to safeguard markets and build operational resilience.

From recover to thrive

Companies with a strong balance sheet but expecting significant degree of structural disruption have indicated they wish to use M&A to rebuild supply-chain links and accelerate the long-term transformation of their business models. Meanwhile, for companies that are financially resilient and strategically well placed, this crisis presents unique opportunities to use disruptive M&A strategies to invest at the edge of their business and position themselves to become market leaders in years to come.

Execution priorities – how will your next deal differ?

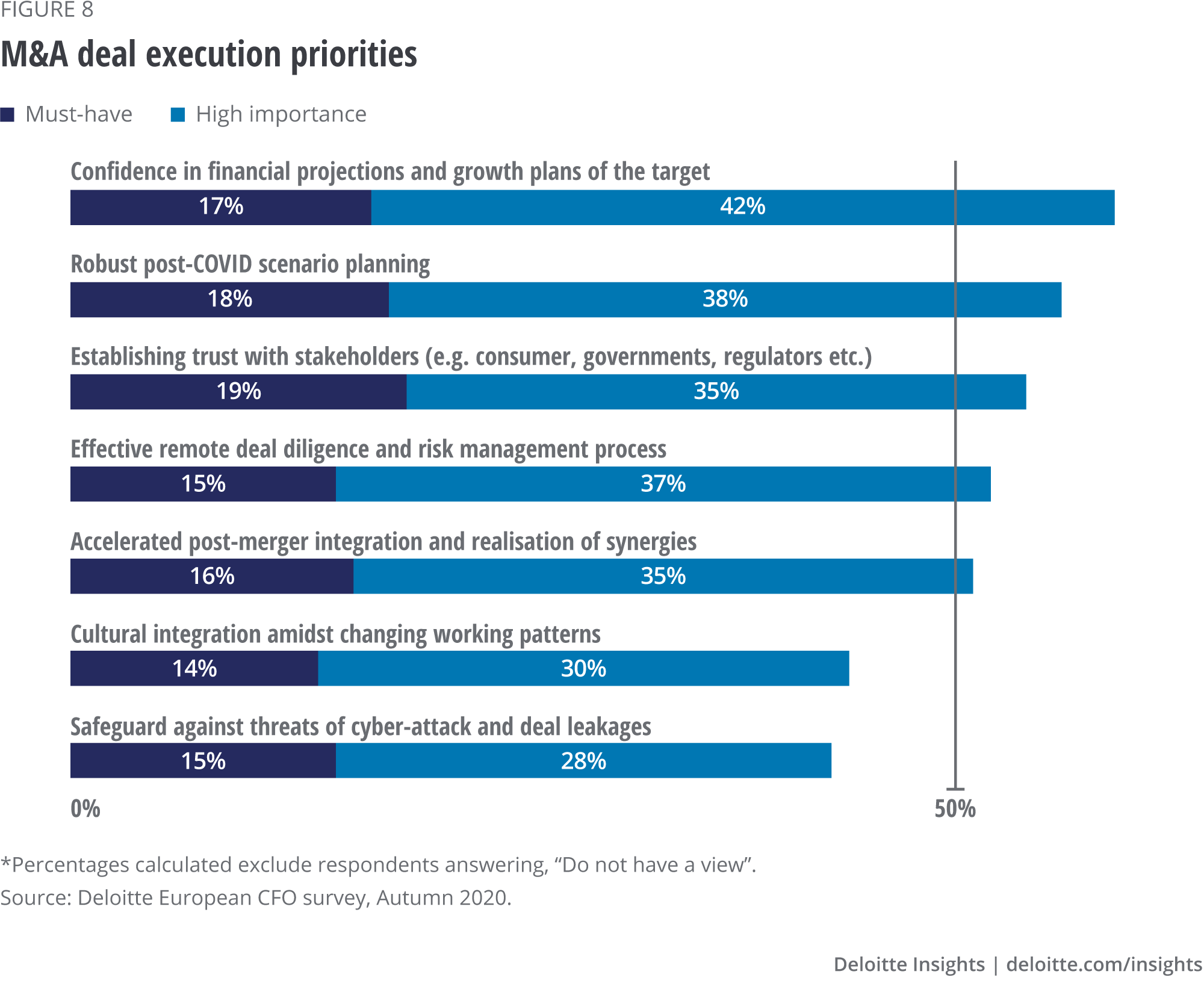

The pandemic has fundamentally changed the environment for transacting M&A deals. Well-enshrined features such as onsite visits for the purposes of conducting operational due diligence and face-to-face conference-room negotiation marathons will probably no longer be standard. Instead, the use of digital and analytical tools is likely to remain an integral part of the entire M&A process, from sourcing and execution, all the way to post-deal value creation. We asked CFOs about deal execution priorities, and their responses show they are adapting to these shifts (figure 8).

Forecasting may require new maths: Nearly 60 per cent of CFOs acknowledge that gaining confidence in the finances and growth plans of possible targets, and robust post-COVID-19 scenario planning, are top execution priorities. Indeed, given the current unprecedented circumstances, historical financial data may become less reliable for forecasting purposes. Instead, companies may want to focus on scenarios and projections across a range of pandemic/recession durations.14 The due diligence process may also need to be extended, focusing on areas where vulnerabilities may have been exposed, including the impact of changing scenarios on valuations, supply chains or IT infrastructure.

Reinventing the M&A process: About 52 per cent of respondents have highlighted having effective remote deal diligence processes as a priority. The virtual environment is expected to remain central to deal-making for the foreseeable future. The sheer volume of deals done this year means companies have already started using virtual and digital tools in the M&A process. The consistent use of predictive analytics, artificial intelligence and automation technologies in the post-deal value-creation process can help extract deeper insights in business domains, identify risks and uncover new synergy opportunities. Leaders need to pay particular attention to ensure cultural integration is handled sensitively in the virtual environment.

Trust takes centre stage: The pandemic has firmly put the spotlight on trust, and it has emerged as a fundamental corporate objective. Nearly a fifth of CFOs have identified it as a must-have, the highest share across the ‘must-have’ priorities. In our recent study, “Future of Trust”, we have identified the four human dimensions of stakeholder trust: physical, emotional, financial and digital.15 Building trust while conducting deals in a virtual environment is difficult, and so leaders need to inspire confidence by engaging with the financial, well-being and safety concerns of their teams – and trusting them to do their jobs. If done well, this approach has the potential to accelerate a company’s recovery and enable it to thrive and shape the future.

Cyber resilience: Protecting against cyber risks is, by contrast, not particularly high on the agenda, with fewer than half the European CFOs considering it an important priority. In our recent Future of M&A Trends survey, in which we surveyed over 1,000 M&A executives at US companies, around 51 per cent identified cybersecurity threats as their top concern during the M&A process.16 The growth in virtual execution means cyber data breaches could have dire implications for M&A. If sensitive data is compromised, it could impact deal assessment and valuations, and increase the risk of operational disruptions, regulatory fines, loss of stakeholder trust – and potentially scupper the deal itself. As M&A activities continue to increase, we expect European companies will start giving cyber risk management a higher priority.

Conclusion

The COVID-19 pandemic has unleashed a process of Schumpeterian ‘creative destruction’17 to which no sector is immune. The dismantling of old structures and business models is opening up new growth opportunities.

In order to thrive in the post-pandemic world, companies therefore need to reinvent themselves. The survey results confirm that M&A is likely to play a major role in this transformative process. Companies have the daunting task of navigating their core businesses amid major uncertainties, while remaining alert to new growth M&A opportunities. They must also integrate these acquisitions and deliver returns under challenging conditions.

In a post-pandemic world, companies will also be under pressure to demonstrate the long-term benefits of their M&A activities through stakeholder value creation. In addition to traditional M&A, a wide range of inorganic growth strategies, such as cross-sector alliances, co-investments with private equity, venture investment in disruptive technologies and partnerships with governments, have become important in this process.

Industry leadership needs to consider, too, the environmental and societal impact of their actions and the ethical use of data in order to inspire trust across a wide coalition of stakeholders, including shareholders, governments and regulators. Well-planned, bold moves will enable companies to cement market leadership together with lasting societal benefits.

Deloitte Global M&A Services

M&A transactions are among the most complex life events an enterprise will undertake. Whether a transaction, integration or separation, Deloitte M&A accesses a cross-functional network of global M&A specialists to support corporates and private equity in maximising value across the deal lifecycle. Our tailored end-to-end services help clients define M&A strategy, access capital or review/reset debt facilities and perform full service due diligence. We stay with clients through the deal to help them capture value by driving results that enhance profits and maximise proceeds from divestitures or exit strategies.

Learn more

Get in touch

- Iain Macmillan

- Managing Partner Global M&A Services Leader

- imacmillan@deloitte.co.uk

- +44 (0)20 7007 2975

© 2021. See Terms of Use for more information.

Discover the CFO collection

-

CEO compensation in a COVID-19 world Article4 years ago

CEO compensation in a COVID-19 world Article4 years ago -

The value of resilient leadership Article4 years ago

The value of resilient leadership Article4 years ago -

COVID-19 and the undisruptable CEO Article4 years ago

COVID-19 and the undisruptable CEO Article4 years ago -

The CEO as ultimate end-user ethnographer Article5 years ago

The CEO as ultimate end-user ethnographer Article5 years ago -