{kind=link}

{kind=link}

{kind=link}

How remote work is influencing what we buy has been saved

The authors would like to thank Marcello Gasdia for his contribution to this article.

Cover image by: Sylvia Yoon Chang

Most of us can recall a few ways the pandemic changed our buying behavior—particularly in the early days. What remains elusive is the pandemic’s long-term impact on consumer behavior.

At this point, it’s unlikely the pandemic will ever have some definitive end. But with each passing month, it becomes a bit easier to see how this global experience may have changed daily life for good. Remote work is among the strongest examples. Nearly two years into the pandemic, and news headlines are still riddled with delayed return-to-office announcements and new hybrid work commitments.1 Some companies aren’t asking employees to come back at all.2

In a relatively short span of time, the physical location where hundreds of millions of people around the world spend their time changed dramatically. And just as the early days of the pandemic proved our buying behavior is a product of our environment, we are interested in how the shift to remote work might influence what we buy in the long term.

To explore this relationship, we tapped into our ConsumerSignals, bringing together data on people’s remote-work behavior and spending intentions across more than a dozen product categories and 23 countries.

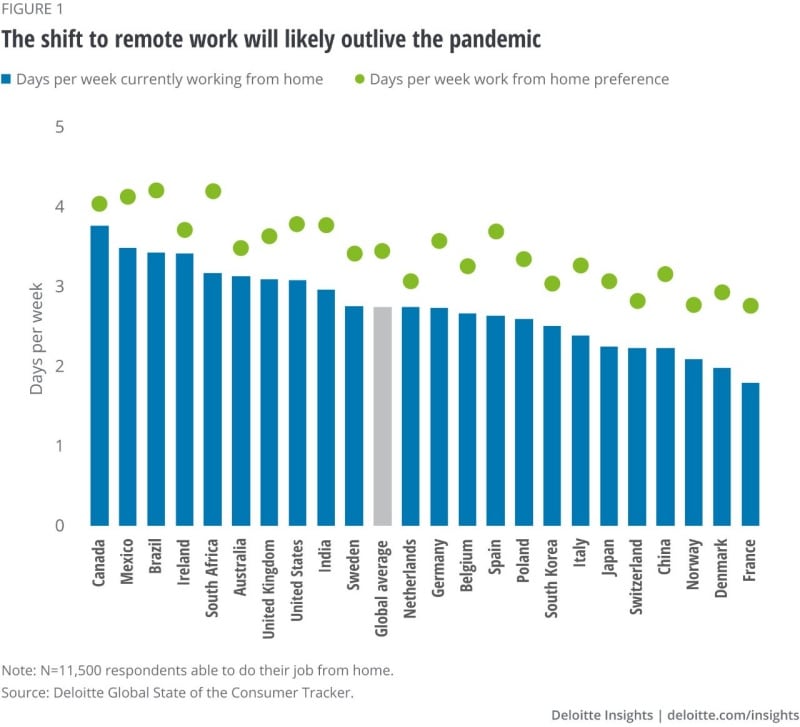

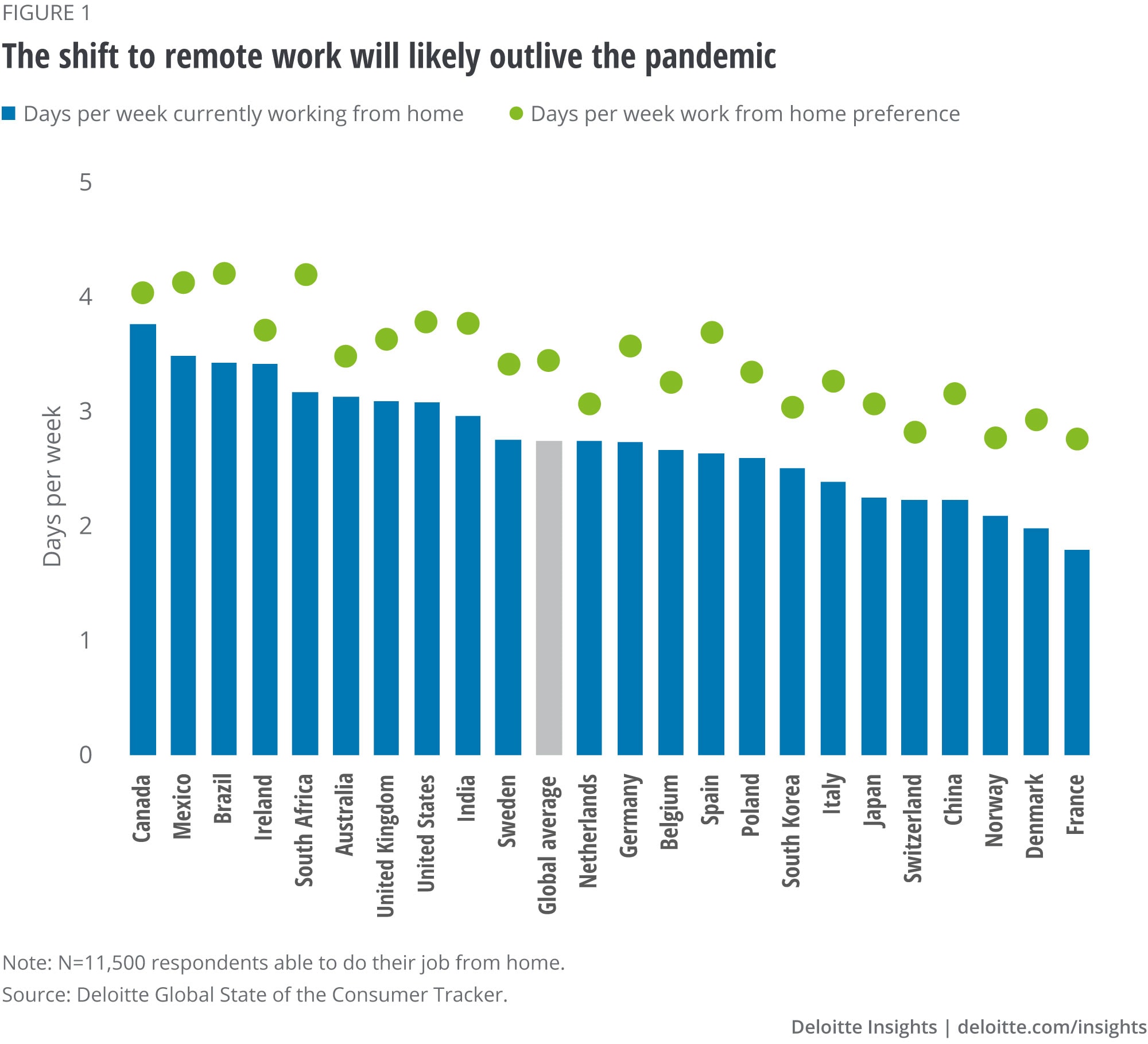

Our analysis of the data strongly suggests the shift to remote work will outlive the pandemic (figure 1). Globally, half of all employed adults (53%) say they can do their job remotely. Among them, working from home represents most of the typical work week—an average of 2.7 days.

In Canada, Australia, the United Kingdom, and the United States, people are spending closer to three or four days a week working from home. In France, Denmark, and Norway, this number is closer to two—suggesting the pace of return to office and hybrid work remains uneven globally.

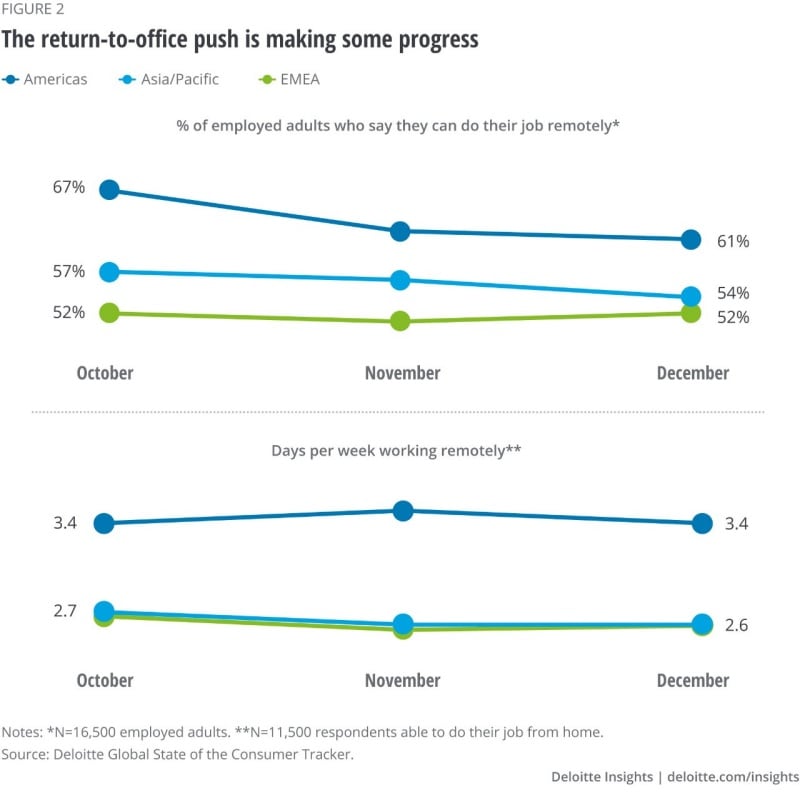

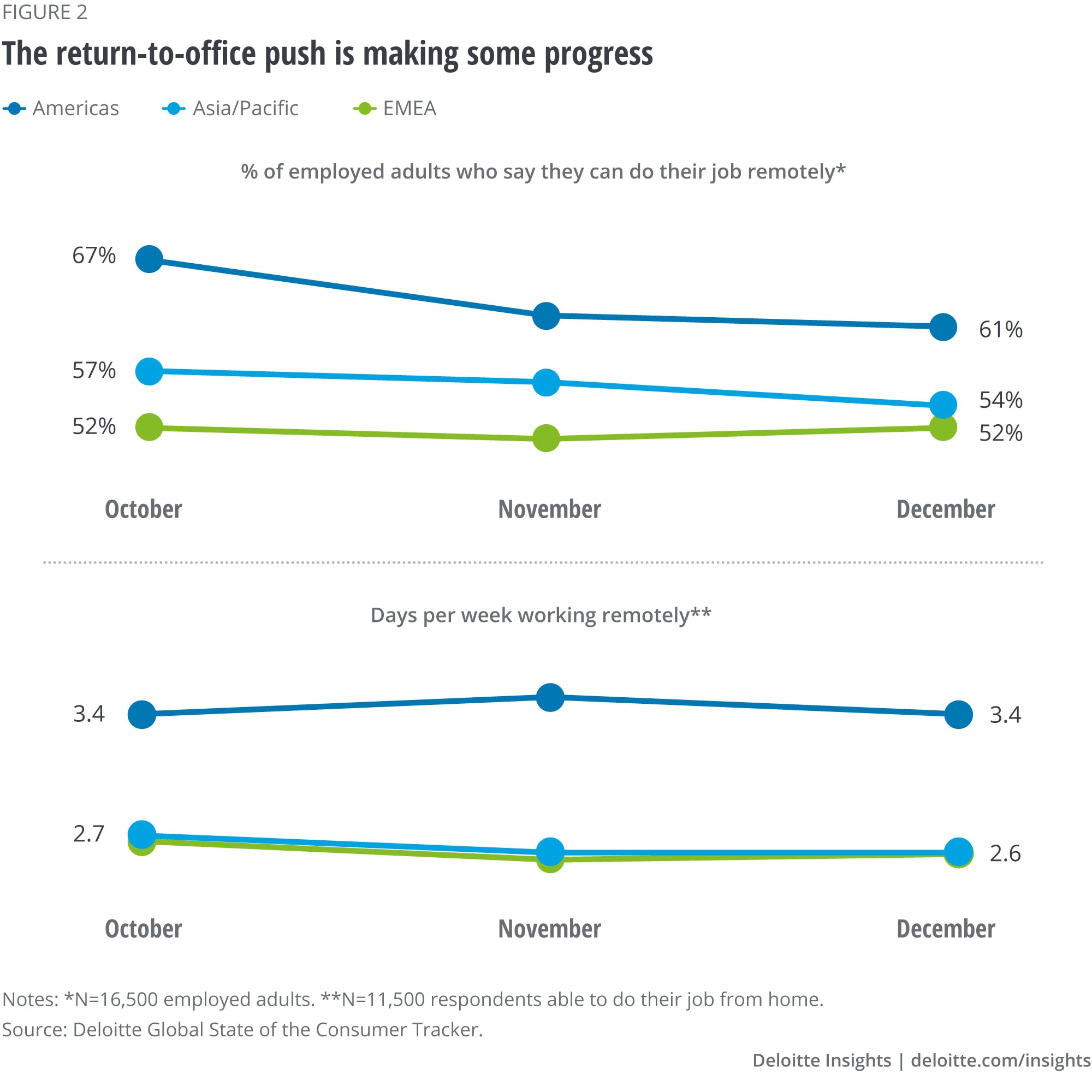

While levels of remote work remain high, there is some evidence that the ongoing return-to-office push is making some progress. In the United States, for example, the percentage of employed adults who say they can work remotely has dropped from 64% to 51% since October (figure 2). This rate of return is similar to recently published3 office occupancy data across the top 10 cities in the United States. And since November, the average number of days per week spent working from home has dipped from 3.5 to 3.1. Globally, however, these behaviors haven’t changed much over the past few months.

If any single metric hints at the longevity of remote work, it’s people’s work preferences. In all 23 countries studied, those who can work from home would prefer to spend 3.5 days on average working remotely or 0.8 days more on average than they currently do (figure 1).

Additional signals also suggest a return to office will continue to clash with evolving work preferences.

Remote work is likely to stick around. This makes its potential impact on our spending behavior all the more important.

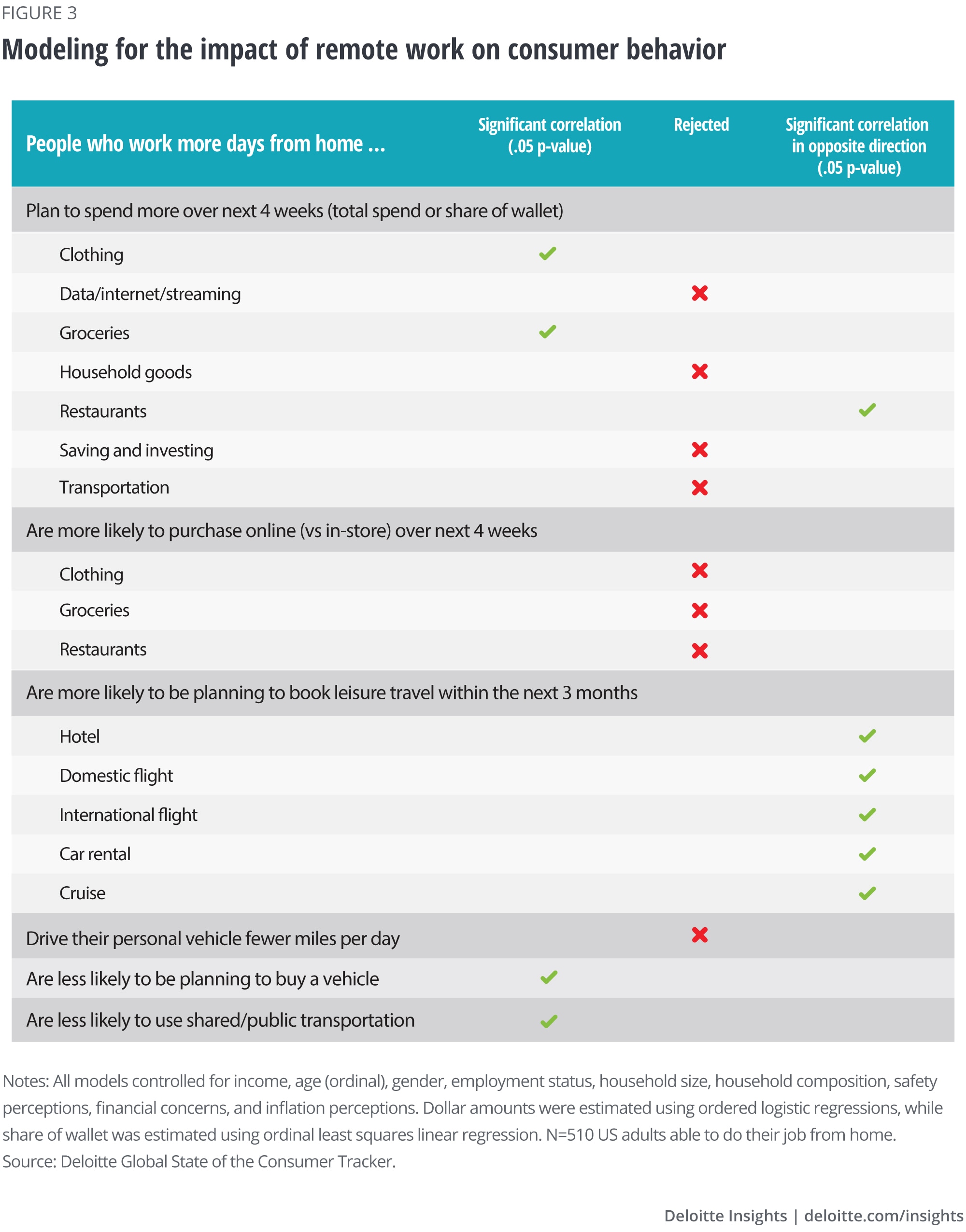

Using multivariate models to control for income, age, household composition, and more, we tested how spending behavior changes as days spent working from home increase. For the analysis, it was useful to focus on a single country. As a large economy near the global remote-work average, we analyze the United States.

The model summary in figure 3 reveals several statistically significant relationships.

The world is eager to understand what pandemic-driven changes, especially behavioral changes, might become permanent. As the months pass, it’s growing more and more likely that a redefinition of the employer-employee relationship will be one of those lasting changes. We continue to watch this trend closely as well as the challenges and opportunities it presents to companies.

Changes of this magnitude, however, can’t happen in a vacuum. Our research suggests this shift toward greater employee independence and agency brings the potential to cause a ripple effect across consumer industry.

Successful businesses will likely be those with the agility to evolve with these shifting work preferences. These shifts in consumer behavior can bring strategic opportunities to adjust product portfolio mixes and routes-to-market, tweak operating models, and take a fresh look at profit contributions.