2025 life sciences outlook

Despite industry uncertainties, life sciences execs expect their organizations to adapt, grow, and generate value

Pete Lyons

Todd Konersmann

Leena Gupta

Darshan Gosalia

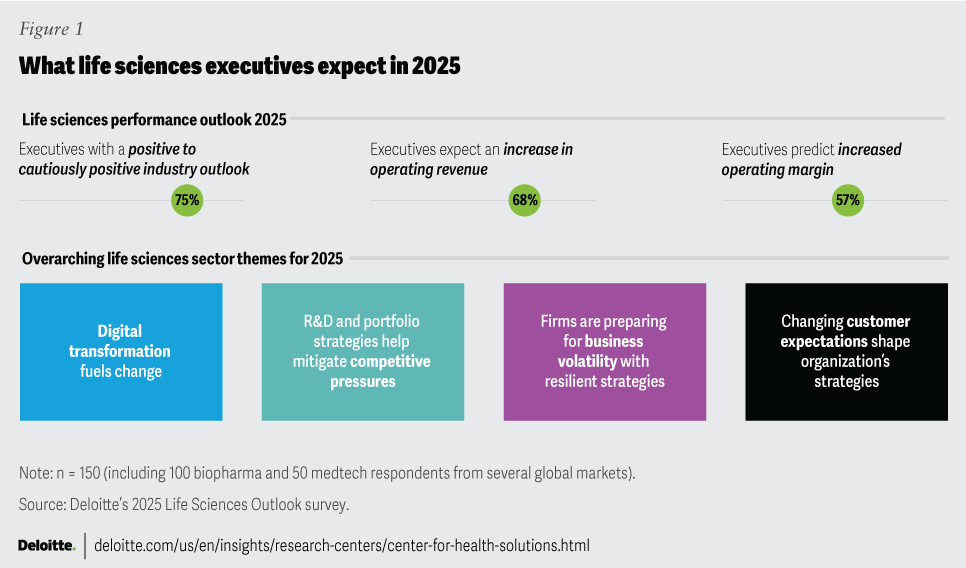

While several potentially disruptive forces could reshape the life sciences industry in 2025, the vast majority (75%) of global life sciences executives are optimistic about the year ahead, according to a recent survey from the Deloitte US Center for Health Solutions. This optimism is fueled by strong growth expectations, with 68% of respondents anticipating revenue increases and 57% predicting margin expansions in 2025. Additionally, ongoing advancements in science and technology could lead to more breakthrough innovations.

The Deloitte US Center for Health Solutions surveyed 150 C-suite executives from pharmaceutical, biotechnology, biosimilar, and medical device manufacturing companies across the United States, Europe (France, Germany, Switzerland, and the United Kingdom), and Asia (China and Japan) in August and September 2024 to learn about the industry’s concerns and priorities. Insights from interviews with three company executives further contextualize the cautious optimism that was revealed in the survey results. It should be noted that while the findings offer a comprehensive view of several global markets, they do not encompass a worldwide perspective. Additionally, this report highlights only the trends and actions that survey respondents rated as being “significant” or “very important.” In doing so, we aim to highlight the industry’s top priorities along with relevant and useful insights.

Life sciences executives are focused on adapting, creating value, enhancing digital capabilities, and growing amid competitive pressure, business volatility, and changing customer needs. The executives we interviewed underscored the importance of proactive planning and strategic implementation. Evan Lippman, chief corporate development and strategy officer at Alnylam Pharmaceuticals,1 stated, “I’m exceptionally optimistic about the future. You need a strategy to take advantage of what the future will look like. That’s what will differentiate companies in the coming years.” Lippman also said that he is optimistic that innovation and leadership will be rewarded in the future.

Digital transformation is likely to drive more change in 2025

Digital transformation remains a key focus in the life sciences industry, driven by advancements in cloud computing, generative AI, and other digital technologies. These innovations provide companies with new opportunities to enhance their products, services, operations, and strategic decision-making, according to survey respondents.

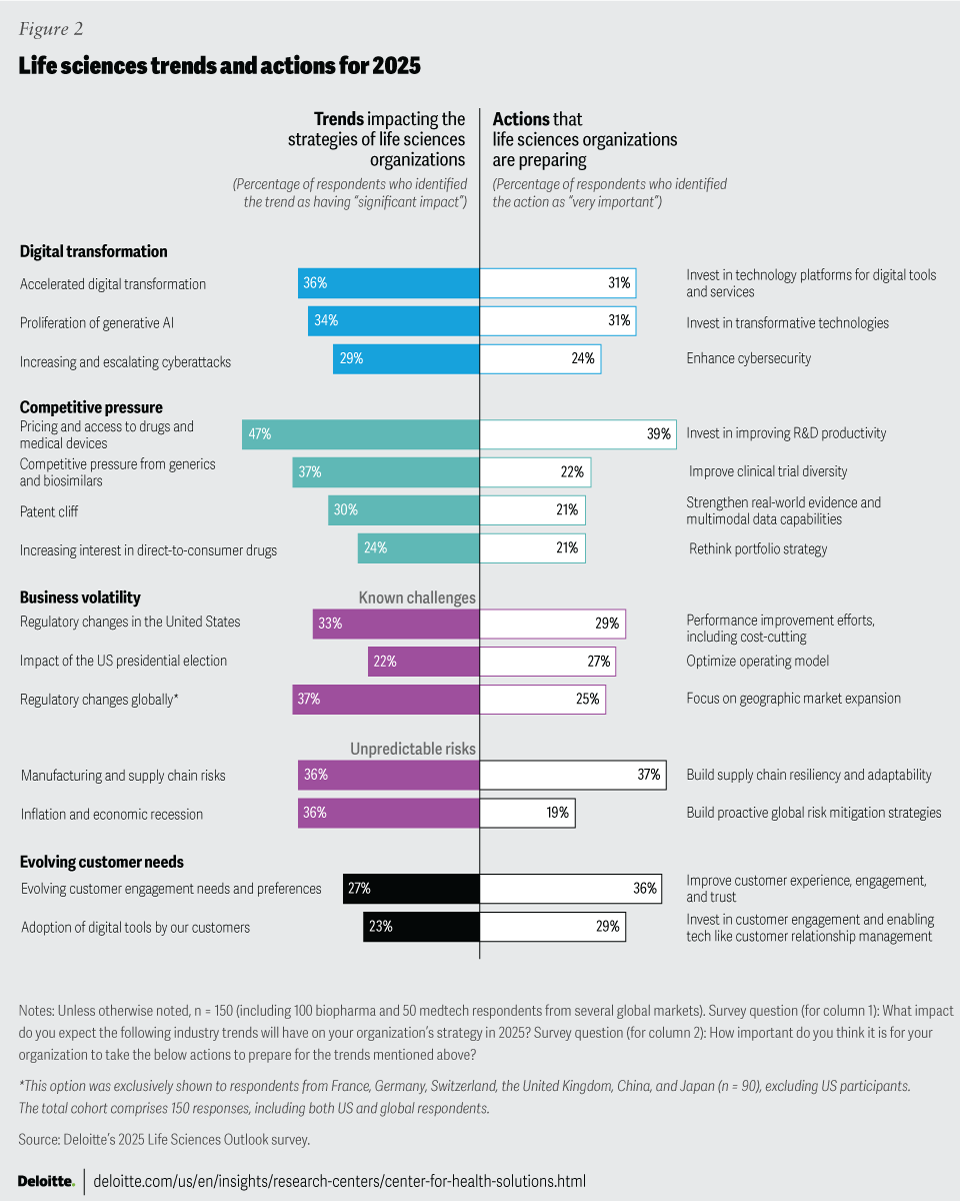

Digital transformation is expected to have a major impact on organizational strategies in 2025. About 60% of executives cited gen AI or digital transformation as key emerging trends they are closely monitoring. Moreover, nearly 60% of executives plan to increase gen AI investments across the value chain, suggesting that companies are moving beyond initial pilot projects and are beginning to realize substantial value from adopting these technologies at scale.

Artificial intelligence investments by biopharma companies over the next five years could generate up to 11% in value relative to revenue across functional areas, according to Deloitte analysis. For some medtech companies, AI implementation could lead to cost savings of up to 12% of total revenue within the next two to three years.2 Gen AI, in particular, is seen as having more transformative potential than previous digital innovations.3 It could reduce costs in research and development, streamline back-office operations, enhance self-service capabilities for customers across digital channels, and boost individual productivity by embedding gen AI into existing workflows.

To fully realize this potential, life sciences leaders should prioritize strategic issues that can most benefit from gen AI. They should clearly define and communicate these issues to stakeholders and technical experts and ensure the necessary infrastructure is in place to deploy gen AI models effectively at scale.4

In the future, this may evolve further. As Akiko Amakawa, corporate strategy officer and CEO chief of staff at Takeda, shared in an interview, “Currently, digital investments are driven by specific initiatives, but we will need to develop a prioritization framework to manage these investments as a portfolio just like we have been managing our R&D pipeline. The challenge lies in developing consistent metrics, as digital projects span diverse goals including risk management, operational efficiency, and customer satisfaction that don’t easily compare under one measure like ROI. Creating a meaningful prioritization framework for these investments is still evolving.”

R&D and portfolio strategies could help mitigate competitive pressures

C-suite executives identified pricing and access to drugs and medical devices as the most significant issue facing the life sciences industry. Nearly half of those surveyed (47%) expect pricing and access to significantly affect their strategies in 2025 and another 49% expect a moderate impact. This trend mirrors last year’s survey results.

Additionally, 37% of respondents view competition from generic drugs and biosimilars as a top trend, while 30% cite the patent cliff as a significant concern. Our analysis of EvaluatePharma5 data indicates that the biopharma industry is facing a substantial loss of exclusivity, with more than US$300 billion in sales at risk through 2030 due to expiring patents on high-revenue products. This looming patent expiration is likely to drive interest in mergers and acquisitions, with 77% of surveyed executives expecting M&A to increase in 2025.

Innovation is how life sciences companies respond to such market dynamics. But innovation takes time and can create competition when companies pursue similar strategies. Some biopharma companies are pursuing profitable disease areas and indications, such as oncology and immunology, to close pipeline and revenue gaps. However, many assets target the same biological pathways or employ similar mechanisms of action.6 This overlap creates competition, which can drive down prices and negatively impact market share and margins, even before generics or biosimilars enter the market.

Meanwhile, the market success of GLP-1 receptor agonists is revitalizing interest in general medicines, or small-molecule drugs that treat common conditions. Over the past two decades, many biopharma companies have scaled back their general medicine product portfolios in response to competitive pressures and financial incentives that favor the development of treatments for specialty and rare diseases.7 However, several organizations are racing to capture a share of the US$200 billion GLP-1 market now that these drugs have shown to be effective in treating obesity, which affects 1 in 8 people in the world.8 These drugs are being evaluated for a wide range of common conditions including sleep apnea, addiction, Alzheimer’s disease, nonalcoholic fatty liver disease, and steatohepatitis.9 GLP-1s could also impact the broader life sciences and health care industry by reducing the demand for medical devices and surgical procedures related to diabetes and obesity.10

Our survey data indicates R&D is likely to be a major focus in 2025, although there is no universal approach. Companies are exploring a variety of initiatives to enhance their market positions, including:

Rethinking R&D strategies

Declining R&D productivity is a significant industry concern. Half of the surveyed medtech executives and 56% of the biopharma executives (data not shown in the figures) said their organizations need to rethink their R&D and product development strategies over the next 12 months. Nearly 40% of all survey respondents emphasized the importance of improving R&D productivity to counter declining returns across the industry. A recent Deloitte Center for Health Solutions report on measuring the return from innovation illustrates how some pharmaceutical organizations are integrating gen AI and other advanced technologies into their R&D strategies.

The traditional R&D process is often slow and stage-gated, typically requiring large trials to establish meaningful impact. Additionally, failure rates for new drug candidates can be as high as 90%.11 In response, some biopharma companies are leveraging AI and digital twins. Digital twins, which serve as virtual replicas of patients, allow for early testing of new drug candidates. These simulations can help determine the potential effectiveness of therapies and speed up clinical development.12 Sanofi, for example, uses digital twins to test novel drug candidates during the early phases of drug development. The company also employs AI programs with improved predictive modeling to shorten R&D time from weeks to hours.

About 20% of survey respondents are evaluating their portfolio strategies to balance innovation capabilities with market needs. In 2024, a number of companies scaled back on their product pipelines to focus on high-potential candidates.13 Given the high cost of clinical development, such cuts can have an immediate impact on expenses.14 The challenge often lies in deciding which programs to eliminate. Strong clinical data can point to the most promising candidates based on unmet market needs. Companies might also assess how well programs align with their overall goals and capabilities.15

In our survey, 32% of biopharma respondents plan to prioritize innovations like cell and gene therapies using CAR-T cells and CRISPR technology over so-called me-too drugs. Additionally, 30% of medtech respondents said they would consider new modalities and platforms, while 24% chose the development of Class III devices as a priority over Class II or I devices.

Ensuring acquisitions align with corporate strategies

Over the years, M&A activities have been a reliable source of innovation for some large life sciences companies. Our previous report highlighted that the biopharmaceutical industry often uses acquisitions to address portfolio gaps, partly driven by the patent cliff. However, success in these endeavors often depends on the ability to align therapeutic expertise with commercial capabilities. For instance, Pfizer’s acquisition of Biohaven Pharmaceuticals helped the company expand its neurology portfolio in a growing market.16 Similarly, Medtronic’s acquisition of Mazor Robotics allowed the integration of the company’s advanced robotic systems into its surgical offerings, thereby improving precision and patient outcomes in minimally invasive surgeries.17 However, not all acquisitions meet expectations. Factors such as clinical trial uncertainties, integration challenges, and strategic misalignment can limit intended benefits.

Strengthening real-world and multimodal data capabilities

Over half (56%) of our survey respondents say their companies are prioritizing real-world evidence and multimodal capabilities, which combine clinical, genomic, and patient-reported data. However, of these, only 21% view it as a “very important” priority. This suggests that while interest in real-world evidence is growing, a number of life sciences companies may still lack the necessary capabilities for multimodal data strategy. These capabilities include a robust analytics infrastructure and data science expertise to gather, standardize, and make data from multiple sources accessible to business users.

Life sciences firms brace for business volatility in 2025

While most industry executives are optimistic about 2025, some are preparing for unexpected challenges and business volatility. About one-third of survey respondents expressed concern about potential changes to US regulations in 2025, while 37% are apprehensive about global regulatory changes and geopolitical uncertainties. These percentages are slightly higher than in past years, while concerns related to inflation and economic uncertainty have declined.

Although the Inflation Reduction Act is top of mind for the pharmaceutical sector in the United States (see “Implications of the new US leadership”), the regulation of software as a medical device and the overturn of the Chevron doctrine could have industry-wide implications. Under the Chevron doctrine, courts deferred to federal agencies like the Food and Drug Administration or Centers for Medicare & Medicaid Services to reasonably interpret ambiguous laws. Going forward, it is unclear whether courts will continue to defer to agencies for statutory, scientific, and technical interpretations of the law, and informal rulemaking.18

In Europe, several regulatory changes are underway.19 Of immediate concern to both sectors at the time of survey fielding was clinical trial regulation. Although the implementation timeline for new and ongoing clinical trials concludes in January 2025, the law contains several requirements that the industry has yet to master. These requirements include plain language summaries of scientific publications and data anonymization and redaction.20

Thirty-six percent of surveyed executives are also evaluating the potential impact of unpredictable challenges such as inflation, economic recession, and disruption in supply chain and manufacturing. With scenario-planning, companies can work to address known challenges and mitigate unpredictable risks, focusing on resilience, agility, and strategic foresight. Key approaches include:

- Fortifying supply chains: Microchip shortages, geopolitical conflicts, and severe weather can have a negative impact on supply chains.21 As such, 37% of life sciences executives identified building resilient and adaptable supply chains as a top organizational priority for 2025. A 2024 study from the Deloitte US Center for Health Solutions highlights how supply chain digitalization can help support these efforts. Supply chain issues tend to affect medtech and biopharma differently.

Medtech supply chains can be particularly fragmented, often spanning multiple countries and requiring diverse, specialized components from various suppliers. This complexity can make them especially vulnerable to disruptions and underscores the need for resilience. Regulatory changes such as the European Union medical device regulation and in-vitro diagnostic regulation, combined with inflation and shared demand for materials, add further layers of complexity. As a result, 48% of surveyed medtech executives said manufacturing and supply chain risks could significantly impact their 2025 strategy. In contrast, only 30% of biopharma executives shared this concern.

- Optimizing operating models and reducing costs: In response to the growing costs of developing new drugs and devices, the life sciences industry faces significant pressure to enhance productivity.22 Nearly 60% of surveyed executives identified optimizing the operating model as a priority for 2025, with 27% categorizing it as “very important.” Additionally, nearly 30% of executives planned to focus on performance improvement initiatives, such as cost cutting, to help boost efficiencies and increase returns. In 2024, cost-cutting measures included restructuring, offshoring, outsourcing, and even layoffs.23 Looking ahead to 2025, some companies are turning to gen AI and other emerging technologies to help streamline operations and reallocate resources more effectively.

- Strengthening cybersecurity: Cyberattacks pose significant risks to the life sciences industry, with the potential to disrupt supply chains, compromise manufacturing processes, erase years of research, and cause substantial financial damage. Companies that fail to adequately protect against cyberattacks also face potential fines.24 In response to these threats, 24% of surveyed executives rated investments in cybersecurity as “very important,” while 43% rated them as “important.” Cybersecurity is at the heart of the business, playing a critical role not only in safeguarding operations but also in helping businesses achieve their desired outcomes.25

- Preparing for new climate and sustainability reporting requirements: Eighty-three percent of non-US survey respondents (data not shown in the figures) said the European Union’s Corporate Sustainability Reporting Directive will have a significant-to-moderate impact on their 2025 strategies. This is in addition to other related EU regulations and policy changes. Among US respondents, 77% anticipated more regulatory emphasis on sustainability in 2025.

A majority of life sciences companies have reported better-than-average progress in meeting environmental, social, and governance goals, according to Deloitte’s 2024 Sustainability Action Report. However, until financial markets begin to view sustainability as an investment rather than a cost, corporate sustainability–related actions are likely to remain mostly a compliance issue, rather than a business strategy.

Implications of the new US leadership

President-elect Donald J. Trump highlighted several prescription drug topics during his 2024 campaign and through his endorsement of the 2024 Republican platform. He has promoted programs that aimed at lowering drug costs for seniors, but has not explicitly endorsed the drug-pricing provisions of the Inflation Reduction Act. Instead, he has indicated a preference for revising a proposal from his first term, which involved creating a “most favored nation” model to cap Medicare drug prices at the levels paid by other countries. During his first term, President-elect Trump enhanced generic drug competitiveness, allowed the importation of certain prescription drugs from Canada, and pushed for legislation to cap out-of-pocket spending for seniors.

The incoming administration has stated its intention to increase price transparency and expand choice and competition among prescription drugs. It may initiate policy changes around drug pricing to establish its own approach to drug price negotiation.

Although President-elect Trump has not specifically called for reforms to pharmacy benefit managers’ business models, several Republican lawmakers have been involved in bipartisan negotiations on this topic.26 At the end of his first term, President-elect Trump issued a final rule replacing the safe harbor for Part D rebates with a new safe harbor that applies only to discounts offered at the point of sale.27

Additionally, the first Trump administration made cuts to the 340B program that were later overturned by the Supreme Court; President-elect Trump may revisit cuts.28

Trump has criticized the Creating Helpful Incentives to Produce Semiconductors and Science Act (CHIPS Act), which encourages domestic manufacturing of semiconductor chips. Medtech companies rely on these chips for many of their products. The incoming administration may seek changes to the distribution of funds under the CHIPS Act.29

With the Republican control of the White House, the Senate, and the House of Representatives, Congress can use the budget reconciliation process30 to pass new legislation and modify existing laws. Reconciliation can only be used for policies that have a direct impact on the federal budget. Laws passed through budget reconciliation include the Affordable Care Act during President Obama’s administration, the Tax Cuts and Jobs Act during President Trump’s administration, and the Inflation Reduction Act during President Biden’s administration.

To prepare for the incoming Trump administration, biopharma and medtech organizations should:

- Monitor Presidential appointees within the Department of Health and Human Services, as they could signal the department’s and agency’s approaches to health policy.

- Assess how control within the House of Representatives and the Senate could influence health policy.

- Strengthen strategies for potential regulations and compliance at the federal, state, and local levels.

- Monitor bipartisan coalition-building in Congress around drug pricing, pharmacy benefit managers’ reform, and other policy issues affecting the industry.

Evolving customer expectations could influence strategies in 2025

Customer preferences and expectations are likely to shape strategies in 2025 and beyond. Life sciences companies are navigating increasingly complex relationships among a wide range of customers including consumers, hospitals, health systems, and health care professionals, whose needs, incentives, and expectations diverge. In our survey, 36% of C-suite executives indicated that improving customer experience, engagement, and trust was very important and 29% said they were prioritizing investments in a customer-engagement strategy.

Biopharma organizations demonstrated significantly more urgency in addressing customer engagement needs compared to medtech companies. Specifically, 32% of surveyed biopharma executives viewed evolving customer engagement needs as a significant trend, compared to just 18% of medtech executives. Additionally, 32% of biopharma respondents considered investments in customer engagement and enabling technologies a priority for 2025, whereas only 24% of medtech respondents shared this view.

Life sciences companies are also using digital technologies to personalize customer interactions. For example, Johnson & Johnson Innovative Medicine in Japan uses AI to tailor customer interactions based on feedback and preferences. Shuhei Sekiguchi, president and representative director of J&J Innovative Medicine in Japan, described the company’s approach during an interview: “In our commercial function, we are using AI to make sure that we’re taking in customer feedback, understanding their preferences, and then determining what our next interaction should look like and what channels we should use.”

Health care providers, including hospitals, health systems, and health care professionals (HCPs) are a core customer group for pharmaceutical firms and other life sciences organizations. However, only about one-third of HCPs say a pharmaceutical company’s customer-facing resources meet their needs, according to a 2024 Deloitte survey. By contrast, over 80% of pharma executives said they are satisfied with their current customer engagement strategy.31

While HCPs can be important influencers, health care consumers are increasingly acting as the “CEOs” of their health.32 Some consumers are turning to gen AI when making decisions about their care. They also are becoming more selective about their HCPs, and often demand increased personalization of therapeutics, frictionless support services, and technologies. In response, some life science companies have launched direct-to-consumer programs. In the United States, for example, Lilly announced a portal in early 2024 through which patients can purchase certain medicines directly from the manufacturer, often at a price lower than traditional channels.33 A few months later, Pfizer launched its PfizerForAll consumer portal.34 On the medical device side, Dexcom, a manufacturer of glucose monitors, recently released an over-the-counter continuous glucose monitor that can be purchased without a prescription.35

Biopharma and medtech companies show some differences in addressing the consumer experience as well. While 54% of biopharma respondents look to simplify enrollment in patient-support programs, only 26% of medtech respondents share this focus. At the same time, both sectors are similarly committed to enhancing patient care journeys and providing personalized insights. More than half (52%) of biopharma and 44% of medtech respondents said they plan to customize patient-support programs or care journeys based on consumer needs. Additionally, 50% of biopharma and 44% of medtech respondents reported that they plan to offer consumers more personalized health insights.

Preparing for future growth and innovation

The life sciences industry appears poised for significant transformation in 2025, driven by digital advancements and scientific innovations. Despite competitive pressures and business volatility, most global life sciences executives are optimistic about the future. “We are full of expectations for personalized medicine,” explained a senior vice president of a small German pharma company. “With advances in genomics and biomarkers, we can provide patients with more precise treatment options. This not only improves efficacy but also significantly reduces side-effects, allowing patients to have a better treatment experience.” Such advances demonstrate the power of innovative therapies and a path for navigating external pressures on pricing and reimbursement, regulatory processes, and geopolitical uncertainty.

The integration of technologies like gen AI and the increased use of data are expected to boost operational efficiencies and drive breakthrough innovations. As companies adapt to this evolving landscape, their ability to implement new initiatives will be crucial for differentiation and market expansion. The industry’s focus on advancing therapeutic solutions and improving patient outcomes highlights a promising future.

{kind=link}

{kind=link}