{kind=link}

{kind=link}

{kind=link}

Green products come of age has been saved

Cover image by: Natalie Pfaff

The authors would like to thank Marcello Gasdia for his contributions to the article.

Netherlands

United States

United States

United States

Sustainable products are no longer niche. According to Deloitte’s ConsumerSignals, nearly half (46%) of consumers across 23 study countries purchased at least one sustainable good or service in April 2023.1 This figure was even higher in 2021 (61%)—before inflation put a squeeze on household finances and fewer consumers could justify the heavier price tags green products sometimes command.

The current percentage of global consumers buying green represents a solid demand floor in the face of economic uncertainty. Demand for green products isn’t coming from a niche segment of young, affluent climate activists; it’s coming from the mainstream audience.

As buying green goes mainstream, consumer expectations of sustainable products are beginning to mature across a growing number of product categories. But consumers are also signaling intentions to reward innovative brands that deliver on sustainability promises by showing a willingness to pay a premium of 27% on average.

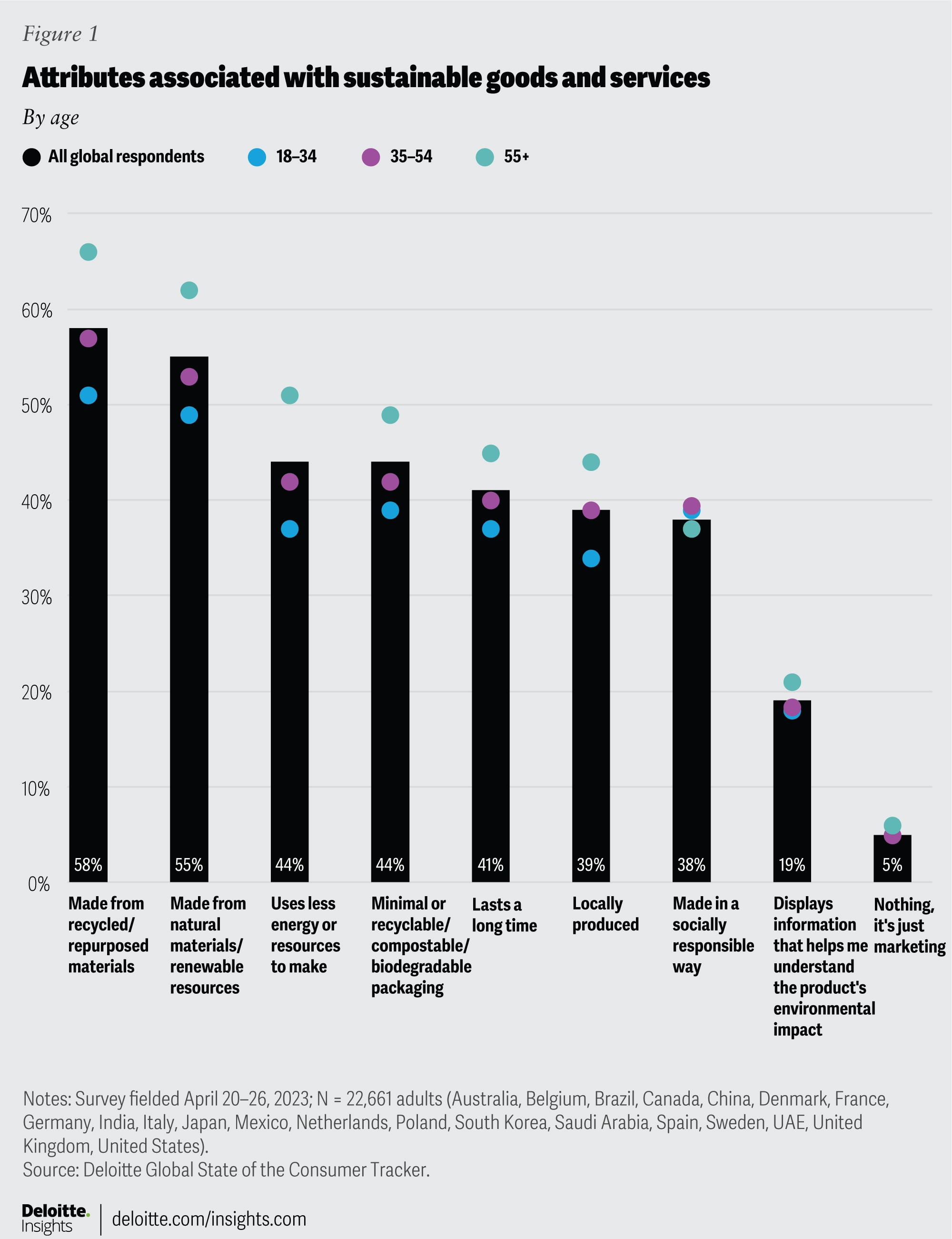

Evidence of the rising maturity of green products isn’t coming just from healthy global demand, but also from consumers’ rising expectations of green products. Only 5% of global survey respondents feel eco-related branding is simply a marketing gimmick (figure 1).

Most consumers associate sustainable goods with a holistic, intertwined set of attributes. When prompted with a set of nine distinct attributes, study respondents defined green products using an average of four. Roughly one-quarter selected six or more.

Attributes related to materials (e.g., natural/renewable or recycled/repurposed) remain the most commonly cited. But consumers don’t just care about what products are made from. Many are paying attention to how and where they’re made too. Factors such as energy or resources used in production (44%) and production location (39%) rank relatively high (figure 1). Many also consider packaging (44%), product durability (41%), and even the availability of information about the product’s environmental impact (19%).

And for many consumers, green products are even branching out of the environmental realm toward social responsibility. Four in 10 stated they consider products sustainable when they are made in a socially responsible way—for example, from brands that employ diverse employees and pay fair wages.

Another sign pointing to the maturity of green products is the proliferation of purchases across more corners of the consumer industry.

Perhaps not surprisingly, food and grocery remains the most popular category, and for good reason. Many consumers were likely first introduced to sustainable products in the food category. Organic, farm-raised, non-GMO (genetically modified organism), and other similar offerings arrived on the scene early at the grocery store and appealed to consumers wanting to do right by the planet—and their health. Relative to other product categories, consumers purchase food often, and people have had time to cement eco-forward purchase behaviors into habit. Among nearly half of the consumers who purchased a sustainable good in the past month, roughly one-third (35%) said their purchase fell in the food category (figure 2). The fresh food subcategory alone represented about a quarter (24%) of the purchases.

The more important implication for consumer companies, however, is that two-thirds of green purchases didn’t happen in food. Daily household goods such as paper goods, cleaning products, and other subcategories represented more than one-quarter of purchases (figure 2). Clothing (8%), personal care and beauty products (5%), transportation (8%), and home furnishings and appliances (5%) are all firmly on the map too. And together, smaller categories such as housing, leisure travel, recreation, and electronics accounted for roughly one in 10 purchases.

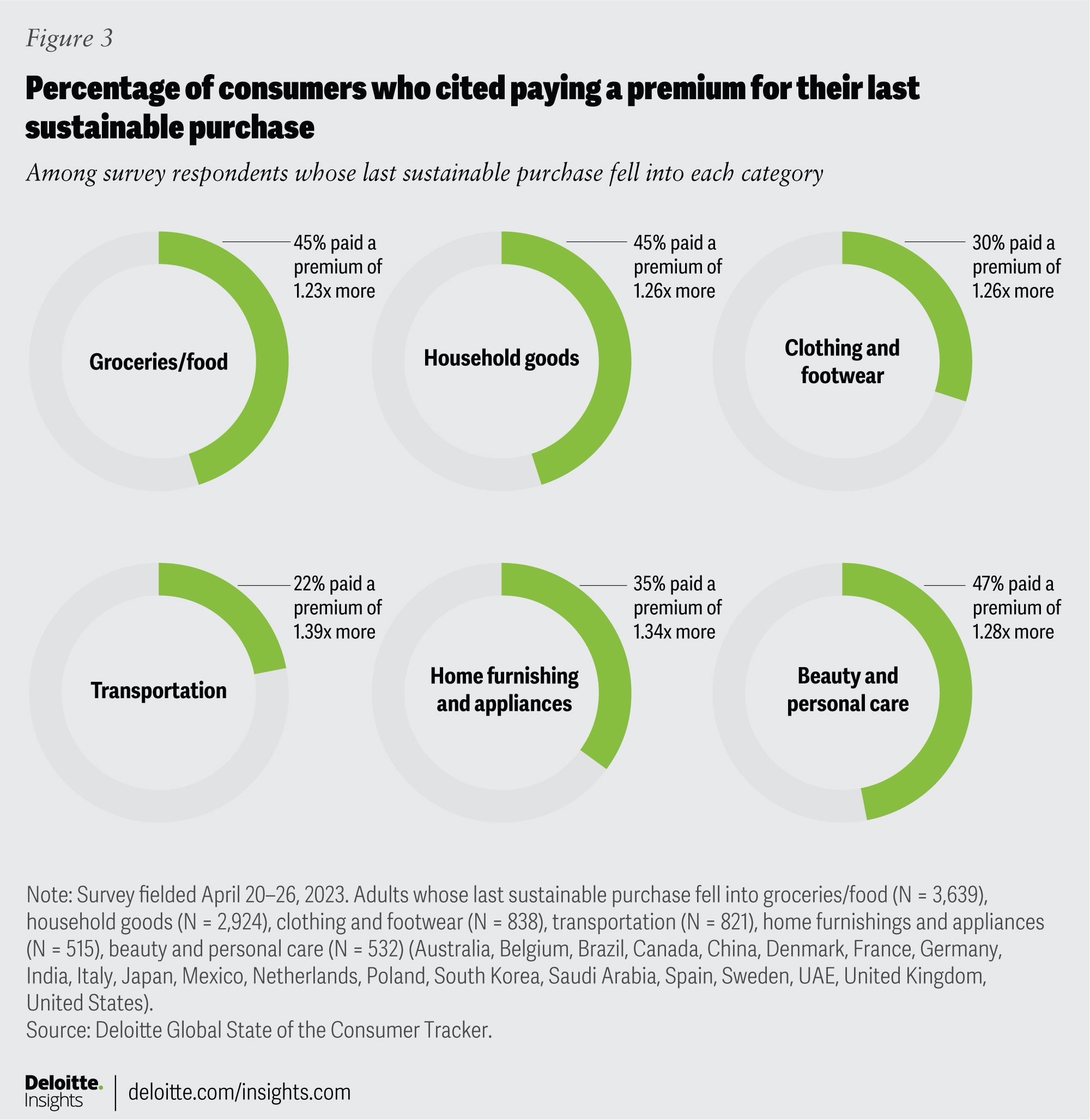

While expectations of green products are rising, consumers are signaling a willingness to reward brands that deliver. When asked about their last sustainable purchase, roughly four in 10 consumers cited paying more for it than an available alternative (figure 3). Among those who spent more, consumers estimated paying 27% more on average.

Not surprisingly, the willingness to pay a premium varies across categories. Consumers are more likely to pay premiums within lower-price-point, frequent-purchase categories—such as groceries, household goods, and personal care. In these familiar categories, the trade-offs tend to be better known and the risk of trying is relatively low. However, premiums paid in these categories tend to be lower.

In contrast, fewer consumers cited paying a green premium for less-frequent, higher-cost purchases such as home furnishings, appliances, and transportation (including vehicles). But the premiums tend to be higher. Consumer companies focused on higher-ticket items face a balancing act. While the addressable market of consumers willing to pay premiums for higher-cost goods is smaller, they’re likely to pay more.

Customer expectations of green products are only poised to accelerate as more brands focus their innovation efforts on sustainability. A recent Deloitte survey of executives in consumer packaged goods companies found that slightly more than half (54%) believe consumer sustainability is a critical area for consumer product innovation.2 Over 70% said their companies are likely to make significant investments in sustainability innovation within the next year, with sustainable packaging and new product offerings cited as top priorities.

With high consumer interest in sustainability, brands will likely need to move quickly. Consumers could easily switch to buying from the growing crop of niche players already making inroads. Partnerships are also likely to be critical. When asked what’s needed for success in sustainability innovation, companies most often point to new technologies and support from third-parties—which could also be a source of new technologies.3 After all, innovation is a team sport.