Science should be coming to the rescue, but innovations in neuroscience essentially stalled in the latter half of the last century. In the early 20th century, a combination of hard work and luck produced three broad types of psychiatric drugs: antidepressants, antipsychotics and anxiolytics. But psychopharmacology developments petered out, and few new drugs reached the market during the last four decades. Further, the treatments on offer today often only delay the progression of the disease without recovering lost brain function.

However, with advancements in brain disorders lagging behind treatments in other fields, such as cancer or treatments for the heart, new energy and ideas are flowing into neuroscience. There is now hope that new treatments will arise to overcome the limitations of existing therapies and relieve the millions of patients suffering worldwide. To help new capital form investment decisions, Deloitte has studied the global neuroscience market (GNM) across segments and regions. Our report provides a comprehensive analysis of available diagnostic and treatment options (as a proxy for the neuroscience market size) to estimate the revenue-based valuation of the GNM until 2026.

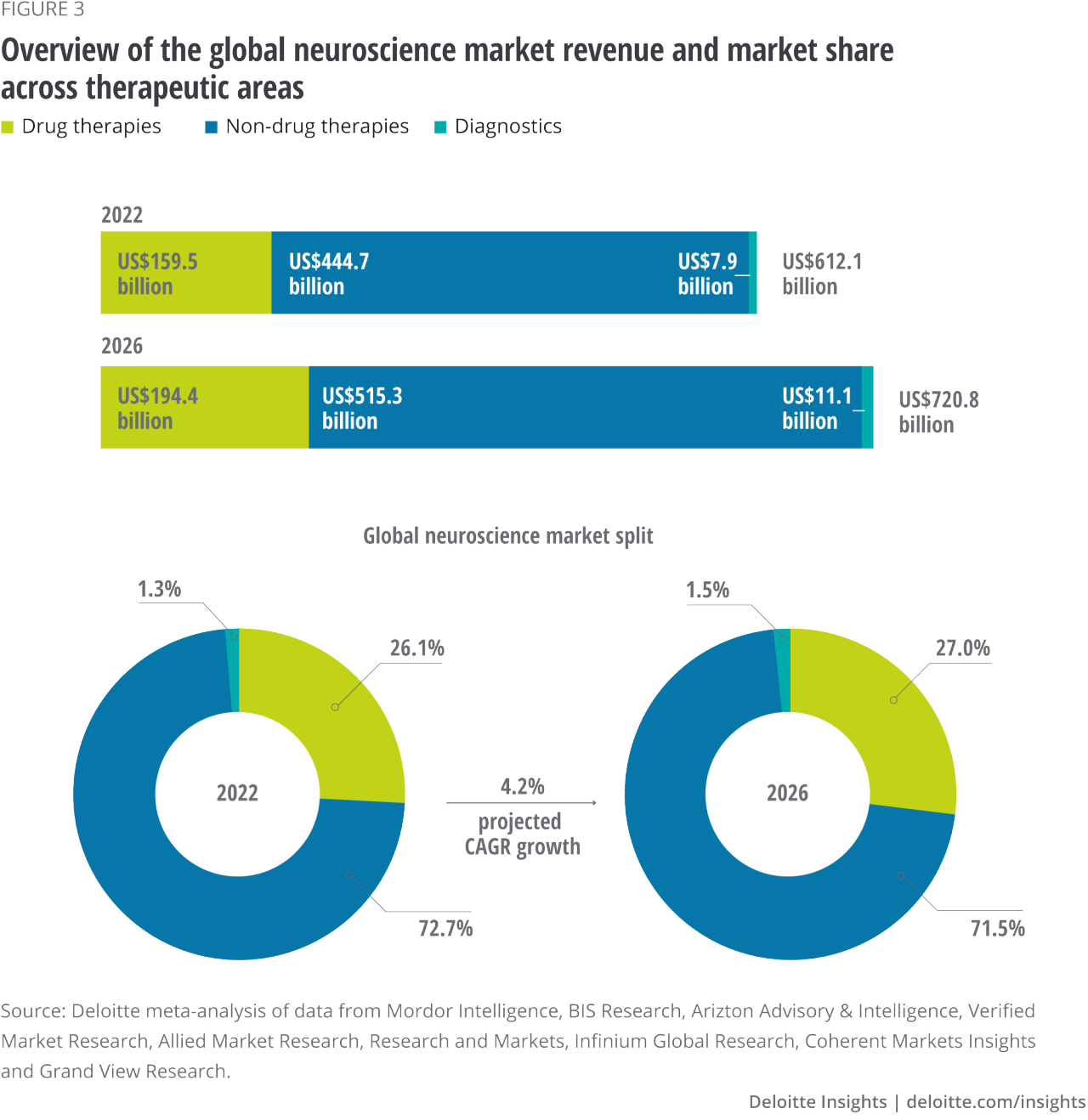

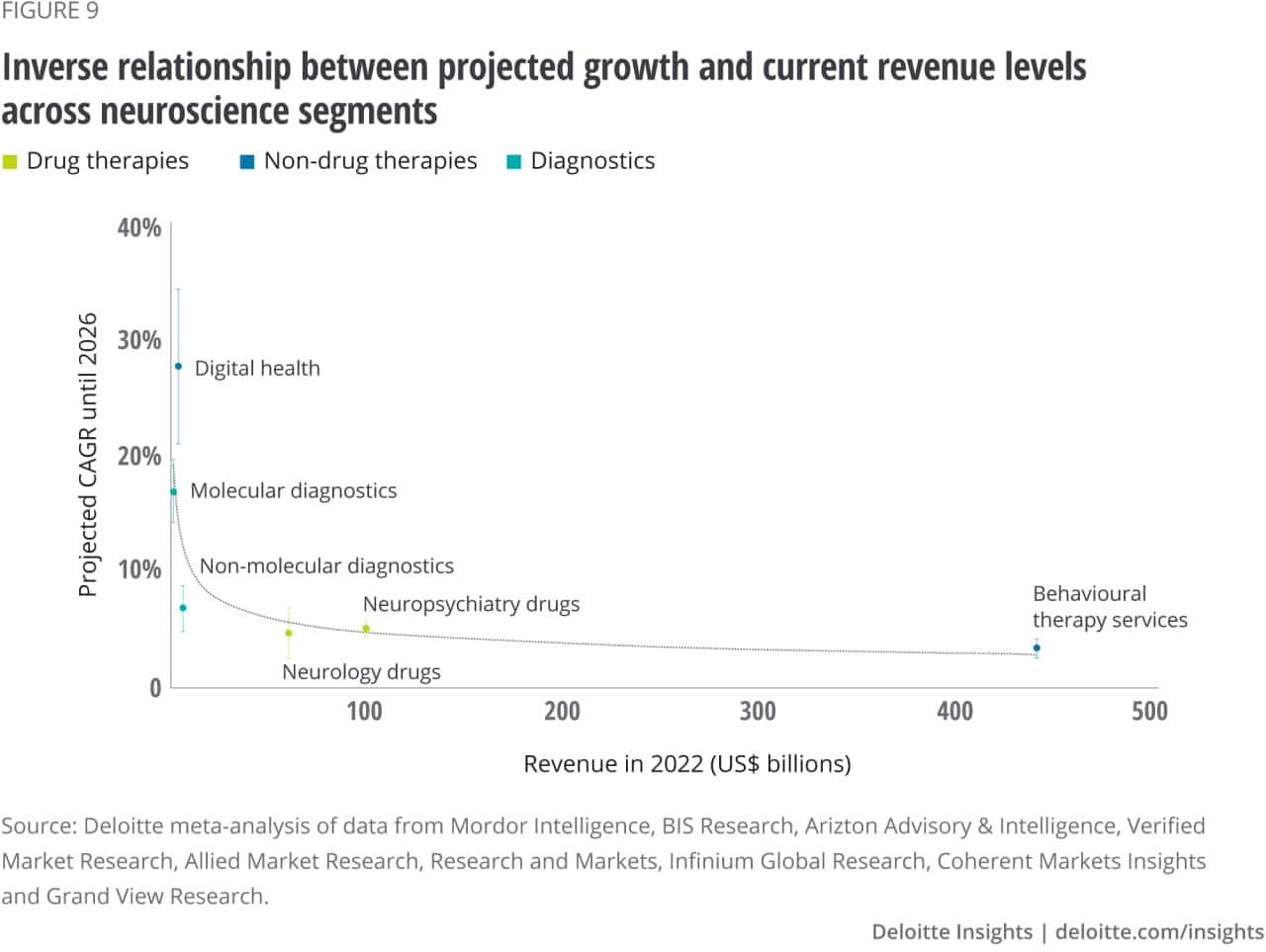

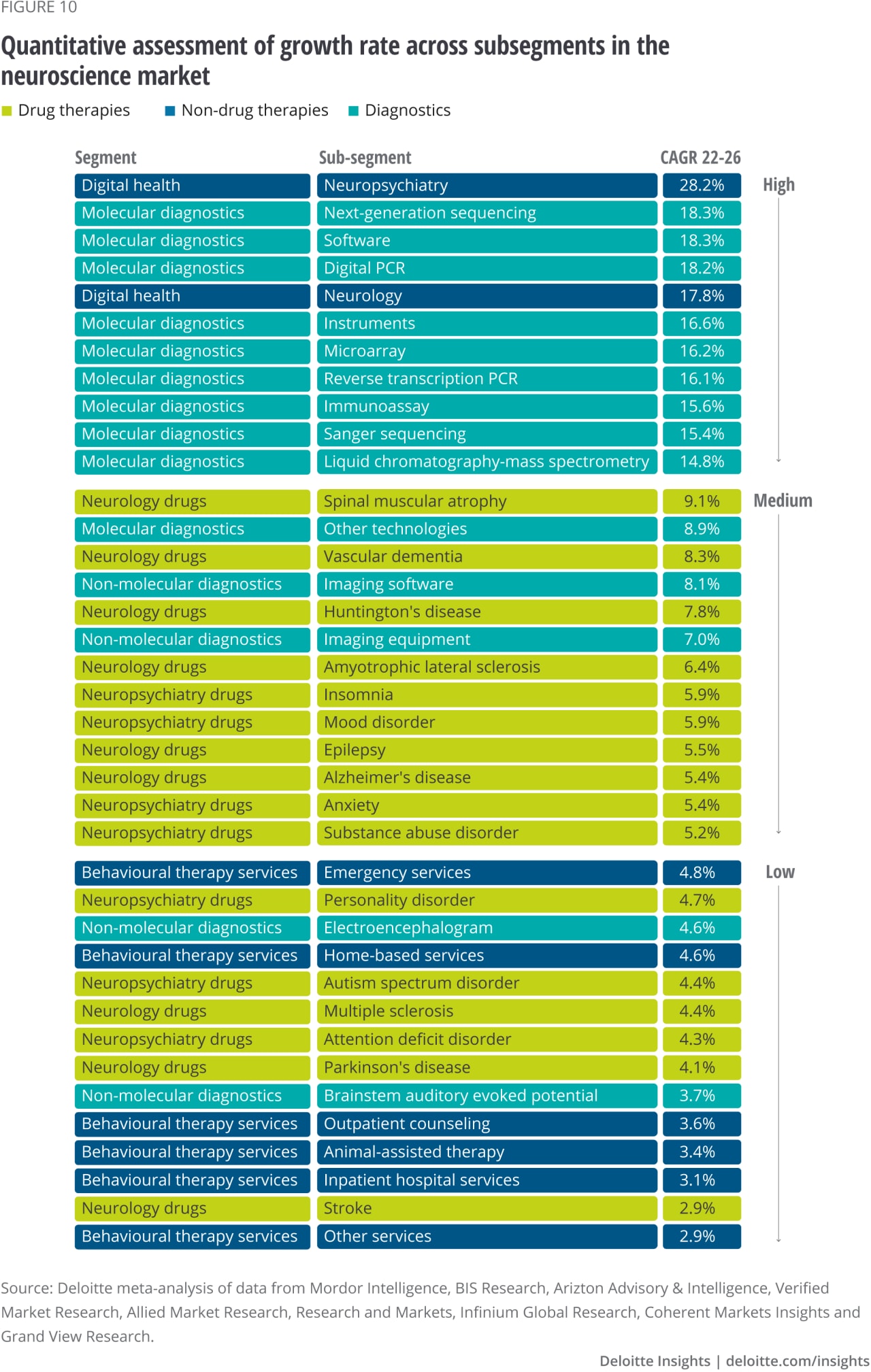

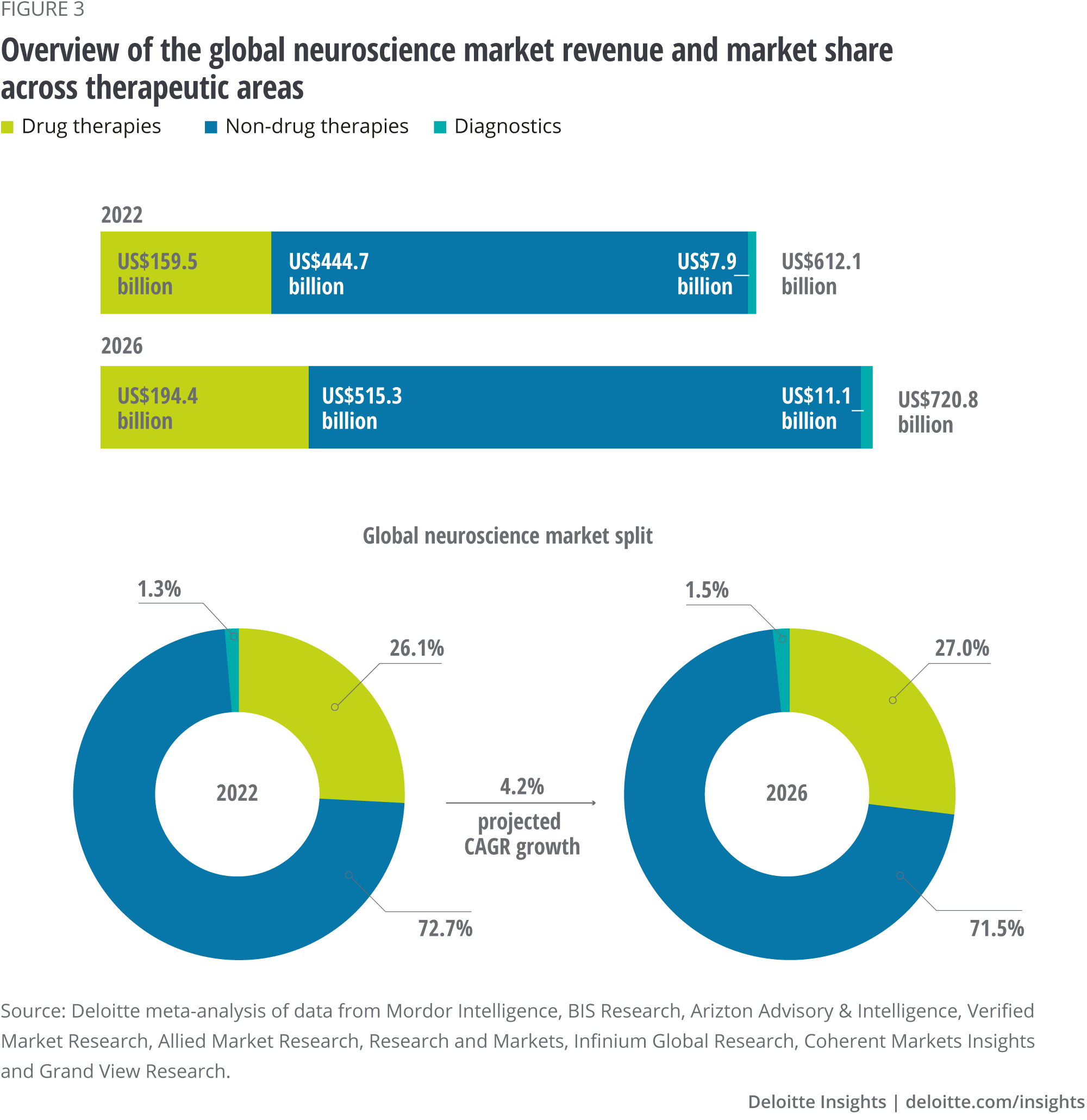

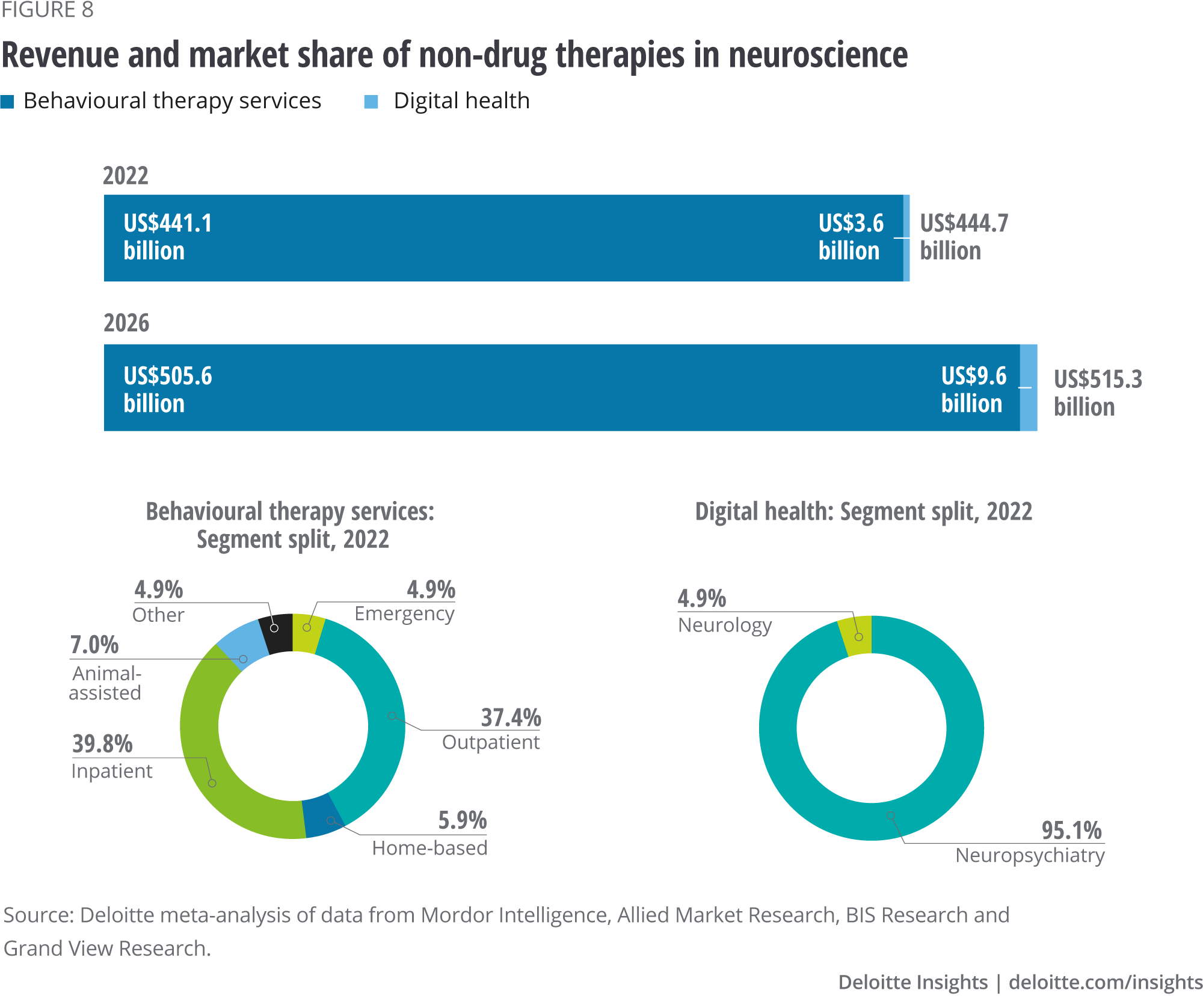

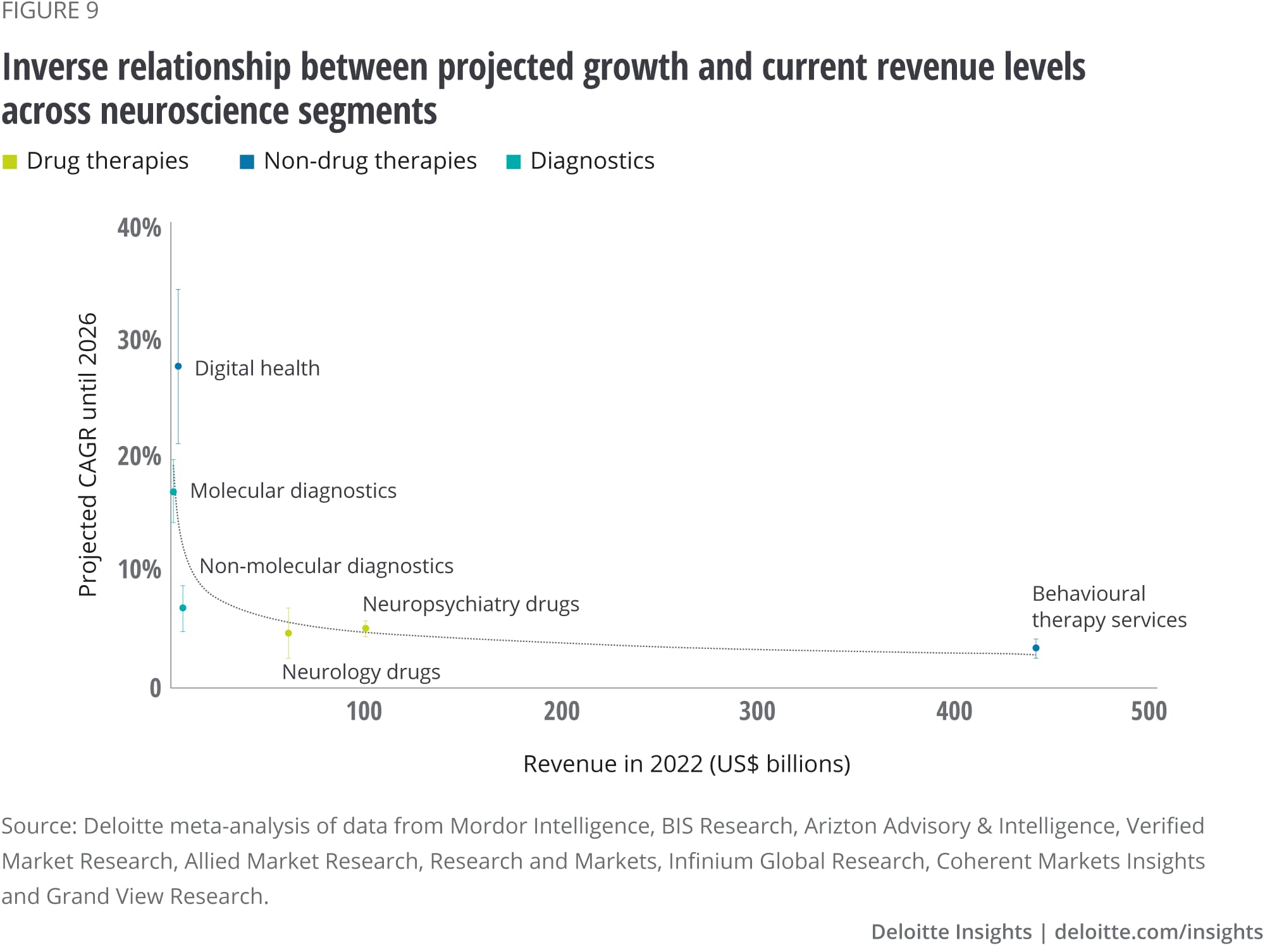

The analysis indicates the GNM was worth $612 billion in 2022 and could grow to $721 billion by 2026, returning an aggregate compound annual growth rate of 4.2 percent across segments (ranging from 3.5 percent for behavioural therapy services to 27.8 percent for digital health).

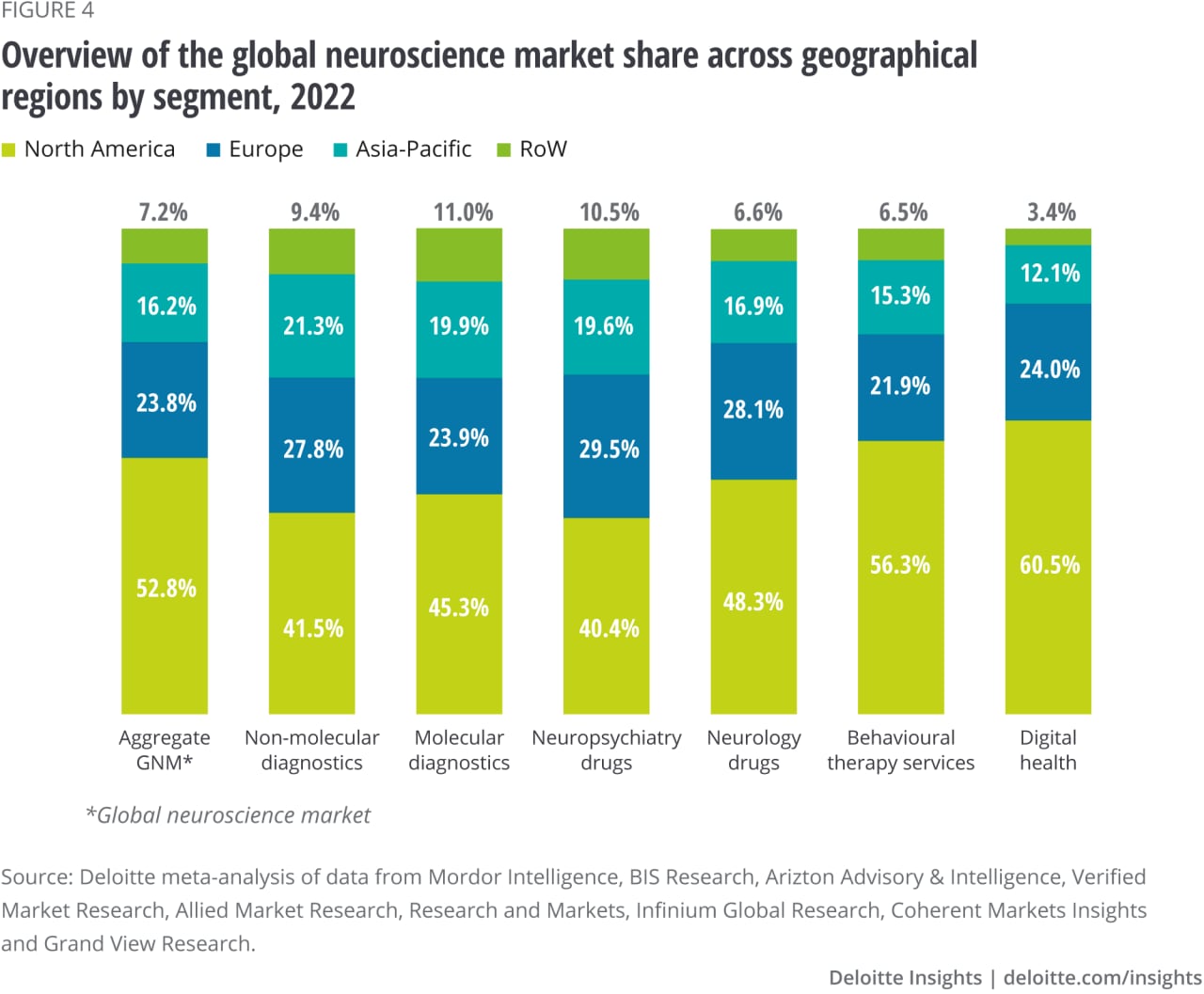

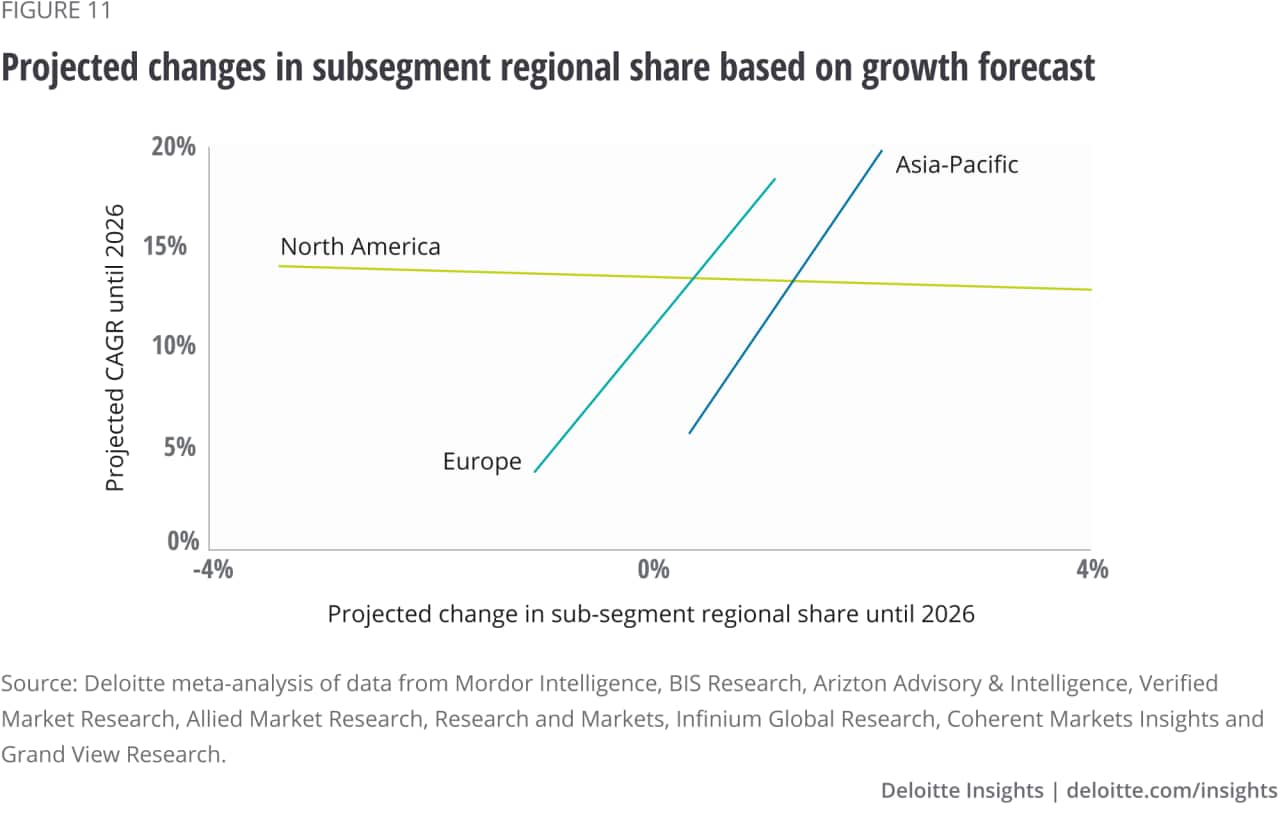

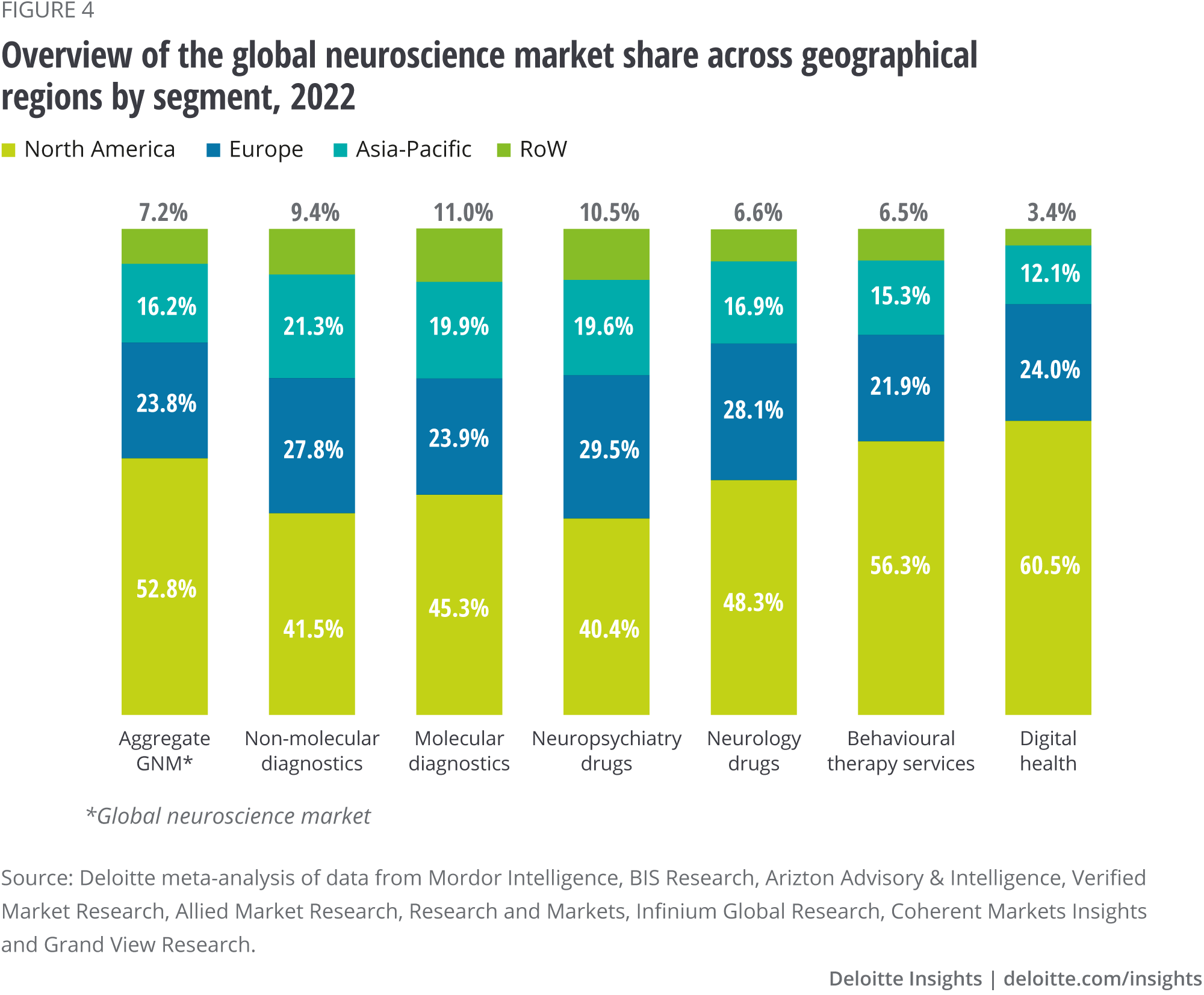

We also conducted segment-specific correlation analysis that identifies an inverse relationship between current revenue levels and future growth rates. This could reflect that smaller value segments have the potential to gain more ground as nascent technologies emerge, sparking investor interest and confidence in novel therapeutic approaches. Further, different segments will drive GNM growth depending on the region.

In summary, we have developed a holistic framework to help guide investment decisions across neuroscience segments. The intention is to identify where patient demand will drive growth and where investments will most readily lead to effective market solutions.

Brain disorders and their impact on patients and society

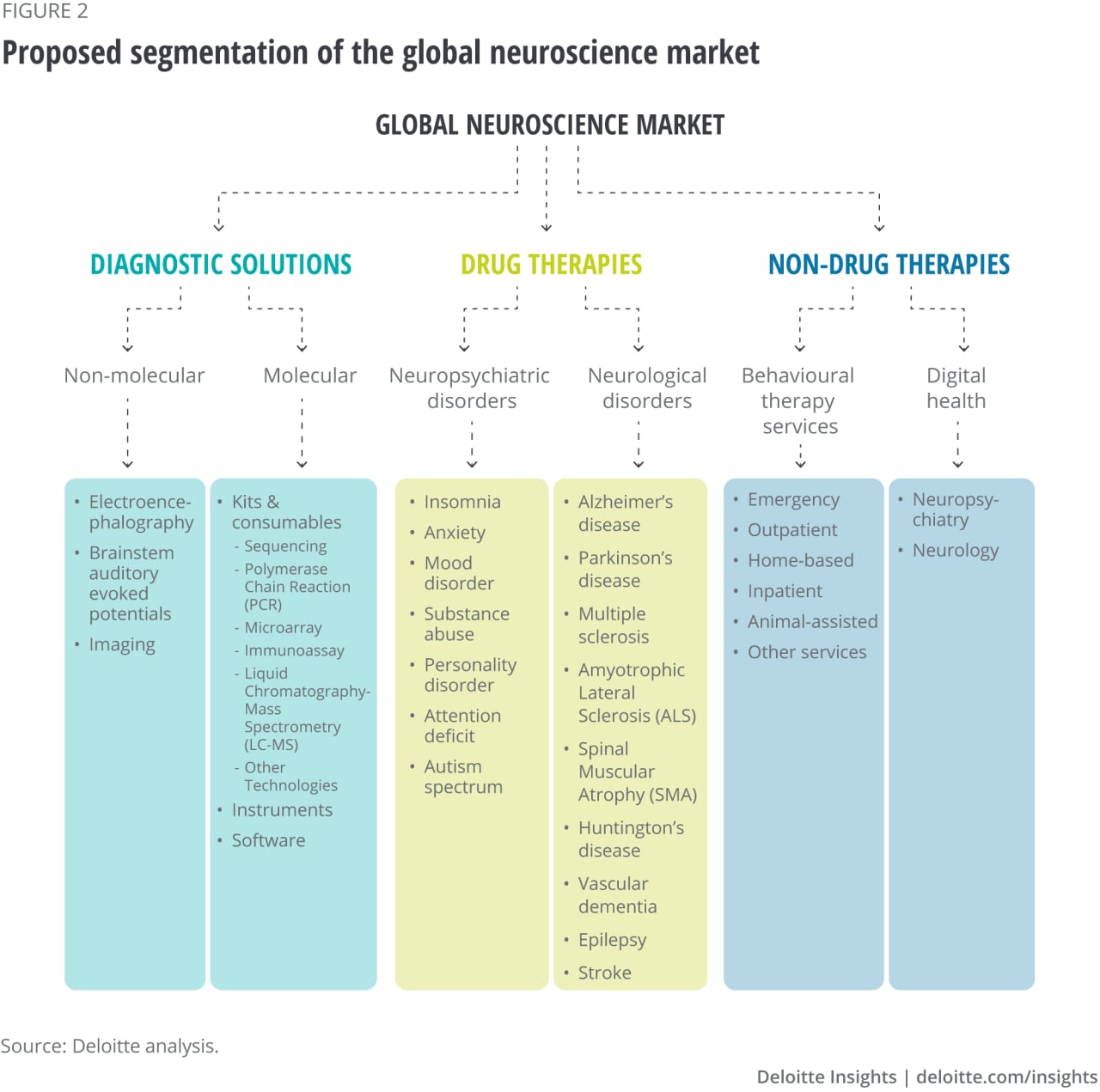

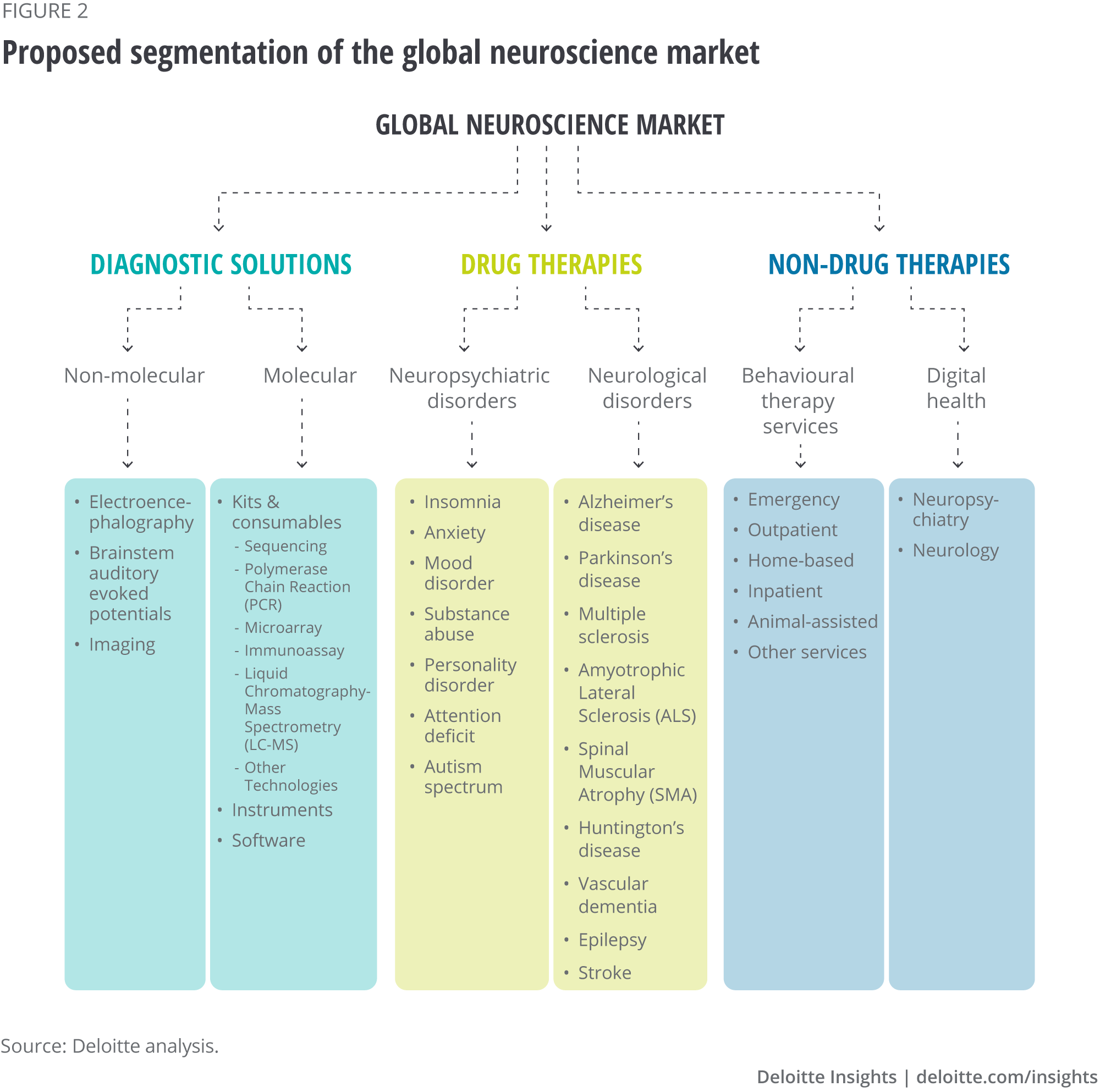

Our central nervous system (CNS) is a sophisticated biological conglomerate formed of billions of neurons and glial cells distributed throughout the brain and spinal cord. Any dysfunction of the molecular, cellular or circuit underpinnings of the CNS triggers (referred to here, for simplicity) brain disorders. There are two main types of brain disorders:

- Neurological conditions—those triggering cognitive and motor dysfunction from damaged neurons and nerves (for example, Alzheimer’s disease, Parkinson’s disease and multiple sclerosis).

- Neuropsychiatric conditions—those characterised by disturbed behavioural and emotional states (for example, anxiety, depression, addiction). The concepts of mental health and mental illness are often applied to neuropsychiatric conditions, although mental illness may also appear as a comorbidity in neurological disorders.

The societal burden of brain disorders

Brain disorders are a significant global health problem and the second largest source of deaths worldwide. Neurological and neuropsychiatric disorders are responsible for 9 million and 8 million annual deaths, respectively. This is over 30 percent of deaths,3 which means every third person on this planet is likely to lose a family member to brain disorder.

Globally, this imposes a high cost on societies. The Global Burden of Disease Study calculates disability-adjusted life-years (DALYs) by summing years lost and years lived with disability for the global population with brain disorders. The annual DALY count is 276 million years for neurological disorders and 184 million years for neuropsychiatric conditions, adding up to 460 million years. Collectively, this represents the leading cause of disability worldwide.4

These DALY and fatality metrics indicate that current treatments for brain disorders leave much room for improvement. They also highlight the desperate need for more resources to be devoted to brain disorders to elevate the standards of care.

Roadblocks to the development of effective brain therapies

The limitations of current treatments arise from three factors. First, we have a limited understanding of the biological basis of brain disorders. These disorders affect an organ characterised by ‘emergent properties.’ These are properties that cannot be explained by the addition of functionalities shown by individual building blocks (for example, higher cognitive functions or consciousness). This adds a layer of complexity that is not present in other therapeutic areas and ultimately hinders the development of effective therapies.

Second, traditional pharmacological treatments are not enough to address brain disorders. If we conceive of the brain as an experience-dependent organ shaped by behaviour, we ultimately need to emphasise interventions beyond pills.

Lastly, the limited availability of early diagnostic tools generates a situation where clinically observable symptoms often only appear once the molecular signatures of the disease are at an advanced stage. This diminishes the efficacy of available treatments in reverting the course of the disease (that is, repairing the brain).

About this report

The negative impact of brain disorders is expected to worsen over the coming years as the COVID-19 pandemic served as an unprecedented global stress test. During the years of lockdowns, people were deprived of social interaction to an extent never before seen in recorded history.

Psychological and neuroscience research has few observations about mass isolation. Still, large-scale studies on social deprivation amongst the elderly show cognitive capacity, mental and physical well-being, and longevity can all be negatively affected.5 As social isolation escalates the risk of depression and dementia,6 the lockdowns are expected to spike the rate of brain disorders.

Reversing this must be a priority, particularly as social isolation increases loneliness among vulnerable people, including those who are disabled, poor or from culturally and linguistically diverse backgrounds. Furthermore, because we are increasingly a ‘Brain Economy’ where most new jobs demand cognitive, emotional and social skills, we need to ensure people are mentally healthy, so our societies continue to be productive. Neuroscience investments are fundamental to achieving such long-term economic resilience.

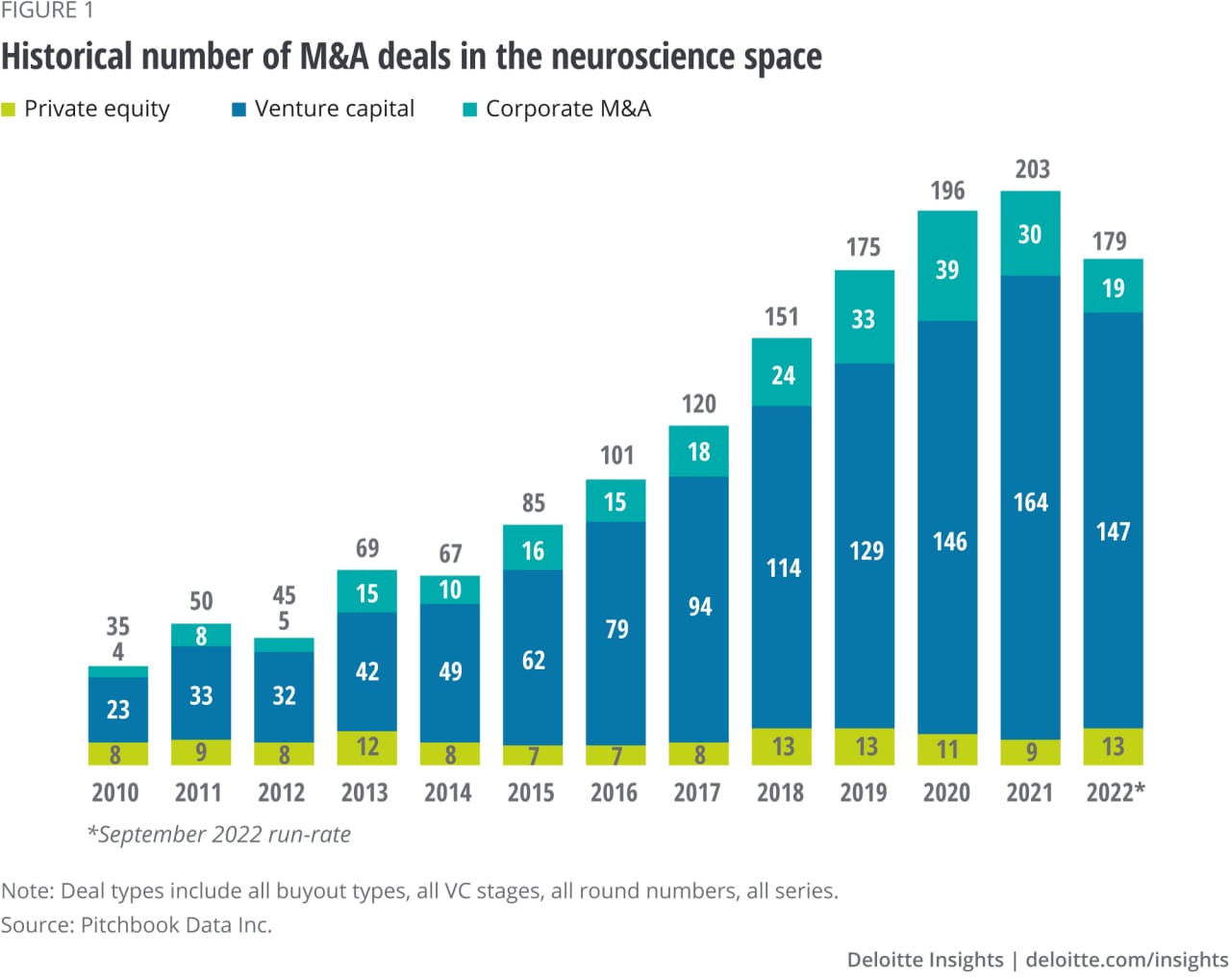

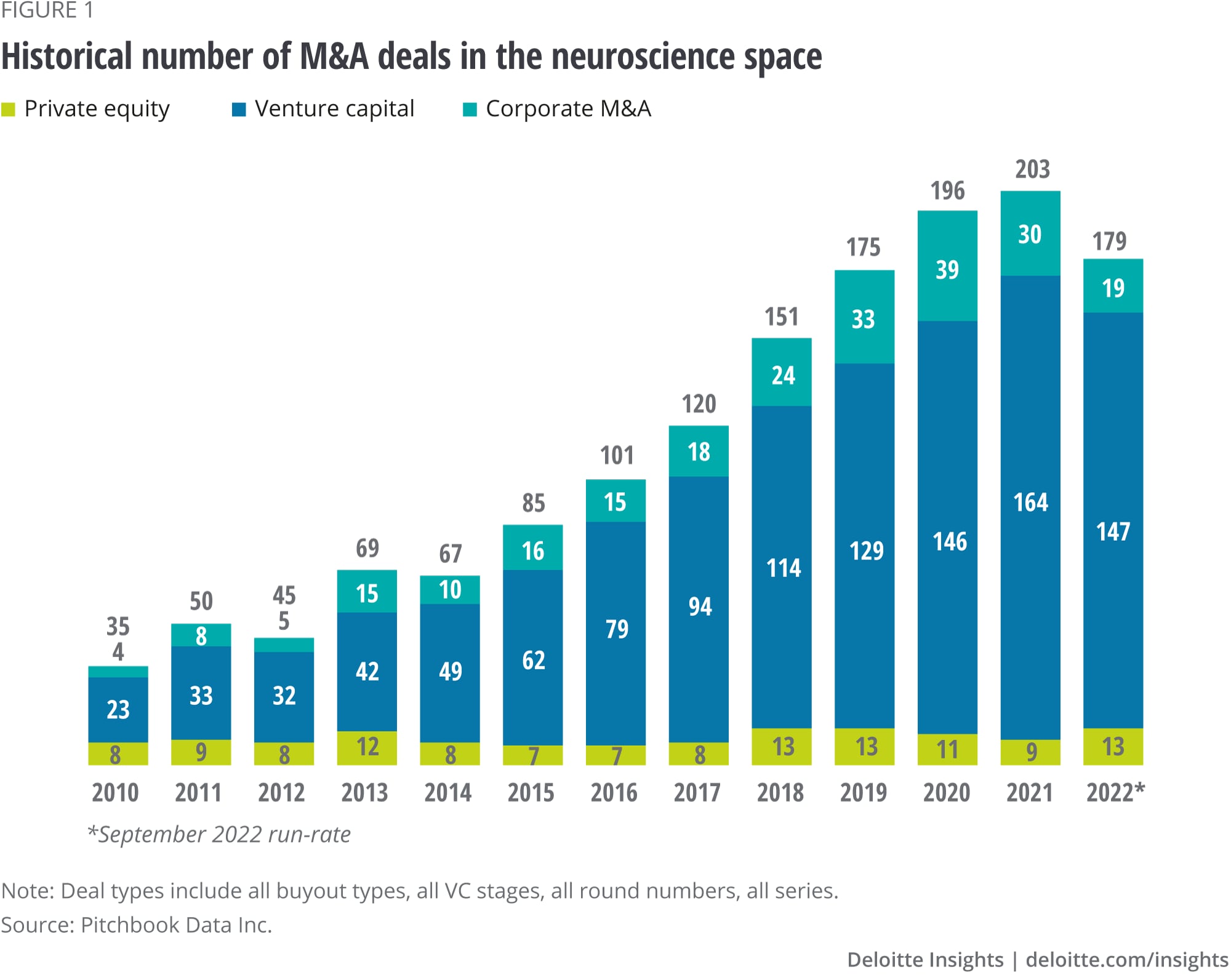

Over the last decade, investment bodies such as private equity, venture capital and corporate M&A divisions have been increasing the amount of capital dedicated to M&A deals in neuroscience (figure 1). However, further and more sizable investments are required if the Life Sciences Industry is to meet the needs of patients suffering from brain disorders worldwide.

This Deloitte report supports the decisions of investment bodies with the means to provide funds to companies focused on the development and commercialisation of solutions for brain disorders. By revealing the global neuroscience market's collective revenue potential in all significant segments and regions, we aim to facilitate capital access in the neuroscience space. New investments will enable the development of new therapies, alleviating the suffering of many and supporting a mentally healthy workforce and a fully functional economy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}