Promoting metals and mining sustainability in critical supply chains

The rising demand for metals and minerals is increasing focus on ensuring consistent supply and reduced emissions.

Stanley Porter

Ian Sanders

John Diasselliss

Brad Johnson

Kate Hardin

Abhinav Purohit

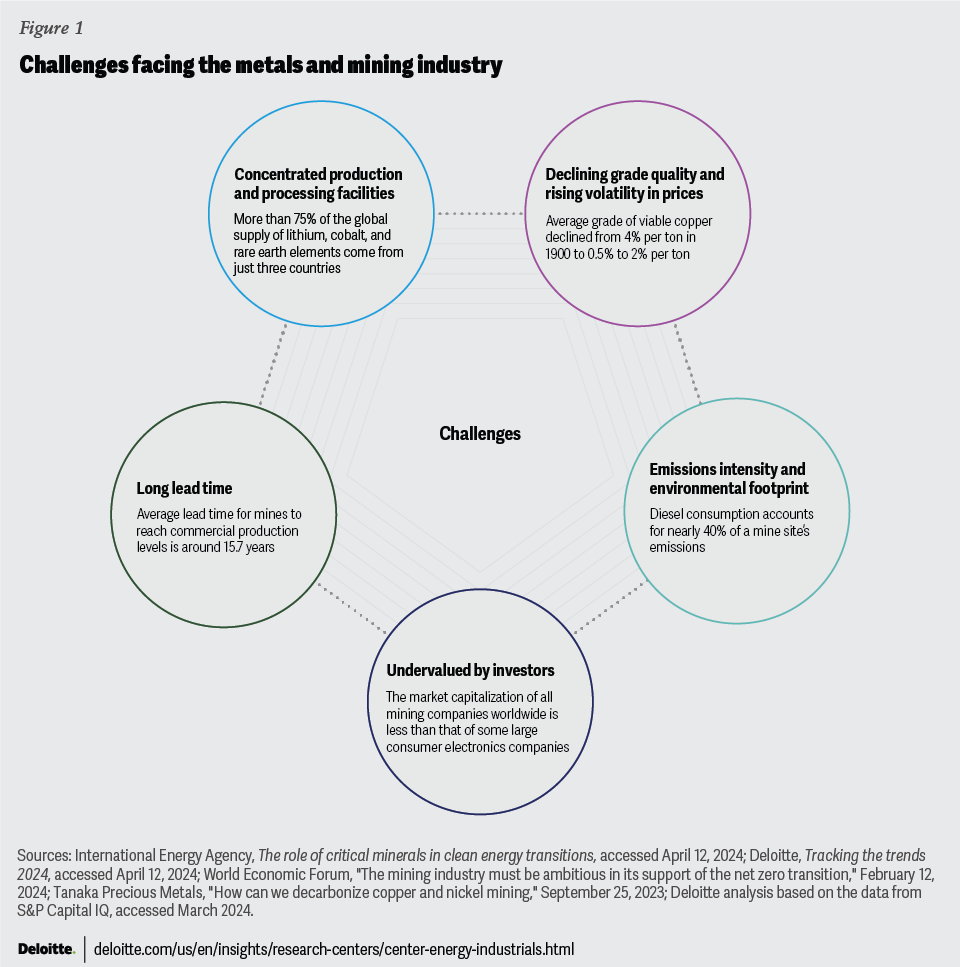

The transition toward a net-zero pathway necessitates an estimated US$850 billion in new investments in the metals and mining industry by 2030.1 The strong demand for renewable energy has resulted in a 200% surge in lithium demand, a 70% jump in cobalt demand, an 8% increase in copper demand, and a 40% growth in nickel demand from 2017 to 2022.2 Consequently, companies are concentrating on converting these resources into commercially viable reserves and subsequently salable metal, while ensuring consistent production and supply, and simultaneously reducing emissions.3 The contributing factors (figure 1) include:

- Concentrated production and processing facilities: Most critical minerals have at least half of the mining/extraction and processing facilities concentrated in just two countries.4 Although diversification is happening on the production side, most planned refining and processing operations are being developed in incumbent countries. China holds half of the planned lithium refining projects, while Indonesia accounts for almost 90% of planned nickel smelting facilities.5

- Long lead time: There remains a mismatch between the demand growth and project development timeline. In fact, mining projects can take more than 15 years to begin first production in part due to the delays associated with complicated permitting processes, with Environmental Impact Statements alone taking an average of 4.5 years to finalize in some cases.6 Gaining support from Indigenous communities is also critical—but it can take time. These realities create concerns about increasing the production capacity to keep pace with rising demand.

- Declining grade quality and rising price volatility: The average copper ore grade for producing mines declined by 25% between 2006 and 2016, requiring 46% more energy to ensure a 30% production boost.7 The development of increasingly complex yet lower-quality deposits necessitates significant investments and price incentives. However, price volatility persists for critical minerals as both demand and supply undergo maturation, and alterations in trade policies can be disruptive. For instance, the slower-than-expected demand growth for electric vehicles, coupled with an oversupply of lithium, resulted in the prices for lithium hydroxide and lithium carbonate falling by more than 80% from their record highs in 2022.8

- Challenges and opportunities in reducing environmental footprint: The metals and mining industry accounts for approximately 15% of annual global emissions, with nearly 40% of mine site carbon dioxide emissions stemming from the diesel used in mining equipment.9 Miners are experimenting with electric vehicles to reduce these transport-related emissions. Meanwhile, the metals and mining industry is aiming to improve its water stewardship across operations, with companies such as Freeport-McMoRan improving its average water-use efficiency from 87% to 89% between 2019 and 2022.10

- Under-owned or undervalued by investors relative to other industries: The foundational role of the metals and mining industry is increasingly being recognized by investors, reflected in the US metals and mining index outperforming the broader US S&P 500 index by 5% over the past three years.11 Despite this, the industry remains under-owned or undervalued, evident in the fact that the market capitalization of all listed metals and mining companies worldwide is smaller than that of many individual technology companies in the United States.12

{kind=link}

Accelerating progress: A phased approach to sustainability in metals and mining

The increasing demand for critical minerals and long development timelines highlight the need for swift production scaling. A tri-phased strategy—focused on the asset, system, and cross-system level—should be considered to help further integrate sustainability into the metals and mining industry.

Building a foundation for sustainability

Efficiency should be enhanced and the environmental impact of existing mines reduced, while integrating new production sources sustainably.

- Improving the efficiency of production processes: Incorporating operational technologies alongside advanced visualization and analytical tools can help improve efficiency in the metals and mining industry.13 Advanced planning techniques like linear programming and integrated planning systems, supported by technologies such as digital twins, drones, and machine learning, can help minimize operational uncertainties and streamline logistics, including hauling routes and equipment scheduling.14 This can enhance precision mining for superior ore extraction and improve resource allocation, while reducing production bottlenecks and downtime. In fact, a relatively inexpensive hyperspectral sensor enabled the discovery of US$25 million of additional resources at a West Australian iron ore mine, while a multinational mining company implemented a machine learning solution that could help predict pump failures in metals refining processes up to 40 days in advance.15

- Optimizing the resources used: Over half of the current lithium and copper production occurs in high water-stress regions, necessitating aggressive water conservation. Additionally, the mining industry employs more than 50,000 large mining trucks, mostly diesel-powered and consuming about 900,000 liters of diesel annually. These hold significant decarbonization potential as merely eliminating diesel can cut mine site emissions by 40%.16 Further, certifications that establish premium pricing for sustainably produced minerals can help promote sustainable practices. For instance, the “Fairmined Certification” ensures that miners receive a fair price, including a premium, as a market incentive to cover the costs of the certification and to invest in mining operations, social development, and environmental protection. In fact, more than US$5 million of Fairmined Premium has been paid to certified mining organizations since 2014 for reinvesting into the community.17

- Adding new capacity in at a lower emission level: Incorporating new technologies can help in developing solutions that result in yield improvements and prioritize sustainability. For instance, leveraging direct lithium extraction may double the yield and reduce the production time from months to days while producing lower emissions compared to traditional extraction methods.18 Similarly, innovative technologies such as molten oxide electrolysis can directly convert metal oxides into metal using electricity, increasing energy efficiency and reducing the carbon footprint.19

Building efficiency and resilience across the value chain

Despite potential resource concentration (particularly of critical minerals), resilient supply chains can help ensure supply reliability and fair pricing. Additionally, value chain partnerships can spur innovation, minimize disruption risk, decrease critical mineral consumption, ease resource stress, and boost equitable access.

- Minimizing supply risk for downstream sectors: More than 75% of the global supply of copper, cobalt, graphite, and rare earth elements remains concentrated in China, Chile, and the Democratic Republic of Congo.20 To mitigate concentration and disruption risks, some companies are shoring up these supply chains by forming global mining partnerships and concluding long-term fixed-price contracts. For instance, General Motors has sought to safeguard its critical minerals supply through several long-term agreements with entities such as Vale Canada for battery-grade nickel, Livent (now Arcadium Lithium) for lithium, Glencore for sustainable Australian cobalt, and MP Materials for US-sourced rare earth materials.21

- Localizing supply chains: Partnering with and upskilling local suppliers can reduce sourcing time, cost, and transport emissions by bringing localized solutions to complex problems. For instance, mining companies in Ghana have collaborated with local manufacturers to create vital mining equipment, thereby reducing operational expenses and boosting local manufacturing abilities.22 Local sourcing requirements are often required or strongly encouraged by governments; therefore, success can help enhance business value and create goodwill with both governments and communities.

- Collaborating for sustainable mineral use: Partnerships with battery manufacturers could lead to new material chemistries, such as iron-phosphorus-based lithium iron phosphate batteries and sodium-ion alternatives, reducing the need for certain critical minerals. Wider adoption of these new material chemistries could eventually reduce mineral demand for EV batteries by 20% in 2050.23

Developing an ecosystem approach to managing expansion and environment

Many growing mining operations, often overlapping with Indigenous lands, necessitate active community collaboration for acceptance and permit acquisition.24 Similarly, recycling of metals and minerals is key to helping reduce environmental impact, conserving natural resources, and enhancing supply chain resilience.

- Emphasizing community engagement for sustainable licensing: Working with local communities in advance of submitting permitting applications and documentation can help with early identification of key sites or ecologically sensitive areas, potentially avoiding delays later in the permitting process. Further, partnerships among industry, academia, and local communities can strengthen the talent pipeline by fostering a training and hiring ecosystem. For example, the partnership between Cameco and the Pinehouse Lake community in Canada offers jobs and business opportunities to the local community.25

- Elevating recycling impact through industrywide synergy: Enhancing recycling rates for critical minerals could create a secondary supply that could help meet around 10% to 20% of mineral demand by 2030 in a net-zero scenario (see sidebar, “Boosting recycling for sustainability”).26 However, the minerals and metals recycling processes currently remain expensive, time consuming, and labor intensive. Mitigating this challenge would likely require spurring new technological innovations through measures such as cross-sector partnerships with industries like automotive. For example, Albemarle and Caterpillar Inc.’s collaboration aims to advance battery cell technology and recycling.27 Some miners are also “forward integrating” by acquiring recycling firms, like Sibanye-Stillwater’s purchase of Reldan, to strengthen its recycling capabilities, potentially increasing metal recycling rates.28

Boosting recycling for sustainability

Electric vehicles that were sold in 2019 alone are predicted to generate a staggering 500,000 tons of unprocessed battery pack waste at the end of their life span.29

This imminent waste surge underscores the imperative to boost recycling levels of minerals like lithium and certain rare earth elements, which currently languish below 10%.30

Moreover, enhancing recycling rates could also cut emissions since, for example, the copper production process from recycling releases around 43% fewer emissions compared to traditional mining.31

The tipping points of change: Important factors shaping sustainability in metals and mining

The pace of unlocking sustainability in metals and mining could be impacted by four factors:

Finance

Even as investments increase for critical minerals mining, meeting the Net Zero Emissions (NZE) scenario would require bridging the investment gap of US$180 billion to US$230 billion for additional projects.32 Some actions to consider for continued funding include:

- Establishing ownership integration: Engage downstream consumers, like automotive manufacturers and defense companies, for direct investments in mining, refining, and precursor materials. In fact, General Motors and Tesla’s acquisition of lithium assets and the US Department of Defense’s agreement to secure graphite for large-capacity battery production represent such an approach.33

- Entering into long-term contracts: Implementing contractual safeguards such as long-term fixed-price contracts can help in anchoring demand and mitigating raw material price volatility. Such agreements can also help encourage sustainable business practices, as witnessed with Glencore’s agreement, which formally embedded responsible sourcing and sustainability into a cobalt supply contract between 2020 and 2029.34

- Capitalizing on government incentives for project security: Utilize tax incentives, early-mover grants, and critical mineral agreements to minimize risks for capital-intensive projects. For example, the US Department of Energy made available US$39 million for 16 projects across 12 states to develop technologies that increase the domestic production and processing capacity of critical minerals for the clean energy transition.35

- Unlocking sustainable financing for lower capital costs: Adopt affordable financing solutions such as sustainability-linked bonds or loans to reduce capital costs. For instance, Teck Resources utilized a US$4 billion sustainability-linked credit facility with key performance indicators related to emissions, safety, and diversity.36

Technology

Declining ore quality has contributed to a 28% productivity drop in global mining operations over the past decade.37 Addressing this can include the use of advanced technologies such as automation, AI, and data analytics. Factors that can help drive technology-led transformation in the metals and mining industry include:

- Digitalizing and automating existing operations: Integrating sensor-based data with existing information networks to unlock Internet of Things (IoT) capabilities can help enhance overall process efficiencies. Glencore, for instance, was able to boost its overall efficiency and increase its average tonnage from 55 tons to 60 tons per outing by leveraging data collected from interconnected resources and equipment using digital sensors.38 Similarly, automating material haulage operations can drive cost reduction and increase productivity, as seen with Rio Tinto, where autonomous fleet operations lowered operating costs by 13% and improved productivity by 14% compared to manual fleet operations.39

- Enhancing performance through asset modeling: Adoption of digital twin systems can help develop virtual models of physical assets, systems, and processes that can be used to simulate different operational scenarios and help optimize activities that improve mining productivity.40 For example, a multinational mining company modeled theoretical truck and operator performance and compared it to actual in-field performance, leading to a 23% reduction in haul cycle times at its Mogalakwena platinum mine in South Africa.41

- Optimizing the exploration process: The use of geophysical and mapping technologies can enhance the effectiveness of the exploration process. Rio Tinto, for example, uses hyperspectral imaging, which is 50 times more effective than traditional multispectral satellite imagery, to identify iron ore outcrops in Australia’s Pilbara region, leading to the discovery of new deposits.42 Similarly, some companies, such as VerAI and Kobold, are leveraging artificial intelligence and machine learning to collect and analyze multiple streams of geological data to predict the location of mineral deposits.43 Meanwhile, Eurasian Resources Group unveiled NOMAD, a remotely operated soil sampling robot, which can explore the complex terrains of Saudi Arabia for critical minerals.44

Business models

To help meet the growing demand for sustainable products, many mineral and mining companies are opting to modify their business models to create further agility and resilience. This could involve the use of strategies that engage stakeholders across the value chain, thereby accelerating adoption.

- Developing new infrastructure models: Scaling up critical minerals production remains challenging due to the absence of single-operator-led capital investment, which typically underpins the development of bulk minerals like iron ore through dedicated rail and port facilities.45 Mitigating this challenge likely requires multi-user infrastructure models that allow users to pool their expertise and resources for developing the necessary capabilities that can expedite the supply in a cost-effective manner.

- Adopting integrated partnership models: Joint ventures and minority investments can integrate the value chain to mitigate supply and pricing risks. Companies developing disruptive technologies can also benefit from such partnerships, as seen with BMW Ventures and Breakthrough Energy’s funding for Mangrove Lithium.46

- Fostering mining-as-a-service models: Mining companies, like Inspire Resources Inc. in Canada, are shifting to operator roles, with communities controlling resources. This helps enable flexible, scalable operations and closer community engagement.47

Talent

Meeting the net-zero target is expected to require around 0.7 million new workers in the critical minerals extraction industry by 2030, representing an 88% increase from 2022 levels.48 Similarly, around 3.5 million job openings are expected to need to be filled in the metals and machinery industry across the European Union between 2022 and 2035.49

- Attracting the next generation of talent: Shifting perceptions from resource extractors to sustainability catalysts could help attract new talent into the industry. This involves regular engagement with youth via school programs and community initiatives. For example, Less Common Metals, a specialty metals manufacturer, partnered with Xplore Science Discovery Museum to create a “Mine to Magnet” workshop for engaging primary school students ages 9 to 11.50

- Leveraging global talent resources: Creating a global talent marketplace would require industry collaboration, standardization of skills and certifications, and adoption of automation and remote work. Establishing such global talent pools can make it easier for companies to recruit for specialized skills, knowledge, and experience.

- Embracing new ways of working and workforce models: Recognizing and embracing the preference of employees to work from non-remote locations could help attract skilled talent to the industry. However, traditional job structures may also need to consider shifting to a skills-based model with project-based work and gig talent integration to enhance talent utilization, skill development, and industry attractiveness.

- Drawing talent across industries through competitive benefits: Diversify recruitment sources by hiring from other programs or industries with similar skills. This could involve tailoring the employee benefit strategies to focus on different benefits such as family assistance, hazard pay, and insurance in line with the reality of the remote and harsh work environments of the metals and mining industry.

Three pivotal architects: Policymakers, companies, and consumers play a distinct yet interconnected role in driving metals and mining sustainability

Simultaneous efforts by all stakeholders—policymakers, companies, and consumers—is important for sustainable development.

- Streamlining permitting processes: Improving transparency in policymaking and permitting processes could prevent duplication of efforts and delays due to multiple authorizations. A singular, integrated process can swiftly evaluate impacts and mitigation strategies. For example, the Government of Canada plans to expedite the permitting process for critical mineral development by adopting measures such as, but not limited to, enhancing interdepartmental and provincial coordination while also introducing a public permitting dashboard for greater transparency and accountability. These measures could potentially reduce the process duration from 12–15 years to approximately five years.51

- Encouraging community engagement early on: Active involvement from all stakeholders can help to align plans and strategies with shared sustainability objectives. Inclusive dialogues with communities remain important to comprehend their needs and vulnerabilities, while enhanced collaboration can help clarify environmental and socioeconomic risks from business expansion.

- Establishing a digital mine: Transitioning to a higher level of digitalization necessitates a solid data management foundation for reporting, simulations, analytics, and decision-making. Organizations may also rely on external support for data readiness and preparation until their internal teams are adequately skilled. The role of resilient, digital leadership is a crucial factor in developing digital strategies that align with business priorities and in utilizing technology to enhance workforce engagement.

- Tracking efficiency and emissions across the supply chain: Efficient supply chain management is important to track and manage emissions. Proactive identification and specific strategies are required to manage emissions and ensure regulatory compliance, stakeholder transparency, and cost-effectiveness through energy conservation and waste reduction. In fact, some major multinational mining companies are leveraging blockchain solutions that track metals and minerals from the source to the customer using key provenance and sustainability indicators to offer transparency regarding emissions.52

To align their actions with the global sustainability goals and the expectations of their stakeholders, the metals and mining industry would likely benefit from streamlined policy guidelines, enhanced collaboration between all stakeholders, and integration of digital technology that improves transparency and efficiency.