2024 Deloitte back-to-school survey

Value moves to the top of the class

Nick Handrinos

Brian McCarthy

Stephen Rogers

Lupine Skelly

Kusum Raimalani

In our 17th annual back-to-school survey, families are caught in a balancing act as they prepare to embark on their second-largest spending expenditure of the year.1 Respondents are juggling several aspects—the need to check necessities off school lists versus splurging on the novelty items their children want, and the need for low prices versus their desire for convenience. They are also trying to balance a cost-of-living squeeze with wanting to prioritize repadding their savings and enrolling their children in extracurricular activities.

In short, it’s an exhausting time for parents and an opportunity for retailers to take some of the friction out of the occasion, especially as $31.3 billion in potential sales are up for grabs.

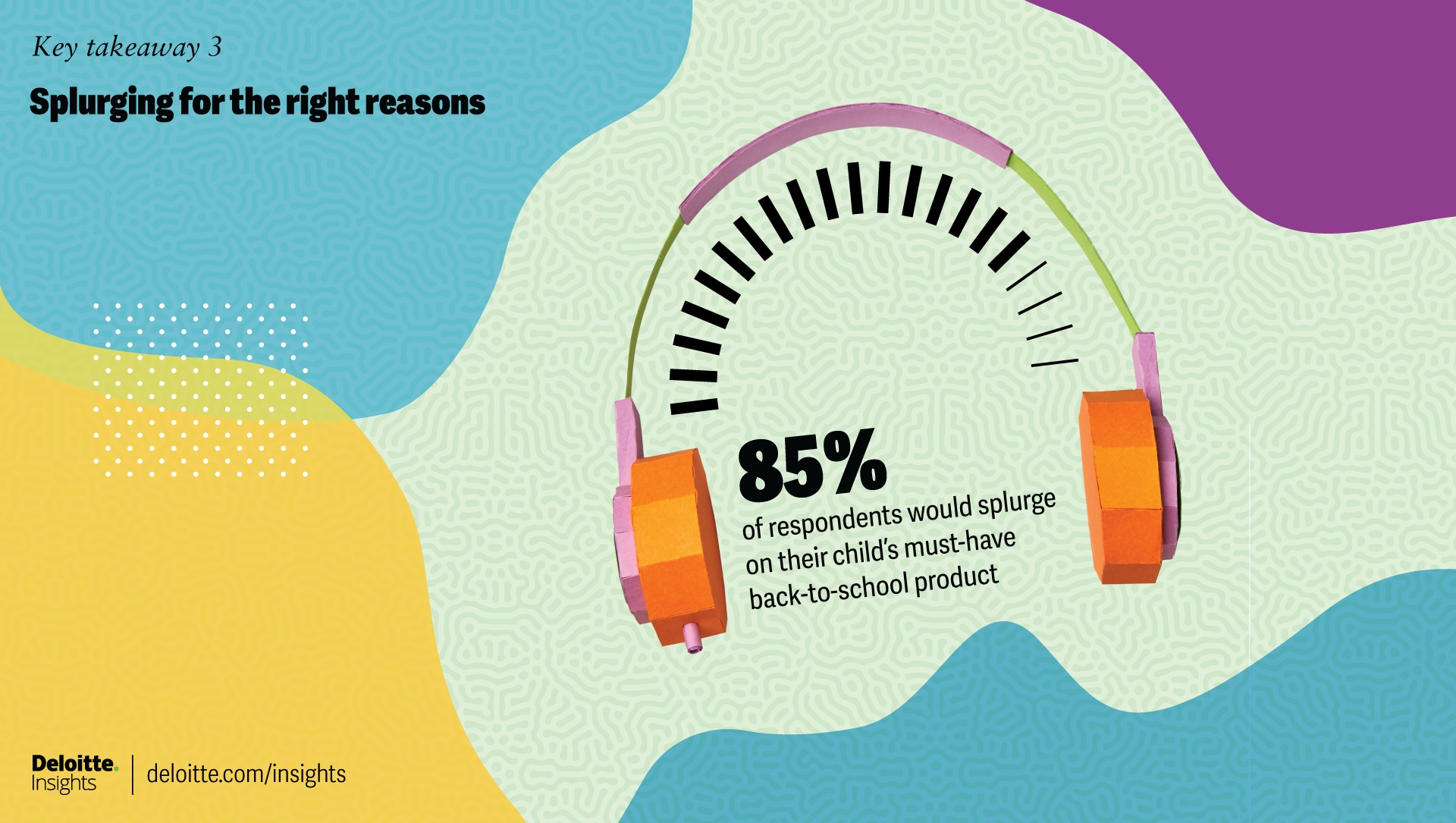

In May 2024, we surveyed nearly 1,200 US-based parents of school-aged children (grades K to 12) to learn about their back-to-school spending plans. The survey respondents made it loud and clear that value is top of mind for them. Further, they’re looking to shop earlier in the season to find the best deals, especially around the mid-July promotional events. The more money they can save early on, the more wiggle room they could have for a few indulgences, as 85% of those surveyed said they could be influenced to splurge on their children’s must-have products, while 50% planned to purchase something for themselves.

To help capture these incremental dollars during an event focused on economizing, retailers should consider leaning on their loyalty levers. Shoring up loyalty programs and creating consistent in-store and online experiences will likely be crucial for retailers to build trust and encourage loyal behavior. Further, retailers can help ease the anxiety around the event by making it convenient for consumers through consistent omni-channel experiences.

Read on for key takeaways and download the full survey findings.

Key takeaways

Parents weigh prices and priorities

As families continue to navigate a cost-of-living squeeze, they’re having to prioritize where their incremental dollars go. With a focus on repadding their savings and investing in extracurricular activities, respondents are taking a cautious approach to back-to-school spending. They plan to spend an average of $586 per child, similar to last year.

What’s in it for retailers

Eighty-six percent of surveyed parents have enrolled their children in extracurricular activities and plan to spend $582 per child on these activities (including fees and equipment). Retailers should therefore consider ways to take advantage of parents willing to go beyond school necessities as they stock up on supplies and gear for these activities.

Low-income (–4% YoY) and middle-income (–9% YoY) parents are pulling back on spending as they struggle with finances and are concerned about economic conditions. To alleviate their anxiety, retailers should consider shoring up loyalty programs and offering incentives to keep consumers shopping all season long as loyal back-to-school shoppers spend 35% more.

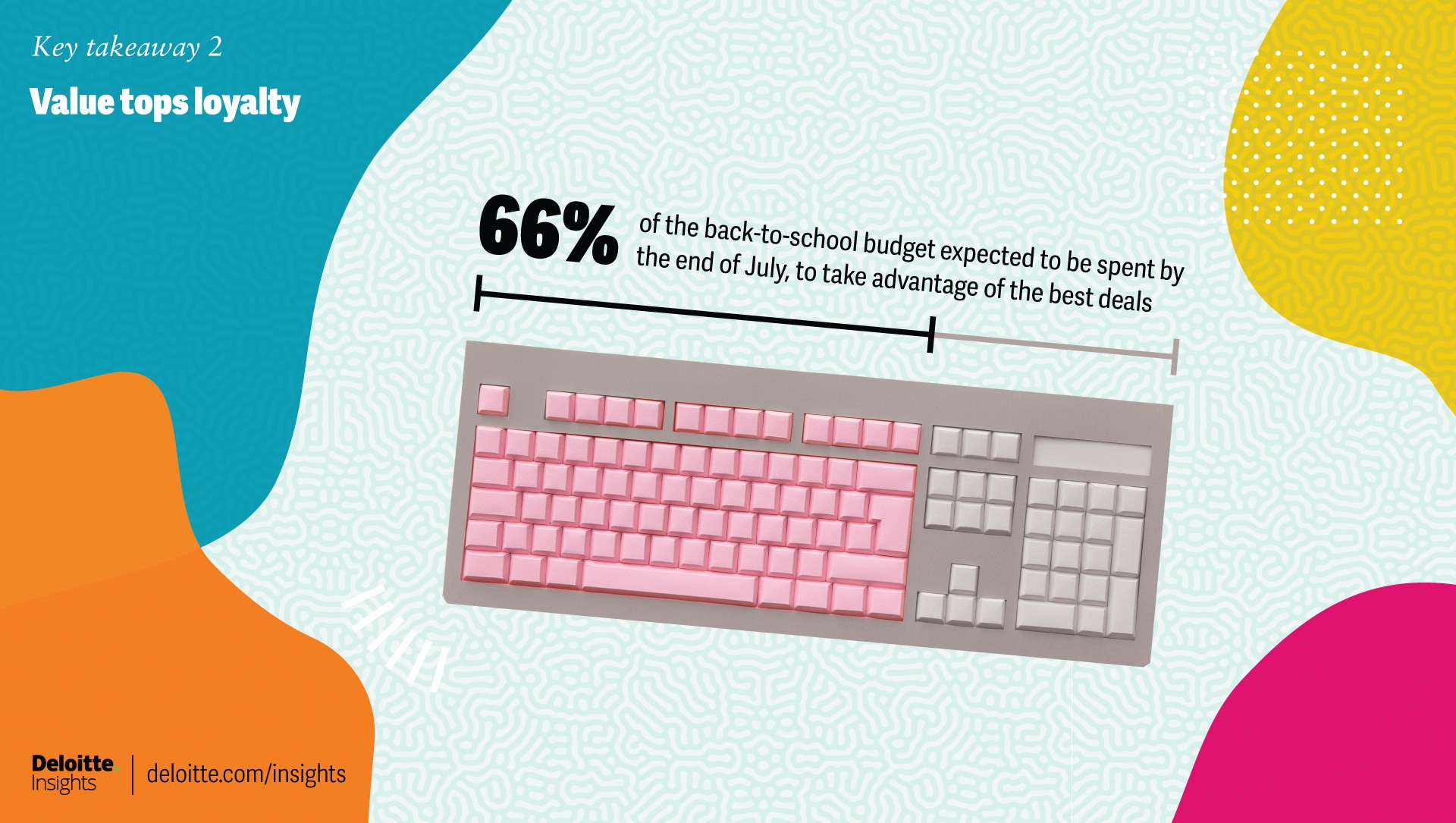

Value tops loyalty

Consumers surveyed are prioritizing value over loyalty, by shopping earlier to find the best deals (66% of the budget is expected to be spent by the end of July versus 59% in 2023), shifting to private label (50%), and shopping at more retail formats to find the best deals (4.7 versus 3.9 In 2023).

What’s in it for retailers

With the shopping season continuing to be pulled forward, retailers should consider messaging and promoting early on digital channels, as early shoppers spend 1.5x more than late shoppers and frequent digital formats more often. And while highlighting value early on will likely be important, retailers should also consider messaging how they plan to make the shopping journey easy, given shoppers prioritize convenience as well.

Four in 10 parents (across income groups) are expected to purchase a used or refurbished item this season, indicating the growing popularity of circularity. Retailers that can expand circular assortments and messages around the benefits of buying through a trusted source may be able to hedge against the growing popularity of peer-to-peer marketplaces.

Splurging for the right reasons

Despite parents focusing on necessities, 85% of respondents said they could be influenced to splurge on a must-have item or brand to make the start of school exciting or help boost their child’s self-esteem. In addition, 50% said they plan to purchase something for themselves, offering retailers opportunities to secure add-on sales.

What’s in it for retailers

With 61% of parents surveyed saying that their children influence them to spend more, retailers should consider engaging children in the shopping journey. By creating a fun and memorable shopping experience for children, retailers could increase their appeal to parents and encourage higher engagement.

Further, parents who shop for themselves while shopping for their children are likely to spend 1.4x more compared to others who don’t shop for themselves. Retailers should note that parents who shop at apparel stores for back-to-school items may be persuaded to shop for themselves too.

{kind=link}

{kind=link}

{kind=link}