2025 US health care outlook

Health care leaders are focused on growth and profitability, while monitoring potential challenges and uncertainties ahead

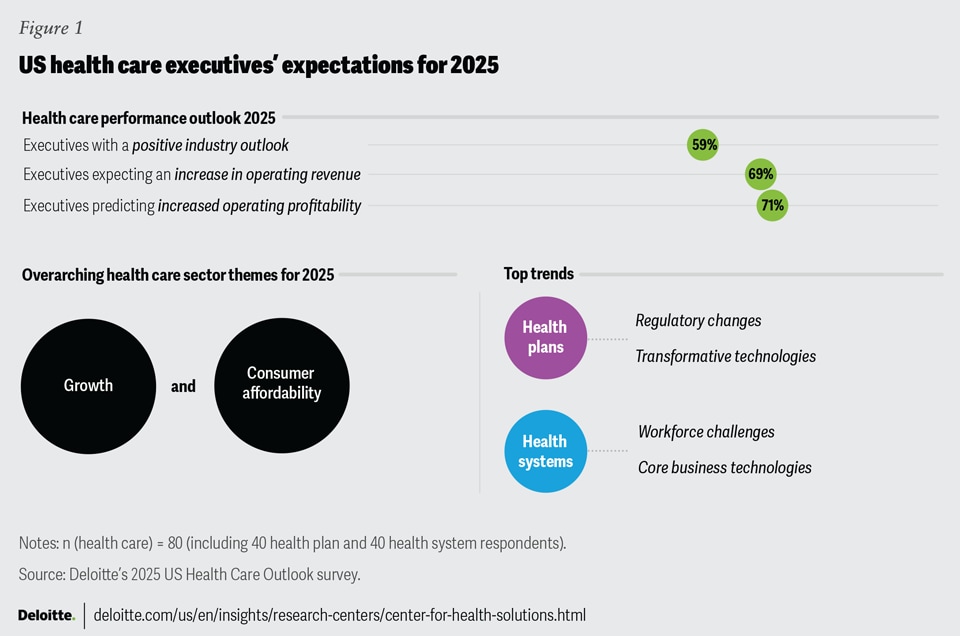

The US health care industry could be poised for change, as executives cautiously express a more favorable outlook for 2025. According to a survey by the Deloitte Center for Health Solutions, nearly 60% of industry leaders hold a favorable industry outlook for the year ahead, a notable increase from 52% just a year ago. This surge in confidence is underscored by the 69% of US health care respondents who anticipate a rise in revenue in 2025 and the 71% who expect improved profitability.

The Deloitte Center for Health Solutions surveyed 80 C-suite executives from large health systems and health plans in the United States (each with revenue greater than US$500 million) between August and September of 2024 to identify the top trends expected to impact their strategies for 2025. Over the past two years, many US health care organizations have faced margin pressure, workforce shortages, and an industrywide push to adopt digital technologies. After several years of stabilizing their businesses, 2025 could mark a turnaround period for the health care sector, driven by innovation, resilience, and strategic growth.

In addition, recent US federal, state, and local elections could lead to regulatory and policy changes that impact the health care industry. Forty-four percent of surveyed health care executives indicated that regulatory uncertainty could influence their strategies in 2025. The incoming administration of Donald J. Trump and the 119th Congress will likely have several priorities and issues to address, including laws and programs that could significantly affect health plans, health systems, and health care consumers. The implications will likely evolve throughout 2025 and therefore should continue to be monitored and assessed at the local, state, and federal levels (see “Industry implications of the incoming government administration”).

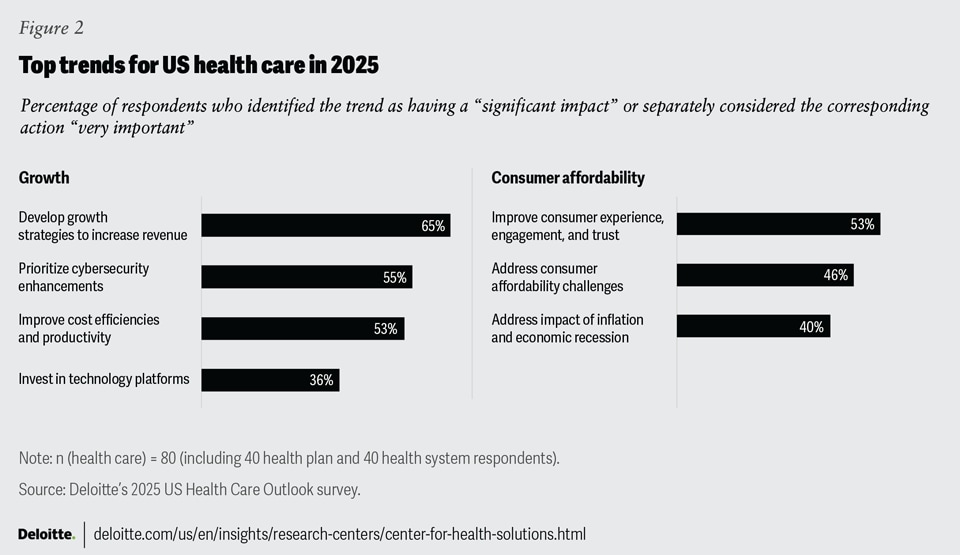

As they head into a new year, US health care organizations appear poised to tackle the dual challenge of driving growth while ensuring access to affordable health care for consumers. Sixty-five percent of executives cited developing growth strategies for their organizations as a top priority for 2025, making it the most selected trend for the sector (figure 2). Additionally, 46% of executives identified consumer affordability in health care as a top trend. However, balancing the growth of margins and profitability while keeping the cost of care in check and navigating an uncertain macroenvironment could be challenging for health plans and health systems. Both health plans and health systems face their own unique challenges and trends in the new year, necessitating a keen focus on identifying the right set of multidimensional strategies for 2025.

Multidimensional growth strategies for 2025

Sixty-five percent of health care executives identified “developing growth strategies to increase revenue” as a priority, making it the top action for 2025. However, growth is unlikely to be driven by a single strategy. Instead, survey respondents indicated they intend to take a multidimensional approach. According to the Deloitte 2024 Health Care CFO survey, about 25% of health care finance leaders reported that operating margins have fallen short of expectations over the past three years. Moreover, they ranked cost reduction as the lowest among their top concerns, despite it being a top priority in the previous four years of chief financial officer (CFO) surveys, likely reflecting that many believe their organizations have reduced costs as much as possible. This makes revenue growth even more important.1 Most health care executives who participated in the outlook survey intend to focus on organic growth in 2025, rather than relying on mergers and acquisitions for growth.

Overall, consumers are seen as an important aspect of this organic growth. In fact, fewer surveyed executives are focusing on mergers and acquisitions compared to strategies aimed at acquiring new consumers. To attract new consumers and drive organic growth, half of health plan executives and 55% of health system executives agree they need to improve consumer engagement, trust, and the overall consumer experience. Health care organizations might explore how other industries like retail or hospitality have successfully driven growth and cultivated consumer loyalty.2 Some of their consumer-centric growth strategies could be adopted by the US health care sector, including more thoughtful use of digital tools and technology platforms to enhance consumer experiences.

Health care organizations should consider the following strategies to help drive organic growth:

- Focus on consumer acquisition and retention: Health systems and health plans should tailor their products and services to specific market conditions and competitive landscapes. This could involve improving brand loyalty, refining product and service offerings, or introducing new products and services that appeal to the communities they serve. Notably, 21% of respondents said the development of new health and wellness-focused products is a priority for the upcoming year.

- Meet the needs of consumers: Health care organizations should consider creating products and services that prioritize consumer affordability and convenience. In fact, cost is the top reason people skip care, according to the Deloitte 2024 Health Care Consumer Survey. Consumers also cited access challenges such as long wait times for appointments, limited office hours, lack of transportation, and caregiving duties as top reasons for forgoing or delaying care.

Health care organizations should also focus on rebuilding trust. Prior focus group research by Deloitte cited poor experiences as a reason for distrust and skipping care. Trust also appears to be a factor with technologies like generative AI (gen AI), where the 2024 Deloitte 2024 Health Care Consumer Survey found that consumers want transparency and are concerned about gen AI being used to make decisions about their health and how their personal health data is being used.

- Invest in digital platforms: About one-third of health care executives identified technology investments as a priority for 2025. This underscores the important role of investing further in strategic digital transformation to help drive growth while also improving consumer experience. Digital platforms can include patient portal tools that help consumers schedule appointments, view test results, access health records, and receive provider communications, but they can also support apps that connect consumers with monitoring devices, symptom triage tools, and virtual visit services. The adoption of digital platforms should be considered in system redesign efforts aimed at improving patient experience because of their potential to reduce friction and enhance convenience and affordability.

- Strengthen cybersecurity measures: The transition to a digital environment has opened health care organizations to cyberattacks.3 Enhancing cybersecurity measures is important not only for mitigating risks and protecting brand reputation but also for safeguarding financial and brand stability. As such, 60% of health system executives and 50% of health plan executives reported that their organizations are prioritizing cybersecurity enhancements for 2025.

- Prioritize health equity as a business imperative: Some US consumers may require tailored or additional support to achieve equitable access to high-quality health care and outcomes. Health inequities—combined with social, economic, and environmental drivers of health—can negatively affect outcomes and experiences. Although only 23% of health care executives cited health equity as a priority for 2025, it can be an important lever for growth.

Developing products and services for specific populations could help health plans and health systems attract new customers and address unmet needs. One opportunity to help enable this effort is Community Health Needs Assessments (CHNAs), a regulatory requirement for nonprofit hospitals and health systems to gather data on the health status and gaps in their communities. These assessments provide an opportunity for these organizations to use the insights collected to develop services that address the unique needs of the communities they serve.

Addressing health care affordability for consumers

Health care executives identified “health care affordability for consumers” as a key trend likely to shape their 2025 organizational strategies. Since 2020, out-of-pocket costs have consistently outpaced the overall growth in health care spending, creating a potentially unsustainable situation.4 According to Deloitte’s actuarial analysis, women spend 20% more on out-of-pocket costs—based on their covered benefits—than men. Even after excluding maternal health expenses, employed women still spend 18% more than men on health care.5

This financial burden may compel some consumers to skip or delay essential care. The Deloitte 2024 Health Care Consumer Survey found that both men and women avoid care due to costs,6 women being 31% more likely to do so. Avoiding or delaying routine care can lead to the deterioration of health conditions, the exacerbation of chronic illnesses, and missed opportunities for early disease diagnosis, ultimately resulting in more severe health issues and higher treatment costs, especially for underserved populations.7

Health system and health plan executives should consider these strategies to help address consumer affordability:

Develop inclusive products and services

Health plans should examine their existing plan designs to ensure they meet the needs of all members equitably. Similarly, health systems should evaluate their service offerings by location to ensure they cater to the needs of all communities. Coverage and services should be affordable and accessible, regardless of ethnicity, gender, geography, or race. Additionally, offering health coverage products and care delivery services tailored to individual needs can help reduce costs (premiums and out-of-pocket expenses) for some. By implementing these strategies, health system and health plan executives can better address the affordability challenges faced by consumers. This, in turn, is likely to improve access to essential health care services and promote overall health and well-being.

Expand services and hours for alternative sites of care and virtual health

Health care services that are accessed digitally at home and outside the traditional nine-to-five clinic hours are becoming increasingly important to consumers as they prioritize convenience.8 To meet this demand, health systems should consider investing in alternative sites of care, extending clinic hours to include evenings and weekends, and offering virtual and digital health options. These measures can help reach a broader consumer base while potentially lowering out-of-pocket costs and indirect costs such as transportation and time away from work.

Our 2024 US Health Care Consumer Survey, found that 64% of consumers consider virtual visits more convenient, which is the primary reason they prefer virtual care over in-person visits. To help ensure broad adoption, health systems should evaluate the needs of the populations they serve. This includes addressing barriers such as lack of broadband access, unfamiliarity with technology, and the absence of private spaces for conducting virtual visits.

Invest in consumer-facing digital technologies

A growing percentage of consumers are using connected monitoring devices and digital tools for their health care—43% in 2024 compared to 34% in 2022.9 These technologies can enhance consumer experiences, aligning with the highly personalized experiences they’re accustomed to in industries like banking, retail, and entertainment. Digital monitoring tools, for example, can provide consumers with trending data that supports their health concerns, thereby giving them more agency during patient-clinician interactions. This can provide consumers with greater control and confidence, especially in areas like maternal health, where timely and informed interactions are crucial for preventing adverse outcomes.

Work more closely with employers

Employer-sponsored health insurance plans cover about 154 million people in the United States.10 Employers can play a pivotal role in promoting healthier lifestyles, as indicated by Deloitte’s actuarial modeling on aging. Health plans are well-positioned to help employers improve the health of their workforce through wellness programs, preventive care services, and customized coverage options. Health systems should also look for opportunities to collaborate with local employers to help improve workforce health. Health systems could design and implement onsite workplace prevention and screening clinics, directly contract with employers for the health system to deliver certain health care services to their workforce like joint surgery, and provide education and resources to improve workforce well-being. These strategies could help reduce the overall cost of patient care for employers and their workforce by decreasing the need for medical interventions.

Enhance operational efficiencies

Both health systems and health plans are focusing on strategies to reduce operational costs. More than half of the surveyed health care executives (53%) cited improving efficiencies and enhancing productivity as priorities for the coming year. This could include optimizing operating models to outsource or offshore capabilities that are not core to the business. It could also include using staffing models that upskill clinicians to the top of their license, investing in automation technologies and gen AI for efficiencies, and creating centralized command centers to boost efficiencies. Additionally, health care organizations might have opportunities to receive cash refunds, tax credits, or incentives through the Inflation Reduction Act (IRA) and from state and local jurisdictions related to decarbonization efforts.11 These measures could help strengthen operations and reduce overall costs.

Industry implications of the incoming government administration

President-elect Donald Trump highlighted several health care topics during his 2024 campaign and through his endorsement of the 2024 Republican platform.12 Republican leaders have said they do not intend to repeal the Affordable Care Act. The premium assistance tax credits, which are used to help defray the cost of health coverage purchased through the Affordable Care Act’s public insurance exchanges, were enhanced in 2021 as part of the response to the COVID-19 pandemic. The enhanced credits helped increase the number of enrollees to 21.4 million in 2024.13 The enhancements are set to expire at the end of 2025.14 That could push more people onto Medicaid and increase the uninsured population.

President-elect Trump also aligned to the GOP’s platform positions of protecting Medicare and targeting the high cost of some drugs.15 Consistent with actions taken during his first term, President-elect Trump has indicated plans to address surprise medical billing, price transparency, and out-of-pocket costs for consumers. While there is still pending information dependent on the incoming administration’s decisions, the use of budget reconciliation to change tax rules and government spending could put the provisions of various legislation on the table. Initially, the new administration is likely to focus on bipartisan-supported issues such as pharmacy benefit managers regulations, site-neutral payment policies, and drug-pricing limits under the Inflation Reduction Act. He has also been vocal about granting states’ oversight of reproductive-health decisions.16

The implications for health care organizations from the incoming Trump administration could likely continue to evolve throughout 2025. To prepare, organizations should consider:

- Monitoring presidential appointees: Keep an eye on presidential appointees within the Department of Health and Human Services and the Centers for Medicare and Medicaid Services, as they could signal how the department and the agency approach health policy.

- Evaluating legislative control: Assess how control within the House of Representatives and the Senate could influence health policy.

- Strengthening regulatory strategies: Strengthen strategies for potential regulations and compliance at the federal, state, and local levels.

Health plans and health systems have different priorities for 2025

The outlook survey responses indicated that health plans and health systems are prioritizing different goals and approaches for 2025. Most health plans are primarily focused on adopting transformative technologies, including gen AI. In contrast, health systems are more focused on strengthening their core legacy business technologies rather than investing heavily in digital tools and transformative technologies. Both sectors can benefit from leveraging transformative technologies across their organizations, but they have different levels of adoption with health systems lagging and focusing on improving legacy systems first.

Additionally, each sector faces unique market challenges: Health plans should navigate regulatory uncertainty in several areas that are expected to have important impact specifically for health plans, while health systems, though also navigating regulatory uncertainty, tend to be more concerned with workforce issues. These differences underscore the distinct strategies each sector appear to be employing to navigate the future landscape.

Health plans: Preparing for impending regulatory actions and embracing gen AI

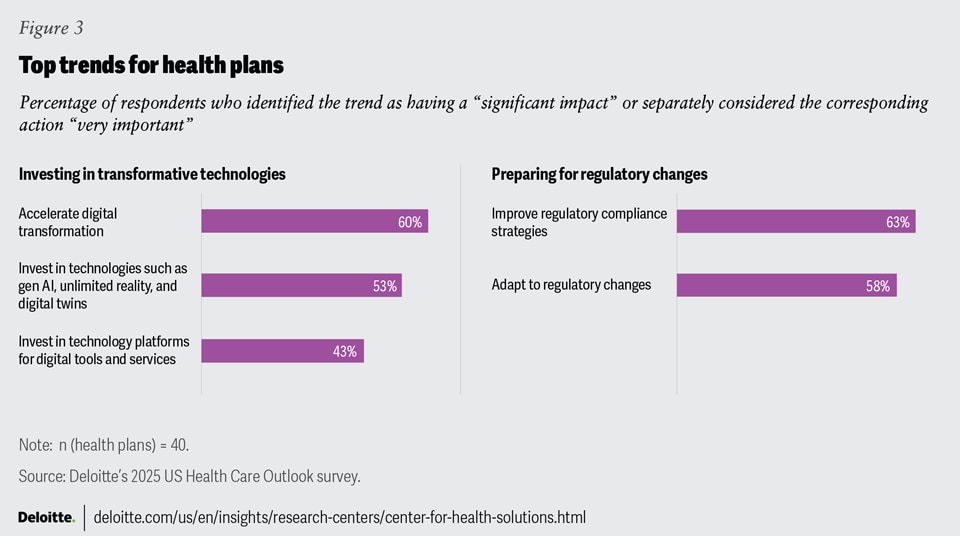

Sixty percent of health plan respondents anticipate the adoption of digital technology to accelerate in 2025, while 53% expect that gen AI and other transformative technologies like unlimited reality and digital twins will impact their organizational strategies (figure 3). Furthermore, we asked the executives to list the emerging trends they are tracking, and 58% identified AI and automation. Many health plans are already using gen AI17 in areas like claims processing, underwriting, personalized treatment plans, fraud detection, and document extraction. To help ensure health plans maintain momentum with this transformative technology, they should consider the following actions:

Strengthen governance

A well-defined governance structure is crucial for health plans as gen AI becomes more prevalent in the industry. Effective governance should foster interdisciplinary collaboration, encourage innovation, help ensure ethical considerations in AI deployment, and enable efficient management of vendors.

Prioritize data quality

High-quality, unbiased data is important for developing effective AI algorithms. Health plans should aim to incorporate diverse data sets, including social, environmental, and economic data related to the drivers of health, and maintain rigorous data quality standards.

Enhance consumer trust

While prior Deloitte research indicates that health care consumers are already engaging with gen AI, Deloitte’s 2024 US Health Care Consumer Survey found that 30% of consumers do not trust the information provided by gen AI, and 80% want to be informed when their doctor uses the technology to make decisions. Some consumers might be using free, publicly available gen AI tools, which can sometimes rely on inaccurate or incomplete information.18 These experiences impact their perspectives on the use of gen AI by health care organizations and present an opportunity for organizations to both educate consumers and design health care–specific gen AI tools.

Broaden technology use

Health plans should identify and assess opportunities to leverage transformative technologies beyond their current use cases. Gen AI has the potential to transform compliance activities, accounting, and other functions. By combining unstructured data sets with gen AI, health plans could create opportunities for improved and more efficient tracking, reporting, and monitoring.

Nearly 60% of health plan respondents expect that recent and upcoming regulatory changes will influence their organizational strategies in 2025. Issues that could potentially affect margins and medical loss ratios include adjustments to Medicare Advantage payment rates, Medicare drug-price negotiations under the Inflation Reduction Act, price-transparency regulations, stricter rules regarding mental health parity,19 and the 2025 Notice of Benefit and Payment Parameters.20

Regulatory changes are likely to continue, highlighting the need for health insurers to remain strategic. To effectively navigate this evolving landscape, health plans should prioritize strategic compliance planning, as the dynamic regulatory environment demands a strategic approach to compliance. In fact, 63% of health plan respondents are already prioritizing compliance strategies in 2025 to address these challenges head-on (figure 3). Additionally, health plans should be agile and proactive by actively monitoring discussions at federal and state levels regarding any legislation or proposals that could affect their business. This proactive stance is important for adapting to and managing regulatory changes.

Health systems: Addressing workforce challenges and strengthening core business technologies

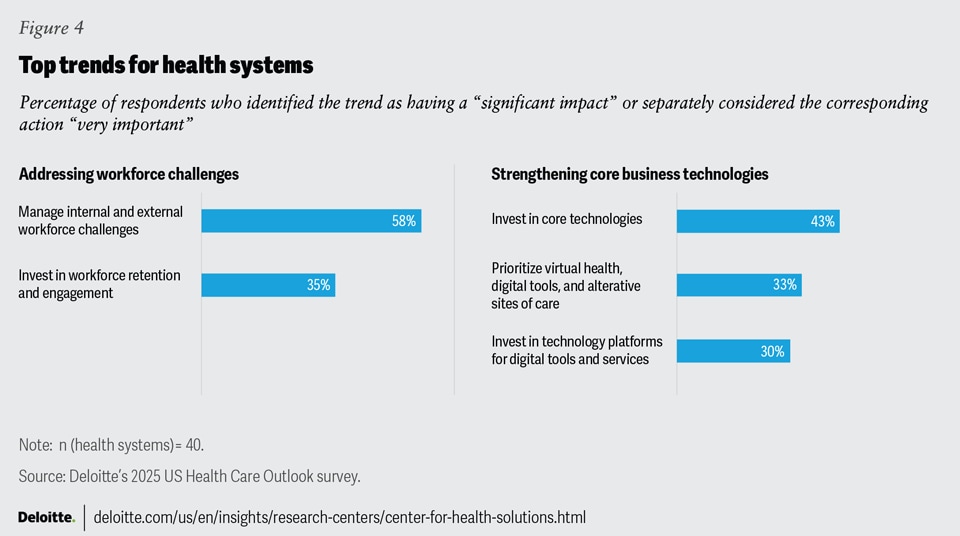

More than half (58%) of health system executives expect workforce challenges, such as talent shortages, the need for upskilling, and retention issues, to influence their organizational strategies in 2025 (figure 4). While workforce challenges remain a top concern, the urgency has decreased compared to two years ago when 85% of executives cited these issues during a substantial exodus of clinical staff, as noted in previous Deloitte US health care outlook surveys. Despite this, many health systems still face clinical talent shortages, clinician burnout, and rising labor costs. Health system leaders have an opportunity to rebuild trust and restore a sense of meaning, value, and purpose in their employees’ jobs. To address these challenges, health system leaders should look for opportunities to:

Reclaim workforce trust

The Deloitte clinician survey revealed a lack of trust among frontline clinicians, with less than half (45%) trusting their leadership to do what is right for patients, and even fewer (23%) trusting their leaders to do right by workers. To help rebuild this trust, health systems should consider actively listening to frontline workers’ concerns, foster a more inclusive culture where employees feel valued, and create leadership positions specifically for clinicians.

Redesign work teams

To enhance employees’ connection to the organization and acknowledge their important roles, health systems can establish comprehensive interdisciplinary care teams, provide curated training programs, and map out new career paths for their staff.

Invest in cost-saving technologies

According to the Deloitte workforce technology study, gen AI and automation technologies can cut in half the amount of time revenue-cycle staff spend on mundane tasks and give bedside nurses 20% more time to spend on direct patient care. Health systems should consider leveraging these technologies and exploring new work modalities, such as virtual nursing, to enable remote work possibilities for clinical staff.

Support workforce wellness needs

Health care organizations should offer benefits and programs aimed at improving the overall health and mental well-being of their workforce. These initiatives can include efforts to improve health literacy, provide access to preventive services, address burnout, and support overall well-being.

Health care organizations, especially health systems, have historically lagged other industries in terms of technological maturity.21 However, for 2025, health system executives plan to prioritize several tech-enabled strategies to strengthen their core operations. Specifically, 43% of executives mentioned investing in core business technology solutions like customer relationship management, enterprise resource planning (ERP), electronic health records (EHR), and automation (figure 4). Additionally, 30% cited investments in technology platforms for digital tools and services as top action items for 2025. Health systems aiming to strengthen their core business technologies can consider the following actions:

Invest further in core technologies

Health systems can focus on unifying their entire system of care on the same EHR platform, particularly for those involved in recent mergers and acquisitions. Additionally, expanding alternative sites of care and adopting ERP systems can be critical for creating efficiencies at the organizational level.

Modernize data

Updating data and management systems to be more efficient, streamlined, and accurate is critical to help ensure that a health system’s data is more useful. This involves integrating data from multiple platforms across the health system, creating interoperability with other health care organizations, and incorporating external social, economic, and environmental data sets. Governance, automation, privacy, and security should all be considered. This modernization is essential for effectively implementing cloud, gen AI, and other transformative technologies.

Adopt a cloud environment

Migrating to the cloud as the platform for all core technologies can help improve operations, efficiencies, and care delivery. Greater investments in cloud infrastructure, which offers substantial computing power, data storage, and security, are important for fully realizing the value of core technology investments. These capabilities are important enablers of AI and gen AI, positioning health systems to eventually invest in transformative technologies.

Establish command centers

Establishing centralized governance and operations structures, such as a center of excellence or a digital command center, can help drive better clinical operations, enhance supply chains, and improve interoperability between emerging technologies like gen AI, cloud, and 5G, and legacy health information technology systems like EHR and ERP.

Prioritize equity in design

All technology and operational investments and implementation projects at health systems should help ensure equitable access, experience, and impact for all users—consumers, clinicians, and administrative staff. Understanding the needs and impacts of different populations from a technology or operational change and intentionally designing to meet those needs or mitigate those impacts can help ensure broader adoption.

Opportunities for health system and health plan leaders in 2025

Health care executives appear to be entering 2025 with a renewed sense of optimism. However, balancing growth, profitability, and affordability of care for consumers is likely to remain a challenge. To help them achieve their goals for the new year, health plan and health system leaders should consider the following strategies that we’ve outlined throughout this outlook:

- Execute a multidimensional growth strategy: This includes retaining and acquiring consumers through improved experiences, trust, and services; leveraging digital tools and transformative technology; enhancing data quality; ensuring privacy; and tightening security.

- Meet the needs of all health care consumers: Understand the needs of different groups and identify ways to make high-quality products and services more affordable, accessible, convenient, and equitable.

- Remain resilient, innovative, and responsive: Be prepared to navigate the evolving competitive market and regulatory landscape.

Given the complexity of the market trends, no single strategy will suffice. By adopting a combination of these approaches, health care leaders can better position their organizations for 2025.

{kind=link}

{kind=link}

{kind=link}

{kind=link}