{kind=link}

{kind=link}

{kind=link}

{kind=link}

Europe’s tech industry plugged in for cross-industry success has been saved

The authors would like to thank Paul Lee and Ben Stanton of Deloitte UK for their contributions to this article.

Cover image by: Rovinya Sollitt.

Germany

Germany

Germany

Germany

The technology industry is an essential economic factor for Europe, representing sales of €1.5 trillion and more than 8% of European economic output. Even during the COVID-19 pandemic, the industry’s gross output continued to increase.

European technology has, for example, become indispensable to the digitization of automotive and mechanical engineering, and has offered sizable support to many other industries. This has led to unique digitization priorities: Unlike in the United States or Asia, the tech industry in Europe relies less on large software and online groups, instead fostering symbiotic relationships with traditional industries.

As European technology companies have turned industrial digitization into sales growth, they have faced stiff global competition in other areas. This is especially true in the hardware segment, whose production has decreased dramatically across Europe. The result has been sometimes painful but ultimately successful evolution: Today, there is a much stronger focus on the software and services industry segment, which now accounts for two-thirds of industry revenue (a reverse from the positions those segments occupied two decades ago).

Deloitte’s research informing this report answered key questions about the European technology industry: Where does it stand today? With which other industries/sectors are the economic interdependencies in Europe particularly strong? And last, but not least: Will the strong growth continue, and what’s driving it?

We conducted a model-based simulation to quantify and forecast European technology industry sales. Input-output analysis identified interdependencies among various sectors. This and the corresponding qualitative analysis, based on expert interviews, found that: Until the end of the decade, the European technology industry is expected to grow at more than 5% every year.

Driving that will be powerful, resilient trends, such as artificial intelligence (AI), new Internet of Things (IoT) business models and additional “as-a-service” business models. Even geopolitical tension, including the Russia-Ukraine war, seems unlikely to slow growth significantly in the long run. But success is no guarantee. Six essential steps can help companies focus and strategize now to support growth, clearing the course for long-term upward trend.

There is no generally accepted or consistently used technology industry definition. The industry is sometimes interpreted narrowly and sometimes broadly, meaning that the market-size figures from relevant sources vary (in some cases quite significantly), depending on the underlying definition.

The analysis and figures presented in this report are based on the segments “Hardware” (code 26) and “Software and services” (codes 62 and 63) according to ISIC, Rev.4 classification (International Standard Industrial Classification of All Economic Activities). The main industry segments of computer hardware, semiconductors, communications equipment, consumer electronics, IT services, and data processing and hosting are thus included.

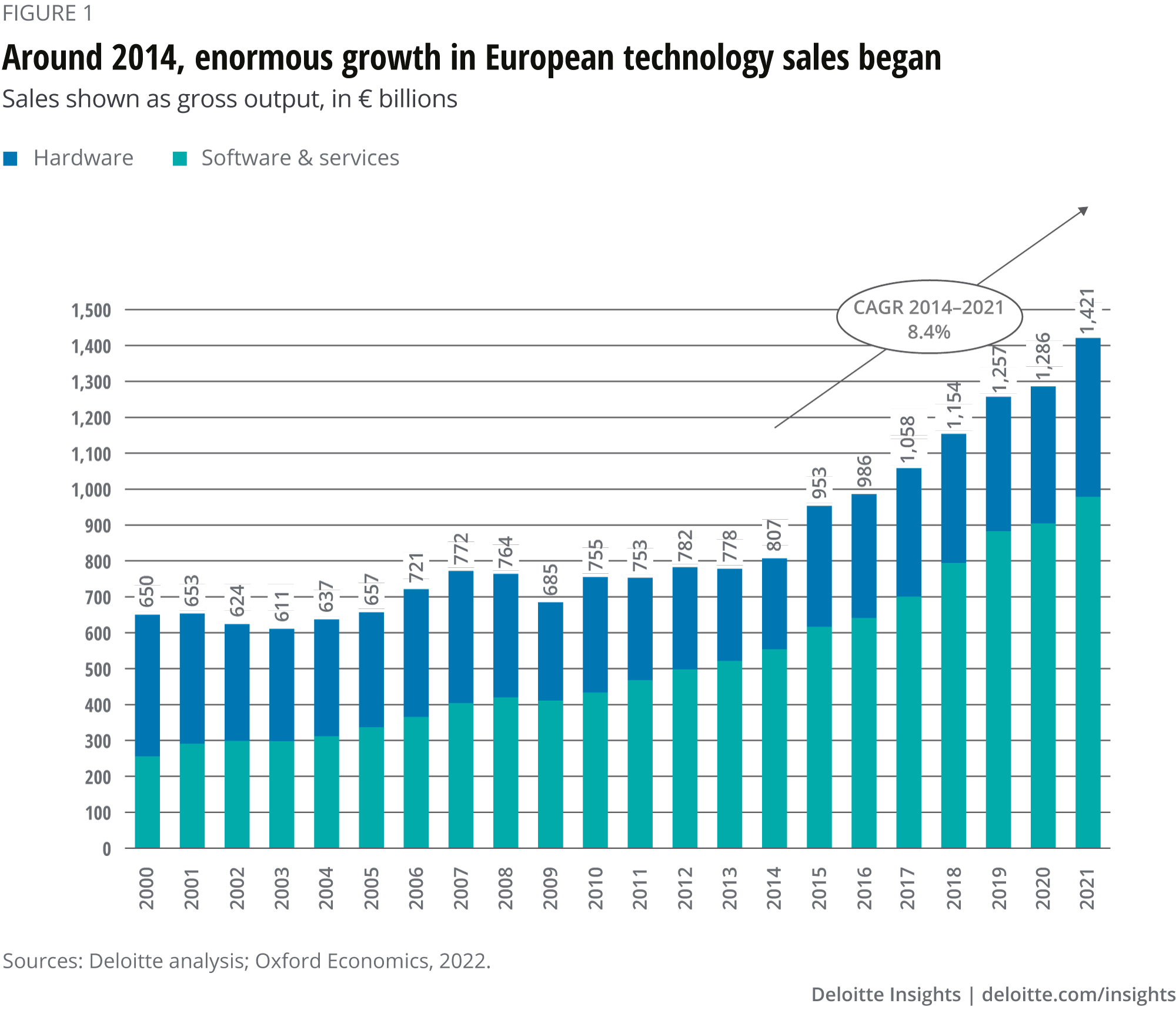

Technology was a solid, but slow-growing, industry in Europe1 for the first 13 years of the millennium. Since then, growth has been strong and continuous, at a compound annual growth rate (CAGR) of 8.4% between 2014 and 2021, equivalent to 84% growth in that period. Figure 1 shows that growth by key segment (software and services, and hardware).

The strong increase since 2014 is explained by the accelerating digitization of processes and business models—in both the B2B and B2C worlds. Consider developments such as faster and ubiquitous internet, or new media-streaming offerings: These have transported consumer services into the digital age, with positive effects on technology sales.

At the same time, technology has become an essential element of business models outside the tech industry; numerous digital growth areas have emerged at the intersection of technology and other industries. For example, take the evolution of Industry 4.0: For connected cars, or FinTech, the expertise and services of tech companies have become indispensable.

The tech industry’s very stable growth is evident in its performance as the pandemic emerged: It was one of just seven industries/sectors in Europe to grow in 2020. Only pharmaceuticals, mining, the public sector, health care and social work recorded higher or similar growth rates. And in 2021, technology sales continued to surge.

Looking back at the sales evolution over the past 20 years, it is striking to note the shift in emphasis away from hardware and toward software and services. At the turn of the millennium, hardware accounted for 61% of technology sales. By 2021, it was only 33%. These figures illustrate the fundamental change that the European tech industry has undergone, as the importance of the two key segments exactly reversed over the past two decades.

Software and services revenue has almost quadrupled since 2000. Here, too, digitization is the trigger.

The demand for digital services has not only heavily amplified the demand for various software—the need for IT services has risen sharply amid the increasingly large number of digital solutions, many of which present complexity. Especially in the past decade, demand has been driven by technological improvements in such areas as data analytics; software and services have become highly economically relevant.

By contrast, the hardware segment’s importance declined significantly, particularly in the years up till 2014. During that period, sales actually dropped year-on-year in some cases. The reasons were manifold: a sustained drop in prices for numerous hardware categories, the loss of importance of traditional consumer electronics, and Asian countries (such as China and Vietnam) adding talent, infrastructure and, most importantly, scale that achieved efficiencies not possible in Europe. The result was very modest European hardware growth—barely able to benefit from the digital megatrends.

But there are signs of a trend reversal in the hardware segment. Since the start of the European tech boom in 2014, hardware’s share of tech sales has stopped shrinking. On the contrary, it has crept up by two percentage points over the past seven years. The reason stems from the big gains in software and services, which require corresponding hardware. The stabilization of the hardware segment in the recent past can also be explained by companies having successfully found new future-proof fields of activity: reorienting themselves from consumer hardware to the B2B segment.

Technology is no longer a monolith. Instead, its success is closely linked to digital offerings from other industries. What is particularly attractive for the technology industry is that these areas of intersection are important macroeconomic growth drivers: of commitment, hope for the future and a lot of investments. Examples include smart cities, FinTech, connected cars, and digital health services.

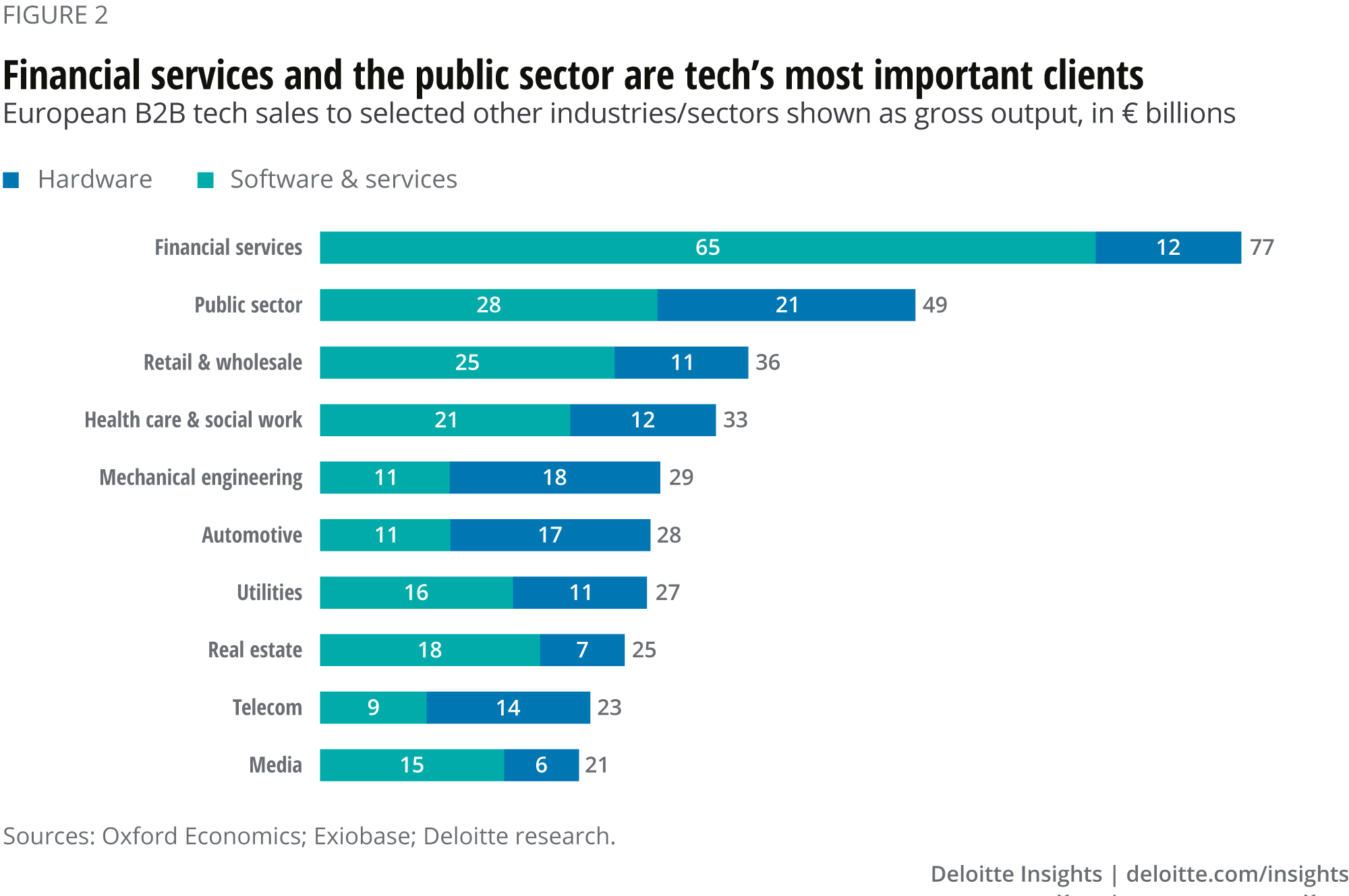

Where are the strongest interdependencies between technology and other industries in Europe? The sales numbers in figure 2 illustrate the results of our input-output analysis and show that the financial services area plays a special role for European tech companies—no other industry/sector generates more revenue. Demand from the public sector is also considerable, but significantly lower. Sales to the mechanical engineering and automotive industries rank in the middle range.

In examining the proportion of hardware to software and services sales at the industry level, significant insights come to light. In financial services, software and services clearly dominate; the now predominantly electronic payment transactions, and the widespread use of online and mobile banking, require corresponding software solutions and consulting services.

Given the high complexity of digital offerings from the financial services sector, software and services will continue to generate high revenue. The recent situation is similar with the retail-and-wholesale industry, and in health care and social work: Sales of software and services dominate, fostered by a rise in the number of digital offerings.

The exact opposite situation exists with automotive and mechanical engineering. In both industries, technology companies are supplying more hardware components than software and services. For mechanical engineering, an orientation toward Industry 4.0 is driving a demand for sensors, cameras, and robots, for example, which are boosting hardware’s share of sales. The automotive industry requires similar hardware components—to implement assisted driving, in-vehicle connectivity and infotainment, and other innovations.

Up to 2030, industry convergence will continue to gain importance. The digitization of many industries is far from complete, and in some cases remains in its infancy. And the vertical growth areas mentioned above have only exploited their potential to a small extent. A look at Asian markets, for example, illustrates how extensively public administration or health care can be digitized. Moreover, smart cities, autonomous driving, and certain other trends cannot be stopped—to the benefit of European tech companies.

The European technology sales growth of recent years is a real success story, especially when measured against the numerous changes and challenges in the industry. But inevitably there is a question of whether the positive trend is set to continue at a similar rate, leading up till 2030. And which megatrends will drive growth in Europe’s tech industry?

From today’s perspective, we identified six megatrends that will fuel the industry’s growth until the end of this decade. Many of these are globally relevant drivers, but others are very Europe specific, such as the resettlement of critical hardware production. Rather than representing abstract visions of the future, these megatrends are already making a tangible, real, and direct impact—with one exception.

1. Interconnected life and business

Across Europe, the number of “connected” objects have exceeded the 1.5 billion mark. According to Deloitte’s calculations, that figure is likely to almost double by the end of this decade. The enormous potential of IoT is clear, and it reaches far beyond primary communication devices, such as smartphones or laptops. New cross-industry business models are emerging and pushing up the demand for corresponding software and hardware solutions.

5G and fiber infrastructures are important enablers. Thanks to short latency times and high reliability, the new generation of networks will make possible even more sophisticated IoT services, such as assisted driving or aspirational digital health care (remote diagnoses, for example). Fixed wireless access (FWA) will also have a major impact in this context, providing high-speed internet to many poorly connected places and people in the coming years. The technology industry is expected to benefit significantly: not only supplying the hardware for the new network infrastructure, but also contributing strengths in software and services implementation.

2. Analytics and AI

Our interconnected life and business will keep generating a significantly increasing volume of data in the coming years. As a result, the importance of analytics and AI will continue to grow. The precise analysis of data is valuable for society, companies, and consumers alike.

The potential for wide-ranging benefits can be seen in AI-supported diagnosis of X-ray images, or in enabling predictive maintenance or targeted advertising, for example. With the intelligent control of traffic flows, AI can even lead to significant energy savings and reduction is costs and climate impact. European companies from various industries are developing and implementing such highly specific use cases, and technology is an indispensable component of the solutions. Tech companies in general, and the software and services segment in particular, are key players in this context.

3. XaaS

Numerous business models have already undergone radical change. Providers are increasingly focused on offering a prespecified and guaranteed service, rather than the one-off sale of a corresponding product. Especially in the technology industry, as-a-service (XaaS) business models have become common practice.

Tech companies have a knowledge-and-experience advantage here, from which they will profit enormously. This is because XaaS will continue to gain importance and become an important factor in establishing innovative technologies. As an example, “AI-as-a-service” will contribute significantly to the spread of AI and also make it accessible to small- and medium-sized companies.

4. Digitization booster COVID-19

The COVID-19 pandemic further stimulated and accelerated digitization processes around Europe. Implementing many of the measures takes time and will have a positive impact on technology sales until the end of this decade. As an example, COVID-19 has revealed a great need to catch up digitally in many fields in Europe, such as health care, education, and public administration. In addition, the pandemic has led many companies to push the digitization of processes, services, and customer communication channels.

The consumer segment has also experienced a boost from COVID-19. Consider the number of digital media subscriptions, which increased significantly in the first few months of the pandemic; in Germany, the gain was 21%.2As a result, digital media offerings and streaming have become even more popular. New offerings, such as advertising-based video on demand, will only increase the nonlinear share of media consumption time. Sales of required consumer hardware, such as connected TVs and networked audio components, will continue to benefit in the long term.

5. Questioning supply chains

Recent months have shown that global supply chains are fragile entities. Even though semiconductor production has grown rapidly, demand has been higher than the increasing supply. The European technology industry has been severely affected, as evident in the huge semiconductor supply bottlenecks. The massive shift of hardware production to Asian regions has taken its toll. In addition, the Ukraine crisis has caused additional disruptions to the supply of very specific hardware components (e.g., vehicle wiring harnesses), as well as raw material shortages (palladium, platinum, and nickel).

As a result, many European technology companies see danger in the dependence on foreign manufacturing; they want to become more resilient in global supply relationships and bring back the production of critical hardware to Europe. The hardware segment will benefit particularly but rebuilding suitable production facilities will take time. Significant impact on revenue is unlikely to become apparent before the middle of this decade.

6. Future metaverse

The buzz about the newest tech trend is peaking at the moment, but in many respects the metaverse is still a vision of the future—one that numerous tech and online corporations are investing heavily in building. It is conceivable that the metaverse will become a major revenue driver for the global technology industry by the end of the decade.

Underlying technologies, such as XR (virtual, augmented, and mixed reality) and the blockchain, require tech competencies for developing services within the metaverse. On top of that, the metaverse could help XR hardware achieve a final breakthrough, immensely boosting sales in the consumer hardware segment when more users want to experience the metaverse as a three-dimensional virtual space. Also, the industrial sector potentially benefits from the metaverse, such as through the comprehensive integration of digital twins.

Compared to the previous five megatrends, the success of the metaverse is less predictable. However, its huge potential means it should not be missing from this list.

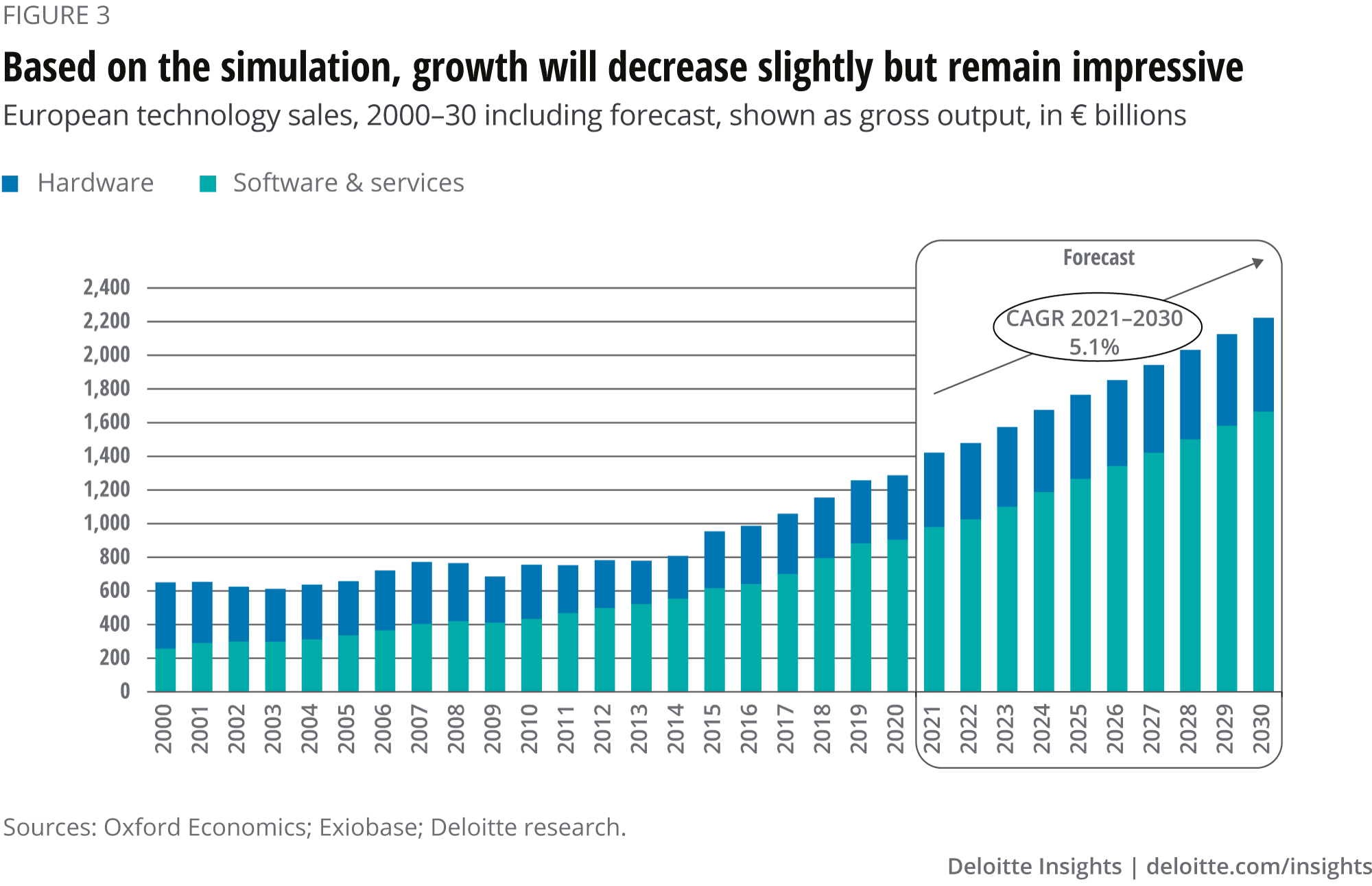

The relevance of the six megatrends already suggests that sales within the European technology industry will continue to rise. But how strong will this growth actually be? Deloitte’s model-based simulation shows: The European technology industry is expected to grow by an average of 5.1%, per year, up till the year 2030 (see figure 3). This increase is lower than the 8.4% growth in the boom phase of 2014 to 2021, but is still impressive.

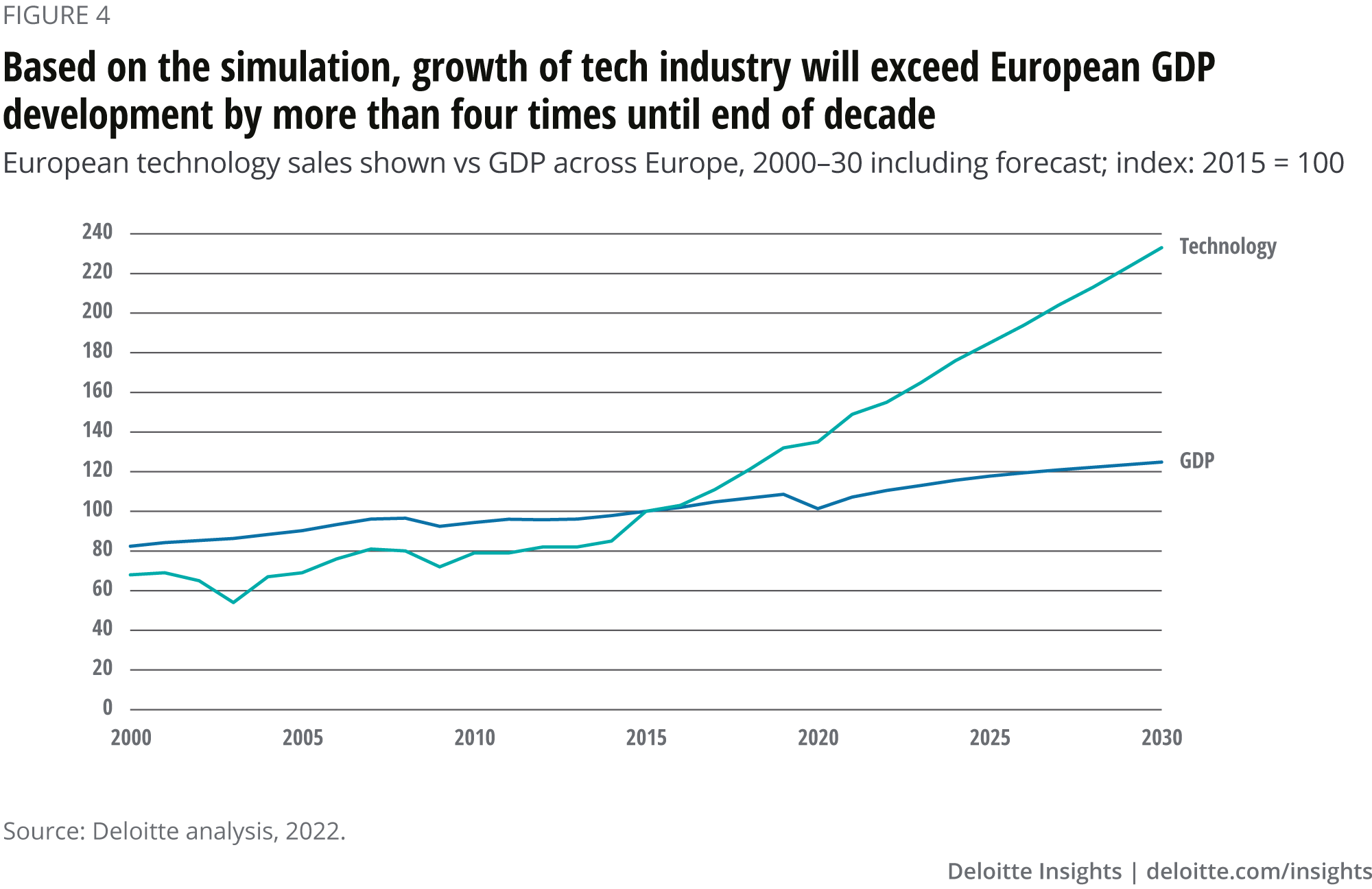

To put this growth forecast into overall economic context, we compare the long-term development of technology sales with gross domestic product (GDP). An interesting picture emerges here. The lines in figure 4 show that technology sales developed more or less in parallel with GDP until the middle of the past decade. Since then, technology has significantly outperformed GDP.

This positive trend will continue in the coming years. The growth drivers outlined above are resilient and hardly affected by the currently uncertain outlook stemming from the Russia-Ukraine war, inflation fears, and supply-chain problems. Instead, the long-term potential of the European technology industry is coming to fruition. Tech sales in Europe are expected to continue to exceed GDP significantly by the end of the decade. The already existing performance gap is about to widen even more.

In other words: Especially in difficult times, the European technology industry is a growth engine for the entire economy. And an increase of tech sales in relation to the GDP will ultimately lead to a higher significance of the technology industry in the economy. This makes tech companies in Europe not just substantial suppliers of products and services, but essential alliance and cooperation partners.

The positive outlook forms a solid basis for Europe’s technology companies to secure their position in the global tech market over the long term. But even in this tech-friendly environment, they still need the right strategies and focus. From our analysis of the economic framework data, we identified six essential steps for strengthening the European technology industry:

The analyzed data is based on statistics from the EXIOBASE Input-Output database up to 2022. EXIOBASE was developed by a consortium of several research institutes in projects financed by European research framework programmes. The database maps global industry and country links, and shows the share of intermediate products of the technology industry in terms of value added to another industry/sector. This makes visible the current interconnectedness of technology with other industries.

In addition, the input-output data and their past growth and convergence trends were combined with the latest growth figures from the Global Economics Database of Oxford Economics. The development of the European tech industry could thus be projected up to 2030. Included in the analysis is the technology sector’s share of GDP—in other words, everything that is generated in Europe (EU 27 plus UK).

The tech industry has been gaining much ground, but the longevity of its comeback is not assured. Industry leaders and decision-makers should remain focused on the actions above, especially in the face of geopolitical disruptions, a skilled-worker shortage, regulatory requirements (such as for dealing with data and AI) and the establishment of new hardware production sites. Growth has its price, and the industry must be willing to pay all costs to fully reap the benefits.