In our previously published report, “A higher bottom line: The future of financial services,” we asserted that the future of financial services largely lies in firms’ ability to reach a “higher bottom line,” one that “values the future of our planet and people just as much as profits. It blurs the line between the striving and the successful until there’s less inequality and more shared wealth… [it] represents both the financial and human profit to be gained from a more educated, equitable, sustainable world.”1 Responsible digital transformation is expected to be a key driver of achieving a higher bottom line going forward.

Responsible digital transformation will mean different things to different stakeholder groups—customers, employees and management, regulators, society, and shareholders. Below are considerations and steps firms could deploy to help achieve this goal, stakeholder by stakeholder.

Customers

As financial services firms digitally transform their operations, focusing on ease of use, personalization, and on-demand services may help drive customer satisfaction.2 Meeting these needs responsibly can help firms differentiate and build their brand value. While firms can focus digital transformation efforts on delivering improved product offerings and providing better customer service, responsible digital transformation goes a step further. It offers customers more transparency and control over their data and ensures data security, all of which can help build trust and engender brand loyalty.

Providing personalized service involves merging disparate data sets, such as credit rating, social media, geolocation, and web browsing history, to derive customer-specific insights. However, if firm communications are too personalized, customers may find it invasive and experience discomfort. In a Deloitte survey of financial services firm customers, most respondents (57%) agreed that privacy has become even more important to them over the past few months.3 Companies that succeed at responsible digital transformation will likely address these concerns by offering customers more transparent and easy-to-understand privacy policies.

Another key aspect of responsibility relates to how companies use artificial intelligence (AI) models to evaluate customers, assess risks, and price offerings. Customers expect that firms should be able to explain the rationale behind their evaluation decisions. For example, if customers are denied a loan, they may want to know the reason so they can take corrective measures.4 If data sourced from third parties feeds into the models, customers may prefer an opportunity to check data accuracy and correct data mistakes, if any. Adopting data governance policies that address these concerns may help improve customer engagement and data accuracy. More broadly, these measures could help customers feel more confident about the firms’ digital transformation.

Employees and management

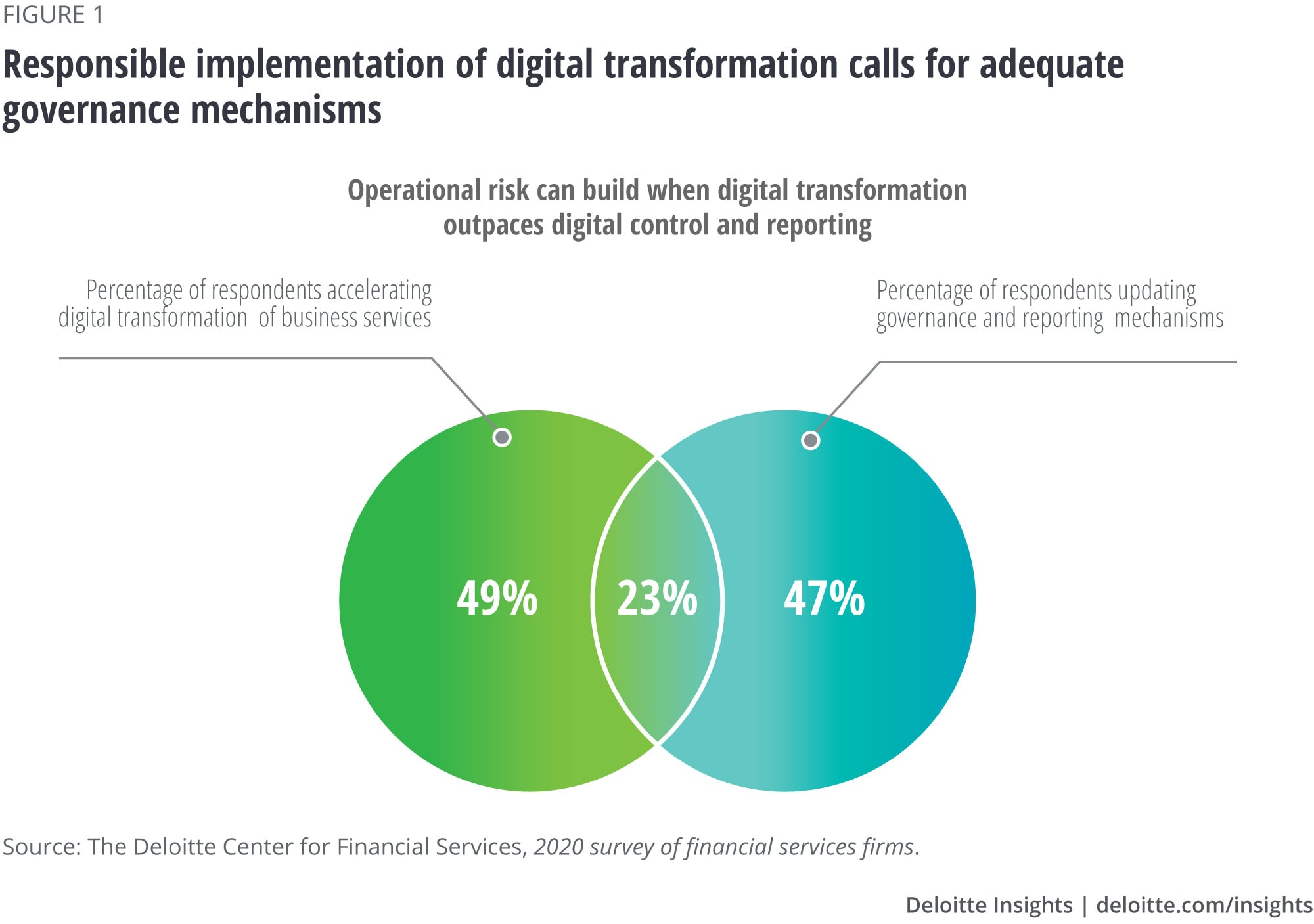

Employees and management can work together to create a digitally advanced, responsible operating environment. They will need to make systems and processes fit for a digital future without losing sight of their organization’s long-term vision and strategy.

They will also need to minimize operational risks, such as cybersecurity, fraud, reputation, and strategic risks. For example, implementing customer transparency and data modification measures may require new control systems to be set up to protect against identity theft and fraud. Importantly, managers and employees will likely need to upskill on new technologies to meet other stakeholders’ expectations and deliver high performance in a virtual environment. As Deloitte has written about previously, most “successful digital transformations realign the organization to a singular vision.”5Therefore, if changes are made to the operating model, management should ensure digital transformation aligns with these changes.

Having a unified cloud and cybersecurity approach can help digital projects succeed; comprehensive strategies tend to be more resilient than nascent ones.6 Digital risk monitoring is an ever-increasing priority, and some firms now have a board-level committee to manage and control digital risk. The committee can call for regular audits, changes to management reporting, and stress testing for events to incorporate and enhance resilience.7

Organizations that establish a strong reputation for responsible behavior may gain an edge in recruiting the most talented job candidates. This, in turn, may create a virtuous cycle, because people are the drivers of successful digital transformation.8

Regulators

Firms will likely have to digitally transform the compliance function to sustainably and responsibly meet evolving regulatory requirements; existing mechanisms may not be able to handle the incremental burden. Furthermore, by taking a more proactive and forward-looking approach to transformation, firms may avoid lapses in governance, which could mitigate some financial penalties, lawsuits, and reputational damages.

One way to build a more responsible compliance function is to embed the requirement into frontline business units. This action may allow the compliance team to perform initial assessments and track regulatory requirements; frontline units could then focus on delivering positive business outcomes within the implementation framework.9 This collaboration could reduce cost and help minimize damages due to noncompliance with early detection and faster mitigation of problems.10 However, according to the Deloitte global risk management survey, 58% of respondents faced significant challenges in getting buy-in from businesses and functions and only 33% of respondents said that control testing was embedded in the frontline functions of their organizations.11 Clearly, the industry has a long way to go to successfully integrate control mechanisms into the frontline units.

Moreover, firms that use entrepreneurial regulatory technology (RegTech) firms to digitally transform the compliance function may need to think holistically to avoid having a suboptimal mosaic of tactically applied solutions.12Siloed approaches to implementing RegTech solutions may lead to low interoperability and conflicting outcomes. For a RegTech example, United Overseas Bank (UOB) successfully increased true positive detection by 5% and reduced false positives by 50% in its anti-money laundering (AML) program.13 UOB teamed up with Tookitaki, a Singapore-based RegTech startup, to use machine learning as part of its AML program.14 To make this new AI-assisted approach work responsibly, UOB updated its staffing considerations for model supervision skills, data privacy factors, and processing system interoperability.15

In addition to updating old mechanisms, responsible digital transformation explores internal and external avenues to sustainably reinvent compliance and accountability.

Society

From a societal perspective, responsible digital transformation factors in financial inclusion, fairness, sustainability, and financial system stability during the digital transformation planning process. As a result, firms are more likely to be viewed as a positive force for good.

Responsible digital transformation aims to boost financial inclusion and fairness by mitigating bias among employees, data, and AI models.16 Being responsible is easier said than done. Requiring antibias training for employees, qualitatively and quantitatively managing data quality, and using explainable AI models may help prevent biases from forming and spreading across the financial system.17 Firms that remove bias and decouple financial decision-making from factors that have no impact on risk could raise their social reputation as well as improve environmental, social, and governance (ESG) ratings.

On the sustainability front, firms can take a number of actions, including: finance green enterprises, use clean energy sources, reduce and offset emissions, and adapt infrastructure to withstand more extreme weather.18 Wells Fargo achieved carbon neutrality in its operations in 2019 and has committed to achieving net zero in its financing activities by 2050.19

As firms develop their digital transformation plans, it is important to provide the public the reporting metrics needed to support full transparency.

Another aspect of social responsibility is advancing diversity, equity, and inclusion (DE&I) efforts within the firm. In this work, recognizing that people have different starting positions in today’s society is paramount. An equitable enterprise “listens to, invests in, and actively works to dismantle the systemic inequities” that have influenced the world as we know it today.20 Firms that incorporate this approach may be able to strategically break down the underpinnings on which the inequities are built, for the betterment of society.21

Last, but not least, firms can evaluate the impact of their advanced digital systems on financial system stability. As AI systems more frequently communicate with one another, firms may need to add new governance processes and safeguards to detect and prevent incidents.22 Black box AI-decision logic can be revealed and monitored to mitigate risk consequences across interconnected institutions. Systemwide risks may arise due to:

• Herding behavior: Market movements fueled by momentum can escalate when different systems construe market signals in a similar way

• Algorithmic competition: Multiple AI systems bidding against each other may artificially inflate the price of an asset after one drops out, which may create an incentive to engage in riskier behavior or perhaps never even enter the market in the first place

• Information vacuums: AI systems may misinterpret human inaction following a shock to the market as disinterest and continue selling as prices fall, exacerbating the effects of the shock due to the absence of human demand.23

Apart from regulatory requirements, firms can use techniques such as scenario modeling, human-in-the-loop, and sentiment analysis to identify and mitigate systemwide risks.24

Financial institutions that achieve responsible digital transformation can “positively affect society without negatively affecting profits.”25 This is likely to boost a firm’s brand value at a societal level.

Shareholders

Shareholders tend to care about far more than just profit and loss statements. Most positively view firms that incorporate high ethical standards and societal impact into their operations. Shareholders expect responsible firms to be adequately transparent and disclose identified material risks. Taking these steps can help firms achieve a higher bottom line, which is increasingly important in shareholders’ eyes.26

In addition to considering financial returns, most shareholders now expect firms to consider operational risks from an ethical and resilience perspective.27 For example, if digitization means offshoring, the cost savings may not be worth it if offshoring ties firms to corruption, human rights violations, or use of unfair labor practices in other countries.28

The US Securities and Exchange Commission, acting as an advocate for shareholders, is stepping in with recommendations for ESG reporting frameworks. As more and more shareholders measure their investments more broadly than financial results alone, the additional measures firms take are becoming more regulated and are affirmed by accountable third-party auditors or rating agencies. Overall, firms’ success, in the eyes of shareholders, now depends on verified measures that demonstrate a net positive corporate impact.

Looking forward

The scope and goals of responsible digital transformation extend beyond a typical upgrade to reporting and governance. Given all of these factors, to achieve this level of transformation, financial services firms may have even more catching up to do than our survey data indicated. Still, there is enormous opportunity for firms that are able to get this right.

Financial services firms made significant advances in their digital transformation journeys during the height of the COVID-19 pandemic. They can now take those advances to the next level and create new benefits by taking steps to ensure their transformation efforts are not just need-based, but also responsible. Then, they can succeed in achieving a higher bottom line.

{kind=link}