Prioritizing infrastructure decarbonization

Developing low-carbon assets for the future is important, but scaling the decarbonization of existing infrastructure, especially in transport, buildings, and industries, should be prioritized.

Stanley Porter

Teresa Thomas

Misha Nikulin

Kate Hardin

Anshu Mittal

Ayla Haig

Global carbon dioxide emissions hit a record high of 36.8 billion metric tons in 2023, a 1.1% increase over 2022.1 Although emissions growth has decelerated in recent years, these current figures, especially in a sluggish macroeconomic environment, indicate that emissions have not yet peaked. While developing new low-carbon assets for tomorrow is important, attention should shift to decarbonizing existing infrastructure to realize the time value of carbon. Reducing emissions today has more value—it requires lower capital expenditures and can mitigate the impact of future emissions—than delaying the process to tomorrow.

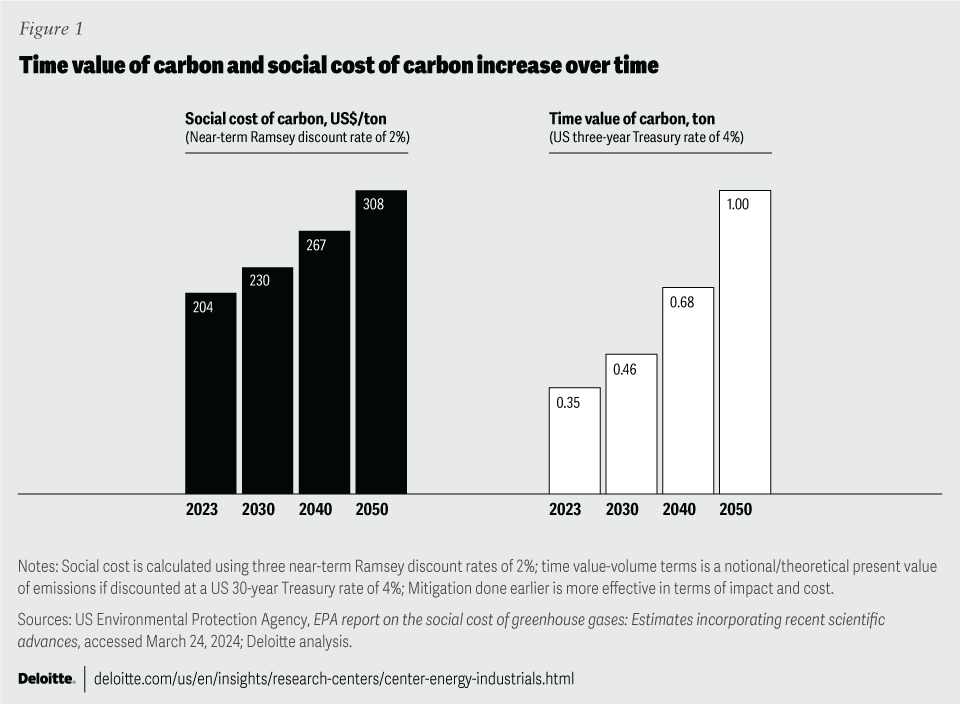

To understand the urgency to decarbonize now, consider this: Each year’s delay in carbon reduction incurs US$150 billion in incremental costs.2 In terms of time value, the present social cost of carbon is roughly 33% lower than the projected 2050 cost, and capturing 1 metric ton in 2050 is akin to capturing only 0.35 metric tons today (figure 1).3

{kind=link}

Scaling decarbonization of industries, buildings, and transportation

Industries (40%), buildings (39%), and transportation (20%) are the three principal (direct and indirect) emitters of global energy and process-related carbon emissions, which makes them an essential component of scaling decarbonization.4 Initial efforts to decarbonize have delivered noteworthy outcomes: Electric vehicles currently represent one of seven new passenger vehicles sold globally,5 and emissions across the building and industrial sectors have barely increased over the past five years, even amid strong GDP growth.6 Yet, to leverage the time value of carbon promptly, an exponential increase in the speed and intensity of decarbonization across the three sectors is crucial.

To systematically scale up the decarbonization of industries, buildings, and transportation, consider a tri-phased scaling approach that focuses on asset, system, and cross-system transformation.

Industry

Decarbonization in the hard-to-abate heavy industrial sector is among the most complex. Major modifications in the industry, motivated by an array of objectives and end advantages, often have a direct effect on regional economic prosperity and competitiveness, requiring adaptations in processes, feedstocks, and subsequently, cost structures. A tri-phased approach could focus on:

- Advancing energy efficiency and electrification: In light industries, more than 90% of heat demand requires temperature below 400 degree Celsius, where technologies such as heat pumps and electric boilers are already commercially available.7 But heavy industries such as steel and cement, which require continuous high heat, face significant challenges in achieving full electrification. These challenges stem from high initial capital expenditure, a lack of feasible alternatives, and the complexity of replacing their current self-sourced 24x7 dedicated power supply with a low-carbon alternative. However, solutions like long-term power purchase agreements can offer avenues for securing reliable, low-carbon electricity. A US-based steel mill, for example, operates under a 20-year fixed-rate power purchase agreement, which provides electricity that is 50% more cost-effective than direct grid procurement.8

- Capturing dual waste outputs—carbon and heat: Industries facing high costs of decarbonization can potentially reduce their emissions by plugging into emerging carbon capture and storage (CCS) hubs. By connecting to CCS hubs, industries can mitigate their emissions without entirely overhauling their existing infrastructure, which could be particularly beneficial for those where decarbonization through renewable energy is expensive or technically challenging. About 390 CCS projects that can capture and store up to 360 million tons per annum of CO2 are in production and under-development phases, with increasing diversity in CCS applications across industries.9 Likewise, capitalizing on waste heat, particularly using heat pumps to reclaim and utilize it for facility operations, could be among the quickest and most cost-efficient methods to decarbonize industries. According to some estimates, between 50% and 80% of the primary energy input used for thermal purposes in light industry manufacturing plants is discarded as waste heat.10

- Fostering industrial symbiosis to help maximize resource efficiency of underutilized by-products or residues: Instead of single-sector groupings or industrial parks, consider the benefit that industrial symbiosis could bring, whereby industries are set up based on their interconnectedness of by-products, waste, residues, logistics, etc. and can therefore maximize resource efficiency and minimize value chain emissions. An industrial symbiosis project in the city of Kalundborg, Denmark, is a case in point where the partnership involving 17 public and private companies is reported to result in annual savings of three million cubic tons of groundwater and 62,000 tons of residual material that is recycled. Moreover, estimates suggest it has led to an 80% reduction in CO2 emissions since 2015.11

Buildings

The Global Buildings Climate Tracker decarbonization index stands at only 8.1 points out of 100 as of 2021.12 To reach the 2050 target for decarbonization, it would need to be about twice as high.13 The challenge at hand: Any improvement in energy efficiency and decarbonization is more than offset by the expansive growth in global floor area, which has grown by over 10% in the last five years to above 240 billion square meters.14 A tri-phased scaling strategy for systematically scaling up the decarbonization of buildings should consider:

- Retrofitting existing buildings: With 80% of the homes that people will inhabit in 2050 already built and up to 75% of today’s buildings expected to still be in use by 2050,15 one priority to consider should be to retrofit existing buildings with energy-efficient and smart energy management solutions (for example, smart electric panels, plus thermostats). On average, only 1.5% of residential buildings are retrofitted annually in advanced economies; this can be partly attributed to the high upfront costs for retrofitting, which can reach as high as US$50,000 per home in the United States.16 Incentivizing homeowners to make this investment can reduce their carbon footprint. For instance, Maryland's EmPOWER program offers incentives and technical support to homeowners, renters, and businesses for improving insulation, sealing air leaks, and installing energy-efficient appliances.17

- Emphasizing building codes to help limit embodied emissions in new construction: The global floor area is projected to double to 450 billion square meters by 2050, significantly increasing the embodied emissions linked with the construction of new buildings.18 More than two-thirds of this new building stock is expected to be in emerging and developing economies, where the absence of effective building codes and sustainable construction practices may pose a challenge in limiting embodied emissions in new construction. Even in developed economies, local authorities could regularly update building codes, enforce stringent emissions limits for large buildings (like New York’s Local Law 97 for buildings over 25,000 square feet, starting from 2024), and improve incentives for owners to pursue green tax credits and certificates.19

- Investing in new material and digital design capabilities: Emphasis should be placed on developing proficiency in both passive-cum-standardized solutions (such as solar-oriented building placement and green roofs) and advanced, digital design and materials (such as smart glass windows and treated wood). This fusion could be essential for creating cheaper-to-retrofit universal solutions for a range of building types and climates while simultaneously promoting innovation to bolster the durability, flexibility, and overall efficacy of buildings. A case in point is the ductless air-to-air heat pump, which is cheaper than natural gas boilers for new installations in small houses across mature markets, such as Denmark and Japan, owing to reduced piping and installation costs.20 But building owners should be mindful of their role in decision-making, as their decisions can influence the adoption of new materials and practices.

Transportation

Among the three primary sources of emissions, transportation emissions remain below the 2020 pre–COVID-19-pandemic levels, partially reflecting rising electrification in the transportation sector. However, beneath this positive development, challenges persist, such as societal dependence on personal vehicles and the absence of a connected public transportation system in suburban or rural areas.

- Continuing the innovation in automotive and material technologies: Advancements in automotive technologies, such as enhanced engine efficiency, the utilization of lightweight materials, and the integration of hybrid fuel technologies, can be crucial for achieving immediate and substantial emissions reductions from lightweight vehicles, particularly in countries with nascent electric infrastructure. These progressions could be amplified by accelerated innovation, driven by collaborative efforts in battery, fuel cell, and material development. The global hybrid vehicles market, for example, is projected to rise at a compound annual growth rate of 28.8% from 2023 to 2032.21

- Scaling electric vehicle infrastructure: From less than 5% in 2020, about 18% of all new cars sold globally are electric in 2023.22 But high initial costs (23% more expensive without credits than an internal combustion engine vehicle), range anxiety, and lack of charging infrastructure still hinder adoption.23 Rapidly expanding electric vehicle infrastructure growth in the residential, commercial, and private sectors would require leveraging electric vehicle–ready building codes as well as new elements in urban planning. Moreover, the impact on the grid should be addressed by considering intelligent charging management and dynamic pricing mechanisms that can encourage off-peak charging. Finally, establishing a robust supply chain along with advanced end-of-life battery and charging options can help mitigate the impact of the disruptions across the electric vehicle value chain.

- Expanding and enhancing mass transit: There’s a pressing need to enhance and make mass transportation options (bus, rail, air, and ship) more environmentally friendly, while also improving road, port, station, and airport infrastructure—especially in suburban areas—and connecting them more effectively to mainland networks. Over the past five years, total inland transport infrastructure investment (in constant US dollar terms per inhabitant) for 29 major nations have been growing at a compound annual growth rate of only 3.5%, nearly at par with the global GDP growth rate.24 This underscores the necessity for potential value of government funding and investment, similar to the investments authorized by legislation like the Infrastructure Investment and Jobs Act, which provides US$102 billion for total rail funding.25

The tipping points of change: Important factors contributing to the decarbonization trajectory

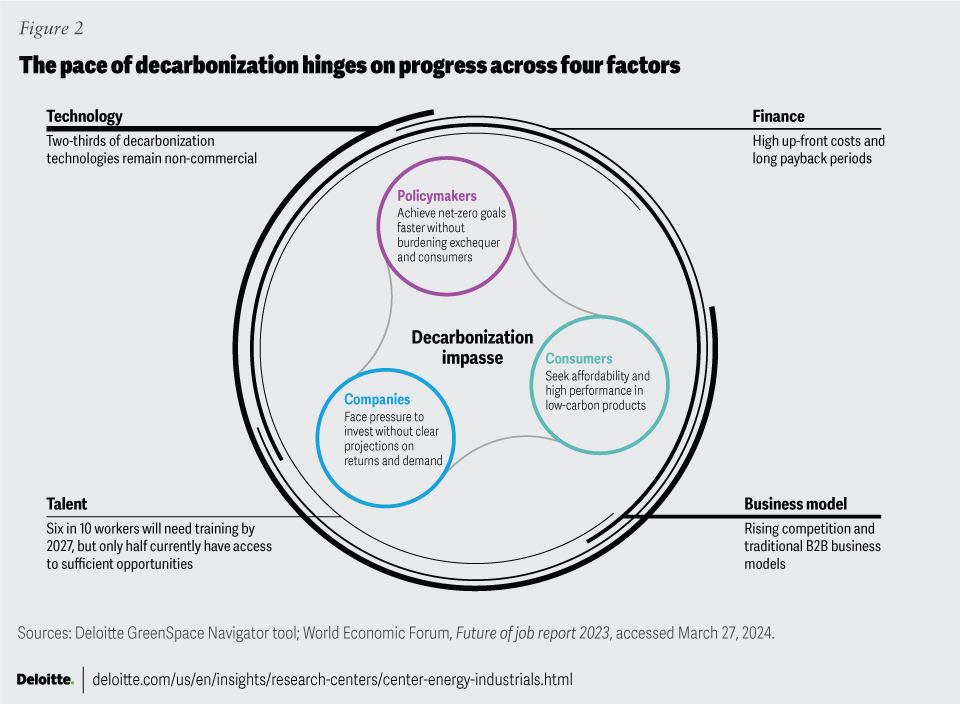

The pace of decarbonization efforts hinges on capital availability, talent accessibility, technology readiness, and commercial business models (figure 2). Progress across these factors has become a complex cycle of interdependencies. Funding often relies on proven technology, yet new business models may struggle to justify investment. Simultaneously, uncertain demand can contribute to conservative hiring, while a lack of technical skill sets hinders innovation.

{kind=link}

Finance

High upfront costs with long payback periods and cost-conscious consumers often limit the adoption of low-carbon products. Unlocking financial support for decarbonization measures could involve:

- Exploring alternative financing mechanisms: Financing mechanisms like transition finance and energy efficiency–linked financing, where energy savings fund the cost of the equipment and infrastructure generating those savings, could play a role in decarbonization efforts. KlimaDAO, for example, is a platform piloting the collective funding of climate projects by decentralized autonomous organizations.26 Once those credits are sold, these organizations can distribute dividends to investors or reinvest back into projects. The federal government is also widely using energy-savings performance contracts as an alternative financing mechanism to fund critical energy, water, and resilience-related updates, while paying a loan off through guaranteed energy savings.27

- Leveraging insurance offerings to distribute risk: These could mitigate risks in low-carbon projects through the establishment of insurance pools, which distribute risk across investors, thereby enhancing project attractiveness to financial institutions. In CCS projects, for example, where there is limited loss history available, underwriting by insurers can instill confidence in investors and project developers, facilitating the scaling of these solutions by minimizing the risks associated with debt-based financing.28

- Funding project finance with public-private partnership: Financing large-scale projects often involves substantial capital investments, and raising capital could also be done via the public-private partnership model wherein the federal investments (public funds) are matched to the private sector investments. For instance, the US federal government announced plans to allocate around US$6 billion for 33 projects aimed at decarbonizing eight hard to abate industrial applications. Although the federal investment, which is made available through the Inflation Reduction Act and Infrastructure Investment and Jobs Act, is subject to negotiation between the companies and the US Department of Energy, it is expected to be matched by the projects and would offer over US$20 billion for demonstration of commercial-scale decarbonization solutions for a net-zero industrial sector.29

Technology

About two-thirds of decarbonatization technologies for hard-to-abate sectors aren’t commercial yet.30 Certain steps can help propel technology-led decarbonization:

- Incorporating advanced materials: Materials such as carbon-fiber composites and advanced coatings can improve product efficiency and durability. For example, the energy and carbon payback period for wind turbine blades made with these materials has seen a 5% to 13% reduction, compared with traditional materials.31 Nevertheless, the production processes for these materials may involve forging new supply chains. To tackle these concerns, some companies are pioneering recycled carbon fiber production, and others like Bcomp Ltd. and BMW are developing lightweight flax fiber materials as alternatives to carbon-fiber-reinforced plastic in specific applications.32

- Pre-commercializing innovation hubs: Such hubs can build an ecosystem where a consortia of government, universities, and companies collaborate on early-stage research and development for low-carbon solutions. This can also facilitate training employees on these new technologies.

- Leveraging digital assets for improved decision-making: Digital technologies, such as artificial intelligence and data-driven analytics, can help comprehensively assess decarbonization investments and projects across a spectrum of outcome-based parameters that encompasses financial and environmental dimensions. Virginia’s System for the Management and Allocation of Resources for Transportation Scale, for instance, evaluates potential transportation projects based on multiple factors, including safety, congestion mitigation, accessibility, economic development, and environmental impacts.33 Moreover, a growing number of global platforms are now utilizing blockchain technology to track emissions throughout product life cycles, enhancing understanding of supply chain sustainability.34

Business models

Energy and industrial companies could adapt their traditional business-to-business bulk supply to a dynamic business-to-business-to-consumer model and, in some cases, move from a commodity mindset to a customer mindset. Competition from nontraditional entrants and the uncertainty of obtaining a premium for low-carbon products from consumers can present business challenges. The following actions can help companies better adapt to evolving market reality:

- Leveraging third-party or contract business models: These could be useful intermediaries, such as heat as a service, energy efficiency as a service, or energy service companies. These companies can offer subscription fees; equipment leasing; maintenance, repair, and operations services; and performance-based contracts.

- Offering bundled products and services: These embed energy solutions into everyday purchases. For example, the Dutch Energiesprong retrofitting program combines energy retrofits with upgrades of kitchens or bathrooms, potentially reducing the time to retrofit and also reducing a building’s energy use by as much as 80% in some cases.35

- Adopting impact-based pricing strategies: Implementing such strategies can alleviate consumer hesitancy regarding paying a premium and promote the adoption of low-carbon products. Deloitte’s ConsumerSignals data found that 45% of surveyed consumers were willing to pay a premium of 27% for sustainable products over available alternatives.36

Talent

Competition for skilled employees across sectors is often exacerbated by tight labor markets in many countries amid rising demand for new digital skill sets. The World Economic Forum highlights that by 2027, six in 10 workers will need training, yet only half currently have access to sufficient opportunities.37 Improving the talent availability would require new approaches to talent recruitment, such as:

- Expanding the talent pool: Recruiters should look to broaden their scope beyond traditional skill sets. About 30% to 50% of green jobs in the United States in 2022, including roles like solar consultant, waste management specialist, and environmental technician, were filled by individuals transitioning from adjacent fields with no prior experience in green sectors.38

- Encouraging green skill intensity in manufacturing and oil and gas: Sustainability jobs, like sustainability analysts, sustainability specialists, and sustainability managers, are among the fastest growing roles on LinkedIn in the past four years. LinkedIn’s data indicates that the manufacturing and oil and gas sectors have the most jobs or roles that require green skills.39 According to the World Economic Forum, Austria, Germany, Italy, the United States, and Spain are leading in the adoption of green skills within the manufacturing sector. In the oil and gas sector, India, the United States, and Finland are at the forefront in terms of green skills implementation.40

- Building of talent ecosystems: Businesses should actively partner with universities to develop tailored programs and tap into the growing number of students enrolling in urban planning degrees, thereby investing in a skill set that can yield future benefits with significantly reduced training costs. This collaboration could be essential for helping to build a comprehensive talent ecosystem, alongside partnerships for skills training, raising awareness of green job opportunities, and fostering vocational programs and apprenticeships.

Three pivotal architects: Policymakers, companies, and consumers play a distinct yet interconnected role in driving decarbonization

Decarbonization requires action from three important players: policymakers, companies, and consumers. Recognizing the compounding effect of their collective efforts is important for helping achieve exponential progress. Are there common starting points that can expedite progress of enablers and harness the power of collective action?

- Stimulating internal demand: Governments could be both producers and consumers of low-carbon energy, and their high purchasing power can provide the necessary scale for clean technologies and products to companies. For example, the largest municipality in the United States, New York City, could have the potential to substitute up to 27% of its fossil gas procurement with carbon-negative renewable natural gas generated from wastewater biogas co-digested with food waste.41 These efforts would align with the goals outlined in the Biden administration’s Federal Sustainability Plan, which includes measures such as disclosing federal contractor greenhouse gas emissions with science-based targets, promoting low-carbon materials through a “buy clean” initiative, and adopting a sustainable products policy.42

- Integrating urban planning: Policymakers and companies should involve urban planners and city governments in the discussion, fostering a strategy for non-personal vehicle solutions. This collaboration should prioritize addressing last-mile challenges, improving commuting options, and reimagining urban infrastructure, such as streets and sidewalks, with consideration for rising temperatures and unpredictable weather patterns.

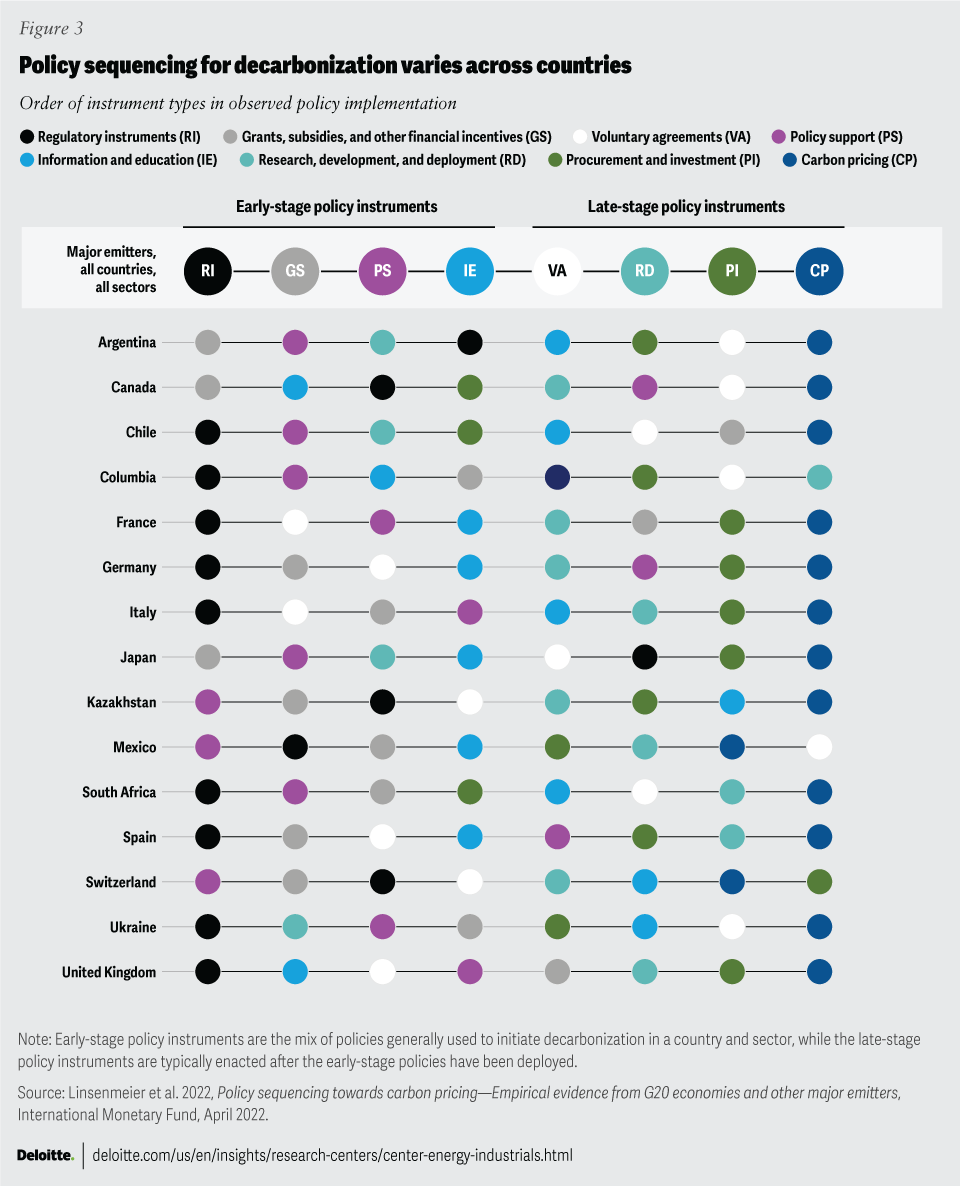

- Creating balanced and unified policy frameworks: Policymakers may have an opportunity to design policies that reduce compliance costs (figure 3), thereby helping to alleviate undue financial strain on the treasury or consumers (see sidebar, “Global unification of emissions reporting framework”). Such policies could prioritize emissions reduction while remaining technology agnostic. With the global public debt of governments at a record-high of US$92 trillion in 2022, revenue-neutral policies that implement carbon pricing mechanisms and direct the generated revenue to offset costs for consumers and companies could be crucial.43

- Building confidence together: Financial regulators, lenders, and borrowers can help mitigate risks at every stage of low-emission technology projects, from development to operation, facilitating their expansion. Tokio Marine & Nichido Fire Insurance Co.’s Mega-Solar Package Program, for example, combines insurance coverage across property, liability, and warranty, with risk consulting services, for solar power plant facilities.44

- Maintaining consumer centricity: Process-focused decarbonization is pivotal, but companies should not overlook their customers and end users. A comprehensive decarbonization strategy should enable customer-side decarbonization, prioritize affordability, and proactively address their purchase hesitancy.

{kind=link}

Global unification of emissions reporting framework

The global consolidation of emissions reporting frameworks, led by the International Sustainability Standards Board (ISSB), is a stride forward. This unified approach streamlines reporting, offering clarity for companies managing multiple standards.

Aligned with the board and major frameworks and endorsed by the dissolved Task Force on Climate-Related Financial Disclosures, this consolidation boosts consistency and effectiveness in promoting sustainable practices.

Tailoring decarbonization strategies to national contexts

Universal progress across these dimensions is important for the world to embark on the long road to net-zero. But the path to decarbonization will likely be unique for each nation, adapted to meet its specific needs and circumstances. Along this path, a myriad of decarbonization options are expected to emerge, requiring three actions: strategic policy sequencing, risk mitigation, and resource prioritization from both governments and companies.

A nation’s policy sequencing, ranging from early-stage programs that initiate decarbonization to later-stage policies that amplify its adoption, would be guided by relative policy costs and deliverability. According to research conducted by the International Monetary Fund, there exists a notable divergence in policy sequencing among major emitters (figure 3).

Each nation should balance decarbonization efforts with considerations for economic output, manufacturing competitiveness, affordability, and energy security, in both the short term and longer term. Equally, each nation should prioritize decarbonization projects based on their potential co-benefits beyond emissions reduction, encompassing job creation, social equity, biodiversity protection, etc.

As this intricate journey toward net-zero is underway, the diversity of national approaches highlights the complexity of decarbonization; yet, within this diversity lies the fertile ground for innovation and collaboration, propelling toward a sustainable future.